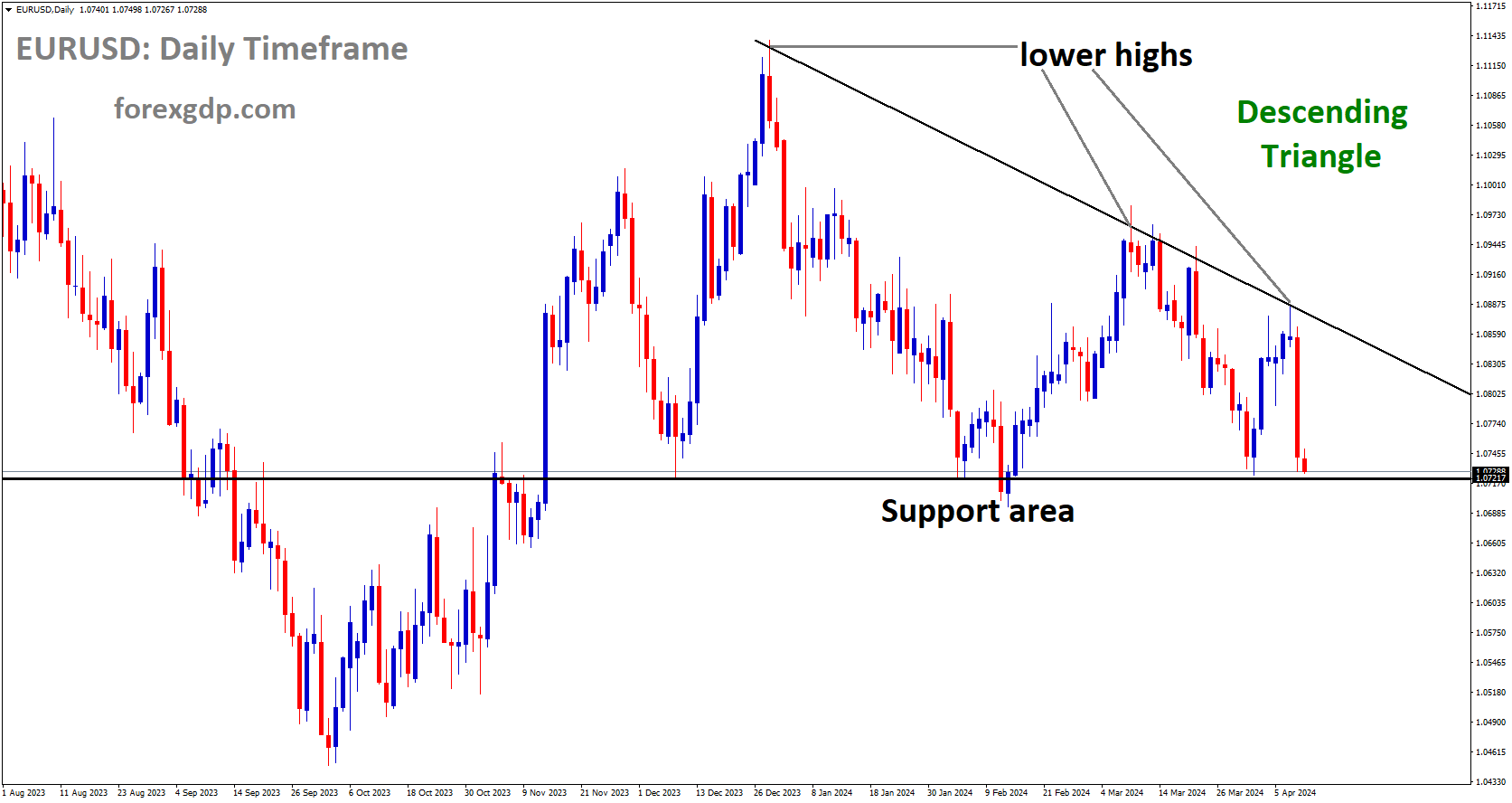

EURUSD is moving in Descending Triangle and market has reached support area of the pattern

EURUSD – ECB Meeting and US Inflation Surge

ECB is widely forecasted to maintain interest rates at their current levels. Meanwhile, March saw the US CPI figure rising by 0.4% MoM, exceeding the anticipated 0.3% increase.

