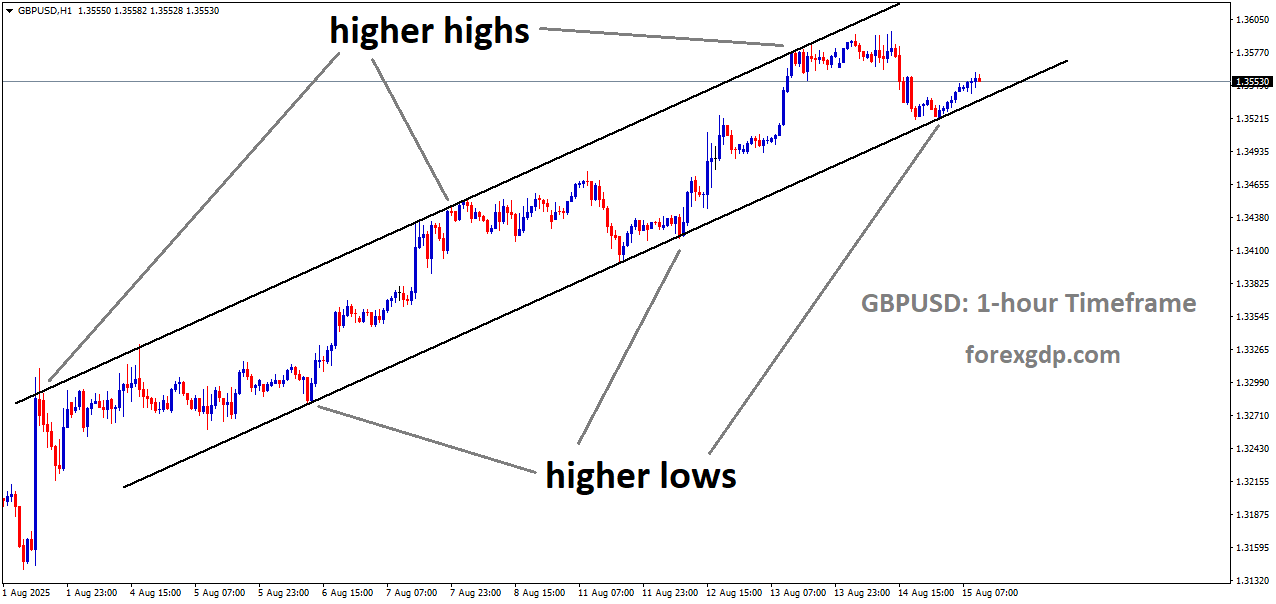

GBPUSD is moving in an uptrend channel, and the market has rebounded from the higher low area of the channel

GBPUSD climbs as traders await crucial US consumer spending report

The GBP/USD currency pair has been showing strength in the early European session on Friday, finding support from both economic and sentiment factors. With the US Dollar losing some ground and the UK economy delivering better-than-expected growth data, the Pound Sterling is benefiting from a wave of optimism. At the same time, traders are reassessing their expectations for US Federal Reserve interest rate cuts, which is influencing the overall direction of the market.

Stronger UK Economic Growth Lifts Pound Sentiment

One of the biggest drivers behind the recent rise in GBP/USD has been the encouraging UK GDP report. The UK economy managed to grow by 0.3% in the second quarter (Q2) of 2025 compared to the previous quarter, outpacing forecasts of just 0.1% growth.

Although the pace of growth was slower than in Q1, when the economy expanded by 0.7%, the fact that it came in well above expectations is a positive sign. On a yearly basis, GDP grew 1.2%, also beating the market consensus of 1.0%. This performance suggests that the UK economy is proving more resilient than many had predicted, despite ongoing challenges in global trade and domestic cost pressures.

Economic resilience tends to boost investor confidence in a currency, as it can signal stability and encourage capital inflows. For the Pound, this means stronger buying interest from traders who see the UK’s growth outlook as comparatively healthy.

Shifting US Interest Rate Expectations and Their Impact

In recent weeks, the US Dollar had been under pressure from rising expectations that the Federal Reserve might cut interest rates as soon as September. These expectations were fueled by weaker US job data and a softer inflation trend in the Consumer Price Index (CPI).

