Gold – Gold Price Forecast: XAUUSD Edges Up in Light of Softer Risk Tone, Lacks Bullish Conviction

Gold prices moved lowered after the US ISM Services PMI data came at 53.4 versus 50.5 in the previous reading. Hawkish speeches from FED members moved the US Dollar higher against Gold in the market.

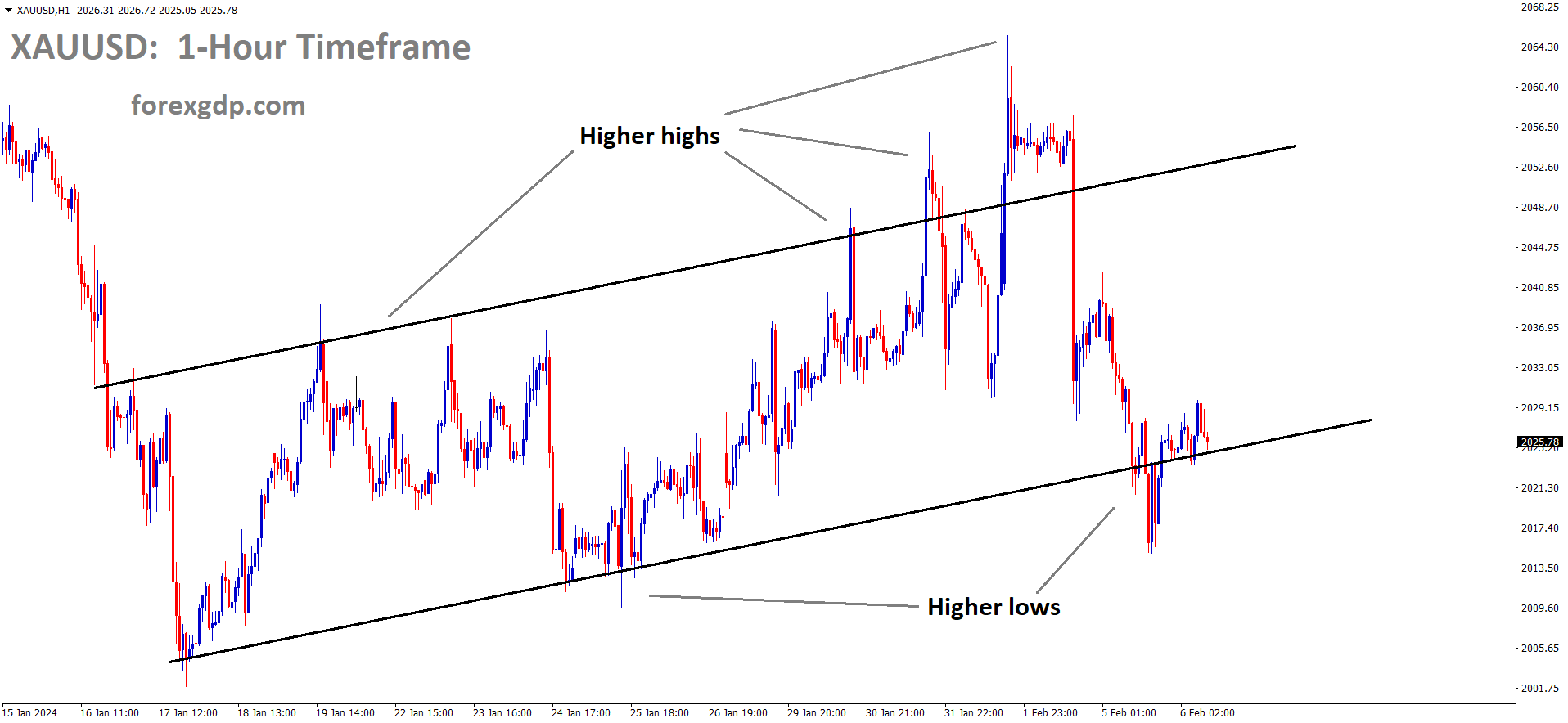

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

The US Dollar remains strong, supported by expectations of prolonged higher interest rates following upbeat US jobs data. The Institute for Supply Management (ISM) reported a Non-Manufacturing PMI increase to 53.4 in January, contributing to the sentiment of a less aggressive Fed easing in 2024, reinforced by hawkish comments from FOMC members.

