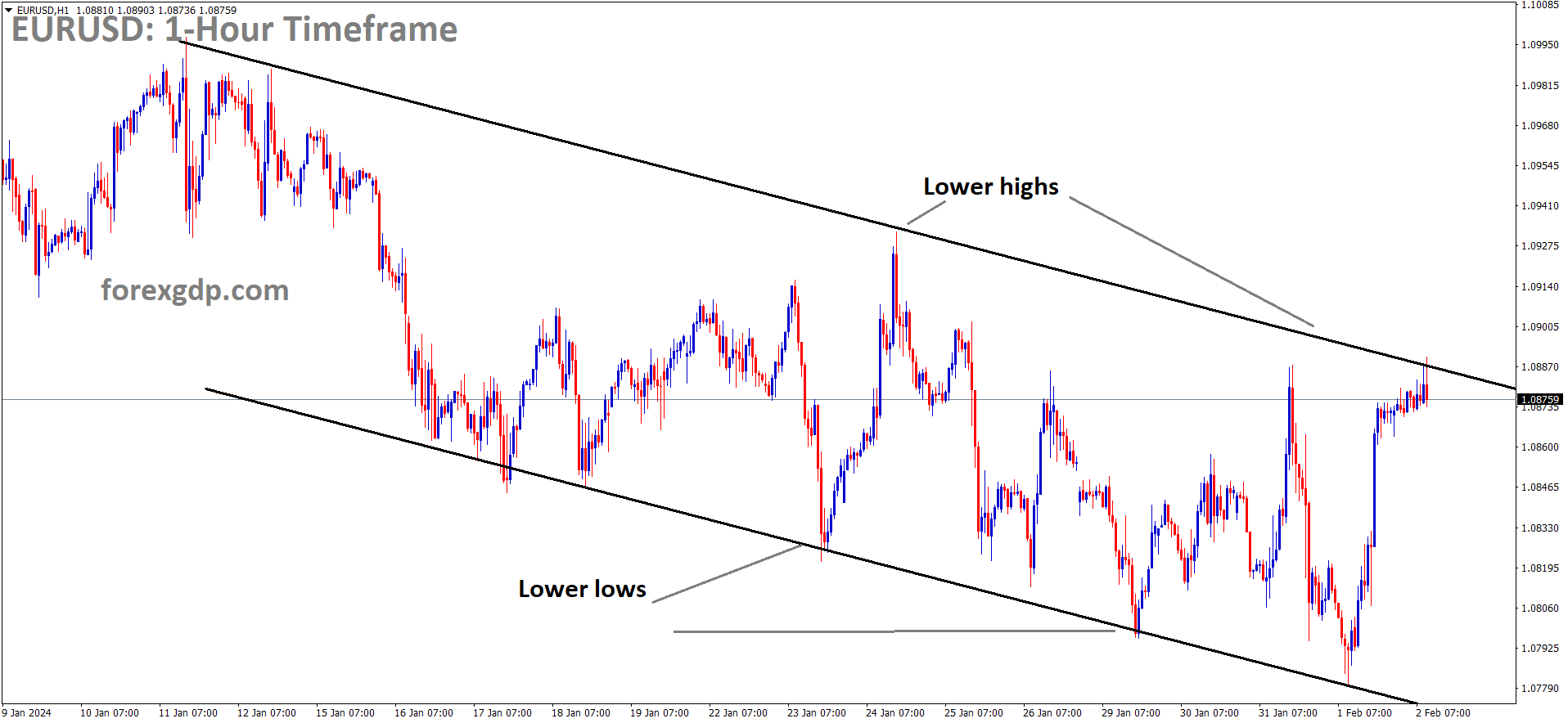

EURUSD Analysis:

EURUSD is moving in the Descending channel and the market has reached the lower high area of the channel

In January, Euro area inflation data surprised by rising to 3.3%, slightly above the anticipated 3.2%, yet marginally below the previous month’s figure of 3.4%. Interestingly, the Euro currency displayed little movement following the release of this data.

The Bank of England made a noteworthy decision by voting for both rate cuts and rate hikes simultaneously, a rare occurrence not seen since 2008. This move by UK central bank policymakers resulted in a split decision, with 6 votes in favor of no change and rate hike votes outnumbering rate cut votes by a 2-to-1 margin. As a result, the financial markets underwent significant adjustments in their expectations regarding rate cuts by the Bank of England. However, it’s worth noting that money markets still anticipate four rate cuts by the end of 2024.

