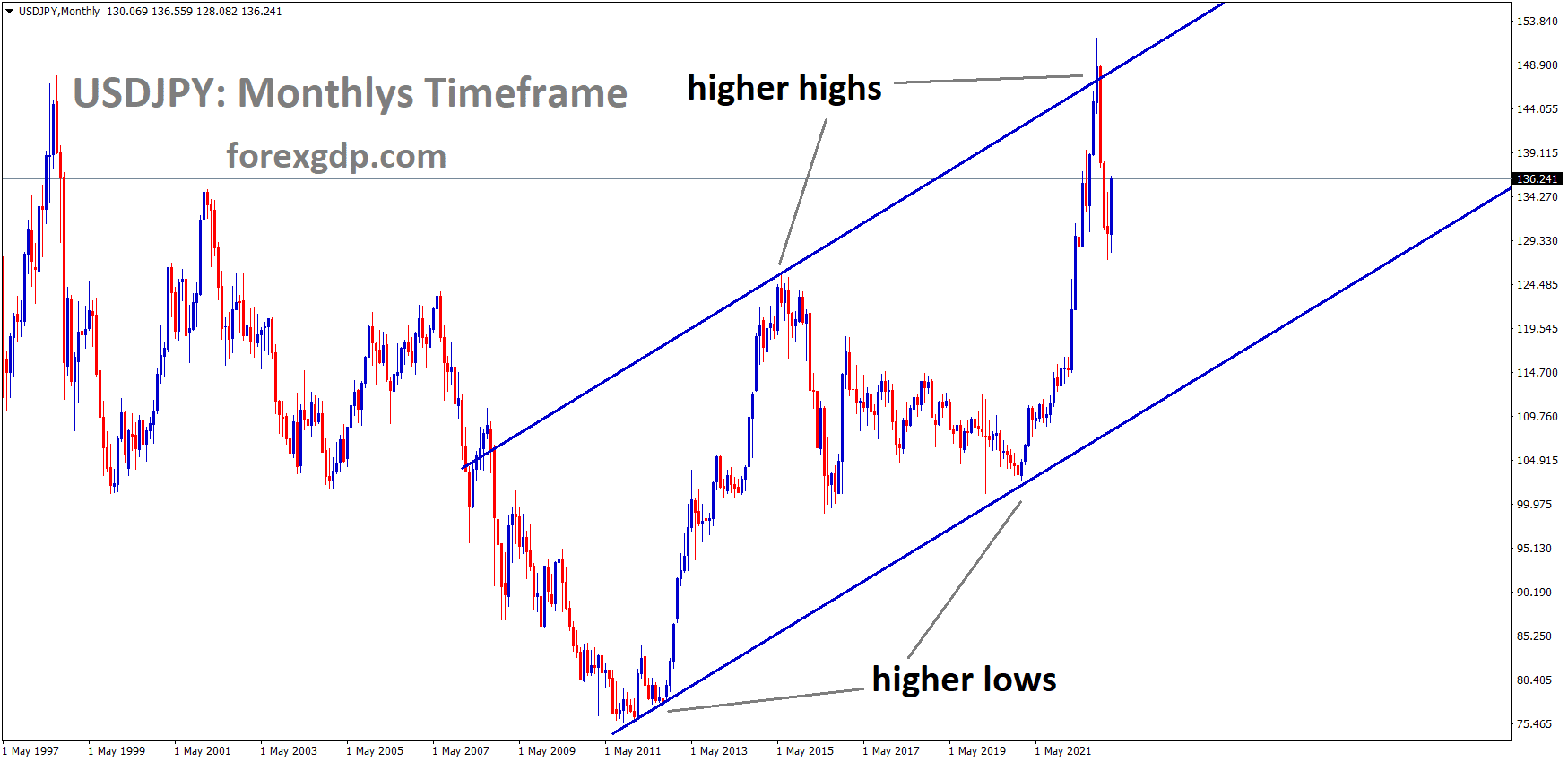

GOLD Analysis:

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel

Gold prices saw an uptick in trading following the release of better-than-expected US JOLTS Job Openings data. As the market anticipates the upcoming Federal Reserve interest rate decision today, gold prices are currently in a holding pattern, awaiting a clear direction.