Fed Chair Jerome Powell, in a “60 Minutes” interview, emphasized patience in deciding when to cut interest rates. Minneapolis Fed President Neel Kashkari suggested officials have time to assess data, while Chicago Fed President Austan Goolsbee expressed the need for favorable inflation data. Elevated US Treasury bond yields continue to bolster the USD, acting as a headwind for non-yielding Gold.

Despite uncertainty over inflation and geopolitical tensions, Gold finds support as investors turn to safe-haven assets amid a corrective decline in US equity markets. With no significant economic releases from the US, confirmation of a near-term bearish breakdown awaits strong follow-through selling.

XAGUSD – USD Opens Week Strong with Robust ISM Services PMIs

US Dollar moved higher after the US Services PMI (Jan )data came at 53.4 from 50.5 in the previous reading. The first week of the day started higher against Counter pairs.

XAGUSD Silver price has broken the Box pattern in downside

The Dollar’s rise is credited to the strengthening ISM Services PMI for January, which boosted the Dollar Index as market expectations for a March interest rate cut diminished.

The Federal Reserve’s hawkish stance, backed by a solid jobs report and ongoing strong Q1 growth, challenges earlier predictions of imminent rate cuts. Fed Chair Powell remains cautious, highlighting the importance of monitoring inflation’s sustained movement toward the 2% core target.

Daily Market Digest: USD Strengthens on Higher-than-Expected Services PMI

– January’s ISM Services PMI surpasses expectations at 53.4, beating both the consensus figure of 52 and the previous month’s 50.5, according to the Institute for Supply Management (ISM).

– US bond yields reach monthly highs, with 2-year, 5-year, and 10-year bonds trading at rates of 4.45%, 4.11%, and 4.15%, respectively. These increased rates, exceeding 2%, make the US Dollar appealing to foreign investors.

– CME’s FedWatch Tool indicates reduced chances of a March rate cut, currently at 15%. Odds rise to 50% in May, with significant probabilities of a hold.

USDCHF – Holds Below 0.8700 Amid Weaker USD

SNB like to rate cuts in September 2024, but inflation is likely to remain under the 2% target in 2024. Yesterday US ISM Services index came at 53.4 versus the 52.0 expected. ISM Services employment index rose to 50.5 from 43.8 previous reading.

USDCHF has broken the Descending channel in upside

Bond yields may be influenced by global sentiment following recent remarks from Federal Reserve Chair Jerome Powell, suggesting that a March rate cut is premature.

The Swiss National Bank, in its last 2023 meeting, opted to maintain its key interest rate at 1.75%, concluding its recent tightening cycle. Monthly consumer prices remained stable, with a slight increase in the core rate. Projections for the current year suggest inflation averaging below 2.0%, leading analysts to anticipate the possibility of the SNB implementing its first rate cut in September 2024.

In January, the US ISM Services Purchasing Managers’ Index (PMI) exceeded expectations, registering a reading of 53.4, surpassing both the anticipated 52.0 and the prior month’s 50.5. Additionally, the ISM Services Employment Index increased to 50.5 from the previous 43.8.

Federal Reserve Chairman Jerome Powell emphasized the need to closely monitor inflation’s sustained movement toward the 2% core target. This stance contributed to the strengthening of the US Dollar, providing support for the USD/CHF pair.

USDCAD – Rises below 1.3550, Focus on Canadian PMI Data

The Bank of Canada is expected to rate cuts in April 2024 from 22-year highs of 5% according to the survey report. By year end 4% target is expected from BoC in the view of Analysts side.

USDCAD is moving in box pattern and market has rebounded from the support area of the pattern

A stronger US Dollar and higher US Treasury bond yields support USD/CAD, currently trading near 1.3540, up 0.03% on the day. The January Canadian Ivey Purchasing Managers Index (PMI) is expected to ease from 56.3 in December to 55.0 in January.

