The Maruti Suzuki fell 2% on Friday ahead of Q4 Earnings, Analysts expected net profit Rs.3916 cr it is 50% from previous quarter and Revenue will be upto 21% as Rs.38772 cr in January- March Quarter. Brokers estimated Cars will be sold 5.84 units in this Jan-March 2024 quarter.It is 13.4% higher than previous quarter as expected from analysts view.

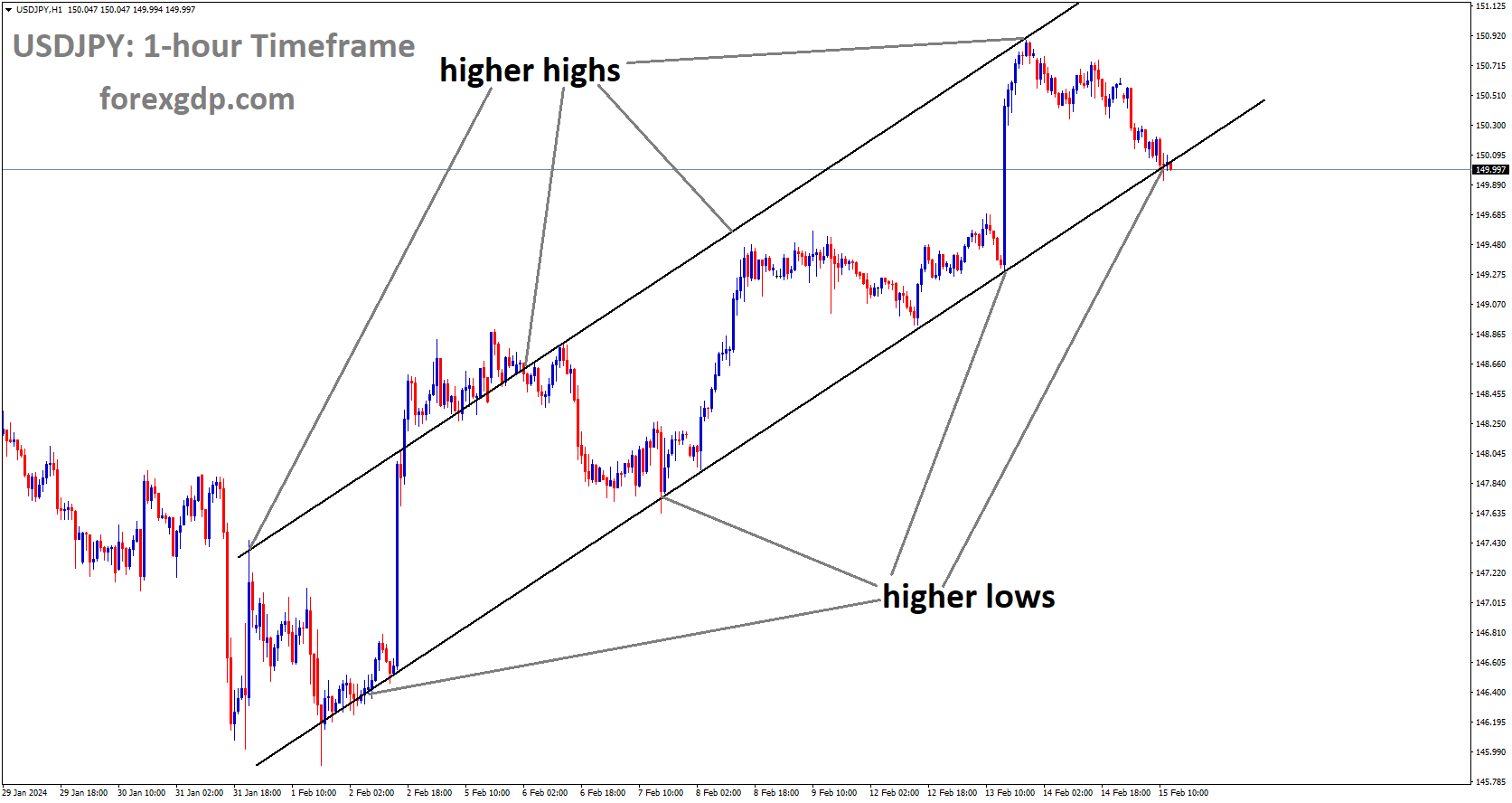

MARUTI SUZUKI Market Price is moving in Ascending channel and market has reached higher low area of the channel

Maruti Suzuki India Limited experienced a 2 percent decline in afternoon trading on April 26, just before revealing its fourth-quarter financial results later that day.

India’s leading automobile manufacturer is anticipated to announce a nearly 50 percent surge in net profit to Rs 3,916 crore, as per a Moneycontrol survey involving nine brokerages. Revenue is projected to climb by 21 percent to Rs 38,772 crore.

Axis Securities noted, “The increase in revenue is expected to be driven by higher overall unit sales, improved product mix, and a greater proportion of SUV and export sales.”

Brokerages estimated that Maruti Suzuki sold 5.84 lakh cars in the January-March quarter, marking a 13.4 percent increase compared to the same period last year.

The demand outlook, particularly for the entry-level segment, is under scrutiny. Analysts foresee a potential decline in sales, particularly for models like Alto and S-Presso, with volumes possibly dropping by 28 percent year-on-year. Compact car volumes, including models such as Ignis, Celerio, and Swift, may experience a milder decline of 3-4 percent.