Investors have tempered their expectations for an imminent Federal Reserve interest rate cut, buoyed by the robust US labor market indicated by Tuesday’s JOLTS report. This shift in sentiment has bolstered the US Dollar, exerting downward pressure on the precious metal. Nevertheless, the recent dip in US Treasury bond yields may restrain aggressive USD bullishness, given the uncertainty surrounding the Fed’s rate-cut timing. The spotlight remains on the eagerly awaited FOMC monetary policy meeting, scheduled for later today. Amidst this backdrop, persistent geopolitical tensions in the Middle East and concerns about China’s economic growth slowdown should provide some support for gold, a safe-haven asset.

The US Dollar’s resurgence is driven by reduced expectations of an aggressive Federal Reserve policy easing, causing a retreat in gold prices from their two-week peak reached the previous day. The Job Openings and Labor Turnover Survey report, released by the Bureau of Labor Statistics, unexpectedly revealed an increase in US job openings to 9.02 million in December. Furthermore, the US Consumer Confidence Index, as measured by the Conference Board, continued its third consecutive monthly improvement, surging to 114.8 in January from the previous 108.0. Additionally, the International Monetary Fund upgraded its forecast for US economic growth in 2024 to 2.1%, compared to the 1.5% expected in October, before easing to 1.7% in 2025. These developments suggest that the US economy remains robust, lending support to the notion of the Fed initiating interest rate cuts in the first quarter. Consequently, this lends strength to the US Dollar and weighs on gold. The yield on the 10-year US government bond hovers near the 4.0% mark, further reinforcing support for XAU/USD, in conjunction with geopolitical concerns and China’s economic challenges. China’s National Bureau of Statistics reported a slight improvement in the official Manufacturing PMI to 49.2 in January, though it has remained in contraction territory for four consecutive months. This signals a sluggish domestic recovery and weak external demand, partially offset by a marginal increase in the Non-Manufacturing PMI to 50.7 in January, up from the previous 50.4. Investors are now eagerly awaiting the FOMC policy decision for clues regarding the timing of the first interest rate cut, which will undoubtedly steer gold’s direction. As we approach this pivotal central bank event, traders will also keep an eye on the release of the ADP private-sector employment report and the Chicago PMI during the North American trading session.