Fed Chair Jerome Powell’s statement suggests three potential interest rate cuts this year, starting as early as May, boosting the Greenback. The likelihood of a March rate cut has dropped to 15%, down from 38% a day ago.

Investors anticipate the Bank of Canada to cut its benchmark interest rate from a 22-year high of 5% in April, with the median forecast for the policy rate reaching 4% by the end of 2024.

Declining oil prices may pressure the commodity-linked Loonie, as Canada is the largest oil exporter to the United States. Canadian Building Permits and Ivey PMI data are anticipated on Tuesday, with attention shifting to labor market data, including the Unemployment Rate, on Friday.

EURUSD – German Factory Orders Surge 8.9% MoM, Exceeding 0% Forecast

Germany Factory orders came at 8.9% MoM in December month versus 0.0% in November month. Overall annual rate growth at 2.7% from -4.7% in the previous period.

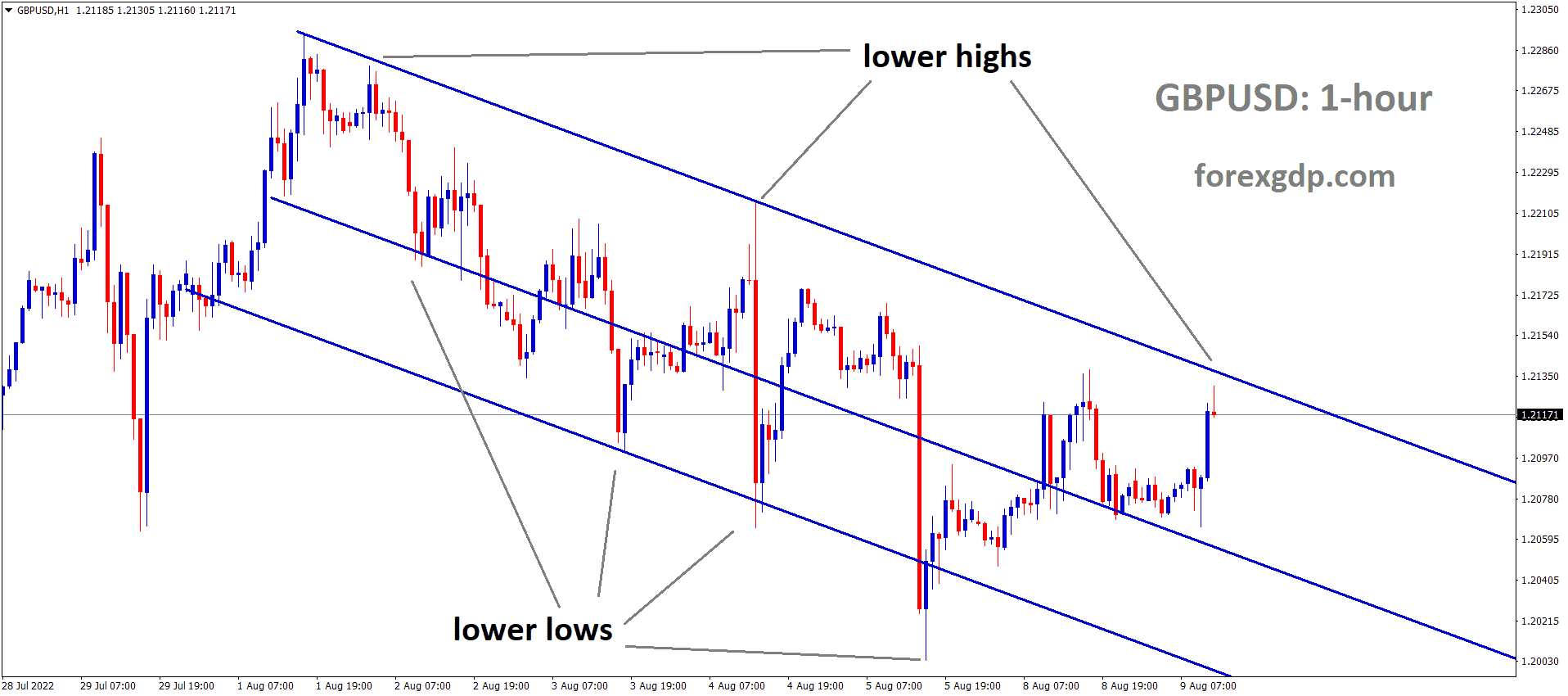

EURUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel

German Factory Orders Make Surprise Rebound in December, Showing Renewed Momentum

