DMART: DMart Surges 7% to Hit New 52-Week High Post CLSA’s Buy Rating

D-Mart Grocery retail company has given upgraded rating by CLSA Brokerage firm, the main reasons are D-Mart selling its lower prices when comparing to peers. D-Mart sell its products with its private labels in most home using products.

Avenue Supermarts shares, the parent company of DMart stores, surged 3% on the BSE, hitting a fresh 52-week high of Rs 4,299 in Friday’s intra-day trading. This upward trend marks the stock’s third consecutive day of gains, rising 7% since CLSA initiated coverage with a BUY rating and a target price of Rs 5,107.

Despite valid investor concerns regarding competition from quick commerce and vertically integrated players, the brokerage has factored these into the stock price. Trading at its highest level since November 2022, the stock previously reached a record high of Rs 5,900 on October 18, 2021.

DMart concluded the December quarter (Q3FY24) with a notable revenue growth of 17.2% compared to the same period last year. Management noted stabilized contributions from General Merchandise and Apparel, with encouraging post-Diwali trends. However, festive season sales were lower than anticipated in Non-FMCG, particularly within FMCG where agri-staples (excluding edible oil) faced significant inflationary pressures.

AVENUE SUPERMARTS Market Price is moving in uptrend line and market has rebounded from the higher low area of the pattern

Offering a diverse array of products across various categories, DMart remains a discount retailer with minimal operating costs, fostering low consumer prices, high sales velocity, and improved scale. This virtuous loop enables DMart to capture market share in a price-sensitive market environment, according to CLSA.

Rapid expansion of its private-label assortment is anticipated to be the next catalyst for share gains. Despite a forward PE multiple of 53.7x FY26CL EPS, one of the highest among large-cap, steady-state businesses, CLSA maintains a positive long-term outlook on DMart, especially considering its recent underperformance compared to broader indices.

In addition, CLSA has observed DMart’s strategic emphasis on increasing private-label offerings over the past year, collaborating with more suppliers for exclusive brands. With exclusive brands spanning a wide range of categories, DMart offers private labels at a significant discount compared to well-known brands, without compromising on quality. This strategic move is perceived as a key differentiator, particularly in comparison to e-commerce and quick commerce platforms, according to CLSA.

NIFTY IT INDEX: Accenture Guidance Cut Drags Down IT Giants: TCS, Infosys, HCLTech Fall

Nifty IT index fell down 6% on Friday after the Accenture IT Company downgraded its revenue growth from 2-5 percent to 1-3 percent. The main reason is clients fears of Geopolitical issues, inflation higher in the economy, $600 billion invested in Gen AI system projects. This results made downfall for our Indian IT index and companies.

Nifty IT Index Market Price has broken Ascending channel in downside

On the National Stock Exchange (NSE), shares of information technology (IT) companies experienced a significant decline of up to 6 percent during Friday’s intraday trading session. This downturn occurred in response to Accenture’s announcement of a reduction in its full-year revenue growth forecast. Accenture, a global consulting and professional services firm, revised its guidance from an initial range of 2-5 percent down to 1-3 percent. This adjustment dealt a blow to hopes of a sectoral recovery in the fiscal year 2024-25.

The Nifty IT index, which tracks the performance of IT stocks, notably emerged as the only sectoral index to incur losses on Friday. It concluded the trading session with a decline of more than 2 percent, contrasting sharply with the marginal 0.4 percent increase observed in the broader Nifty50 index. At its lowest point during intraday trading, the IT index had experienced a nearly 4 percent dip.

The reduction in revenue guidance by Accenture was prompted by its reported revenue of $15.8 billion for the second quarter of fiscal year 2024. This revenue figure remained flat year-on-year (YoY) in constant currency (CC) terms and declined by 2.6 percent sequentially. While this performance aligned with the company’s guidance and Bloomberg consensus estimates, the weak revenue growth forecast for the third quarter and the lowered full-year guidance fell short of Bloomberg consensus expectations. Accenture follows a September-August financial year.

Analysts and industry observers had previously anticipated a growth uptick in the fiscal year 2024-25. However, Accenture’s downward revision of revenue growth guidance, coupled with subdued growth in managed services, indicates that prospective clients are exercising caution in their spending decisions.