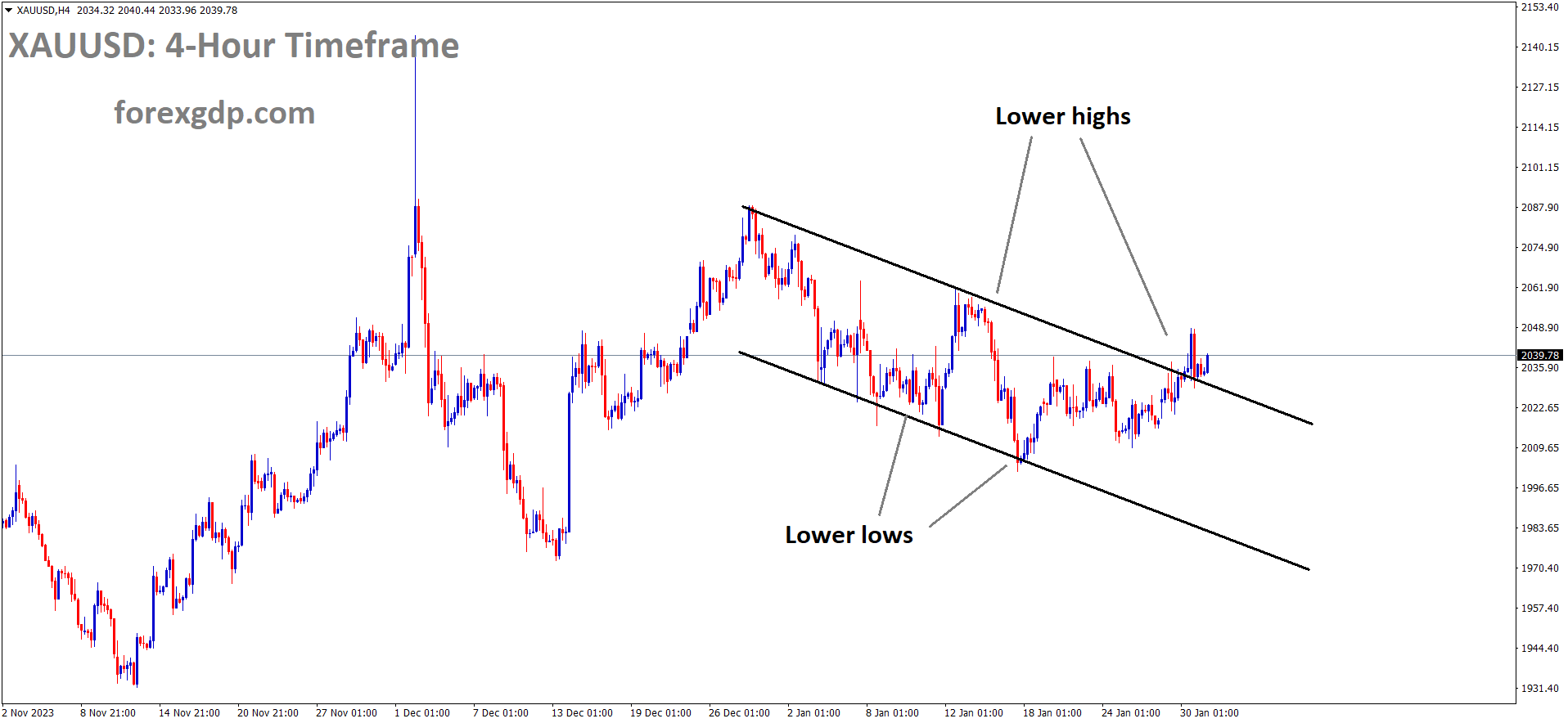

SILVER Analysis:

XAGUSD Silver price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Today, we are expecting the release of US ADP Non-Farm Employment Change data. The December report had shown a significant increase in job vacancies, contributing to the US Dollar’s strength against other major currencies.

On Wednesday, the US Dollar displayed its resilience against competing currencies, with the upcoming policy decisions from the Federal Reserve taking center stage. Following the conclusion of the January policy meeting, Chairman Jerome Powell is set to provide insights into the policy outlook later in the day. Additionally, the US economic calendar will include the release of ADP Employment Change data for January.

The cautious market sentiment observed on Tuesday contributed to increased demand for the USD during the American session. However, the currency’s gains were somewhat restricted due to declining yields. Despite closing the day with minimal changes, the USD Index gained momentum early on Wednesday and remained firmly in positive territory, surpassing the 103.50 mark. Meanwhile, the yield on the benchmark 10-year US Treasury bond managed to maintain its position above 4%, despite experiencing a more than 2% decline earlier in the week. Concurrently, US stock index futures registered slight losses, ranging from 0.1% to 0.8%.

USDCHF Analysis:

USDCHF is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern

Switzerland’s Federal Customs Administration has released trade balance figures, revealing a decrease to 1248 million, down from 3833 million. Both imports and exports experienced a decline during the month of December.

The prevailing positive sentiment in the market can be attributed to the anticipation and support leading up to the Federal Reserve’s imminent interest rate decision later today. It seems that market participants have already factored in the likelihood that the Fed will maintain its current stance in this month’s meeting. However, it’s worth noting that the CME’s FedWatch Tool suggests a 43% probability of the Federal Reserve implementing its first rate cut in March, along with a 53% chance of a 25 basis points rate cut in May.