During the early stages of the Asian session on Thursday, the EUR/USD pair finds itself in a defensive position. This can be attributed to the unexpected surge in US CPI inflation figures for March, which propelled the US Dollar to its highest levels of the year, consequently impacting the major pair. Market participants are eagerly awaiting the European Central Bank’s interest rate decision and subsequent press conference later in the day, alongside the unveiling of the US Producer Price Index (PPI) report.

While the ECB is expected to maintain interest rates at their record high during the April meeting, ECB President Christine Lagarde is likely to address the inflation data and the potential for a rate cut in June. In contrast, the Federal Reserve may postpone its easing cycle this year, given the strength of the economy and the unexpected upticks in inflation. Although the ECB maintains an independent policy stance, the divergent interest rate paths between the Fed and ECB could exert downward pressure on the Euro and pose challenges for the EUR/USD pair.

The unforeseen increase in US inflation data for March has led to speculations that the US central bank might postpone interest rate cuts. Subsequently, the Greenback surged to yearly highs exceeding post-release of the data. According to the Labor Department’s report on Wednesday, the US Consumer Price Index (CPI) rose by 0.4% MoM in March, surpassing the anticipated 0.3% gain. On an annual basis, the CPI registered a 3.5% YoY increase, slightly above the expected 3.4% rise.

Moreover, the Core CPI figure, excluding volatile food and energy prices, exhibited a 0.4% MoM increase in March, outpacing the market consensus of 0.3%. Additionally, the Core figure recorded a 3.8% growth, exceeding the projected 3.7% uptick. Later in the day, markets will turn their attention to the release of the US Producer Price Index for March and the weekly Initial Jobless Claims data.

GOLD – Prices Rebound Amidst Geopolitical Tensions and Fed Speculation

Gold prices experienced a resurgence in investor interest on Thursday, bouncing back from the previous day’s decline triggered by the release of the US Consumer Price Index (CPI). Despite the dollar’s resilience, geopolitical tensions provided additional support to the safe-haven appeal of XAU/USD.

XAUUSD is moving in Ascending channel and market has reached higher low area of the channel

During the first half of the European trading session, gold prices struggled to maintain their intraday gains and hovered near the lower end of the daily range. The CPI report from the US, unveiled on Wednesday, sparked speculation that the Federal Reserve might delay implementing interest rate cuts. This sentiment was reinforced by the minutes of the March Federal Open Market Committee (FOMC) meeting, which hinted at a possibility of prolonged higher interest rates. Consequently, the US dollar remained firm, acting as a barrier to gold’s upward movement.

In addition to these factors, hawkish expectations surrounding the Fed’s monetary policy, combined with ongoing concerns about the escalating crisis in the Middle East, continued to influence investor sentiment. The prevailing cautious market atmosphere acted as a catalyst for gold prices, potentially preventing a significant downturn from the all-time high levels observed recently. As a result, market participants exercised caution and awaited confirmation of sustained selling pressure before concluding that XAU/USD had reached its peak.

Looking ahead, market focus shifted to key US macroeconomic data releases, such as Weekly Initial Jobless Claims and the Producer Price Index (PPI), as well as speeches from Federal Reserve officials. These events were anticipated to provide short-term trading opportunities and further shape market sentiment towards gold.

The surge in US Treasury bond yields witnessed the previous day, fueled by the robust CPI report, exerted downward pressure on gold prices. The US Bureau of Labor Statistics reported a 3.5% year-on-year increase in the headline CPI and a 0.4% month-on-month rise, surpassing market expectations. Furthermore, the core CPI, which excludes volatile food and energy components, accelerated to a 3.8% year-on-year rate, raising concerns that the Federal Reserve might delay implementing rate cuts.

Minutes from the March FOMC meeting revealed that policymakers were hesitant to consider rate cuts until they were confident that inflation was moving steadily towards the 2% annual target. Consequently, market expectations for the timing of the first rate cut shifted to September from June, with fewer anticipated cuts throughout the year.