In January, Maruti Suzuki raised prices across models by up to 0.45 percent. A second increase followed on April 10, with prices rising for Swift and select variants of Grand Vitara Sigma by up to Rs 25,000.

KPCL: Kirloskar Pneumatic stock surges on strong Q4; analysts bullish on growth

The Kirloskar Pneumatics reported robust performance in the Q4 results, Net profit rose to 86.82% as Rs.60.23 cr and Net revenue rose to 36.26% as Rs.489.96 cr. The company has order book of Rs.1770 cr till date, Still the company is planned for Another Rs.400cr order book as forecast.

KIRLOSKAR PNEUMATIC Market Price has broken box pattern in Upside

Good order book now and FY26-27 planned for new products launching plans in India.

Kirloskar Pneumatic’s stock saw a remarkable surge for the second consecutive day, soaring by 18 percent on April 26, reaching a new all-time high at Rs 1,076.7, following the company’s impressive performance in Q4FY24.

In the quarter ended March 2024, the company’s net profit nearly doubled year-on-year, leaping by 86.82 percent to Rs 60.23 crore compared to Rs 32.24 crore in the corresponding period last year. Revenue from operations also witnessed a substantial increase, rising by 36.26 percent to Rs 489.96 crore from Rs 359.58 crore in the same period.

Management highlighted robust demand for the company’s products, with new order bookings for the year reaching a record high of Rs 1,770 crore, approximately Rs 500 crore higher than the previous year. Additionally, the company anticipates securing more than Rs 400 crore of orders per quarter, with a focus on boosting domestic sales and introducing new products to expand the order book.

Looking ahead, management revealed plans to launch new products by 2026-2027, specifically targeting the Tezcatlipoca centrifugal compressor market in India.

Sahil Sanghvi of Monarch Networth Capital expressed optimism about KPCL’s growth prospects, stating, “Adjusted PAT beat our estimates broadly due to the execution of high-margin orders and controlled other expenses. The management is walking the talk with regards to closing the order book that gives us security on strong revenue growth for FY25 (~27 percent), on track to reach Rs 2 billion revenue by FY26 as guided. We remain positive about the growth prospects of KPCL.”

KPCL announced a final dividend of 200 percent at Rs 4 per share, in addition to the interim dividend of 125 percent, bringing the total dividend to Rs 6.5 per share.

Lauras Labs: Analysts Highlight Laurus Labs’ CDMO Services’ Role in Enhanced Prospects

The Lauras Labs sales declined in the CDMO Project is 57% to Rs.922cr but the company expected in the next couple of years CDMO project will improve. Nearly Rs.2600 cr invested in this CDMO project. Contract Development and Manufacturing Organisation project worth $100 million invested so far by the Management said.Supplies from Animal health will started in FY 25 and Crop protection supplements will completed by End of FY 2024. Brokerages and analysts downgraded the scope of CDMO project due to Rivals are more in this segment.

LAURUS LABS Market Price is moving in Descending channel and market has reached lower high area of the channel

Analysts point to Contract Development and Manufacturing Organization (CDMO) services as pivotal for Laurus Labs’ future growth prospects following the release of its fourth-quarter results.

Kotak Securities analysts emphasized, “A significant revival in its EBITDA margin, mainly hinges on a much-improved CDMO performance, from 15.4 percent in FY2024.”

Laurus Labs reported a 26 percent decline in net profit to Rs 76 crore in the March quarter compared to Rs 103 crore a year earlier. However, revenue saw a 4 percent increase to Rs 1,440 crore.

The management disclosed ongoing investments of $100 million in CDMO services, with animal health facility supplies expected to commence in FY25. Additionally, qualification for intermediate manufacturing in the crop protection segment is slated for completion by the end of FY25.

Laurus anticipates CDMO services to contribute one-third of sales in the next few years, with FY24 witnessing a 57 percent decline in CDMO sales to Rs 922 crore due to a high base from the previous year’s large purchase order.

The company is currently validating two APIs (active pharmaceutical ingredients) and plans to file new drug applications for them shortly. It aims to include more late-stage products and expand its project scope, albeit without significant sales contributions expected from potential new CDMO clients in the next year.

Over FY22-24, Laurus Labs invested approximately Rs 2,600 crore in capacity building, including CDMO (Rs 900 crore), API-CDMO combined (Rs 1,040 crore), and drug product/finished dosage form (Rs 650 crore).

While there’s a gradual increase in macro tailwinds for its CDMO segment, Kotak Securities analysts noted delays in crucial CDMO projects beyond animal healthcare and later crop science contracts in FY2026. This lack of visibility on additional commercial CDMO contracts raises concerns.

Motilal Oswal analysts revised their earnings estimate downward, anticipating only a gradual pickup in the CDMO business and factoring in delays in abbreviated new drug approvals and increased competition in the API segment.

Jefferies analysts also lowered the company’s FY25/FY26 estimates by 15 percent and 3 percent, respectively, due to lower CDMO sales.

In contrast, DAM Capital analysts remained optimistic about Laurus Labs’ prospects, expecting sharp EBITDA/PAT growth from FY25 onwards driven by increased revenue/capacity utilization in higher-margin non-antiretroviral/CDMO businesses.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!