Deutsche Bank witnessed a 4% increase in its shares on Thursday, following the announcement that the European bank would be reducing its back-office workforce by more than three thousand employees, equivalent to nearly 4% of its total workforce. This move is aimed at returning €1.6 billion in value to shareholders, especially after the bank’s fourth-quarter earnings experienced a 30% decline quarter-on-quarter, although this decline still exceeded expectations. The French bank also reported a QoQ sales miss but did not propose staff reductions as a means to compensate for the loss and benefit shareholders. Meanwhile, Volvo shares surged by over 25% following the announcement that it would cease funding for its struggling subsidiary, Polestar. Volvo intends to transfer control of Polestar to Geely Holding, a Chinese investment company with nearly an 80% stake in Volvo.

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher high area of the channel

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher high area of the channel

Gold prices saw an uptick in response to the unexpected increase in US Weekly Jobless claims reported yesterday. Investors are now awaiting the release of Non-Farm Payrolls data today, with future movements contingent on this crucial economic indicator.

The current market momentum is reflected in the four-hour chart, where indicators are showing signs of leveling off, approaching overbought conditions. This suggests a potential saturation in the market. On the fundamental front, market participants are eagerly awaiting the release of crucial Nonfarm Payrolls data for January, scheduled for Friday. Notably, higher-than-expected weekly Jobless Claims figures from the US had a weakening effect on the Greenback during the session.

Federal Reserve Chair Powell has expressed skepticism about the likelihood of the bank gaining enough confidence by March to begin easing its policies. Consequently, the US Dollar experienced a rally on Wednesday as market sentiment shifted away from earlier expectations of imminent rate cuts. However, it’s important to note that forthcoming data releases will play a pivotal role in guiding the central bank’s decision regarding the timing of any easing cycle. If the labor market figures released on Friday turn out to be weak, it could potentially lead to further gains for precious metals, as expectations of lower interest rates typically benefit non-yielding assets.

XAGUSD Analysis:

XAGUSD Silver price is moving in the Box pattern and the market has rebounded from the support area of the pattern

The upcoming January US Non-Farm Payrolls data is anticipated to show 180K new jobs, a slight decline from the 216K reported in December. This dip in employment numbers coincided with a temporary cessation of hostilities in the Gaza conflict, leading to a drop in the US Dollar’s value. Furthermore, the US Unemployment rate is predicted to increase to 3.8%, up from the previous month’s figure of 3.7%.

The eagerly awaited Nonfarm Payrolls data is on the brink of being disclosed by the United States. This forthcoming data release holds considerable significance for the trajectory of the US Dollar. Initial anticipations for the NFP report in the inaugural month of 2024 indicate the inclusion of 180,000 jobs, marking a reduction from the robust creation of 216,000 jobs in December. Simultaneously, the Unemployment Rate is foreseen to increment from December’s 3.7% to 3.8% for the current reporting period. Another pivotal metric to monitor is Average Hourly Earnings, which is forecasted to ascend by 4.1% over the year leading up to January, mirroring the pace observed in December.

The US labor market data plays a pivotal role in establishing the timeline and prospective rate modifications by the US Federal Reserve in the approaching year. This consideration has taken on added significance subsequent to the recent deferment of market expectations for a March rate cut. Throughout the two-day policy meeting, the Fed kept its benchmark interest rates consistent within the 5.25% to 5.50% spectrum, as was broadly projected. Nevertheless, the accompanying statement conveyed a somewhat hawkish tone, asserting that a rate cut would only be entertained once the Committee possesses the conviction that inflation is progressively gravitating towards the 2 percent target. In his press conference following the policy meeting, Fed Chair Jerome Powell insinuated that, based on the current meeting’s outcome, it appears improbable that the Committee will have garnered adequate confidence by March to pinpoint it as the opportune moment for a rate alteration. The likelihood of a March Fed rate cut receded from approximately 50% at the onset of the week to 35% following the Fed’s policy declarations, according to CME Group’s FedWatch Tool. Conversely, the markets are presently attributing a 90% likelihood to a Fed rate reduction in May.

