XAUUSD – Gold Poised for Bullish Weekly Close Amid Elevated US Unemployment Rate

Gold prices continues to higher at $2180 last day after the US Labor data shows disappointment in the market. Lower Wage growth and higher unemployment rate makes fears in the US economy recession mode. Two days FED Powell also Disappointment outcome for US Dollar.

A Potential Shift in Monetary Policy: US Dollar Weakens as Fed Considers Rate Cut

Amidst a notable deceleration in wage growth and an elevated Unemployment Rate, market expectations for the Federal Reserve (Fed) to initiate a reduction in interest rates during the June policy meeting are gaining traction.

The United States Bureau of Labor Statistics (BLS) recently reported an increase in the Unemployment Rate to 3.9%, surpassing expectations and exceeding the previous reading of 3.7%. However, the Nonfarm Payrolls (NFP) for February exceeded expectations at 275,000, although it remained below the previous reading of 353,000.

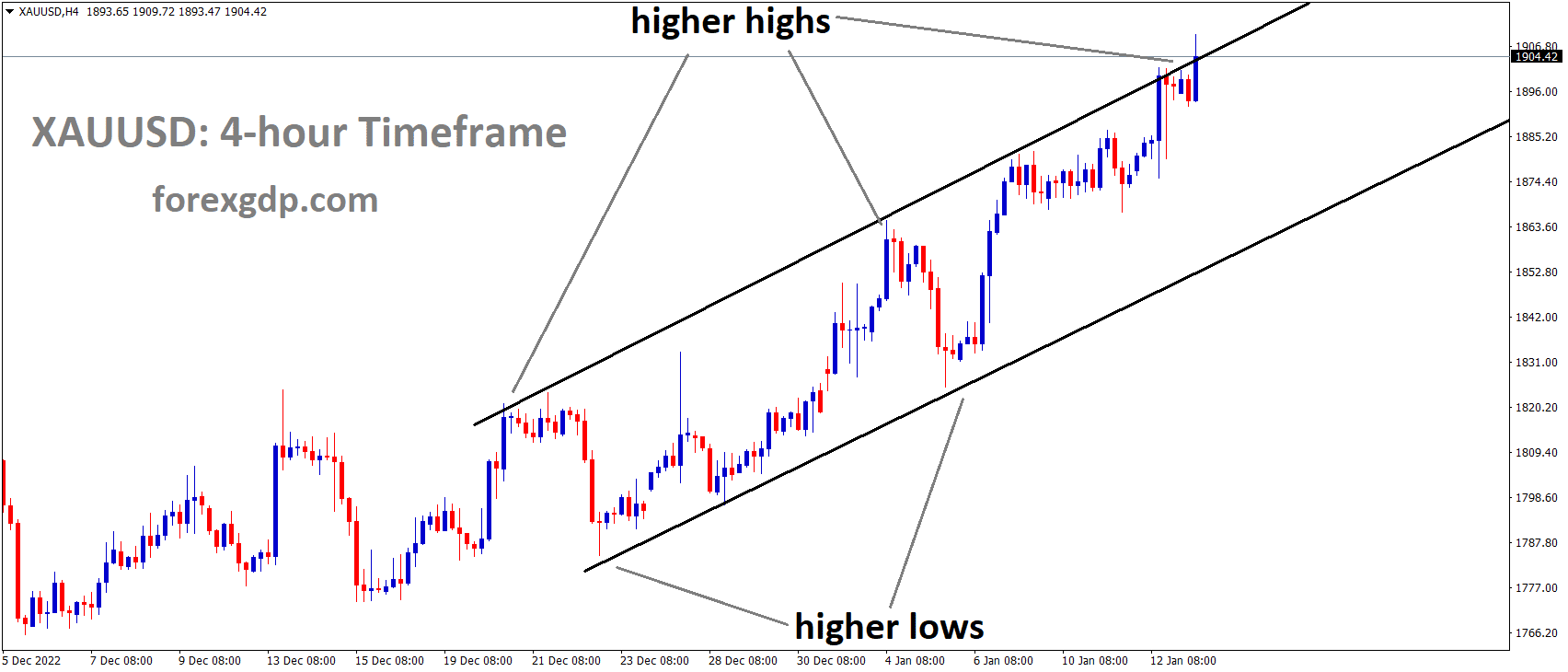

XAUUSD is moving in Ascending channel and market has rebounded from the higher low area of the channel

The inflation outlook is anticipated to cool down as Average Hourly Earnings grew slower than anticipated. Monthly wages saw a modest increase of 0.1%, contrasting with a 0.6% rise in January. Market projections of a 0.3% growth in wage growth were halved. Additionally, annual wage growth decelerated to 4.3%, falling short of expectations and the prior reading of 4.4%. January’s wage growth has been revised down from 4.5%.