However, the release of hotter-than-expected US Producer Price Index (PPI) figures has caused traders to rethink the likelihood of an immediate and aggressive rate cut. While markets still expect a 25 basis point cut, the probability has fallen slightly. According to the CME FedWatch tool, the odds of a September cut now stand near 92%, down from 96% before the PPI data release.

When traders scale back expectations for aggressive Fed rate cuts, the US Dollar can find support, making it more challenging for GBP/USD to extend gains. But with UK data showing strength, the Pound has been able to hold its ground despite this shift in sentiment.

Market Mood Ahead of US Retail Sales Report

Even though the GBP/USD pair is showing strength, traders remain cautious. The upcoming US Retail Sales report is a key event that could influence the next big move in the pair. Scheduled for release later on Friday, this report will provide insights into the health of US consumer spending—a major driver of the economy.

If retail sales come in hotter than expected, it could give the US Dollar a boost, as strong consumption data would signal a more resilient US economy and potentially reduce the urgency for the Fed to cut rates. On the other hand, weaker data could reinforce expectations for policy easing, adding downward pressure on the Dollar and potentially lifting GBP/USD further.

At present, economists expect July retail sales to have risen by 0.5%. While this is a moderate increase, any significant deviation from the forecast could trigger sharp market reactions.

Why This Data Matters for GBP/USD

US economic data has a direct influence on interest rate expectations, and interest rates are one of the biggest drivers of currency values. Stronger US data can make the Dollar more attractive by suggesting higher yields for investors, while weaker data can have the opposite effect.

Since GBP/USD is a relative value trade—measuring the strength of the Pound against the Dollar—changes in either economy’s outlook can shift the balance. Right now, with the UK economy showing better-than-expected growth and the Fed still leaning toward eventual cuts, the Pound has a supportive backdrop. But the picture can change quickly if US data surprises to the upside.

Key Takeaways for Traders and Investors

-

UK Growth Surprised to the Upside: The better-than-expected GDP data shows the UK economy is holding up well, which has boosted the Pound.

-

Fed Rate Cut Bets Trimmed: While a September rate cut is still widely expected, the odds have fallen slightly after strong US PPI data.

-

Retail Sales Could Shift the Mood: Friday’s US Retail Sales report has the potential to cause significant swings in GBP/USD, depending on whether the data beats or misses expectations.

GBPUSD is moving in an uptrend channel

For short-term traders, these developments mean a market that is still very much in play. For longer-term investors, the focus may remain on how both economies perform over the next few months, particularly as central banks adjust their monetary policy stances.

Final Summary

The Pound has been climbing against the Dollar, supported by a resilient UK economy and tempered expectations for US interest rate cuts. UK GDP growth has exceeded forecasts, reinforcing confidence in the nation’s economic outlook. Meanwhile, the Fed’s rate path remains a key factor, with traders closely watching every piece of US economic data for clues. The next big test for GBP/USD comes with the US Retail Sales report, which could either reinforce the pair’s current upward momentum or trigger a pullback. In a market driven by shifting expectations, staying alert to incoming data is essential for navigating the moves ahead.

EURUSD Pushes Higher After Sharp Drop, Shows Signs of Recovery

The EUR/USD currency pair is showing signs of recovery after recent setbacks, as the US Dollar faces renewed pressure from growing expectations of a Federal Reserve interest rate cut. The market mood is shifting, with traders betting heavily on a September rate reduction, giving the Euro a chance to push higher. While recent US economic data temporarily boosted the Dollar, the broader sentiment appears to be favoring the Euro in the near term.

Why the Euro is Climbing Again

The EUR/USD pair has managed to reverse some of its recent losses, trading higher during the Asian session on Friday. This rebound comes after the US Dollar lost its footing amid increased speculation that the Federal Reserve will cut rates in September.

Market tools such as the CME’s FedWatch indicate that traders are pricing in an overwhelming probability of a 25-basis-point rate cut at the Fed’s September meeting. Such expectations tend to weigh on the Dollar, as lower interest rates reduce its appeal compared to other currencies.

