AUDUSD is moving in a descending triangle pattern, and the market has reached the lower high area of the pattern

AUD/USD Eases from Highs as Investor Confidence Wavers

The Australian Dollar (AUD) has pulled back slightly after touching its weekly highs against the US Dollar. Even though it lost a bit of momentum, it’s still comfortably trading above the 0.6500 mark. This dip isn’t surprising—currencies often take a short pause after a strong rally. Despite the minor pullback, confidence in the Aussie remains solid, backed by encouraging signs from the Reserve Bank of Australia (RBA) and a noticeable improvement in local consumer sentiment.

Investors, however, seem cautious for now. Many are waiting on updates about the ongoing US government funding situation before making any bold moves. This uncertainty has kept market participants on edge, leading to a more watchful and less aggressive trading approach.

RBA’s Confident Tone Boosts the Aussie Dollar

One of the main factors helping the Australian Dollar stay firm has been the recent hawkish remarks from the RBA Deputy Governor, Andrew Hauser. His comments hinted that Australia’s economy is on a positive track and that the central bank doesn’t want to risk igniting new inflationary pressures by easing monetary policy too much. This strong tone from the RBA reassured traders that the bank remains confident about the nation’s growth and inflation outlook.

Hauser’s words came at a crucial time. With global markets still adjusting to the effects of inflation and tighter financial conditions, investors found comfort in the idea that Australia’s economy could maintain steady growth without needing further intervention. His remarks not only supported the currency in the short term but also strengthened overall optimism about the country’s financial stability.

Consumers Are Feeling Positive Again

Adding more fuel to the Aussie’s resilience was the release of the latest Westpac Consumer Sentiment report. According to the data, Australian consumer confidence surged by 12.8% in November, marking a strong rebound from the previous month’s decline. The index moved above the 100-point threshold, indicating that optimism now outweighs pessimism among consumers.

This improvement in sentiment suggests that households are feeling better about their financial situations and the broader economic outlook. When consumers feel confident, they’re more likely to spend and invest, which can further support domestic growth. This positive trend aligns with the RBA’s view that the economy is steadily recovering, and it gives investors another reason to maintain faith in the Aussie Dollar.

Why Consumer Sentiment Matters

Consumer sentiment is one of the most closely watched indicators because it often acts as a preview of future economic activity. When people are confident, they spend more freely, boosting retail sales, housing, and other key sectors. In Australia’s case, this rebound in sentiment not only signals economic improvement but also reinforces the idea that inflation may remain manageable without additional rate cuts.

Global Market Mood: A Mix of Optimism and Caution

On the global stage, markets have been showing a mixed tone. Earlier optimism came from news that the US Senate passed a bill to resume government funding, effectively ending what could have been one of the largest government shutdowns in history. This development boosted risk appetite in the financial markets, encouraging investors to take on more risk-sensitive assets like the Australian Dollar.

However, Tuesday’s trading session brought a slightly different mood. Despite the earlier enthusiasm, many traders are now standing by, waiting for further progress before making new positions. The bill still needs approval from the US House of Representatives, where it’s expected to pass smoothly given the Republican majority. Once approved, it will move to the President’s desk for signing.

The uncertainty surrounding this process has made some investors cautious. Markets often prefer clarity, and until the funding issue is fully resolved, traders are reluctant to make significant directional bets. As a result, the Aussie Dollar’s momentum has cooled slightly even though the underlying sentiment remains constructive.

The Fed’s Mixed Messages Keep Traders Guessing

Across the Pacific, the US Federal Reserve continues to play a big role in shaping the USD’s movement—and by extension, influencing how the Aussie performs. Recent comments from various Fed officials have been mixed, with some suggesting that policy tightening might continue if inflation remains stubborn, while others lean toward a more patient approach.

This division within the Fed creates uncertainty in the market. For the Aussie, this can be both a risk and an opportunity. If the Fed signals a slower pace of rate hikes or a softer stance, it can weaken the US Dollar, giving the Australian Dollar more room to climb. On the other hand, any renewed talk of aggressive tightening could limit the Aussie’s gains.

For now, though, the flat performance of the US Dollar Index has provided some breathing room for the AUD. It’s keeping the currency close to its recent highs, even as traders remain cautious.