The combination of slower wage growth and a higher jobless rate has intensified selling pressure on the US Dollar. The US Dollar Index (DXY), tracking the Greenback against major currencies, hit a seven-week low around 102.40.

During the European session, the precious metal, Gold, exhibited strength as Fed Chair Jerome Powell hinted at the central bank nearing confidence in sustainable inflation returning to the 2% target. Powell stated during his two-day testimony before Congress that they are close to gaining confidence and, when achieved, will dial back the restrictive monetary policy stance to prevent an economic recession.

In the daily digest of market movers, Gold reached a fresh all-time high near $2,180, driven by a downbeat US jobless rate, slightly dovish commentary from Powell, and geopolitical tensions. Powell’s testimony built confidence among investors that rate cuts could be announced sooner, with expectations for the Fed to reduce interest rates in the June policy meeting remaining firm. New York Fed Bank John Williams also acknowledged the downward pressure on aggregate demand due to restrictive monetary policy.

Geopolitical tensions in the Middle East further escalated as Iran-backed Houthis caused the death of three civilians on a merchant ship in the Red Sea, adding to the overall risk in the region.

EURUSD – Hits New High, Retracts on Mixed US NFP Impact

The Euro zone Q4 GDP data came at 0.0% and it is inline with expected reading, German PPI reading January month came at -4.4% from -5.1% decline in December month. The Euro currency lifted up after the data showing positive hints in the market.

EURUSD is moving in uptrend line and market has fallen from the high of the pattern

The bullish momentum witnessed initially faced a setback as investors digested the complexity of the US Nonfarm Payrolls (NFP) report, revealing a more intricate picture than the initial reaction suggested.

While the US NFP showcased job additions surpassing expectations for February, the optimism was dampened by a substantial downward revision to the previous month’s figures, bringing it down from an 11-month high. Simultaneously, European final Gross Domestic Product (GDP) figures largely met expectations, prompting market attention to shift towards the forthcoming Consumer Price Index (CPI) inflation prints for both the United States and the euro area scheduled for next Tuesday.

Breaking down the specifics of the US NFP data for February, it revealed the addition of 275,000 new jobs, exceeding the forecasted 200,000. However, the figure marked an increase over the revised lower January print, which had initially peaked at an 11-month high of 353,000 but was revised sharply downward to 229,000. Notably, US Average Hourly Earnings growth in February slowed more than anticipated, registering at 0.1% MoM, below the expected 0.3% and a decline from the previous month’s 0.5%. The annualized Average Hourly Earnings also eased to 4.3%, missing the forecast of 4.4%, with the previous period undergoing a slight downward revision from 4.5% to 4.4%.

On the European front, the final Gross Domestic Product (GDP) figures for the European Union (EU) remained unchanged from the preliminary release, with Q4’s Quarter-on-Quarter (QoQ) GDP holding steady at 0.0%. In an unexpected turn, Germany’s Year-on-Year (YoY) Producer Price Index (PPI) showed signs of recovery in January, recording a figure of -4.4%, surpassing the anticipated decline to -6.6% compared to the previous month’s -5.1%.

USDCAD – Weak Week for US Dollar: Closes Lowest Since December Amid Mixed NFP

US Dollar index closed at weak price after the mixed bags of Labour data printed at last day. FED Powell testimony is also added fears of economic recession in the US. So US Dollar suffered losses after the US Unemployment rate moved to 3.9% in February from 3.7% in January. NFP Data printed at 275K jobs added versus 200k Jobs expected.

USDCAD is moving in Ascending channel and market has reached higher low area of the channel

Markets Anticipate Easing Cycle Despite Mixed NFP: USD Vulnerable to Additional Losses

Despite the February Nonfarm Payrolls (NFP) report revealing an increase in the US Unemployment rate and a mild easing of Earnings, investors are still optimistic about the easing cycle potentially commencing in June. In the upcoming session, the US Dollar (USD) may face further losses as concerns over an economic slowdown linger.

Breaking down the specifics highlighted in the daily digest of market movements, the NFP figures for February, reported by the US Bureau of Labor Statistics, surpassed expectations by reaching 275,000, a significant increase from the anticipated 200,000. While this indicated robust employment growth, the negative aspects included a rise in the Unemployment rate for February to 3.9%, exceeding expectations set at 3.7%. Additionally, Wage inflation, measured by the Average Hourly Earnings, fell short of the consensus, registering a 4.3% year-on-year increase.