EURUSD is moving in an uptrend channel, and the market has rebounded from the higher low area of the channel

While the Euro has benefited from this shift in sentiment, it’s important to note that just a day earlier, the pair had experienced a drop of nearly 0.5%. That decline was driven by stronger-than-expected US economic data, which briefly reignited support for the Dollar.

US Economic Data and Its Impact on the Dollar

The latest set of US economic numbers came in far stronger than many analysts had anticipated. The July Producer Price Index (PPI) rose by 3.3% compared to the same period last year, far above both the prior reading and the market’s forecasts. Even the core PPI, which strips out volatile items, surged to 3.7%, signaling persistent price pressures.

Labor market data also added to the Dollar’s strength on Thursday, with Initial Jobless Claims dropping to 224,000—lower than both the previous week’s revised figure and market expectations. A healthy labor market often gives central banks more room to keep interest rates higher for longer, which is typically supportive of a currency.

However, despite this economic resilience, market participants seem more focused on the Fed’s potential policy pivot in the coming months. The growing conviction that rates will be cut soon has dampened the Dollar’s momentum, allowing the Euro to regain ground.

The Role of the ECB and the Interest Rate Gap

Another factor supporting the Euro is the outlook for European Central Bank (ECB) policy. The ECB has already completed its easing cycle after implementing eight rate cuts over the past year, bringing borrowing costs down to their lowest level since late 2022.

For now, the ECB is likely to hold steady, with no further moves expected until at least 2025. This creates a potential advantage for the Euro, as the interest rate gap between the Fed and the ECB could narrow if the Fed cuts rates while the ECB keeps its stance unchanged.

When interest rates between two regions move closer together, the currency of the region with the relatively higher or more stable rate often gains support. In this case, the Euro stands to benefit if the Fed begins lowering rates while the ECB holds firm.

Quiet Day for the Eurozone

The European economic calendar remains light, with no major data releases scheduled. This is partly due to the Feast of Our Lady of Heaven holiday, meaning traders will primarily take their cues from US developments and broader market sentiment.

With no fresh news from Europe, the Euro’s movements in the short term will likely hinge on upcoming US data releases, including retail sales figures and consumer sentiment surveys.

What to Watch Next

In the near term, traders will be paying close attention to two key pieces of US data:

-

Retail Sales Report – This will offer insight into consumer spending strength, a crucial driver of economic growth in the United States.

-

University of Michigan Consumer Sentiment Index – A measure of how optimistic or pessimistic consumers feel about the economy, which can influence spending patterns.

Strong numbers could give the Dollar a short-term boost, while weaker data may reinforce expectations of a September rate cut, keeping the Euro on the offensive.

The Bigger Picture

While daily price moves can be influenced by short-term data releases, the bigger story remains the policy divergence between the Fed and the ECB. With the Fed signaling potential rate cuts and the ECB likely to remain steady, the EUR/USD pair could continue to find upward momentum in the months ahead.

EURUSD is moving in an uptrend channel

That said, currency markets are notoriously volatile, and shifts in economic conditions, geopolitical events, or central bank communication can quickly change the outlook. Traders and investors will need to remain alert to evolving developments on both sides of the Atlantic.

Final Summary

The EUR/USD pair is rebounding as the US Dollar struggles against growing expectations of a Federal Reserve interest rate cut in September. Strong US economic data provided temporary support for the Dollar, but broader sentiment is leaning toward a weaker USD outlook in the coming months.

With the ECB holding steady after a series of rate cuts and the Fed potentially preparing to ease, the narrowing interest rate gap could favor the Euro. While upcoming US retail sales and consumer sentiment reports may create short-term fluctuations, the longer-term trend could continue to tilt in the Euro’s favor if the Fed moves forward with its expected policy shift.

USDJPY Retreats, Yen Rallies on Surprising Economic Growth in Japan

The Japanese Yen (JPY) has gained fresh momentum after Japan reported better-than-expected GDP growth for the second quarter of 2025. This improvement came despite ongoing challenges from global trade tensions, particularly the impact of higher US tariffs. The new data has revived hopes that Japan’s economy is holding up better than many had anticipated, giving the Yen a notable push against the US Dollar (USD).