Australia’s Economic Outlook Looks Promising

Looking ahead, the broader picture for Australia remains bright. The economy continues to show resilience despite global challenges. Employment remains stable, consumer confidence is recovering, and the RBA’s focus on maintaining economic balance is reassuring investors. Australia’s strong ties to global trade, particularly in commodities and resources, also give it a steady foundation.

While external factors such as US economic policies and global market sentiment will continue to influence the AUD, domestic strength should help it stay competitive. If the positive consumer outlook continues and the RBA maintains its confident stance, the Australian Dollar could remain one of the more attractive major currencies in the near term.

What Traders Are Watching Next

For traders and investors, the key things to watch in the coming days include:

-

Further developments on the US government funding bill.

-

Any new statements from Federal Reserve officials.

-

Updated data on Australian employment and inflation.

-

Changes in global risk appetite, especially related to geopolitical or economic events.

Each of these factors could play a role in determining whether the Aussie continues its upward path or faces short-term volatility.

Final Summary

The Australian Dollar may have taken a small step back from its recent highs, but the overall story remains positive. Strong comments from the RBA, a rebound in consumer confidence, and a relatively stable US Dollar are all helping to keep the AUD supported. Although uncertainty around US government funding and mixed signals from the Federal Reserve are causing some hesitation among traders, the foundation for the Aussie’s strength remains solid.

In short, while short-term fluctuations are normal, the Australian Dollar’s long-term outlook continues to look optimistic. With growing confidence in the economy and a steady central bank stance, the Aussie remains a currency to watch for those following global markets.

EURUSD steadies as optimism grows after US government reopens

The Euro continues to hover around its familiar territory, moving sideways while the US Dollar gets a slight boost from recent developments in the United States. Market participants seem to be watching closely, waiting for key economic data from both Europe and the US to give clearer direction.

A Breath of Relief for the US Dollar

The United States recently managed to bring an end to the government shutdown, the longest in its history. This event has slightly strengthened the US Dollar, as the reopening of federal offices brings back a sense of stability that the markets were craving. After more than a month of partial closure, many businesses and workers are finally returning to normal, and that alone has created a wave of optimism across financial markets.

The US Senate has already passed a funding package that ensures government operations will continue. It now awaits final approval before being signed by the President. The entire episode reminded everyone how political uncertainty can directly impact the economy, yet once the deal was announced, investors seemed to regain some confidence.

EURUSD is moving in a descending channel

When government operations resume smoothly, spending and productivity naturally improve, which often helps the national currency. That’s exactly what we’re witnessing — a slightly stronger US Dollar against major peers, including the Euro. However, the improvement hasn’t been dramatic, as markets are still cautious, keeping the Euro/Dollar pair within its recent range.

Europe’s Economic Sentiment Comes Into Focus

While the US celebrates the end of its internal standoff, Europe turns its attention toward fresh data that could determine how the Euro performs in the coming days. The German ZEW Economic Sentiment Survey is one of the most closely watched indicators, as it reflects the mood of investors and analysts regarding Germany’s economic future.

A mild improvement in sentiment is expected, showing that confidence among economic experts is slowly recovering. However, despite this optimism, figures remain far below long-term averages, indicating that Europe’s economic recovery still faces challenges.

Germany, being the powerhouse of the Eurozone, often sets the tone for the entire region. Any positive movement in its outlook can bring short-term stability to the Euro, even if the overall environment remains uncertain.

Adding to the mix, European Central Bank (ECB) President Christine Lagarde is scheduled to deliver comments that could influence investor perception. Markets usually pay close attention to her tone — whether she leans toward being cautious or optimistic — as it often hints at the ECB’s future monetary stance.

All Eyes on the US Employment Data

Across the Atlantic, another major factor shaping market sentiment is the US employment report. The ADP employment data, which tracks job creation in the private sector, gives traders an early signal before the official government jobs report.

Recently, a better-than-expected increase in employment numbers helped ease concerns about a weakening labor market. Even though the growth wasn’t massive, it showed resilience in the US economy, which supports the argument that the slowdown many feared might not be as severe as expected.

The US Federal Reserve is also a key player in this story. Several Fed officials have been sharing their views, revealing a mix of opinions within the committee. Some policymakers believe that the economy needs more support through lower interest rates, while others prefer a cautious approach, warning that too much easing could reignite inflationary pressures.