The performance of US Treasury yields demonstrated a mixed picture, with the 2-year yield at 4.48%, the 5-year yield at 4.06%, and the 10-year yield at 4.09%. Despite these fluctuations, the CME FedWatch Tool indicates that the likelihood of Fed interest rate cuts in March and May remains low. The market’s focus is now on preparing for the potential initiation of the easing cycle in June.

USDCHF – Goolsbee of Fed Advocates Lower Rates Amid Falling Inflation

The Chicago FED President Austan Goolsbee said FED must do rate cut in the monetary policy settings once inflation reading has to cool down from current reading. No hurry for rate cuts at this moment. It is unrealistic the reading has to come down to pre-pandemic levels, So be realistic to data in patience manner.

USDCHF is moving in Ascending channel and market has reached higher low area of the channel

Chicago Fed President Goolsbee Expects Lower Rates Later This Year as Inflation Cools

Austan Goolsbee, President of the Chicago Federal Reserve (Fed), anticipates a reduction in interest rates later this year as inflation cools. Goolsbee shared his insights on the Fed’s rate outlook during an interview with Fox News on Friday, marking the last scheduled speaking engagement from Fed officials before the media blackout period preceding the March 19-20 policy meeting.

Key Points:

– The Fed maintains its focus on inflation rather than absolute price levels.

– Goolsbee acknowledges the unrealistic expectation for prices to immediately return to pre-COVID levels.

– Higher rates are identified as contributors to increased housing costs.

In summary, Goolsbee foresees a decline in rates in response to falling inflation throughout the year.

EURCHF – HSBC: Expected to Continue Ascending in the Short Term

Analysts at HSBC said Swiss Franc can depreciate further in coming weeks due to Lower inflation and Lower unemployment rate in Swiss Zone. The SNB most like to rate cuts in upcoming meetings this will impact Swiss Franc against counter pairs.

EURCHF is moving in Descending channel and market has reached lower high area of the channel

HSBC Economists Assess Swiss Franc Outlook: Expectations for USD/CHF to Rise, EUR/CHF to Consolidate

According to economists at HSBC, the Swiss Franc (CHF) is facing a mixed outlook.

The EUR/CHF pair is anticipated to move sideways, reflecting the impact of the CHF’s underperformance linked to its safe-haven status. The Swiss Franc has also been influenced by the Swiss National Bank’s (SNB) altered stance on the currency, with foreign exchange (FX) strength no longer serving as a policy tool or aspiration.

In the near term, HSBC maintains a bullish view on USD/CHF, expecting it to ascend. Conversely, they project the EUR/CHF pair to exhibit a consolidating trend.

EURJPY – Natixis: Three Reasons Why Yen Depreciation Benefits Japan

According to Natixis analysis, weak Yen is best for the Japanese Economy, Japan is doing expansionary policy when compared to other countries doing restrictive monetary policy. Weak Yen is supportive for Japanese Exports and keep inflation level below 2% target. Upcoming Restrictive policy will hurt Japanese exports but Wage price will equal to inflation price is better for rate hike.

EURJPY is moving in Ascending channel and market has reached higher low area of the channel

The Japanese Yen’s Decline: Natixis Analysis on the Benefits for Japan

Natixis analysts elucidate the advantages of Japan’s weakened Yen against the US Dollar (USD) and the Euro (EUR) since the beginning of 2021. Despite the Bank of Japan lacking motivation for Yen appreciation, the country’s expansionary monetary policy, in contrast to other OECD nations adopting restrictive measures, has led to a significant depreciation of the Yen. In reality, this depreciation proves beneficial for Japan’s economy by aiding in achieving the 2% inflation target, stimulating exports, and generating capital gains on Japan’s substantial net external assets, primarily in Dollars and Euros.

Given these positive impacts, there is little expectation for Japan to transition to a more restrictive monetary policy. At most, a symbolic increase in the Bank of Japan’s base rate may be anticipated.

GBPUSD – GBP Surges on Upbeat Market Sentiment Boosted by Sluggish US Wage Data

The Bank of England rate cuts is expected from August month later than FED rate cuts in June month. The BoE said Wage reading is double than what we expected, So Wage reading is scheduled next week, Robust Wage growth in the UK makes BoE to keep rates at hold process than rate cuts.