USDJPY is moving in an uptrend channel, and the market has fallen from the higher high area of the channel

While the USD had recently seen a recovery following a strong US Producer Price Index (PPI) report, its upward run has lost steam. Traders are now reassessing the balance between the Federal Reserve’s likely interest rate cuts and the Bank of Japan’s potential tightening measures, a dynamic that is favoring the Yen in the short term.

Why the GDP Numbers Matter

The Cabinet Office’s preliminary reading revealed that Japan’s economy grew by 0.3% in Q2, translating to a 1.0% annualized growth rate. This is a clear improvement from the previous quarter’s contraction and far better than the 0.4% growth economists had forecast.

Japan’s Economy Minister, Ryosei Akazawa, noted that the results confirm the economy is on a modest recovery path. However, he also warned that rising prices could dampen consumer spending and that US trade policies remain a risk to sustained growth.

This stronger-than-expected performance supports the Bank of Japan’s forecast for 0.6% growth in the 2025 fiscal year. With inflation also trending higher, many analysts believe the BoJ could move toward an interest rate hike before the year ends — a step that would further strengthen the Yen.

Diverging Central Bank Strategies

One of the key reasons the Yen has been finding support is the difference in direction between the BoJ and other major central banks, particularly the US Federal Reserve. While the BoJ is leaning toward policy normalization, the Fed is still expected to lower interest rates later this year.

Recent US economic data shows mixed signals. July’s PPI reading came in hotter than expected, suggesting inflation pressures may still be building. This initially boosted the USD as it reduced the likelihood of aggressive rate cuts. However, traders are still pricing in a 90% probability of a 25-basis-point cut in September, and possibly more cuts before year-end.

This softer outlook for US rates limits the USD’s strength and allows the Yen to hold its ground.

Global Political and Market Influences

Beyond the economic data, political developments are also in play. Markets are closely watching the meeting between US President Donald Trump and Russian President Vladimir Putin in Alaska, aimed at discussing an end to the war in Ukraine. Any major developments from this high-stakes summit could sway global risk sentiment — potentially benefiting the Yen, which is often seen as a safe-haven currency in times of uncertainty.

USDJPY is moving in an Ascending channel, and the market has reached the higher low area of the channel

On the US side, upcoming economic reports such as Retail Sales, the Empire State Manufacturing Index, and the University of Michigan’s Consumer Sentiment data will be closely monitored. Comments from Federal Reserve officials could also give traders more clarity on the likely policy path in the coming months.

Final Summary

Japan’s economy is showing resilience, and the strong Q2 GDP results have reinforced expectations that the Bank of Japan may tighten policy sooner rather than later. This shift, combined with the US Federal Reserve’s likely rate cuts, has given the Japanese Yen an edge against the US Dollar.

While global trade tensions and political uncertainty remain risks, the Yen’s safe-haven appeal continues to draw buyers. With key US economic data and geopolitical developments on the horizon, volatility in USD/JPY is likely to persist — but for now, the momentum appears to favor the Yen.

USDCHF Extends Strength on Robust US Inflation Data

The USD/CHF currency pair is showing solid strength, holding onto its recent gains after the latest US economic data delivered a surprise to the markets. This development has drawn the attention of traders and investors, as it not only signals potential shifts in economic momentum but also raises questions about future central bank actions in both the United States and Switzerland.

Let’s break down what’s driving this move and what it could mean going forward.

USDCHF is moving in a descending Triangle pattern

A Strong Boost from US Inflation Data

The primary driver behind the recent USD/CHF strength is the hotter-than-expected US Producer Price Index (PPI) for July. This index measures inflation at the wholesale level — basically, the price changes that producers experience before goods and services reach consumers.

For July, both the headline PPI (which includes all items) and the core PPI (which excludes food and energy) posted a notable 0.9% rise compared to June, when the data was completely flat. On a yearly basis, wholesale prices climbed by 3.3% for the headline reading and 3.7% for the core reading.

This marks the fastest pace of producer inflation in the US in three years, largely driven by the impact of tariffs. Many analysts believe businesses are now beginning to pass the higher costs caused by tariffs onto consumers rather than absorbing them within their profit margins.