Geopolitical tensions in the Middle East, particularly ceasefire talks between Israel and Hamas, coupled with potential retaliation from Iran over an alleged Israeli strike in Syria, contributed to investor apprehension. These geopolitical uncertainties further supported the safe-haven appeal of gold, adding to its attractiveness amidst the prevailing market conditions.

USDJPY – Yen Weakens Amid Dollar Strength

The Japanese Yen faces resistance against the US Dollar, hovering near multi-decade lows and struggling to maintain modest gains. Differing policy outlooks between the Federal Reserve and the Bank of Japan undermine the yen, providing momentum to the USD/JPY pair. Concerns over potential intervention by Japanese authorities to bolster the yen may deter further selling pressure and limit gains for the pair.

USDJPY is moving in Ascending Triangle and market has reached resistance area of the pattern

Amidst the European session, the Japanese Yen relinquishes its minor gains against the US Dollar, propelling the USD/JPY pair above 153.00 and closer to recent multi-decade highs. The widening interest rate gap between the US and Japan plays a pivotal role in weakening the yen and bolstering the currency pair. Notably, the Bank of Japan adopts a cautious stance following its March meeting, refraining from outlining future policy directions or the pace of normalization.

Conversely, robust US inflation data, as evidenced by the recent Consumer Price Index (CPI) report, prompts investors to postpone expectations of the Federal Reserve’s rate cut to September from June. Additionally, minutes from the Federal Open Market Committee (FOMC) meeting express concerns over sluggish progress in inflation, suggesting a prolonged period of higher rates. These factors, combined with stabilizing global equity markets, diminish demand for the safe-haven yen and aid the USD/JPY pair’s ascent.

Investors remain vigilant amid speculation of potential Japanese intervention to support the yen, potentially curbing bearish bets and restraining further upside for USD/JPY. Nonetheless, the pair’s breakout from a short-term trading range and renewed buying interest indicate a bullish bias. Market participants await impetus from the US Producer Price Index (PPI) report and speeches by influential FOMC members.

The US Dollar strengthens across the board following robust consumer price data, driving the Japanese Yen to multi-month lows. The US Bureau of Labor Statistics (BLS) reports higher-than-expected CPI figures, contributing to speculation of delayed rate cuts by the Federal Reserve. Japanese officials’ efforts to verbally support the yen offer brief relief, yet geopolitical tensions and uncertainty persist, influencing market sentiment.

The Bank of Japan maintains a cautious stance post-March meeting, refraining from signaling future policy moves, constraining further yen appreciation. Market focus shifts to US economic indicators and FOMC member speeches for further direction.

USDCAD – Central Bank Decisions and Inflation: Impact on USD/CAD Pair

The Bank of Canada (BoC) stood firm, keeping its benchmark interest rates steady at 5% for the sixth consecutive gathering, a decision announced amidst a backdrop of economic scrutiny on Wednesday. Across the border, March unveiled a surprising surge in US inflation, throwing a curveball at expectations and prompting the Federal Reserve (Fed) to reconsider the timing of any potential rate cuts this year.

USDCAD has broken Ascending channel in upside

Fueling the ascent of the USD/CAD pair was the unexpected vigor of US inflation in March, injecting fresh vigor into the Greenback, propelling it to heights not seen in the current year. Investors, with bated breath, now await the unveiling of the US Producer Price Index (PPI) later on Thursday, with forecasts pointing to a prospective uptick in both headline and Core PPI figures, expected to clock in at 2.2% and 2.3% year-over-year, respectively.

On the subsequent Thursday, the Bank of Canada (BoC) convened for its April session, maintaining the key interest rate at 5% for the sixth consecutive time since July. BoC Governor Tiff Macklem, in a press conference following the announcement, acknowledged the glimmers of positivity in the inflationary landscape but underscored the necessity for a more sustained validation before contemplating any alterations to the rate trajectory. Macklem tantalizingly hinted at the possibility of a rate cut come June.