This division creates uncertainty about the Fed’s next move, and such uncertainty often limits large movements in currency pairs like EUR/USD. Until the Fed sends a clearer message, traders are likely to continue reacting to short-term economic releases rather than long-term trends.

The Market Mood: Sideways and Watchful

For now, the Euro seems to be trapped in a sideways pattern. Neither the Eurozone nor the US has produced strong enough signals to push the pair decisively in one direction. The mix of cautious optimism in Europe and moderate recovery in the US keeps the market balanced.

The end of the US government shutdown has undoubtedly brought some relief, but it hasn’t been enough to trigger a major rally. Similarly, Europe’s economic data, while stable, hasn’t inspired enough confidence for the Euro to gain significant ground.

Investors are keeping a close eye on upcoming data releases and central bank commentary to determine where to place their bets next. Many traders prefer to stay patient during such phases, waiting for a clearer breakout before taking larger positions.

The Broader Picture: Hope and Hesitation

The current environment shows an interesting balance between hope and hesitation. On one hand, there’s relief that the US political situation has stabilized, and employment numbers look decent. On the other hand, concerns about global growth, inflation, and central bank decisions are keeping enthusiasm in check.

Europe continues to face structural challenges such as slow growth and geopolitical uncertainty, while the United States grapples with inflation management and fiscal policy tensions. The result is a global market that moves cautiously — making small steps rather than bold leaps.

For everyday investors or traders, this type of market can be tricky. Without clear direction, short-term trades require tighter risk management and patience. Long-term investors, however, might view this stability as a sign that the worst turbulence has passed, and that both regions are gradually finding their footing again.

Final Summary

The Euro and the US Dollar are locked in a delicate balance. The reopening of the US government has given the Dollar a gentle lift, but not enough to overshadow lingering economic concerns. Meanwhile, Europe’s economic sentiment is slowly improving, yet far from the strength needed to spark a strong Euro rebound.

With both regions showing signs of cautious optimism, the EUR/USD pair remains stable for now, reflecting a market that’s still figuring out its next move. Upcoming data releases, particularly from Germany and the US labor market, will play a major role in shaping that direction.

In short, it’s a time of quiet anticipation. The market isn’t ready to celebrate, but it’s also not in panic mode. Traders, analysts, and investors alike are simply waiting for the next solid clue — whether from policy changes, new data, or central bank decisions — to decide which way the wind will blow next.