Why This Matters for the Dollar

The US Dollar tends to strengthen when inflation data is hotter than expected. This is because higher inflation increases the chances that the Federal Reserve will keep interest rates higher for longer, or at least avoid aggressive cuts. Although many traders still expect the Fed to consider a rate cut in September, strong inflation data makes that decision more complicated.

Another factor is the timing of these price pressures. Importers who had stockpiled goods before tariff announcements are now running low on inventory, and the replenishment comes at a higher cost due to the new duties. This change means that cost increases are now hitting the economy in a more noticeable way.

The Swiss Side of the Story

While the US Dollar is benefiting from stronger inflation numbers, the Swiss Franc is facing pressure from the opposite situation. Switzerland’s Producer and Import Prices fell by 0.9% in July, following a 0.7% decline in June. This consistent drop in producer-level prices shows that inflationary pressure in Switzerland is weakening.

Potential Impact on the Swiss National Bank (SNB)

If prices in Switzerland continue to fall, the SNB might need to consider more aggressive monetary policy actions to stimulate the economy. This could even mean pushing interest rates further into negative territory, which would generally weaken the Swiss Franc.

For USD/CHF traders, this contrast between rising US inflation and falling Swiss inflation creates a stronger bias toward a higher exchange rate. When one country’s central bank is under pressure to cut rates while the other is potentially holding steady or cutting more slowly, the currency with the relatively higher rates often gains value.

Investor Sentiment and Market Expectations

Right now, sentiment in the currency market leans toward favoring the Dollar. The US Dollar Index (DXY), which measures the USD against a basket of major currencies, is holding firm near recent highs. This reinforces the idea that the Dollar’s strength is not just limited to the Swiss Franc but is more broad-based.

That said, markets are still closely watching the Federal Reserve’s next move. Even with stronger PPI data, many traders believe the Fed could still deliver a small rate cut in September if economic growth starts slowing. However, the hotter inflation numbers make it less likely that the Fed will move aggressively in that direction.

What This Could Mean Going Forward

Looking ahead, several factors will likely influence the USD/CHF pair:

1. US Economic Data

If upcoming US data — such as consumer inflation (CPI) and employment reports — continues to show strong momentum, the Dollar could hold onto or even extend its recent gains. On the other hand, if data weakens sharply, it may renew speculation about earlier or larger Fed rate cuts.

2. Swiss Inflation Trends

The persistent decline in producer prices in Switzerland is a concern for the SNB. If this trend continues, the central bank may feel compelled to take policy actions that could weaken the Franc further.

3. Global Trade and Tariffs

Since tariffs have been a major driver of recent inflationary changes in the US, any new trade developments could have a quick impact on the currency market. If trade tensions escalate, cost pressures may increase further, potentially keeping US inflation elevated.

USDCHF is moving in a box pattern, and the market has reached the support area of the pattern

Final Summary

The USD/CHF pair is currently benefiting from a perfect mix of stronger US inflation data and weaker Swiss inflation numbers. Hot US PPI figures have boosted expectations that the Federal Reserve may delay aggressive interest rate cuts, giving the Dollar an edge. Meanwhile, the Swiss Franc is under pressure due to falling producer prices, which could push the Swiss National Bank toward looser monetary policy.

While the near-term outlook seems to favor the Dollar, future movements will depend on upcoming economic data and central bank decisions. For now, traders and investors are watching both economies closely, knowing that shifts in inflation trends or policy signals could quickly change the balance in this currency pair.

EURGBP Climbs Past 0.8600 as Markets Await Trump–Putin Talks

The EUR/GBP currency pair has been edging upward, reflecting a mix of political expectations and economic updates. While the market often reacts to technical patterns and price levels, this time the movement is largely driven by fundamental developments, particularly surrounding an important meeting between two major global leaders. Let’s break down what’s really influencing the Euro and the British Pound right now, without drowning in complex jargon.