However, across the southern border, the narrative took a divergent turn as the unexpected robustness of US inflation in March prompted the Federal Reserve (Fed) to extend the tenure of its elevated benchmark rates. Figures released by the Labor Department’s Bureau of Labor Statistics indicated a startling 0.4% month-over-month surge in the US Consumer Price Index (CPI) for March, with a notable 3.5% year-over-year ascent. Further analysis revealed Core CPI, excluding the erratic fluctuations of food and energy, mirroring the momentum with a 0.4% uptick from the previous month and a substantial 3.8% increase from a year ago.

In the wake of the CPI revelations, the likelihood of a rate cut in June, as discerned by the CME FedWatch tool, took a nosedive from 53% on Tuesday to a mere 21%. The report on US inflation for March painted a picture of an unpredictable trajectory, casting doubts on the prospects of any imminent monetary policy adjustments. As a result, the US Dollar Index (DXY) soared to its zenith for the year, providing a semblance of support to the USD/CAD pair amidst the uncertainty.

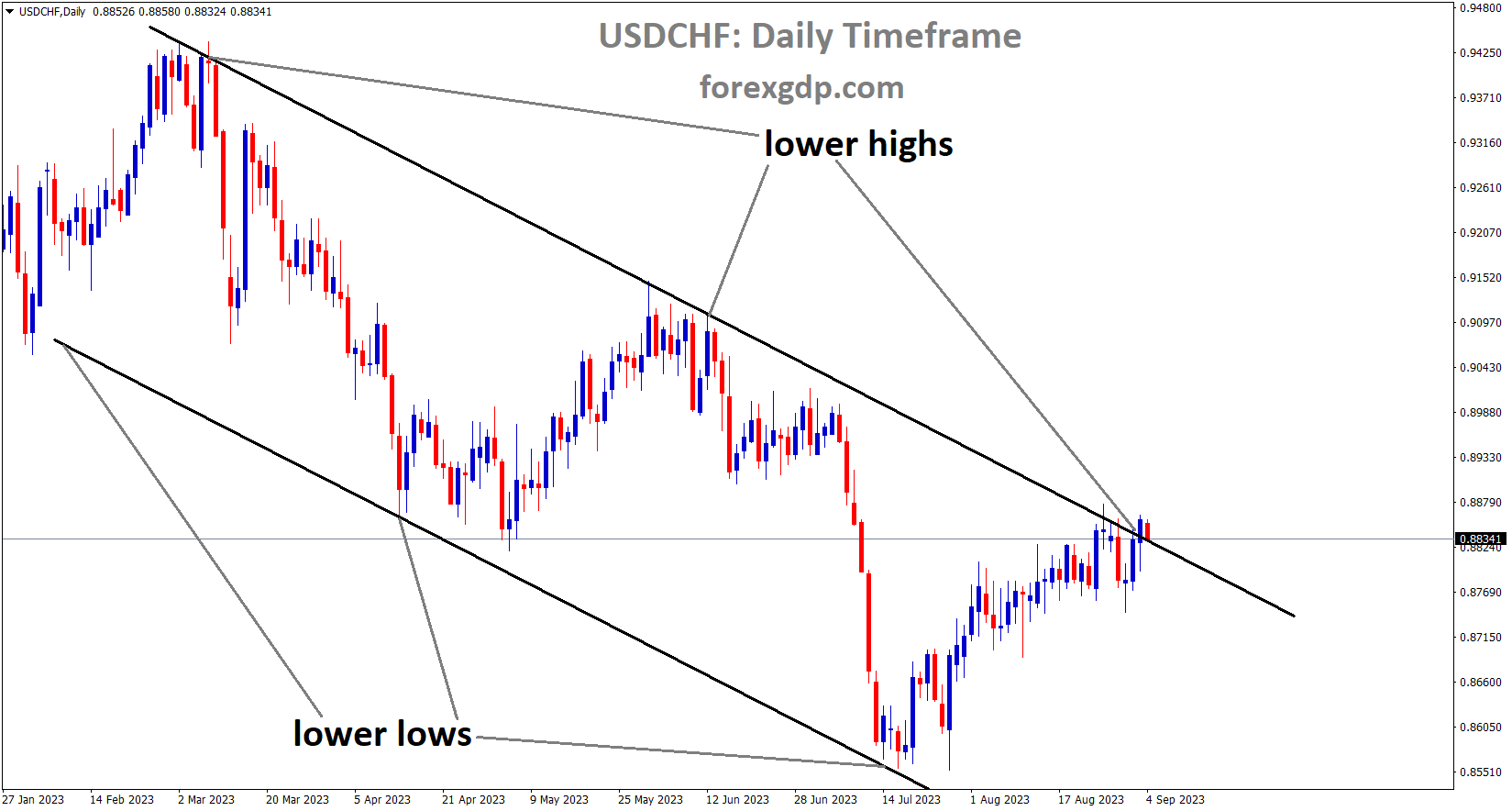

USDCHF – US CPI Surge and Geopolitical Risks Affect USD/CHF Pair

US Consumer Price Index (CPI) data revealed a surprising surge, with a monthly increase of 0.4% and a significant year-over-year rise of 3.5%. These figures surpassed earlier expectations, catching many market participants off guard and sparking discussions about the trajectory of inflation in the United States. This unexpected acceleration in price levels signaled potential challenges for policymakers tasked with maintaining economic stability.

USDCHF is moving in Ascending channel and market has reached higher high area of the channel

Against this backdrop, the USD/CHF currency pair experienced notable movement, reaching its highest level since October 2023 during the early European trading session on Thursday. The momentum in the pair was driven by investors recalibrating their expectations regarding US monetary policy. The stronger-than-anticipated inflation data led many to reconsider previous assumptions about the timing and magnitude of potential interest rate adjustments by the Federal Reserve.

However, amidst the market’s focus on economic indicators, geopolitical tensions in the Middle East added layers of complexity and uncertainty. Ongoing conflicts and diplomatic negotiations in the region contributed to a cautious sentiment among investors, potentially limiting the extent of the pair’s upward movement.

