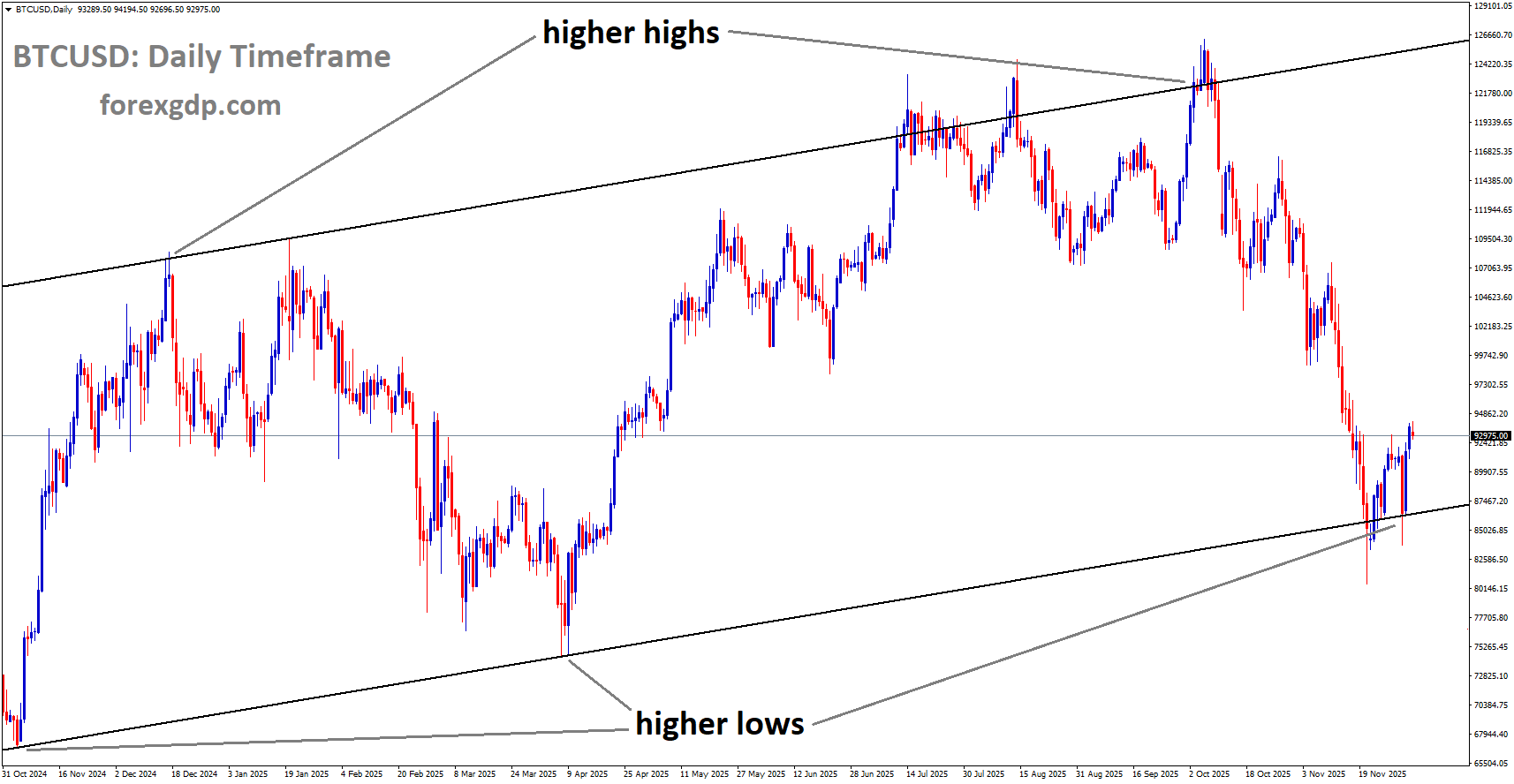

BTCUSD is moving in an uptrend channel, and the market has rebounded from the higher low area of the channel

BTCUSD Market Rebuild Begins, But the Hard Part Comes Next

Bitcoin has been trying to steady itself after a sudden and intense selloff that shook the wider crypto market. The move lower was fast, emotional, and powerful enough to reset sentiment in a short time. Since then, trading has looked calmer, with price showing signs of stabilizing rather than continuing to fall in a straight line.