GBPUSD is moving in uptrend line and market has rebounded from the higher low area of the pattern

The Pound Sterling (GBP) Strengthens on Improved Market Sentiment Following Soft US Wage Data

In the early American session on Friday, the Pound Sterling (GBP) experienced a surge as market participants embraced a more positive risk appetite. This shift was influenced by the release of the United States Bureau of Labor Statistics (BLS) report, indicating sluggish wage growth and a significant rise in the Unemployment Rate for February.

The GBP/USD pair remains in favor, supported by the expectation that the Federal Reserve (Fed) will implement interest rate cuts before the Bank of England (BoE). This expectation contributes to a temporary reduction in the policy divergence between the two central banks.

While market projections anticipate a Fed rate cut in June, investors foresee the BoE reducing interest rates starting in August. The UK continues to exhibit higher inflation than other Group of Seven (G-7) nations, primarily due to robust wage growth driving sticky services inflation.

Looking ahead, the UK’s Average Earnings data for the three months ending in January will play a crucial role in shaping the inflation outlook. Robust wage growth would potentially diminish expectations of a rate cut. BoE policymakers caution that wage growth remains nearly double the level needed for inflation to return to the 2% target.

In the context of daily market movements, the Pound Sterling extended its upward trajectory, reaching a seven-month high at 1.2840. This occurred amid a risk-on sentiment ahead of the pivotal US Employment data release for February.

As economists anticipate US employers adding 200K jobs, lower than January’s robust 353K, the Unemployment Rate is expected to remain at 3.7%. Investors are particularly interested in the Average Hourly Earnings data, as it provides insights into the inflation outlook.

The GBP/USD pair is poised for weekly gains, primarily attributed to the weakened appeal of the US Dollar. Looking forward, the Pound Sterling’s direction will be influenced by the UK’s labor market data for the three months ending in January, offering cues regarding the potential timing of the BoE’s interest rate reduction, currently anticipated in August.

BoE policymakers refrain from specifying a timeframe for interest rate cuts, emphasizing the need for confidence in a sustainable return of inflation to the 2% target. Additionally, UK house prices have risen for the fifth consecutive month, supported by a recent decline in mortgage rates and expectations of impending rate cuts.

On the other side of the Atlantic, the US Dollar faces significant pressure following the release of the Nonfarm Payrolls (NFP) report for February. The Unemployment Rate increased to 3.9%, surpassing expectations and the January reading of 3.7%. Although US employers added 275K workers, lower than the previous 353K, it still exceeded market expectations of 200K.

The soft Average Hourly Earnings data, expected to cool down the inflation outlook, has intensified the pressure on the US Dollar. Monthly wage growth was a mere 0.1%, falling short of expectations of 0.3% and the prior release of 0.6%. Annual wages rose at a slower pace of 4.3%, below expectations and the previous reading of 4.4%. The January wage growth has been revised down from 4.5%.

GBPCAD – Canadian Dollar Drops vs. Greenback on Volatile NFP Friday

The Canadian Dollar moved down after the Canadian Job report shows higher reading than expected last day. The Jobs creation for February is 40.7K versus 20.0K expected, Unemployment rate higher at 5.8% from 5.7% in January month.

GBPCAD is moving in Ascending channel and market has reached higher high area of the channel

On Friday, significant market turbulence ensued as the Canadian Dollar (CAD) experienced fluctuations against the US Dollar (USD) in response to a mixed set of US Nonfarm Payrolls (NFP) figures and Canadian employment data that were largely overshadowed by the prevailing influence of US economic indicators. The CAD demonstrated a general softening throughout the day, losing ground against all major currencies.

In terms of Canadian employment, the country exceeded expectations by adding more jobs than anticipated in February. However, this positive development was tempered by a slight deceleration in wage growth, coupled with a marginal increase in the Unemployment Rate. Meanwhile, on the US front, an impressive outperformance in the February NFP figures was dampened by a substantial downward revision to January’s job figures, creating a situation where positive sentiments were offset by mixed employment data.

Looking ahead, the upcoming economic calendar for the following week indicates a notable lack of major Canadian releases, shifting market attention to the upcoming update on US inflation. The Consumer Price Index (CPI) for February is set to be unveiled next Tuesday, serving as a pivotal point of interest for investors.