In December, monthly contracts for ‘Made in Germany’ goods surged 8.9%, a significant turnaround from the 0% reported in November and surpassing expectations of no growth. Additionally, Germany’s Industrial Orders experienced a year-on-year increase of 2.7% during the same period, contrasting with the previous decline of 4.7%. This data, released by the Federal Statistics Office, indicates a robust recovery in the German manufacturing sector.

EURGBP – Dips Near 0.8570 Before Eurozone, UK Retail Sales Data

UK Composite PMI increased to 52.9 versus 52.5 expected in the January month reading. Services PMI data came at 54.3 from 53.8 expected. Euro PPI data showed a 10.6% decline in December month versus the 10.5% decline expected. So GBP moved stronger against the Euro in the market.

EURGBP is moving in Ascending channel and market has fallen from the higher high area of the channel

– Pound Sterling (GBP) potentially strengthened against Euro (EUR) with improved UK Purchasing Managers Index (PMI) data. Retail Sales data from both economies will be closely watched on Tuesday.

– Bank of England’s Chief Economist Huw Pill noted potential interest rate cuts in the future but cautioned against premature expectations. BoE awaits stronger evidence of decreasing UK inflation before considering rate-cut measures.

– UK S&P Global/CIPS Composite PMI rose to 52.9 in January, exceeding expectations of 52.5. Services PMI improved to 54.3, surpassing the expected 53.8.

– EU Producer Price Index (PPI) recorded a substantial 10.6% decline in December, surpassing the expected decrease of 10.5%. Monthly index fell by 0.8%, in line with expectations.

– EUR/GBP faced downward pressure due to the EU’s disinflationary trend, possibly prompting the European Central Bank (ECB) to consider policy measures. OECD anticipates inflation in Europe above the ECB’s 2% target until after 2025.

EURJPY – BoJ’s Ueda: More Time for Decision on ETF Holdings

The Bank of Japan Governor said we have to review our massive stimulus programme, then only we decide to buy or sell the ETF’s purchases. So we have more time to decide on changing monetary policy settings.

EURJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Bank of Japan Governor Kazuo Ueda stated on Tuesday that, during the review of their extensive stimulus program, they will assess the continuation or discontinuation of various measures, including ETF purchases. Ueda emphasized that when deciding on the fate of BoJ’s ETF holdings, there is ample time to reach a decision.

AUDJPY – AUD Climbs post RBA Decision; Gov Bullock Open to Policy Options

RBA maintained the interest rate at 4.35% today, Retail sales for the 4th quarter ending 2023 are up by 0.30% versus a 0.20% rise in the previous quarter. The Australian Dollar moved positively after the decision came.

AUDJPY is moving in the Box pattern and the market has rebounded from the support area of the pattern

AUD vs. USD Movement:

– The Australian Dollar (AUD) strengthened against the US Dollar (USD) as the Reserve Bank of Australia maintained the Official Cash Rate at 4.35% in February, as expected.

– However, the AUD/USD pair weakened due to hawkish comments from Federal Reserve (Fed) Chair Jerome Powell and reduced commodity prices.

Retail Sales Data:

– Australian Bureau of Statistics released Retail Sales (QoQ) data, showing a 0.3% rise in the fourth quarter, an improvement from the previous growth of 0.2%.

Cost-of-Living Crisis and RBA’s Policy:

– The Australian economy faces a cost-of-living crisis, limiting room for RBA policymakers to raise interest rates.

– Focus shifts to when the central bank might consider reducing interest rates.

RBA Governor’s Perspective:

– RBA Governor Michele Bullock, in a post-interest rate decision press conference, mentioned that the bank is not ruling anything in or out regarding policy decisions.