EURGBP is moving in a box pattern, and the market has reached the support area of the pattern

Why EUR/GBP is Climbing – The Political Factor

One of the biggest drivers behind the Euro’s recent strength is the renewed hope for a potential resolution to the ongoing Ukraine conflict. Investors and traders are focusing heavily on the scheduled meeting between US President Donald Trump and Russian President Vladimir Putin. This isn’t just another diplomatic conversation—it’s a potential turning point that could influence global markets for months to come.

Trump has suggested that Putin may be open to ending the war, but he also hinted that peace would likely require another meeting, one that includes Ukraine’s President Volodymyr Zelenskyy. If these discussions lead to even the smallest breakthrough, it could ease geopolitical tensions in Europe. For the Eurozone, that means reduced uncertainty and possibly lower energy costs, both of which tend to support the Euro in the foreign exchange market.

Why This Meeting Matters for Currencies

Global currencies, especially those tied to large economic blocs like the Eurozone, are sensitive to political stability. When tensions rise, investors often seek safer assets, which can weaken risk-linked currencies. But when there’s even a whisper of peace or stability, it can flip the script—demand for the Euro can rise as confidence returns.

The Pound Sterling is also in focus, but in this scenario, the Euro is getting a slightly bigger boost. That’s because the direct economic benefits of lower European energy costs and a calmer political environment would be felt more strongly within the Eurozone than in the UK.

UK Economy Shows Resilience

While the Euro’s rise is tied to political hopes, the British Pound isn’t sitting idle. The latest UK economic data surprised analysts by showing less of a slowdown than expected. According to the Office for National Statistics, the UK economy grew by 0.3% in the second quarter of the year, compared to a 0.7% increase in the previous quarter.

Many experts had predicted far weaker growth, so this stronger-than-expected result gives the Pound some resilience. The UK economy managed to hold up despite challenges such as weaker employment figures and the lingering effects of global trade pressures.

Why the Growth Numbers Matter

Economic growth is one of the key indicators currency traders watch when deciding where to put their money. Stronger GDP growth usually means a healthier economy, which can encourage foreign investment and push a currency higher. In this case, while UK growth has slowed compared to earlier in the year, the fact that it outperformed expectations means the Pound still has a reason to hold its ground.

However, this could also limit how far EUR/GBP can climb. If both currencies are showing strength—one from political optimism and the other from better economic data—the exchange rate movement may be more gradual than dramatic.

Balancing Political Hopes and Economic Reality

Right now, the market is in a sort of balancing act. On one side, we have the Euro benefiting from optimism about a potential peace deal in Ukraine. On the other, the Pound is supported by the UK’s relatively better-than-expected economic performance.

If the Trump-Putin meeting produces signs of progress toward peace, the Euro could gain further momentum. But if the talks end without any meaningful steps forward, that optimism could fade quickly, giving the Pound a chance to push back.

Short-Term Market Mood

Traders are cautious but hopeful. The fact that the Euro is slowly climbing instead of surging shows that investors aren’t betting everything on a positive political outcome just yet. At the same time, the Pound’s underlying strength means any move higher in EUR/GBP might face resistance from those willing to take profits or shift back to Sterling.

EURGBP is moving in a descending triangle pattern, and the market has fallen from the lower high area of the pattern

The Bigger Picture

Beyond today’s headlines, both the Euro and Pound face their own long-term challenges. For the Eurozone, slowing growth in some member states and ongoing trade disputes can limit gains. For the UK, uncertainties around its trade relationships and domestic economic policies still hang over the market.

That’s why events like the Trump-Putin meeting get so much attention—they can be rare moments where political developments provide a clear short-term push in one direction or another. But the underlying economic health of each region will still play a major role in shaping the currency pair’s trend over the coming months.

Final Summary

The EUR/GBP pair’s current upward drift is fueled by a mix of political anticipation and economic resilience. The Euro is gaining support from hopes that the Trump-Putin meeting could lead to progress toward ending the Ukraine war, potentially easing European energy costs and boosting confidence. Meanwhile, the UK economy has surprised with stronger-than-expected growth, helping the Pound avoid major losses.

Both currencies are showing strength for different reasons, creating a tug-of-war effect that keeps the market cautious. Whether the Euro continues to climb will depend heavily on the outcome of today’s political talks, while the Pound’s future will hinge on how well the UK economy holds up in the months ahead.