XAUUSD – Gold’s Ascent Fueled by Mixed Manufacturing Data and Dwindling Treasury Yields

The ascent of gold finds its fuel in the latest manufacturing Purchasing Managers’ Index (PMI) reports, which underscore a promising outlook. S&P Global’s revelation of manufacturing conditions reaching their most robust since July 2022 sends a ripple effect, propelling gold prices higher.

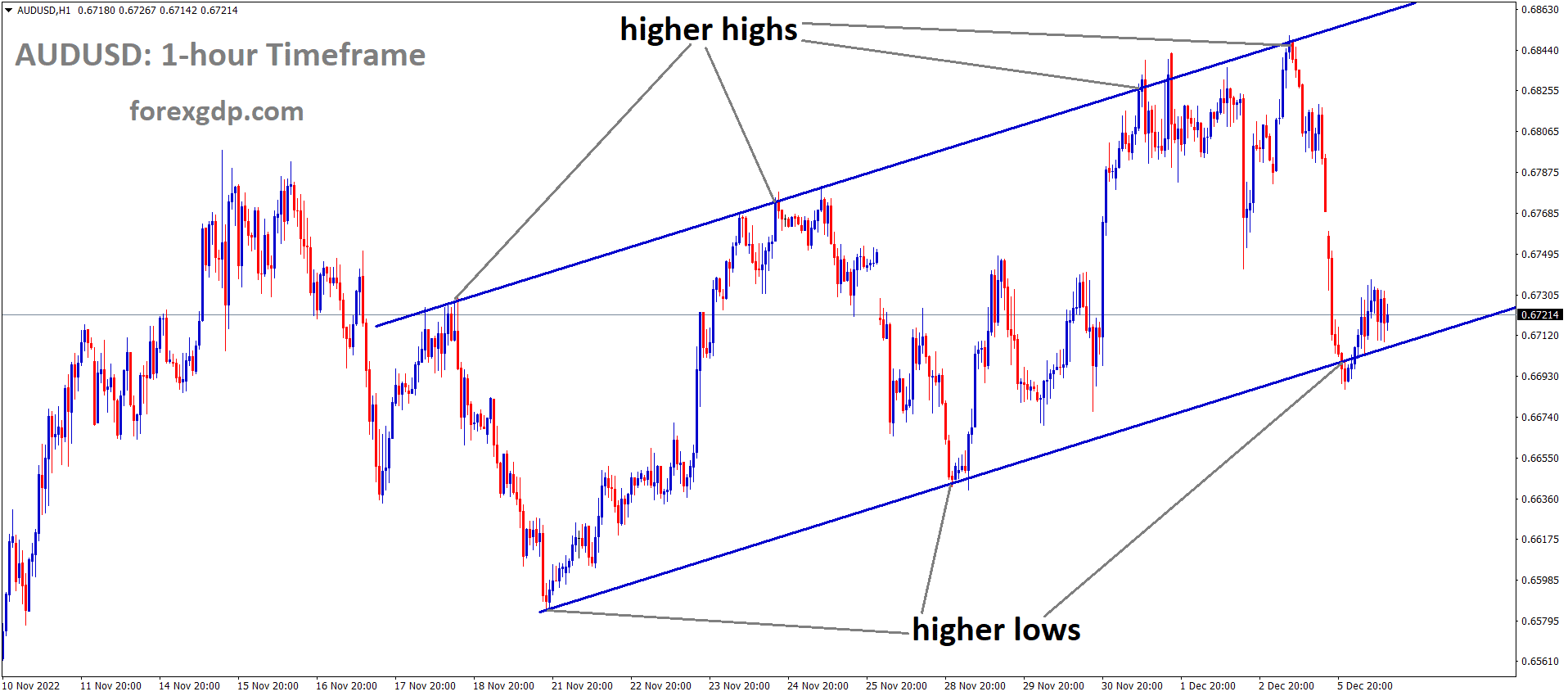

XAUUSD has broken Descending channel in upside

February’s Manufacturing PMI climbed to 52.2 from 50.7, marking an encouraging surge. Chris Williamson, the Chief Business Economist at S&P Global, expressed optimism, noting signs of recovery in the goods-producing sector after a prolonged period of stagnation. However, juxtaposing this buoyancy, the Institute for Supply Management’s (ISM) data delivers a contrasting narrative. The ISM February Manufacturing PMI plummeted to 47.8 from 49.1, signifying a contraction and a swifter downturn compared to January. Timothy Fiore, Chair of the Institute for Supply Management, pointed out the concerning indicators: slowing demand, easing output, and accommodative inputs, all contributing to the sector’s contraction. This duality in manufacturing reports becomes a pivotal factor driving gold prices, especially as US Treasury yields decline, making gold even more appealing.

The dip in US Treasury yields, notably the 10-year bond yield, which fell by five and a half basis points to 4.197%, adds to gold’s allure. Real yields, measured by 10-year Treasury Inflation-Protected Securities, witnessed a parallel drop from 1.934% to 1.878%. The resultant decline in the US dollar further accentuates gold’s attractiveness. Market sentiment regarding interest rate adjustments undergoes a notable shift, reflected in the CME FedWatch Tool’s probability metrics. Traders increasingly anticipate a rate cut as early as June, with probabilities reaching 53.2% at the time of assessment. Federal Reserve officials’ commentary provides further insight into the evolving monetary policy landscape. Divergent views emerge, ranging from Atlanta Fed President Raphael Bostic’s advocacy for prolonged rate hikes to Richmond Fed President Thomas Barkin’s cautious approach towards easing policy. While some, like San Francisco Fed President Mary Daly, emphasize the readiness to adjust rates in response to data, others, such as New York Federal Reserve President John Williams, underscore the importance of incoming data in shaping policy decisions.