– Risks are perceived as balanced, and the bank is actively seeking data confirming a return of inflation to the target level.

– Governor Bullock sees the central bank on a potentially narrow path to achieving the goal of bringing inflation back to the target, citing a 2.8% inflation forecast for 2025.

US Dollar Index and ISM Services Data:

– The US Dollar Index surged following the Federal Reserve’s hawkish stance.

– ISM Services PMI for January exceeded expectations at 53.4, surpassing the consensus figure of 52.0 and the previous month’s 50.5.

– ISM Services Employment Index improved, rising to 50.5 from the previous reading of 43.8.

Powell’s Influence on USD:

– Federal Reserve Chairman Jerome Powell contributed to the strengthening of the US Dollar by dampening expectations of a rate cut.

– Powell emphasized the importance of monitoring inflation’s sustained movement toward the 2% core target, leading to increased US Treasury yields and downward pressure on the AUD/USD pair.

Daily Market Digest: AUD Weakens on Fed’s Hawkish Stance

– Australian Trade Balance for January decreased to 10,959M, down from the revised December figure of 11,764M.

– Australia’s Judo Bank Composite Purchasing Managers Index (PMI) rose to 49 in January from the previous 48.1, with the Services PMI improving to 49.1 from 47.9.

– Aussie TD Securities Inflation grew by 4.6%, down from the previous growth of 5.2%.

– Australian TD Securities Inflation (MoM) increased by 0.3% in January, a decline from December’s rise of 1.0%.

– Chinese Caixin Services PMI dropped to 52.7 in January, compared to the previous reading of 52.9.

– US ISM Services Prices Paid increased to 64.0 in January, up from December’s reading of 56.7.

– The US Services New Orders Index for January improved to 55.0 from the previous figure of 52.8.

– US S&P Global Composite PMI for January came in at 52.0, slightly lower than the prior reading of 52.3.

CADJPY – Japan’s December Labor Cash Earnings and Household Spending Below Expectations

Japan Labor cash earnings for December came at 1% versus the 1.3% forecast. Overall Household spending data came at -2.5% versus -2.1% expected. It shows a minor recovery from -2.9% in the previous month.

CADJPY is moving in box pattern and market has fallen from the resistance area of the pattern

Japan’s annualized Labor Cash Earnings and Overall Household Spending fell short of market expectations for the year ending in December. Labor earnings grew by 1%, missing the forecast of 1.3%, with minimal wage growth compared to the previous period’s 0.7%, which had a significant upward revision from 0.2%.

Overall Household Spending for the year through December dropped by 2.5%, below the market’s expected -2.1%, showing only a modest recovery from the previous period’s -2.9%.

NZDUSD – Defends Mid-0.6000s Amid Robust US Dollar, Elevated Bond Yields

NZ Country is today’s holiday account of Waitangi Day, Tomorrow NZ unemployment rate Q4 is scheduled and Thursday China data of CPI and PPI is scheduled. NZ Dollar moved lowered after the US Domestic data came at robust numbers in the market.

NZDUSD is moving in box pattern and market has reached support area of the pattern

– US ISM Services PMI for January surpassed expectations at 53.4, with New Orders reaching a three-month high of 55.0. Employment Index rebounded to 50.5, and Prices Index jumped to 64.0.

– Minneapolis Fed President Neel Kashkari stated a strong economy and potentially higher neutral interest rate allow the Fed to delay benchmark interest rate cuts. Fed Chair Jerome Powell’s cautious approach reduces the likelihood of a March rate cut, with markets pricing less than a 20% chance.

– China’s Services PMI, released by Caixin, came in at 52.7 for January, slightly below expectations. A property crisis and slow economic recovery in China may pressure the New Zealand Dollar.

– New Zealand’s markets are closed on Waitangi Day. Traders await cues from Fed’s Mester speech on Tuesday and upcoming releases including New Zealand’s Unemployment Rate on Wednesday, and Chinese Consumer Price Index and Producer Price Index for January on Thursday.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/