Furthermore, insights from the minutes of the Federal Reserve’s recent meeting revealed concerns among policymakers regarding persistent inflationary pressures. The lack of clarity on whether inflationary trends were transitory or more enduring heightened uncertainty in the market. This uncertainty, coupled with geopolitical developments, created a dynamic environment for traders, with the potential for rapid shifts in sentiment and asset prices.

Additionally, statements from key political figures regarding potential escalations in tensions added to market jitters. Israeli Foreign Minister Israel Kat’s warnings of retaliation against potential attacks from Iran, in response to provocative statements by Iran’s supreme leader regarding events in Syria, underscored the geopolitical risks facing investors.

In this intricate landscape, the trajectory of the USD/CHF pair remained subject to the interplay of economic data releases, central bank policies, and geopolitical developments. Traders navigated these complexities with careful consideration, weighing various factors to make informed decisions in a market characterized by both opportunity and risk.

GBPUSD – US Economy’s Fed Influence; GBP and BoE Dynamics

Resilient US Economy May Delay Fed’s Rate Cuts; GBP on Edge for BoE Insights. Amidst anticipation of interest rate cuts, the Federal Reserve could face hurdles due to the sturdy performance of the US economy and sustained inflation pressures. The British Pound (GBP) is poised sensitively as any indications of potential rate cuts in May or dovish sentiments from the Bank of England (BoE) could exert downward pressure.

GBPUSD is moving in box pattern and market has reached support area of the pattern

The recent dip in the major currency pair reflects the strengthening of the US Dollar (USD) following unexpected positive outcomes in the US Consumer Price Index (CPI) data for March. Investors are keenly awaiting the upcoming release of the US March Producer Price Index (PPI) and weekly Initial Jobless Claims, while also keeping an eye on the UK’s monthly Gross Domestic Product (GDP) figures slated for later this week.

Release of CPI data underscored the notion that persistent inflationary trends might compel the Federal Reserve (Fed) to rethink its interest rate cut plans. Market sentiment, as per the CME FedWatch Tool, has shifted expectations for the first rate cut from June to September.

March’s CPI figures reveal a 0.4% month-on-month (MoM) increase, driving the annual inflation rate to 3.5%, as reported by the Labor Department’s Bureau of Labor Statistics. Concurrently, the Core CPI, excluding volatile food and energy prices, also exhibited a 0.4% MoM rise and a 3.8% year-on-year (YoY) surge, surpassing market projections.