In other economic news, Tuesday saw an improvement in the US JOLTS Job Openings for December, which reached 9.026 million, surpassing both the previous figure of 8.925 million and the expected 8.7500 million. Meanwhile, the US Housing Price Index held steady at 0.3% in November. Investors are keeping a close eye on the upcoming release of US ADP Employment Change data scheduled for Wednesday. This data is often considered a precursor to the more comprehensive US Nonfarm Payrolls report set to come out later in the week. Shifting our focus to Switzerland, the Federal Customs Administration released December’s Imports report, which indicated a decrease from 20,454 million to 17,551 million. Exports also declined from 24,287 million to 18,798 million, resulting in a reduced Trade Balance of 1,248 million from 3,833 million. Notably, SNB President Thomas Jordan recently expressed uncertainty regarding the Swiss National Bank’s stance on the persistent strength of the Swiss currency. Traders will be keenly watching Wednesday’s Real Retail Sales and the ZEW Survey to gauge the overall health of the Swiss economy.

CADCHF Analysis:

CADCHF is moving in the Descending channel and the market has reached the lower high area of the channel

The Canadian Dollar experienced an upward trajectory against other currencies, buoyed by heightened anticipations surrounding the forthcoming Canadian GDP data for November. This optimism comes in the wake of the Bank of Canada’s recent statement, indicating a slowdown in Canada’s economic growth since mid-2023, with expectations of a flat 0.0% growth in the first quarter of 2024.

The currency pair’s rebound is buoyed by positive developments in the United States, notably the robust job openings and consumer confidence data, which have given a boost to the US dollar. All eyes are now on the forthcoming Federal Reserve monetary policy meeting scheduled for Wednesday, where no changes in interest rates are anticipated. In a surprising turn, data from the Bureau of Labor Statistics revealed that the number of available jobs in the US increased unexpectedly in December, reaching 9.026 million. This marks the first time that job openings have surpassed the 9 million mark since September. Furthermore, the Conference Board Consumer Confidence index for January climbed to 114.8, up from the previous reading of 108.0, marking its highest level in two years.

As anticipation mounts for the Federal Reserve’s interest rate decision, investors widely expect the central bank to maintain the federal funds rate within the established range of 5.25% to 5.5%. Following the conclusion of the Fed meeting, all ears will be tuned to Fed Chairman Jerome Powell’s press conference for any hints regarding the timing of potential rate cuts. Shifting focus to Canada, Statistics Canada is set to release the Gross Domestic Product data for November, with a forecasted expansion of 0.1% month-on-month. This release comes on the heels of the Bank of Canada’s recent announcement, indicating that Canada’s economic growth has stagnated since mid-2023 and is likely to remain near zero in the first quarter of 2024. Persistent core inflation readings prompted the Bank of Canada to maintain its interest rate at a 22-year high just last week. Meanwhile, the Loonie, Canada’s currency, may find support from elevated oil prices due to ongoing geopolitical tensions in the Middle East. Looking ahead, the Canadian GDP growth figure is scheduled for release on Wednesday, coinciding with the Federal Reserve’s monetary policy meeting and Powell’s press conference. The week will conclude with a close watch on the US Nonfarm Payrolls report on Friday, a significant event that will capture the attention of market participants.

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

In December, German retail sales data showed a notable increase of 1.6%, marking a significant improvement compared to the previous month when it had declined by -2.5%. Following the release of this data, the Euro currency exhibited a slight weakness in its performance.

In December, Germany’s retail sales took a dip, marking a 1.6% month-on-month decrease, which was less severe compared to the 2.5% decline experienced in November. These figures, released by Destatis on Wednesday, came as a surprise to the market, which had anticipated a 0.7% increase. On a year-on-year basis, retail sales in Germany’s robust economy declined by 1.7% in December, a slight improvement from the 2.4% annual drop seen the previous month.