XAGUSD has broken and retested the lower high area of the descending channel

The economic data landscape presents a mixed bag of indicators, ranging from fluctuations in inflation metrics to diverging trends in jobless claims and housing market activity. These data points add layers of complexity to the ongoing discussions within the Federal Reserve regarding the appropriate course of action. Looking ahead, market participants brace for upcoming data releases, including ISM Services PMI, Factory Orders, Initial Jobless Claims, and Nonfarm Payrolls. These indicators are poised to influence market sentiment and further shape expectations regarding monetary policy adjustments.

EURUSD – Rebounds on Surging Eurozone Inflation, Central Bank Speculation

The EUR/USD pair rebounds from its weekly lows, driven by a surge in Eurozone inflation figures that surpass market expectations. Amidst this backdrop, both European and US bond yields experience an uptick, lending support to the euro as anticipation mounts regarding potential policy moves by the European Central Bank (ECB) and the Federal Reserve.

EURUSD is moving in box pattern and market has rebounded from the support area of the pattern

Market sentiment is notably influenced by remarks from key figures within these central banks, adding further complexity to the evolving narrative on monetary policy. The release of Eurozone inflation data during the mid-European session unveils figures that, while slightly lower, manage to surpass economists’ projections. The EU Harmonized Index of Consumer Prices (HICP) registers a year-on-year increase of 2.6%, exceeding the forecasted 2.5%. Additionally, the Core HICP rises by 3.1% year-on-year, surpassing the consensus of 2.9% but falling short of January’s 3.3%. This data triggers a rise in yields across both European and US markets, serving as a catalyst for the EUR/USD pair’s upward trajectory. Market participants continue to anticipate potential rate cuts in 2024, with projections pointing towards the likelihood of the first cut occurring in June. Analysts at institutions such as Nordea and Commerzbank speculate on the ECB gradually reducing rates, underpinned by expectations of imminent wage increases.