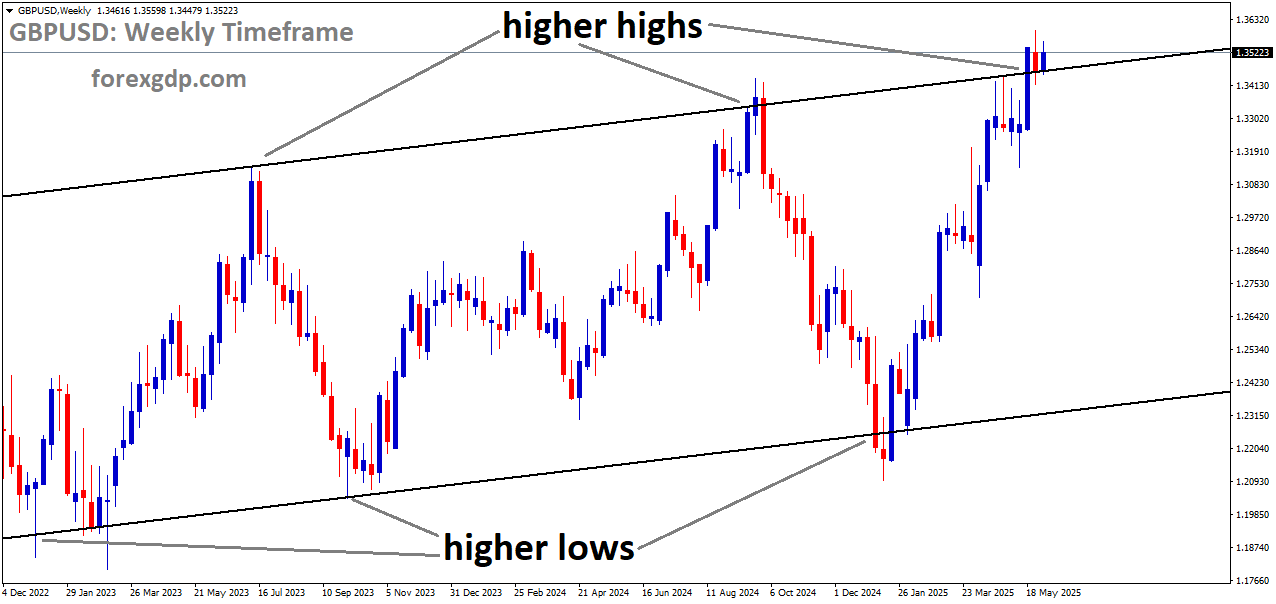

GBPUSD Drops as UK Labor Market Shows Rising Job Losses

The British Pound has had a rough ride lately, and the main reason behind this decline is the disappointing employment data coming out of the United Kingdom. The latest report from the Office for National Statistics (ONS) shows that the UK job market is not as strong as many had hoped. Let’s take a deeper look at what’s happening, why it matters, and what could come next for the Pound and the broader UK economy.

GBPUSD is moving in a downtrend channel

A Weak Job Market Drags Down the Pound

The Pound Sterling fell sharply against other major currencies after the ONS reported that employment in the UK dropped in the three months ending in September. Employers laid off around 22,000 workers during this period, which is a concerning shift compared to the 91,000 new jobs added in the previous three months. This marks the first overall decline in employment since early 2024, signaling that the labour market is losing momentum.

Adding to the worries, the unemployment rate rose to 5%, which is slightly higher than economists’ expectations of 4.9% and the previous rate of 4.8%. This is the highest unemployment rate the UK has seen since March 2021, when the country was still recovering from the economic effects of the pandemic.

A higher unemployment rate generally means fewer people have disposable income, leading to reduced spending and slower economic growth. When this happens, investors tend to lose confidence in the currency, which is why the Pound has been underperforming against its peers like the US Dollar and the Euro.

What’s Fueling the Economic Slowdown?

Fewer Jobs and Slower Wage Growth

One of the key concerns for economists is that the pace of wage growth in the UK is slowing down. According to the latest data, Average Hourly Earnings excluding bonuses rose by 4.6% year-on-year, matching forecasts but slightly below the previous 4.7%. Similarly, Average Earnings including bonuses increased by 4.8%, which was weaker than the 5% seen earlier.

Slower wage growth means that people are earning less in real terms, especially when inflation remains a concern. If wages don’t rise as fast as prices, households feel the squeeze, leading to lower consumer confidence and spending.

Rising Layoffs Indicate Business Caution

Another sign of economic trouble is that businesses are becoming more cautious about hiring. With the UK economy showing only modest growth and the cost of living remaining high, many employers are cutting back on recruitment or even reducing their workforce. These layoffs, although small in number compared to the total workforce, suggest that companies are preparing for tougher economic conditions ahead.

The Bank of England’s Dilemma: Cut or Hold Rates?

The weak employment data has also fueled speculation that the Bank of England (BoE) might cut interest rates sooner than expected. When unemployment rises and economic growth slows, central banks often step in to support the economy by lowering borrowing costs.

Hints of a Softer Stance

In its recent policy statement, the BoE dropped the word “careful” from its guidance on monetary easing. This subtle change in language has been interpreted as a signal that the central bank is becoming more open to rate cuts. Many traders are now expecting a possible rate reduction at the December policy meeting, which could provide short-term relief to the economy but might also put further pressure on the Pound.

Balancing Inflation and Growth

The challenge for the BoE is finding the right balance between controlling inflation and supporting growth. Cutting rates too quickly could reignite inflation, while keeping them high for too long might deepen the slowdown. With the job market weakening and wage growth slowing, the bank faces a tricky path ahead.

Global Developments Add More Pressure

While domestic issues weigh heavily on the Pound, global developments are also playing a role in shaping its direction.

US Political and Economic Stability

Across the Atlantic, the US Dollar has remained relatively stable after the US Senate advanced government funding bills to the House of Representatives. This move has reduced fears of a government shutdown and supported confidence in the US economy. A stronger Dollar naturally puts downward pressure on the Pound, especially when investors view the US as a safer option.

Market Expectations on the Federal Reserve

Investors are also keeping an eye on the Federal Reserve (Fed). The market currently expects a roughly 62% chance that the Fed will cut interest rates by 25 basis points in its December meeting. If the Fed does cut rates, it might weaken the Dollar slightly, giving the Pound some breathing room. However, if the Fed holds steady, the gap between the UK and US interest rate outlooks could widen, keeping the Pound under pressure.