Even after a drop of that size, many investors focus on one simple question: is Bitcoin still holding up, or is it getting weaker? So far, the market action suggests that buyers have not disappeared. Instead, they have continued to show up in areas where interest was already strong, helping Bitcoin avoid another wave of panic.

That doesn’t mean the path forward will be easy. Bitcoin may be calmer now, but the market still has a lot of selling pressure sitting above. As the recovery develops, it will likely run into areas where many traders and long-term holders may decide to take profit, cut risk, or re-enter short positions. Those moments can create push-and-pull price action and slow progress.

Why Bitcoin’s Stability Matters Right Now

When a market falls hard, it often reveals two things at once: where fear is strongest and where confidence begins to return. Bitcoin’s recent behavior has been more like a pause and regroup than a full breakdown. That kind of stabilization matters because it can signal that the market is shifting from forced selling to more balanced trading.

This stage is also important psychologically. During rapid declines, many traders react quickly, often selling because they don’t want to be the last one out. Once the selling wave fades, the market typically enters a quieter period where participants reassess what happened. Some buyers begin to step in again, while some sellers remain cautious but less aggressive.

In other words, stability doesn’t promise a rally, but it can reduce the odds of another immediate free fall. It also creates room for more thoughtful decision-making, which is often when stronger hands begin to accumulate and weaker hands step away.

Where the Next Big Decisions May Happen

Markets tend to remember areas where the most intense buying and selling happened before. With Bitcoin, that means there are “busy zones” overhead where earlier trading was active and where many positions were opened, closed, or liquidated. When price returns toward those zones, the reactions can be sharp because people still have unfinished business there.

Here are three broad areas that may influence what happens next:

-

The first major hurdle during recovery

This is the area that could determine whether the rebound has real strength or whether it fades quickly. Many markets stall at the first point where earlier selling accelerated, because traders who were trapped may use the bounce as an opportunity to exit. -

A second area where selling may return

If Bitcoin continues upward, the next decision zone can attract a different group of sellers—those who believe the recovery has gone far enough and want to reduce exposure again. This stage can often feel slower, with more hesitation and more sudden intraday swings. -

A higher zone that could cap progress

Even if Bitcoin clears the earlier hurdles, there is usually an upper area where the market becomes much more selective. This is where the discussion often shifts from “recovery” to “strength,” and participation becomes more divided. Some will expect a larger move higher, while others will assume a pullback is overdue.

What Bulls and Bears Are Likely Thinking

Bitcoin’s market is driven not only by news, but by positioning and emotions. After a violent decline, both buyers and sellers tend to become more tactical.

What buyers tend to want

Buyers usually look for steady progress and proof that the market can absorb selling without falling apart. They also want to see confidence return gradually, with fewer sharp rejection moves and less panic-driven selling.

What sellers tend to want

Sellers often watch for signs that interest is fading. If price rises but momentum feels weak, sellers may step in, expecting the market to roll over again. They also look for areas where buyers appear hesitant, since that can be an opening to push the market lower.

This tension is exactly why recoveries after sharp drops are rarely smooth. Instead, they often unfold with stops, starts, and emotional swings as both sides test each other.

What to Watch in the Coming Days and Weeks

Bitcoin’s next chapter will likely be shaped by how it behaves when it meets heavy selling interest above. If it can keep moving upward without repeatedly getting pushed back, confidence can rebuild and participation can broaden. If it struggles and gets rejected again and again, the market may shift back into caution.

A practical way to think about this moment is simple: Bitcoin has stabilized, but it still has to earn its way higher. The market is no longer in panic mode, but it also isn’t in a carefree phase where gains come easily.

For long-term holders, this can be a period for patience and risk management. For active traders, it can be a period where discipline matters more than excitement, because choppy conditions can punish impulsive decisions.

Summary

Bitcoin has calmed down after a powerful selloff, showing signs of stability rather than continued panic. While that stability can be encouraging, the market still faces heavy selling interest above, which may slow any recovery and create sharp push-and-pull moves. The next phase is less about dramatic headlines and more about whether Bitcoin can keep buyers engaged as it moves into areas where sellers may return.