Breaking down the specifics of the NFP data, the US added 275,000 new jobs in February, surpassing the forecasted 200,000. However, the previous month’s NFP figure underwent a significant correction, revised downward from the previous 11-month peak of 353,000 to 229,000. Annualized Hourly Earnings growth for the year ending in February slightly eased to 4.3%, falling short of the anticipated 4.4%, with a minor revision from the previous 4.5%. The US Unemployment Rate also experienced a rise in February, ticking up to 3.9%, deviating from the anticipated steady print at 3.7%.

On the Canadian front, the employment scenario in February revealed a positive note as 40,700 jobs were added, more than doubling the forecasted 20,000 and showing a slight increase from the previous month’s 37,200. However, the Canadian Unemployment Rate also edged higher to 5.8% in February from 5.7%, aligning with expectations. Additionally, Canadian Average Hourly Wages exhibited a year-on-year growth of 4.9%, marking a slight retreat from the previous period’s 5.3%.

AUDUSD – Rises on Varied US Jobs Data and Reduced US Yields

The Australian Q4 GDP data came at 0.40% versus 0.30% expected in Quarter wise reading, 1.5% grew in MoM versus 2.1% previous reading. The Australian Dollar is cheered by US Labor data printed last day.

AUDUSD has rebounded from the low of the pattern

The Australian Dollar strengthens as the US Dollar extends its weekly losses. Recent US Department of Labor data shows Nonfarm Payrolls for February surpassing estimates at 275K, higher than the downward-revised January figure of 229K. The job market cools as the Unemployment Rate rises from 3.7% to 3.9%, and Average Hourly Earnings decline in both monthly and annual measurements.

AUD/USD continues its rally, reaching a daily high of 0.6664, while US Treasury bond yields dip. The US 10-year benchmark note rate hits 4.044%, the lowest level since February 2.

Simultaneously, the US Dollar Index (DXY) drops by 0.25%, reaching 102.52, approaching an eight-week low.

New York Fed President John Williams notes that neutral interest rates are still quite low, attributing the restrictive monetary stance to reduced demand. The Fed aims to achieve price stability, unaffected by political considerations, and sees the 2023 economy as remarkable.

Australian data for the week includes a Trade Balance surplus and a 0.2% QoQ growth in Q4 2023, slightly below the estimated 0.3%. On a yearly basis, the economy expands by 1.5% YoY, surpassing estimates but falling short of the previous 2.1% reading.

NZDUSD – NZD Strengthens Against USD Post Nonfarm Payrolls

US Average wage reading came at 4.3% YoY and 0.10% MoM it is well below the 4.4% YoY and 0.30% MoM last day for February month. Lower Wage reading makes less inflation in US economy and Lower unemployment rate gives FED to rate cuts in this year very soon than expected. NZ Dollar boosted by China trade surplus reading and US Labor data report.

NZDUSD is moving in Ascending channel and market has reached higher high area of the channel

The New Zealand Dollar Gains Against USD Post Nonfarm Payrolls Release

On Friday, the New Zealand Dollar (NZD) strengthened against the US Dollar (USD) following the release of US Nonfarm Payrolls data, indicating disinflationary trends that could prompt an earlier-than-expected interest rate cut by the Federal Reserve (Fed).

The NZD/USD reached a daily high of 0.6218 during the US session post the Bureau of Labor Statistics (BLS) report. The potential for an earlier rate cut by the Fed, driven by the data, poses a negative outlook for the US Dollar, as lower rates tend to attract fewer foreign capital inflows.

Key Points from Nonfarm Payrolls Data:

– While the headline NFP figure displayed the addition of 275,000 jobs in February, surpassing the expected 200,000, other indicators in the BLS report hinted at weaknesses in the labor market.

– Average Hourly Earnings, a crucial component of inflation, rose by a lower-than-anticipated 4.3% YoY and 0.1% MoM, falling below the predicted 4.4% and 0.3%.

– The Unemployment Rate rose to a higher-than-expected 3.9%, deviating from the projected 3.7%.

– These data points suggest reduced inflationary pressure from wages and low unemployment, potentially prompting the Fed to expedite interest rate cuts earlier in the year, with implications of negativity for the US Dollar due to diminished foreign capital inflows.

NZD Supported by China’s Positive Trade Data:

– The NZD received additional support from better-than-expected trade data from China, its largest export partner, on Thursday.

– Chinese Trade Balance data indicated an unexpected increase in the country’s trade surplus to $125.16 billion in February, surpassing expectations of $103.70 billion and the previous month’s $75.34 billion.

– The higher surplus signifies economic health and prosperity, suggesting increased demand for New Zealand exports, particularly milk and dairy products, and subsequently, a rise in demand for the NZD.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/