With regard to the forthcoming January jobs report, TD Securities analysts are expecting a robust augmentation in payrolls, envisioning the inclusion of 230,000 fresh job opportunities next week. It’s important to note that this report will also encompass the NFP’s annual benchmark and updates to seasonal factors, introducing an added layer of intricacy to the analysis. Separately, private sector employment in the US witnessed an increment of 107,000 in January, as revealed by Automatic Data Processing, falling short of the predicted upturn of 145,000.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has reached the higher low area of the channel

Swiss Bank Julius Baer has decided to replace its current CEO due to concerns about the handling of its private debt business. The company incurred significant losses amounting to 586 million francs last year, which were attributed to the activities associated with Rene Benko’s signal group.

Julius Baer, the Swiss bank, took significant actions on Thursday in response to its financial challenges. The bank announced the removal of its CEO, Philipp Rickenbacher, and revealed its decision to exit the private debt business. This strategic shift comes after substantial losses of 586 million Swiss francs incurred due to loans extended to the collapsed property firm, Signa.

Signa Group, owned by Austrian property magnate Rene Benko, had been Julius Baer’s primary client within its private debt business. However, the insolvency of Signa late last year had a detrimental impact on the bank’s financial health. The decision to remove CEO Philipp Rickenbacher followed a board meeting held on Wednesday, which was prompted by the revelation of a writedown that exceeded analysts’ expectations. Rickenbacher, who had been leading Julius Baer since 2019, expressed his resignation on LinkedIn, stating that it was in the best interests of the bank for him to step down. This decision was made with deep regret, given his two-decade-long association with Julius Baer.

Nic Dreckmann, the deputy CEO, will temporarily assume the role of CEO while the bank embarks on a search for an external candidate. Rickenbacher had been appointed to restore stability to Julius Baer following a series of scandals and regulatory probes that had tarnished the institution’s reputation. Julius Baer’s Chairman, Romeo Lacher, expressed disappointment over the impact of the loss allowance for the largest exposure within the private debt business on the bank’s net profit for 2023. Nevertheless, the bank’s shares experienced a notable 10% surge on Thursday, with investors reacting positively to the measures taken to address the Signa-related issues and steer the bank toward a more stable future.

CADCHF Analysis:

CADCHF is moving in the Descending channel and the market has reached the lower high area of the channel

In January, Canada’s Manufacturing Purchasing Managers’ Index reached 48.3, showing an improvement from the previous month’s reading of 45.4. The expansion in Canadian GDP data for January has already lent support to the Canadian Dollar when compared to other currencies.

Ending a four-week winning streak, the currency pair faced a shift in momentum as the US Dollar lost ground, settling at 103.00. Market participants are eagerly anticipating the US Nonfarm Payrolls report for January, a potential catalyst for market volatility. Notably, recent data released on Thursday showed significant improvement in the US Manufacturing Purchasing Managers’ Index for January. The US ISM Manufacturing PMI exceeded expectations, registering 49.1 compared to the previous reading of 47.1, which had anticipated a figure of 47.0. This boost in growth was primarily driven by a resurgence in new orders and a slowdown in the contraction of production. Despite this positive Manufacturing PMI figure, the Greenback failed to gain traction as traders assessed the insights from the January Federal Reserve meeting.

Concurrently, the Canadian S&P Global Manufacturing PMI for January improved to 48.3, an increase from the prior reading of 45.4. Earlier in the week, Canada’s real Gross Domestic Product demonstrated growth of 0.2% in November. These growth figures highlight the Canadian economy’s resilience and may alleviate pressure on the Bank of Canada to implement interest rate cuts. However, it’s worth noting that a decline in oil prices could exert downward pressure on the commodity-linked Canadian Dollar, given Canada’s status as the largest oil exporter to the United States.

Market participants are closely monitoring the US labor market data set to be released on Friday. The US Nonfarm Payrolls report is expected to reveal the addition of 185,000 jobs in January. Forecasts also suggest a rise in the Unemployment Rate to 3.8%, alongside an anticipated 0.3% month-on-month increase in Average Hourly Earnings. Additionally, there are upcoming releases of US Factory Orders data and the final reading of the Michigan Consumer Sentiment index.

EURCHF Analysis:

EURCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel

ECB Chief Economist Philip Lane noted that natural gas prices in December contradicted earlier expectations of a rise. Surprisingly, even Israel’s war conflict had limited impact on these prices. Additionally, the lower costs incurred for shipping re-routes due to conflicts in the Red Sea region have contributed to alleviating some of the inflationary pressures.