Accenture’s revised revenue guidance now incorporates an expected inorganic contribution of 3 percent. The company has made significant investments totaling $2.9 billion in acquiring 23 companies during the first half of its financial year.

Despite the optimism surrounding large-cap IT companies, with expected revenue growth improvement in fiscal year 2025 compared to the preceding year, analysts at Nomura maintain a cautious stance. They anticipate that any revenue growth in the coming fiscal year will primarily stem from cost take-out deals, rather than discretionary demand recovery.

Accenture’s management highlighted that clients continue to navigate through an uncertain macroeconomic environment marked by economic, geopolitical, and industry-specific challenges. In response to these challenges, clients are strategically prioritizing larger transformations and digital core enhancement initiatives to enhance productivity and allocate more investment towards growth-oriented endeavors with short-term returns on investment (RoI).

Additionally, Accenture’s results revealed that while deals in generative artificial intelligence (GenAI) are being awarded, they are being funded at the expense of other deals. The company reported booking over $600 million in GenAI deals, bringing the total to $1.1 billion in the first half of its financial year.

However, other factors contributing to softness in the tech industry, such as sluggish growth in key regions like North America and EMEA (Europe, Middle East, and Africa), continue to weigh on the Indian IT sector. For instance, North America experienced flat sequential growth, while EMEA declined by 2 percent. The ongoing slowdown in the financial services sector, particularly in banking, financial services, and insurance (BFSI), has further exacerbated the challenges faced by Indian IT firms.

Looking ahead, large IT services companies are expected to approach fiscal year 2025 with cautious guidance, with growth prospects varying considerably across companies based on factors such as mega-deal ramp-ups, vertical exposure, and discretionary spending trends. While the ramp-up of large deal wins may support growth for select Indian companies in fiscal year 2025, the persistent weakness in discretionary spending poses a risk to high single-digit growth expectations for large-cap IT firms.

Accenture’s workforce also witnessed changes, with a sequential drop of 723 employees reported at the end of the second quarter of fiscal year 2024. Additionally, the company’s attrition rate rose to 13 percent for the second quarter, up from 11 percent in the preceding quarter.

SKIPPER: A Vertex trading company is the promter group of Skipper company, buying more stake in its own company worth and increased its stake to 5.02% from 4.86%.

SKIPPER LTD Market Price is moving in Uptrend line and market has rebounded from the higher low area of the pattern

Skipper Company bought the project worth of Rs.737 crore from Power Grid Corporation for Transmission and distribution of Power lines. Company said Rs.3900 order book currently has in our company. We are concentrating other than this power lines, we are focussed on Pipes business also.

Skipper’s stock continued its upward momentum on Friday, surging by 12.7% to reach Rs 292 on the BSE. This marks a significant increase of nearly 22% since Wednesday’s closing price. The surge follows an announcement that Skipper’s promoter group entity, Ventex Trade Private Ltd, has increased its stake in the company from 4.86% to 5.02% over March 19-20.

Ventex Trade acquired 114,000 shares of Skipper on March 19, raising its stake to 4.96%. This was followed by an additional purchase of 66,000 shares on March 20, further increasing the stake to 5.02%. The total value of these acquisitions amounted to Rs 2.52 crore.

As of February 19, 2024, the overall promoter holding in the company stood at 66.26%.

Despite hitting a 52-week high of Rs 400 on February 26 this year, the stock has since declined by 27%.

On February 25, Skipper secured a significant order worth Rs 737 crore from Power Grid Corp for a 765 kV transmission line project. Management highlighted that this order significantly strengthened Skipper’s order book in the transmission and distribution (T&D) domain, contributing to a year-to-date order intake of over Rs 3,900 crore.

Skipper operates across three business verticals, primarily focusing on power transmission and distribution, polymer pipes, and infrastructure projects. Its power transmission and distribution business accounted for 72% of revenue from April to December 2023. Additionally, Skipper reported robust financial performance in Q3FY24, with an 80% yearly revenue growth to Rs 801.58 crore and a 115% yearly increase in net profit to Rs 20.47 crore.