The data, provided by Statistisches Bundesamt Deutschland, serves as a valuable gauge for tracking shifts in the German retail sector’s sales. It offers insights into the sector’s short-term performance, with percentage changes reflecting the pace of these sales alterations. This information holds significance as it provides a glimpse into consumer spending trends. A positive economic outlook typically favors the EUR, while a lower reading is viewed as detrimental to the EUR’s strength.

EURCAD Analysis:

EURCAD has broken the Box pattern in downside

ECB President Lagarde emphasized that any potential rate cuts would be entirely dependent on data. She stressed the importance of wage data as a critical factor influencing future decisions in the market. Lagarde also made it clear that there is no set timeline for rate cuts at this moment.

On Tuesday, Christine Lagarde, the President of the European Central Bank, held discussions with CNN, shedding light on the central bank’s stance on interest rates and the role of wage data in its monetary policy decisions. Lagarde refrained from providing a specific timetable for potential interest rate cuts, but she made it clear that wage-related data would play a crucial role in shaping the ECB’s approach to monetary easing. She emphasized that before considering any rate reductions, it is essential for the central bank to see further progress in the disinflationary process. The disinflationary process refers to a period in which the inflation rate is declining or slowing down, potentially leading to deflationary pressures. Central banks often employ monetary policy tools, including interest rate adjustments, to counteract these trends and maintain price stability. Lagarde’s statement that the next move will be a cut suggests that the ECB is leaning towards implementing a rate cut as its next monetary policy action. However, she made it clear that this decision would be contingent on specific economic indicators, particularly wage data. Wage data is a critical economic indicator because it provides insights into the earning capacity of the workforce. Rising wages can contribute to increased consumer spending and inflationary pressures, while stagnant or declining wages may indicate economic challenges and disinflationary forces.

By highlighting the importance of wage data, Lagarde indicated that the ECB is closely monitoring the labor market and income trends to gauge the overall economic health of the Eurozone. A thorough assessment of these factors will guide the central bank in determining the appropriate timing and magnitude of any potential interest rate cuts. In summary, while Christine Lagarde did not provide a definitive timeline for interest rate cuts, her remarks underscored the ECB’s commitment to maintaining price stability and its readiness to use monetary policy tools as needed. The central bank’s decision to reduce interest rates will be based on a careful evaluation of economic data, with a particular focus on wage-related indicators.

GBPUSD Analysis:

GBPUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel

The UK economy is grappling with mounting inflationary pressures, causing concerns among the populace as inflation deviates from the target level of 2%. In response, The Bank of England is striving to maintain interest rates at a steady level during this week’s meeting to address these challenges.

The Pound Sterling finds itself in a cautious position as Wednesday’s European morning unfolds, with the looming US Federal Reserve’s monetary policy meeting adding to the uncertainty. Market sentiment leans towards the expectation that the Fed will maintain interest rates within the range of 5.25% to 5.50%. However, the primary focus shifts to any guidance provided by the central bank regarding the potential timing and pace of interest rate cuts. During the Fed’s previous monetary policy meeting, they had projected a reduction of 75 basis points in interest rates for 2024. Currently, the Pound trades in a relatively sideways fashion, with market participants anticipating more defined movements after both the Fed and the Bank of England announce their initial monetary policy decisions for 2024. The BoE, much like the Fed, is expected to maintain the status quo, continuing the trend for the fourth consecutive time. While the UK’s economy has experienced peak price pressures, investors remain uncertain about inflation returning to the 2% target on a sustainable basis. In addition to the Fed’s decision, market volatility is anticipated to increase later in the day as investors turn their attention to the US Automatic Data Processing Employment Change data for January. This will be followed by the Institute of Supply Management Manufacturing PMI and the Nonfarm Payrolls data. The prevailing mood in the market is characterized by caution ahead of the Federal Reserve’s interest rate decision. Expectations lean towards the Fed maintaining the status quo, suggesting no immediate need for a dovish signal given that US inflation remains distant from the desired 2% target. Progress in achieving this target has slowed, as strong labor market conditions, robust consumer spending, and overall economic growth continue to support the US economy.