Upcoming UK GDP Data: The Next Big Test

The next key event for the UK economy will be the release of the Gross Domestic Product (GDP) data for September and the preliminary results for the third quarter. Economists are forecasting that the UK economy grew by only 0.2% in Q3, compared to 0.3% in the previous quarter.

")

If GDP growth turns out weaker than expected, it will reinforce the narrative that the UK economy is losing steam, increasing the chances of a BoE rate cut. On the other hand, a stronger-than-expected GDP report could help the Pound recover some of its recent losses by showing that the economy still has some resilience left.

What This Means for Everyday People

All these developments might sound distant and technical, but they have real-world effects. A weaker Pound can make imported goods more expensive, contributing to inflation in the short term. However, it can also help UK exporters by making British goods cheaper for foreign buyers. For consumers, though, it often means higher prices for fuel, groceries, and holidays abroad.

For people with mortgages or loans, potential interest rate cuts could bring some relief through lower borrowing costs. But for savers, lower rates may reduce the returns on their deposits. It’s a complex trade-off that affects almost every household in some way.

Final Summary

The Pound Sterling’s recent slide highlights the growing concern about the UK’s economic health. With unemployment rising, job creation slowing, and wage growth cooling, the picture isn’t as bright as it was earlier this year. The Bank of England faces tough decisions ahead — it must support the economy without letting inflation get out of control.

Meanwhile, global factors like US political stability and Federal Reserve policy will continue to influence the Pound’s direction. As investors and everyday citizens await the upcoming GDP data, one thing is clear: the UK economy is at a critical juncture. Whether it bounces back or slips further will depend on how policymakers, businesses, and consumers respond in the months ahead.

USDJPY Climbs Higher as Market Doubts Over BoJ Policy Hurt Yen Strength

The Japanese Yen (JPY) has been under noticeable pressure lately, and traders are finding it difficult to trust any upward movement in the currency. With mixed signals coming from the Bank of Japan (BoJ) and renewed optimism around the U.S. economy, the Yen is caught between conflicting global forces. Let’s dive deeper into why the Yen continues to lose its edge and what’s driving the market mood around it.

The Bank of Japan’s Confusing Signals Keep Traders Guessing

The BoJ has always been known for its cautious stance, but this time, the uncertainty feels heavier than usual. Recently, the Summary of Opinions from the BoJ revealed a divided outlook among policymakers about the timing of the next interest rate hike. Some members believe Japan is inching closer to tightening monetary policy, while others think it’s too soon given the fragile state of domestic demand.

USDJPY is moving in an uptrend channel, and the market has reached a higher high area of the channel

Adding to the cautious tone, BoJ’s Junko Nakagawa emphasized that any move on rates will be gradual and carefully considered. This comment reinforced the belief that Japan might hold off on rate hikes longer than expected.

Another layer of uncertainty comes from Japan’s new Prime Minister, Sanae Takaichi, whose administration is reportedly preparing a large-scale economic stimulus plan. If true, this could further delay rate hikes since the government and central bank would want to avoid shocking the economy with tighter policy amid new spending measures.

So far, the market is reading all of this as a signal that the BoJ will remain on the sidelines. As a result, traders are reluctant to bet heavily on the Yen, leaving it vulnerable to swings in global sentiment.

Global Optimism Weakens the Yen’s Safe-Haven Demand

The Yen has long been seen as a safe-haven currency, meaning investors often turn to it during times of uncertainty. However, when markets are optimistic, that appeal fades quickly—and that’s exactly what’s happening now.

In the U.S., hopes are rising that the government shutdown issue might soon be resolved. The Senate has already taken steps toward restoring funding to federal agencies, and this has lifted investor sentiment. When markets feel calm and confident, investors usually pull away from safe-haven assets like the Yen and move toward riskier investments such as equities or emerging-market currencies.

This renewed optimism has also helped U.S. Treasury yields move slightly higher, giving the U.S. Dollar some strength against the Yen. Although the Dollar isn’t exactly soaring—because traders still expect possible Federal Reserve rate cuts—the combination of positive risk sentiment and a cautious BoJ is enough to keep the Yen on the defensive.