During the current quarter, the company successfully concluded a rights issue of 1.03 crore partly paid-up equity shares at Rs 194 apiece, raising nearly Rs 200 crore.

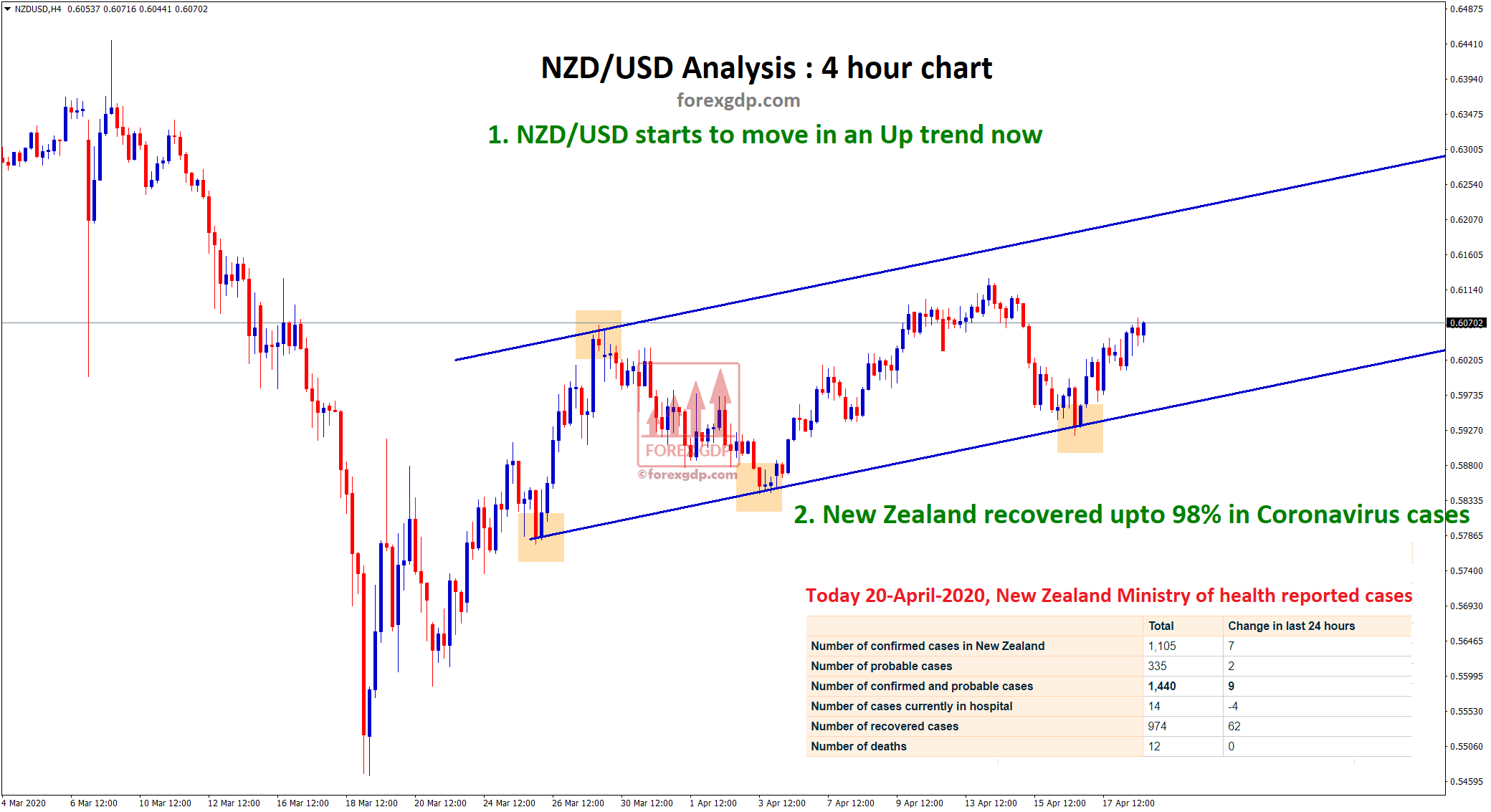

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/