In response to the inflation data, ECB’s Robert Holzmann emphasizes the need for caution, stressing the importance of carefully weighing decisions regarding interest rates in light of inflationary risks. Meanwhile, across the Atlantic, Richmond Fed President Thomas Barkin adopts a more hawkish stance, expressing reservations about potential rate cuts in the near term. Barkin underscores the importance of consistent economic data in shaping policy decisions, indicating a reluctance to hastily ease monetary policy. Amidst these deliberations, S&P Global reports a robust expansion in manufacturing activity for February, with the PMI climbing from 50.7 to 52.2. However, this optimism is somewhat tempered by the Institute for Supply Management’s (ISM) revelation of a lower-than-expected Manufacturing PMI for February, further contributing to the nuanced dynamics influencing market sentiment.

Recent economic indicators pointing towards a downturn are reigniting speculation about potential rate cuts by the Federal Reserve (Fed), injecting fresh optimism into the market. In contrast, the Fed’s latest Monetary Policy Report suggests a growing confidence within the central bank regarding the attainment of the 2% inflation target. Despite economic headwinds, the European Harmonized Index of Consumer Prices inflation experienced a lesser decline than anticipated in February, offering a glimmer of support for sentiment surrounding the Euro.

USDJPY is moving in box pattern and market has fallen from the resistance area of the pattern

Notably, the Pan-European Core HICP inflation surpassed expectations for the year ending February, posting a robust 3.1% year-on-year compared to forecasts of a decline to 2.9% from the previous 3.3%. Although the headline year-on-year HICP inflation retreated slightly to 2.6% against the forecasted 2.5%, previously at 2.8%, it still remains within range. Additionally, February’s US ISM Manufacturing Purchasing Managers’ Index (PMI) slipped to 47.8, diverging from forecasts of an increase to 49.5 from the previous 49.1. The University of Michigan’s Consumer Sentiment survey index for February also dipped to 76.9, falling short of the steady forecast of 79.6. Further contributing to the narrative of economic softening, the ISM Manufacturing Prices Paid for February declined to 52.5, contrasting with expectations of a slight uptick to 53.0 from the previous 52.9. Looking ahead, the focus shifts to next week’s US Nonfarm Payrolls report scheduled for Friday, with the ADP Employment Change preview set for Wednesday. Additionally, anticipation builds for the European Central Bank’s forthcoming rate decision, poised to impact market dynamics in the coming week.

GBPUSD – US Manufacturing Dip Boosts GBP/USD, Fed Rate Cut Hopes

Amidst a surge in broad-market risk appetite, the Greenback finds itself on a downward trajectory. This decline comes as the US ISM Manufacturing Purchasing Managers Index experienced a setback in February, indicating a softening of price pressures within the sector.

GBPUSD is moving in Descending channel and market has reached lower high area of the channel

The GBP/USD currency pair witnessed a sudden uptick on Friday following an unexpected decline in the US ISM Manufacturing PMI. This surprise dip reignited investor appetite for risk, fueled by optimism that easing inflationary pressures could prompt the Federal Reserve (Fed) to embark on a series of interest rate cuts.

The prevailing sentiment surrounding the PMI data has reignited hopes among investors for potential rate cuts by the Fed. These expectations are further reinforced by the Fed’s latest Monetary Policy Report, wherein the central bank reiterated its position that inflation is gradually edging closer to the upper limit of the 2% target range.

Looking ahead, both this week and the next are expected to witness limited economic releases from the UK, which may have a subdued impact on the performance of the Pound Sterling. However, attention is likely to shift towards next week’s robust labor market data from the US.

GBPCAD is moving in Ascending channel and market has reached higher low area of the channel

Key events on the agenda include the release of the Services component of the ISM PMI figures on Tuesday, followed by the ADP Employment Change preview for February on Wednesday. The week will culminate with the highly anticipated release of the US Nonfarm Payrolls report, expected to provide crucial insights into the health of the labor market. Traders are poised to closely monitor these events for potential market-moving developments.