Economic Concerns at Home Add More Pressure

While the BoJ debates its next move, Japan’s economy continues to show signs of strain. Data released last week pointed to weak household spending, a clear sign that higher living costs are dampening consumer demand. Many analysts believe that soft consumption could limit inflation growth, making it even harder for the BoJ to justify a rate hike.

Adding to the concern, Economy Minister Minoru Kiuchi recently admitted that inflation is eroding household purchasing power. He mentioned that the government is considering new measures to help families cope with the rising cost of goods. A weaker Yen is part of the problem—it raises the price of imported goods, which trickles down to higher prices for everyday consumers.

So, while Japan’s export sector benefits from a cheaper currency, the average household feels the pain. This delicate balance makes it even more difficult for policymakers to take bold monetary action.

Intervention Risks and Market Caution

Given the Yen’s rapid decline, there’s growing talk in financial circles about possible government intervention to support the currency. Japan’s Ministry of Finance has a history of stepping in when the Yen weakens too quickly, and traders know that such actions can cause sharp reversals in the market.

This fear of intervention is one of the few factors preventing the Yen from falling even further. Traders are hesitant to push the currency lower because an unexpected move from Japanese authorities could quickly reverse their positions and cause significant losses.

As a result, the market remains cautious. Many traders prefer to stay on the sidelines rather than take big bets until they have a clearer picture of the BoJ’s intentions or any hint of government action.

The Role of U.S. Monetary Policy

The other major factor in the Yen’s story is what’s happening across the Pacific. The Federal Reserve has signaled that rate cuts could be on the table in the coming months. If the Fed does lower rates, the Dollar could lose some of its appeal, giving the Yen a chance to recover.

However, for now, the Dollar remains supported by slightly higher bond yields and a relatively stronger U.S. economy. This combination is keeping the USD/JPY pair steady, even if neither currency looks particularly strong. Traders are watching closely to see whether U.S. inflation and employment data will push the Fed to act sooner or later.

What Traders Are Watching Next

At this stage, everything depends on how the BoJ communicates its next moves and how global markets react to shifting economic headlines. If Japan’s inflation remains subdued and consumption weakens further, it’s unlikely the BoJ will tighten policy soon.

On the other hand, if U.S. growth data starts to cool and the Fed moves forward with rate cuts, the Dollar could weaken, giving the Yen some room to bounce back. But as long as optimism about the U.S. economy continues, the Yen may remain under pressure.

For short-term traders, the biggest challenge is timing. The mix of BoJ uncertainty, intervention risks, and global sentiment makes this one of the trickiest currency pairs to trade right now. Most are taking a wait-and-see approach, preferring to react to news rather than predict it.

Final Summary

In simple terms, the Japanese Yen is facing headwinds from all directions. The Bank of Japan’s cautious and divided stance leaves investors unsure about when interest rates might rise. Meanwhile, improving confidence in the U.S. economy and the potential resolution of the government shutdown have reduced the Yen’s safe-haven appeal.

At the same time, weak consumer spending and rising import costs at home are creating fresh challenges for Japan’s policymakers. With intervention fears hovering in the background and Fed policy shifts still uncertain, the Yen’s outlook remains murky.

For now, it seems that the Yen will continue to struggle for strength until either the BoJ delivers a clear policy message or global market sentiment turns risk-averse once again. Traders and investors alike are watching closely—because when the BoJ finally makes its move, the ripple effects will be felt across global currency markets.

GBPJPY Falls as Soft UK Employment Numbers Pressure the Pound

The British Pound has lost momentum recently, dropping from its earlier highs after the latest UK employment report showed weaker results than expected. Many traders and investors were surprised by the sudden shift in sentiment, as the data painted a less optimistic picture of the UK job market. Let’s dive deeper into what’s happening, why it matters, and what could come next for the Pound against the Japanese Yen.

GBPJPY is moving in a descending channel

UK Job Market Struggles: A Sign of Slowing Growth

The recent employment data from the Office for National Statistics revealed that the UK’s unemployment rate has climbed to 5%, marking its highest level in four years. This increase caught the market off guard since most analysts were expecting the rate to hold steady at 4.9%. While the change may look small on paper, it signals a worrying trend that the labor market could be under pressure as economic growth slows.