Philip Lane, the Chief Economist of the European Central Bank, made remarks on Thursday concerning the state of natural gas prices in the Euro area. Lane noted that these prices are currently significantly lower than what the ECB had anticipated in its projections for December.

Furthermore, Lane addressed concerns related to issues in the Red Sea region, stating that they are relatively contained in terms of their impact on inflation. This assertion was made with regard to the relatively small contribution of shipping costs to overall inflationary pressures in the Euro area.

EURJPY Analysis:

EURJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Japanese Yen saw an upward surge following the announcement from the Bank of Japan. The central bank indicated that a potential interest rate increase could be on the horizon if inflation and wage growth align with their near-term targets.

During the early European session on Friday, the Japanese Yen showed a slight decline against the US Dollar, moving further away from the two-week high reached the day before. This shift is attributed to expectations of increased stimulus from China and diplomatic efforts to secure a ceasefire in the Palestinian region, which boosted investor confidence and reduced the Yen’s appeal as a safe-haven asset. Bearish traders also took note of a rebound in US Treasury bond yields, although various factors are expected to limit any significant downside for the Japanese Yen.

Investors have grown more convinced that the Bank of Japan may start moving away from its ultra-dovish policies later this year. In contrast, the markets are still pricing in a series of rate cuts by the Federal Reserve in 2024, despite the central bank’s recent pushback against expectations for such a move in March. Additionally, investors appear cautious about making aggressive bets ahead of the release of the US monthly employment report, known as the NFP report, scheduled for later in the day. Expectations are that the report will indicate the addition of 180,000 jobs in January, a decrease from the 216,000 jobs reported the previous month. Meanwhile, the Unemployment Rate is anticipated to inch higher from 3.7% in December to 3.8%, while Average Hourly Earnings growth is expected to remain steady at 4.1% year-on-year for the reported month. Furthermore, optimism about potential Chinese government stimulus measures to support its economy has contributed to undermining the safe-haven status of the Japanese Yen. Tensions in the Middle East persist, with the US pledging to take necessary actions to protect its troops after a drone attack in Jordan, and Yemen-based Houthi forces continuing attacks on shipping in the Red Sea. An official factory survey released earlier in the week showed that manufacturing activity in China contracted for the fourth consecutive month in January, indicating challenges for the world’s second-largest economy in regaining momentum. The recent hawkish tilt from the Bank of Japan has also bolstered the Japanese Yen, signaling a commitment to achieving its inflation goal and potentially raising interest rates out of negative territory in March or April. Conversely, the US Dollar has experienced a notable shift, as it retreats from the year-to-date peak recorded on Thursday. The Federal Reserve’s recent statements, including Fed Chair Jerome Powell’s assertion that interest rates are on the decline, have contributed to this sentiment, even though a rate cut in March remains uncertain.