Further developments in the Pound Sterling will also hinge on the Bank of England’s forthcoming monetary policy decision, set to be announced on Thursday. Similar to the Fed, the BoE is anticipated to maintain the current interest rate of 5.25%. While the expectation is for an unchanged monetary policy, market participants will be closely monitoring any indications regarding the future interest rate outlook. Unlike the Federal Reserve and the European Central Bank, the Bank of England has not engaged in discussions about the timing or extent of interest rate cuts in 2024. Consequently, any discussions surrounding potential rate cuts would be viewed as bearish for the Pound Sterling. The rationale behind the BoE’s emphasis on maintaining interest rates at their current levels is rooted in elevated inflation, which exceeds that of other Group of Seven economies. However, the possibility of sluggish economic growth may force the BoE to reconsider its stance. The Lloyds Bank Business Barometer recently surged to a two-year high of 44%, driven by hopes of softer inflation and the potential for interest rate cuts. This survey revealed that businesses are planning to expand their workforces. Meanwhile, the US Dollar Index is on the rise as investors seek safe-haven assets ahead of the Fed’s decision. Alongside the Fed’s policy decision, investors will closely monitor the release of ADP Employment Change data for January, expected at 13:15 GMT, with forecasts suggesting that US private employers added 145,000 jobs, down from the 164,000 payroll additions in December.

GBPJPY Analysis:

GBPJPY is moving in the Descending channel and the market has reached the lower low area of the channel

The Bank of Japan’s Summary of Opinions reveals a hawkish tilt, causing a modest strengthening of the Japanese Yen against other currencies. The BoJ has maintained a patient stance in the market, waiting for wages and inflation to align before taking any significant action.

During the European session on Wednesday, the Japanese Yen experienced modest fluctuations, alternating between minor gains and losses when compared to the US Dollar. It remained within a relatively stable range, consistent with its performance over the past couple of weeks. Traders adopted a cautious approach, hesitating due to uncertainty surrounding the Federal Reserve’s potential interest rate cuts. As a result, the focal point of the day remained the eagerly awaited FOMC policy decision, scheduled for later in the day. This announcement was anticipated to play a pivotal role in influencing short-term price dynamics for the USDJPY pair. Adding to the dynamics, weaker-than-expected Japanese economic data was released earlier in the day, impacting the Yen negatively. Specifically, Retail Sales and Industrial Production figures for December fell short of expectations. On the other side of the equation, there was some buying of the US Dollar, driven by reduced expectations of an aggressive Fed policy easing in 2024. This factor acted as a tailwind for the USDJPY pair. Nevertheless, the Bank of Japan’s hawkish stance, ongoing concerns about geopolitical tensions in the Middle East, and China’s economic challenges provided support for the safe-haven Japanese Yen. Japanese Retail Sales for December registered a 2.1% growth, marking the 22nd consecutive month of increase but missing the consensus estimate of a 5.1% rise. Meanwhile, Japanese factory output rebounded in December, rising by 1.8% compared to November, the largest gain since June. However, it also fell short of expectations for a 2.4% growth. Japanese government officials mentioned a projected decline in January production due to a partial auto plant suspension, and they noted that the Noto earthquake had a limited impact on output planning.