To make matters worse, the number of people claiming unemployment benefits jumped by 29,000 in October, much higher than the anticipated 20,000 increase. This surge in jobless claims suggests that companies across various sectors are becoming more cautious, possibly due to rising costs and economic uncertainty. It also shows that job seekers are finding it harder to secure stable employment, even as the country continues to recover from past economic challenges.

Wage Growth Loses Steam

Alongside higher unemployment, wage growth also slowed down. Average earnings rose by 4.8% over the year, compared to 5% in the previous month. This slight dip indicates that wage pressure is easing, which can have mixed effects. On one hand, slower wage growth might help control inflation, but on the other, it could limit consumer spending since households may have less disposable income.

When wages don’t keep pace with living costs, it affects overall demand in the economy. This imbalance can lead to weaker business performance and lower growth prospects — two key reasons why the latest data has worried both policymakers and investors.

The Bank of England Faces a Tough Decision

These employment numbers come at a critical time for the Bank of England (BoE). The central bank has been carefully balancing its policy between controlling inflation and supporting the economy. With unemployment rising and wage growth slowing, the chances of further monetary easing have increased.

In simpler terms, the BoE might consider cutting interest rates or maintaining an accommodative stance to stimulate economic activity. This would make borrowing cheaper and encourage spending and investment — but it could also weaken the Pound in the process.

Investors are now watching closely to see whether the central bank signals any changes in its upcoming meeting. The disappointing labor data has added pressure for policymakers to take action sooner rather than later, especially if other indicators such as inflation or retail sales also show signs of slowing down.

Global Market Sentiment and Its Impact on the Pound-Yen Pair

Despite the weakness in UK data, the British Pound hasn’t collapsed entirely, thanks in part to the ongoing weakness in the Japanese Yen. The Yen has been under pressure due to expectations that the Bank of Japan (BoJ) will maintain its ultra-loose monetary policy. Japan’s central bank has faced constant pressure not to raise interest rates, even as other major economies are tightening policy.

This divergence between the BoE and BoJ has kept the GBP/JPY pair relatively supported, even as the Pound’s fundamentals weaken. Traders tend to favor the Pound over the Yen when global risk sentiment improves, since the Yen is traditionally seen as a “safe-haven” currency.

Risk Appetite on the Rise

A key factor supporting the Pound recently has been a renewed sense of optimism in global markets. Hopes of the U.S. government reopening and stability in broader economic conditions have encouraged investors to move away from safe assets like the Yen. When market participants feel more confident, they usually prefer higher-yielding currencies such as the Pound.

However, this support may be temporary. If risk sentiment shifts — for example, due to geopolitical tensions or weaker global growth — the Yen could strengthen quickly, putting renewed pressure on the Pound. This tug-of-war between risk appetite and economic data will likely continue influencing the Pound-Yen exchange rate in the coming weeks.

Why This Matters for Everyday People and Investors

For everyday consumers in the UK, the current situation could have real-world implications. A slowing job market means fewer employment opportunities and potentially slower wage increases. For homeowners and borrowers, any move by the Bank of England to lower interest rates could reduce mortgage and loan costs, but it also suggests that the economy is struggling to gain traction.

For investors, this environment creates both risks and opportunities. Currency traders are watching closely for signs of policy changes from the BoE or BoJ. The GBP/JPY pair often reacts sharply to economic news, and periods like this can create volatility — which, depending on the strategy, can be either a challenge or an advantage.

Long-term investors, on the other hand, may view these developments as part of a broader economic cycle. Slower job growth, weaker wages, and central bank adjustments are typical patterns during transitions between economic expansions and slowdowns.

Final Summary

The British Pound’s recent retreat reflects the market’s growing concern over the UK’s economic outlook. Rising unemployment, slower wage growth, and uncertainty about future monetary policy have created a cautious tone among traders and investors. Meanwhile, the Japanese Yen remains under pressure as the Bank of Japan continues its accommodative stance, preventing a sharper fall in the GBP/JPY pair.

The coming weeks will be crucial. If the UK’s economic data continues to weaken, the Bank of England may step in with additional measures to support growth. For now, the Pound’s direction will largely depend on how global markets interpret these shifts — balancing between domestic challenges and international sentiment.

In short, the UK’s latest job market data has stirred new doubts about the pace of recovery, leaving both policymakers and investors searching for clear signs of stability. While the Pound still shows resilience, its strength may be tested if the economic slowdown deepens and confidence continues to fade.