Conversely, the GBP’s performance hangs in the balance, awaiting the release of the UK’s monthly Gross Domestic Product (GDP) and February Industrial Production data. Market chatter suggests the Bank of England may deliberate a rate cut post its June meeting. Any hints towards May rate cuts or dovish remarks from BoE policymakers could significantly impact the GBP, potentially causing ripples in the GBP/USD currency pair.

EURGBP – Central Bank Expectations and Market Caution

EUR/GBP experienced a gradual descent on Thursday, managing to hover above a recent one-week low, but failing to sustain significant upward momentum. The pound sterling (GBP) faced a ceiling due to expectations of the Bank of England (BoE) adopting a more aggressive policy easing stance, which in turn provided some support to the EUR/GBP pair.

EURGBP is moving in box pattern and market has fallen from the resistance area of the pattern

Traders adopted a cautious approach, refraining from making bold moves ahead of the European Central Bank (ECB) meeting. Despite a modest rebound from the previous day’s low, the EUR/GBP pair encountered fresh selling pressure during the early European trading hours on Thursday. Market sentiment remained cautious as participants awaited the outcome of the ECB meeting, with spot prices oscillating within a narrow range.

The ECB was widely expected to maintain its main refinancing rate, directing attention towards the release of updated staff projections. Investors closely analyzed these projections for hints about the potential timing of future interest rate cuts. Market consensus leaned towards the possibility of a rate cut as early as June, driven by concerns over a more rapid-than-anticipated decline in Eurozone inflation. This sentiment weighed on the euro and consequently exerted downward pressure on the EUR/GBP pair.

In this context, market participants closely monitored the ECB President Christine Lagarde’s post-meeting remarks for insights into the central bank’s future policy direction. Meanwhile, the BoE’s stance played a significant role, with expectations of multiple interest rate cuts throughout the year, starting potentially as soon as June. This expectation acted as a limiting factor for the GBP’s strength, preventing significant losses for the EUR/GBP pair.

From a technical perspective, the failure to sustain gains near the 100-day Simple Moving Average (SMA) suggested a bearish bias among traders. However, given the intricate nature of the fundamental landscape, market participants exercised caution, waiting for clear confirmation of sustained selling pressure before committing to significant downward positions. A continued decline could potentially target key psychological levels or revisit the year-to-date low established back in February.

AUDUSD – Fed Rate Speculation and Inflation

AUD/USD Holds Steady Amidst Fed Rate Cut Speculation and Rising Inflation Expectations

During the early European session on Thursday, the AUD/USD pair manages to find support around a key psychological level. However, the outlook remains uncertain as market sentiment grapples with shifting expectations regarding potential interest rate cuts by the Federal Reserve (Fed) and rising inflation expectations in Australia.

AUDUSD is moving in box pattern and market has rebounded from the support area of the pattern

The AUD/USD pair faces a challenging environment as speculation mounts regarding the Fed’s monetary policy stance. Market participants have been readjusting their expectations for a potential rate cut by the Fed, originally anticipated for June, as recent economic data suggests persistent inflationary pressures in the United States. This shift in sentiment towards delaying rate cuts has led to a strengthening of the US Dollar, putting downward pressure on risk-sensitive currencies like the Australian Dollar (AUD).

Against this backdrop, the AUD/USD pair is holding its ground, supported by technical levels. However, the overall sentiment remains cautious as investors monitor developments in US economic indicators and Fed commentary for further clues on the future trajectory of interest rates.

Meanwhile, in Australia, there has been a notable increase in consumer inflation expectations, adding another layer of complexity to the market dynamics. The Melbourne Institute’s report reveals that inflation expectations for the next 12 months have accelerated to 4.6%, up from the previous reading of 4.3%. This uptick in inflation expectations could influence the Reserve Bank of Australia (RBA) in its monetary policy decisions, potentially impacting the AUD/USD exchange rate.

Overall, the AUD/USD pair is currently navigating through a challenging environment characterized by shifting market sentiment, uncertainty surrounding Fed policy, and domestic inflationary pressures in Australia. Traders are closely monitoring economic data releases and central bank communication for insights into future market movements.