EURGBP – Eurozone Inflation Surges: ECB Decision Looms

In a twist of economic events, the Harmonized Index of Consumer Prices (HICP) within the EU exhibited a faster growth rate than initially anticipated throughout February. As investors digest this unexpected surge, attention now shifts towards the forthcoming European Central Bank (ECB) decision scheduled for next week, with market sentiment already factoring in a status quo stance.

EURGBP is moving in Ascending channel and market has reached higher low area of the channel

February’s inflation data for the Eurozone surpassed expectations, marking a notable uptick in the headline rate, which climbed by 2.6% year-over-year. This exceeded the forecasted 2.5% and represented a slight retreat from January’s 2.8%. Meanwhile, core inflation, which strips away volatile elements, also outpaced predictions, registering at 3.1% year-over-year compared to the anticipated 2.9%. Despite this, it marked a decline from January’s 3.3%. These figures paint a picture of inflation’s gradual moderation, albeit with a nonlinear trajectory.

Market expectations regarding upcoming ECB meetings suggest a growing anticipation for potential easing measures, with June looming as a probable starting point for such actions. However, for the immediate future, the consensus leans towards the ECB maintaining its current policy stance. The likelihood of a rate cut in April remains subdued, hovering around a modest 25% probability.

In contrast, the Bank of England appears to be postponing its inaugural rate cut until August, a factor that seems to provide a marginal advantage to the Pound. This delay in monetary action reflects a cautious approach from policymakers amid ongoing economic uncertainties. As markets weigh these developments, currencies are poised for potential fluctuations in the days ahead.

USDCAD – US Manufacturing Dips, USD/CAD Reacts Ahead of BoC Decision

Despite a recovery in Canada’s Manufacturing Purchasing Managers’ Index (PMI), indicating improvement, the sector still remains in contraction. Meanwhile, across the border, the US ISM Manufacturing PMI experienced a decline, contrary to expectations, signaling potential challenges for the industry.

USDCAD is moving in Ascending channel and market has rebounded from the higher low area of the channel

The USD/CAD currency pair stumbled below the 1.3600 level on Friday following the disappointing US ISM Manufacturing PMI release for February. This unexpected downturn in the US Dollar (USD) led to a broad decline, pushing the USD/CAD pair back into familiar technical levels.

Although Canada observed an uptick in its S&P Global Manufacturing PMI, market attention remained fixated on the pivotal data releases from the United States. Looking ahead, investors await the Bank of Canada’s (BoC) latest interest rate decision scheduled for the following Wednesday. Additionally, the upcoming week will conclude with the release of both US Nonfarm Payrolls (NFP) and Canadian labor figures, adding further momentum to the market.

Canada’s S&P Global Manufacturing PMI for February showed a modest improvement, rising to 49.7 from the previous month’s 48.3. However, the index still remains below the 50.0 threshold, indicating ongoing contraction within the sector.

In contrast, the US ISM Manufacturing PMI for February disappointed, dropping to 47.8 compared to the anticipated increase to 49.5 from 49.1, highlighting potential challenges within the US manufacturing landscape.

USDCHF is moving in Descending channel and market has reached lower high area of the channel

The University of Michigan Consumer Sentiment survey index also registered a decline, slipping to 76.9 in February from the expected hold at the previous month’s 79.6, suggesting a possible weakening in consumer confidence.

Furthermore, the ISM Manufacturing Prices Paid index dipped to 52.5, lower than both the forecasted 53.0 and the previous month’s 52.9, indicating easing pressure on manufacturers’ input costs.

AUDCAD is moving in Descending channel and market has reached lower high area of the channel

The easing trend in economic data is fostering increased investor risk appetite, as softer inflation figures raise the likelihood of a Federal Reserve (Fed) rate cut. As market participants digest these developments, they may adjust their positions accordingly in anticipation of potential monetary policy shifts.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/