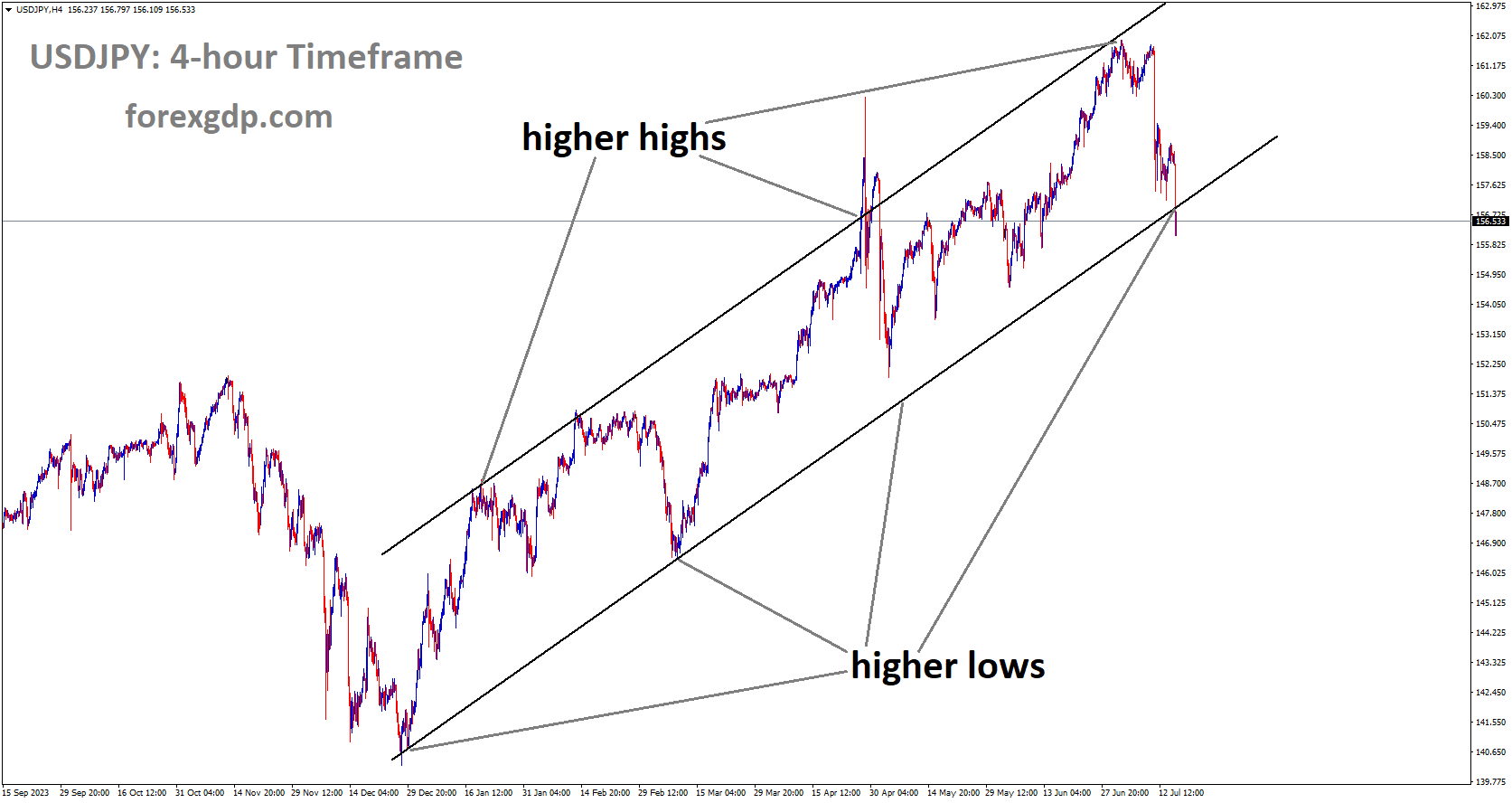

GBPUSD Analysis:

GBPUSD has broken the Descending channel in upside

Yesterday, the Bank of England opted to maintain its interest rates at a stable 5.25%. This decision triggered a varied response in the GBP’s value when compared to other currencies. BoE Governor Bailey expressed that the current inflation rate is considerably distant from the targeted 2%. Consequently, the possibility of future rate cuts remains on the table, contingent upon the achievement of only a meager 2% of the set inflation target. Bailey emphasized this point in his recent statement.

The Bank of England made the decision to keep the UK benchmark interest rate unchanged. However, what’s intriguing is the apparent division within the Monetary Policy Committee, which is the bank’s decision-making body. Six members voted in favor of maintaining the current rates, but two members advocated for a rate hike. Notably, Swati Dhingra, a well-known dovish member, cast her vote in favor of the first rate cut for the Bank of England.

One of the most noteworthy revelations from the monetary policy report was the forecast indicating a drop in inflation to reach the target in Q2 of this year. This signifies significant progress compared to the November projections, which had estimated reaching the 2% target only by the end of 2025. While this appears to be positive news, it’s worth noting that the Bank of England anticipates inflation to resurface and remain above target until the end of 2026. A closely monitored indicator for the Bank’s medium-term inflation outlook is the 2-year Consumer Price Index forecast, which has notably risen to 2.3% from the November estimate of 1.9%. This underscores the concern of persistent inflation. The Bank of England has often referred to the labor market, private wage growth, and general services inflation when discussing the potential for interest rate cuts. Services inflation is expected to experience an end-of-year dip before rising to 6.6% and subsequently declining to around 5% in Q2. On the other hand, wage growth is projected to continue progressing, albeit at a slightly slower pace, dropping to 4% by the end of this year compared to the November forecast of 4.25%. The Bank anticipates that unemployment will ease, but the rate of improvement may be slower than previously anticipated.