In January, the Consumer Confidence Index in Japan increased to 38.0, a 0.8-point improvement over the previous month’s reading of 37.2. The Bank of Japan’s Summary of Opinions report from the January 2024 monetary policy meeting emphasized the importance of maintaining monetary easing under Yield Curve Control. The possibility of ending the negative rate policy was discussed, with some members indicating that conditions for such a move were becoming more favorable. In the realm of international finance, the director of the International Monetary Fund Asia and Pacific Department suggested that foreign exchange intervention could help reduce excessive volatility and align exchange rate movements with economic fundamentals. Additionally, the heightened risk of military conflict in the Middle East favored the safe-haven Japanese Yen, potentially restraining any significant appreciation of the USDJPY pair. An Iranian envoy to the UN issued a warning that any attack on Iran or its interests beyond its borders would trigger a definitive response. On the US front, the US Dollar garnered some positive momentum as investors adjusted their expectations, lowering the odds of an early rate cut by the Federal Reserve, given the resilience of the US economy. The latest Job Openings and Labor Turnover Survey report indicated unexpectedly increased job openings in December, with a total of 9.02 million openings on the last business day of the month. This data suggested that the labor market remained robust, potentially discouraging the Fed from initiating interest rate cuts in the first quarter. As a result of these developments, market participants reduced the likelihood of a rate cut in March to below 50%. Instead, they turned their attention to the forthcoming FOMC policy decision for guidance on the timing of the first rate cut. Additionally, the release of the US ADP report on private-sector employment and the Chicago PMI later in the day could provide some market impetus, though any immediate reactions were expected to be short-lived.

AUDUSD Analysis:

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

Australian Treasurer Jim Chalmers expressed satisfaction with the fourth-quarter inflation figures, describing them as a welcome development. However, he emphasized the importance of implementing labor cost-of-living tax cuts as a necessary measure to counterbalance the elevated rates in the market.

In response to the latest Australian inflation figures, Treasurer Jim Chalmers expressed his views today. He highlighted that the results have exceeded market expectations, marking a positive development. However, he emphasized that many individuals are still grappling with financial pressures. This underscores the significance of the Australian Labor’s proposed cost of living tax cuts for middle-income Australians. The recently released data from ABSStats indicates notable and promising strides in the ongoing battle against inflation. While government policies have played a role in this progress, Chalmers cautioned against prematurely declaring victory. He stressed that the challenges people face due to economic pressures persist and require ongoing attention.

NZDUSD Analysis:

NZDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

The ANZ Business Confidence report for January indicates a positive shift, with a reading of 36.6, surpassing the previous month’s figure of 33.2. However, the New Zealand Dollar faced downward pressure amid ongoing geopolitical tensions in the market.

Amid rising tensions, there is speculation that the Biden administration may greenlight military action in response to a recent drone attack on a US outpost in Jordan. Shifting focus to economic indicators, the ANZ Business Confidence report for New Zealand paints a mixed picture. The business outlook improved, with a rise to 36.6 in January from the previous reading of 33.2. However, the ANZ Activity Outlook showed a slight dip, registering at 25.6% compared to the previous figure of 29.3%. Meanwhile, Paul Conway, the Chief Economist at the Reserve Bank of New Zealand, has taken a hawkish stance, pushing back against expectations for rate cuts.

In his recent statement, Conway expressed cautious but optimistic views regarding the effectiveness of current monetary policy measures. On the currency front, the US Dollar Index faces challenges stemming from subdued US Treasury yields. The Federal Open Market Committee is widely anticipated to maintain interest rates within the range of 5.25% to 5.50% in its upcoming meeting on Wednesday. In the December meeting, Fed officials had projected three rate cuts for 2024. All eyes are now on Fed Chairman Jerome Powell for any signals or insights he may provide. Rate swap markets have seen a gradual extension of expectations for rate cuts, with the CME’s FedWatch Tool suggesting a 43% probability of the first-rate cut from the Fed in March. This is a notable shift from December when swaps initially implied an over 80% chance of a rate reduction in March. Additionally, there is a 53% likelihood of a 25 basis points rate cut in May. Investors are eagerly awaiting the release of the US ADP Employment Change data on Wednesday, with the US Nonfarm Payrolls report scheduled later in the week.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/