NZDUSD – Chinese Inflation and Fed Speculation

NZD/USD pair experiences a downward movement, influenced by weaker-than-expected Chinese inflation data. China’s Consumer Price Index (CPI) for March shows a mere 0.1% year-on-year (YoY) increase, a notable decline from the previous month’s 0.7% rise and falls short of the consensus estimate of a 0.4% increase. This unexpected softness in Chinese CPI is further underscored by a monthly decline of -1.0% in March, contrasting with the 1.0% increase recorded in the prior month.

NZDUSD is moving in Descending channel and market has fallen from the lower high area of the channel

Similarly, China’s Producer Price Index (PPI) for March registers a 2.8% year-on-year decline, slightly surpassing the 2.7% decrease seen in the previous reading. While this exceeds market expectations, it still reflects ongoing concerns regarding economic slowdown and deflationary pressures within China’s manufacturing sector.

The subdued inflationary pressures in China raise uncertainties about the country’s economic trajectory, potentially limiting the upside for the New Zealand Dollar (NZD) against the US Dollar (USD). Given New Zealand’s economic challenges, including its recent entry into a technical recession and declining consumer confidence, the Reserve Bank of New Zealand (RBNZ) maintains its Official Cash Rate (OCR) at 5.5%, signaling a commitment to restrictive monetary policy to curb inflationary pressures.

Meanwhile, speculation persists regarding a potential interest rate cut by the Federal Reserve in light of the robust performance of the US economy and elevated inflation levels. Market sentiment suggests a 66% probability of a rate cut at the Fed’s September meeting, bolstering the US Dollar and exerting downward pressure on the NZD/USD pair.

As investors await the release of the US Producer Price Index (PPI) for March, they anticipate further insights into inflationary trends and monetary policy trajectories. The outcome of this data release is likely to influence market sentiment and shape future movements in the NZD/USD exchange rate.

CRUDE OIL – Oil Prices Rebound Amid Geopolitical Tensions and Dollar Strength

WTI crude oil is rebounding after experiencing a slight retreat earlier in the week, reflecting the resilience of oil markets amidst ongoing geopolitical tensions. Reports of potential retaliatory actions by Iran against Israeli or US assets in the volatile Middle East region are fueling bullish sentiment among oil traders.

XTIUSD is moving in Descending Triangle and market has fallen from the lower high area of the pattern

At the same time, the US Dollar Index has surged following the release of a robust US inflation report, setting the stage for increased market volatility ahead of the European Central Bank (ECB) meeting.

Thursday sees oil prices continuing their upward trajectory, with expectations of further gains fueled by escalating geopolitical tensions and anticipation of the crucial monthly report from the Organization of the Petroleum Exporting Countries (OPEC). CNN reports heightened alerts from US intelligence regarding potential Iranian attacks in response to recent Israeli airstrikes in Damascus, while Reuters indicates renewed aggression from Iranian-backed Houthi rebels in Yemen targeting vessels in the Gulf of Aden, including a reported attack on a US destroyer.

The resurgence of the US Dollar marks a significant shift in currency dynamics, driven by the stronger-than-expected US Consumer Price Index (CPI) for March. This unexpected inflation surge has effectively ruled out the possibility of any immediate rate cuts by the US Federal Reserve (Fed), casting doubt on previous expectations for multiple cuts throughout 2024. These developments are reshaping market expectations and positioning the US Dollar as a dominant force in the currency markets, particularly in anticipation of the ECB meeting.

The focus later in the day turns to the monthly OPEC report, with market participants eagerly awaiting insights into production levels and any potential policy adjustments. While no significant changes are anticipated, any updates on the extension of existing production cuts could influence oil prices.

Meanwhile, Bloomberg reports that Mexican oil exports remain steady but have yet to fully recover from a sharp decline witnessed in March, underscoring ongoing challenges in the global oil market.

In parallel, both Bloomberg and Reuters highlight US intelligence warnings of imminent major drone and missile strikes by Iran, further adding to market uncertainties. Additionally, Occidental Petroleum Corp. is preparing to resume operations in the Gulf of Mexico following a pipeline leak, signaling potential shifts in supply dynamics.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!