AUDUSD Analysis:

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

In the fourth quarter, Australian Producer Price Index figures showed a rise, reaching 4.1% compared to the 3.8% reported in the previous quarter. Following this data release, the likelihood of the Reserve Bank of Australia maintaining its interest rate at 4.35% in the upcoming February meeting appears more probable.

Mixed economic data from the United States exerted downward pressure on the US Dollar, while the Australian Dollar found support from an improved Producer Price Index. This combined to bolster the AUDUSD currency pair. The Australian Bureau of Statistics recently released PPI figures for the fourth quarter, revealing growth of 4.1%, surpassing the previous 3.8% rate. Additionally, a strengthened Australian money market contributes to the Aussie Dollar’s resilience. In Poll, analysts unanimously anticipate the Reserve Bank of Australia to maintain the interest rate at 4.35% in its upcoming February policy meeting.

Former RBA board member Warwick McKibbin has suggested that the Australian cash rate could remain around 4.5% for an extended period. However, the Australian Dollar has faced challenges as bond traders increasingly anticipate early interest rate cuts by the Reserve Bank of Australia, following an unexpectedly weak quarterly inflation report. Futures markets are fully pricing in two quarter-point reductions in 2024, with the first expected adjustment in August. Meanwhile, the US Dollar Index experienced losses after mixed US economic data was released on Thursday, coupled with subdued US Treasury yields. Initial Jobless Claims for the week ending on January 26 rose to 224K, surpassing the previous increase of 215K and the expected figure of 212K. Conversely, the ISM Manufacturing Purchasing Managers’ Index showed improvement, rising to 49.1 from the previous reading of 47.1, exceeding the anticipated 47.0 figure for January. On Friday, additional labor data is set to be released, including US Average Hourly Earnings and Nonfarm Payrolls.

In other economic news, the Australian Producer Price Index increased by 0.9% in the fourth quarter, down from the previous growth rate of 1.08%. Australia’s Investment Lending for Homes declined by 1.3% in December, contrasting with the previous growth rate of 1.9%. Additionally, Australia’s Home Loans fell by 5.6% in December, in contrast to the 0.5% growth recorded in November. On the US front, preliminary Nonfarm Productivity for Q4 increased by 3.2%, surpassing the expected 2.5%, but lower than the previous reading of 4.9%. Challenger Job Cuts in the US rose to 82.307K in January, up from the previous 34.817K in December, while US Unit Labor Costs reported a 0.5% increase, deviating from the expected 1.7% decrease in the fourth quarter, reversing the previous -1.1% figure.

NZDUSD Analysis :

NZDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

In December, New Zealand’s building permits rebounded, showing a growth of 3.7% after experiencing a significant 10.6% decline in November. Additionally, consumer confidence in the country inched up slightly to 93.6 from its previous reading of 93.1 in November. The devaluation of the US Dollar could be ascribed to the lackluster performance of US Treasury yields. These yields faced a downward push due to concerns surrounding regional US banks. Furthermore, the positive medium-impact data from New Zealand might have offered some support to the New Zealand Dollar, consequently acting as a boost for the NZDUSD currency pair.

The US Dollar Index, which measures the US Dollar’s performance against a basket of six major currencies, is grappling with its recent losses. Currently, the DXY is hovering around 103.00, with US Treasury bond yields reflecting rates of 4.21% for the 2-year and 3.88% for the 10-year, at the time of this writing. Moreover, the US Dollar came under pressure following the release of mixed economic data from the United States on Thursday. While Initial Jobless Claims for the week ending on January 26 increased to 224K, surpassing the previous rise of 215K and the expected figure of 212K, the ISM Manufacturing Purchasing Managers’ Index exhibited improvement, climbing to 49.1 from the prior reading of 47.1, exceeding the anticipated figure of 47.0 for January. Additionally, there are expectations for the release of further labor data, including US Average Hourly Earnings and Nonfarm Payrolls, which are scheduled for release on Friday.

In New Zealand, the seasonally adjusted Building Permit data for December showed signs of improvement, with a 3.7% increase reversing the previous decline of 10.6% in November. Additionally, ANZ-Roy Morgan Consumer Confidence for December recorded a reading of 93.6, surpassing the prior reading of 93.1. The Reserve Bank of New Zealand maintains its focus on achieving a target of approximately the 2% midpoint for future inflation. Investors are eagerly anticipating the release of New Zealand’s labor market data next week, which will provide further insights into the country’s economic landscape.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/