EURUSD Pushes Higher With US Labor Signals in the Spotlight

The Euro is staying strong near a five-week peak against the US Dollar, hovering close to the 1.1680 area. After slipping earlier, EUR/USD found its footing again during Thursday’s European trading session and was moving around 1.1670 at the time of writing. Even though fresh data out of the Eurozone wasn’t perfect, the broader weakness in the US Dollar has helped keep the pair supported and has limited deeper pullbacks.

So what’s driving this tug-of-war? On one side, Eurozone retail sales disappointed and briefly pressured the Euro. On the other, US data has raised fresh doubts about the strength of the American job market, increasing hopes that the Federal Reserve may start cutting interest rates soon. That contrast is keeping traders focused on the growing gap between the policy paths of the European Central Bank (ECB) and the Fed.

EURUSD is moving in an uptrend channel

Eurozone Retail Sales Miss Expectations, But the Bigger Picture Isn’t All Bad

A key update from Eurostat showed that retail sales in the Eurozone were flat in October. Markets had expected a small monthly increase, so the lack of growth gave the Euro a mild hit. The previous month’s number was also revised slightly higher, which softened the blow a bit, but the main takeaway was still that consumers didn’t spend more than they did the month before.

However, the annual reading told a more encouraging story. Compared to the same time last year, retail sales rose by 1.5%. That was better than forecasts and also stronger than September’s year-on-year pace. In simple terms, the month-to-month figure looked sluggish, but the year-to-year trend still shows that spending hasn’t collapsed.

That matters because consumer activity plays a big role in how investors view the Eurozone economy. If shoppers keep spending at a steady pace, it supports growth and reduces pressure on the ECB to rush into rate cuts. And right now, markets are paying close attention to anything that could shift the timing of future ECB moves.

Services Data Gives the Euro a Lift

While retail sales stalled, the Euro has been getting backing from stronger business activity data—especially in services. The final HCOB Services Purchasing Managers’ Index (PMI) data released on Wednesday came in better than earlier estimates, painting a brighter picture of the sector.

The headline index was revised higher, showing that the services sector has now expanded for six straight months and is performing at its best level since mid-2023. That’s important because services make up a large share of economic activity in many Eurozone countries. When services are growing, it often suggests stable demand, improving business confidence, and better employment conditions.

There were also upgrades to the services readings in France and Germany, the region’s two biggest economies. Better numbers in those countries tend to carry extra weight, because they influence how investors judge the health of the whole bloc.

Put together, the services data helped balance out the weaker retail sales report. It’s one reason why the Euro hasn’t dropped far even when some data points don’t impress.

Lagarde’s Message: The ECB Is Not in a Hurry

Another source of support for the Euro came from comments by ECB President Christine Lagarde. She struck a fairly upbeat tone about the Eurozone outlook, pointing to household spending and a resilient labor market as key stabilizers for the region.

She also suggested that underlying inflation remains on track, which investors read as a signal that the ECB can afford to keep interest rates steady for now. When central bank leaders sound confident, markets tend to assume less urgency for rate cuts—something that can support a currency like the Euro.

Of course, central banks can change their tone quickly if inflation cools faster than expected or if growth weakens sharply. But at the moment, the message coming from the ECB side is fairly consistent: rates may stay where they are, at least in the near term.

US Jobs Data Weakens the Dollar and Fuels Rate-Cut Hopes

Across the Atlantic, the US Dollar has been on the back foot, and a major reason is growing concern about the labor market. The ADP Employment Change report showed an unexpected drop in net jobs in November—something markets were not expecting at all. Instead of a small gain, the report pointed to a decline, and it was described as the largest fall in more than two years.

Even though ADP data doesn’t always match the official government jobs report, it still influences sentiment. When investors see signs that hiring is slowing or turning negative, they often assume the Fed will be more willing to cut rates to support the economy.

That’s exactly what has happened here. The weaker labor signal added to the idea that the Fed could deliver a 25-basis-point rate cut at its next meeting. As rate-cut expectations build, the US Dollar often loses some appeal because lower rates can reduce the advantage it offers compared with other major currencies.

Mixed US Services Numbers Still Leave Questions

The US also released services activity data that came in slightly stronger than expected. The ISM Services PMI rose a bit, suggesting the services sector remains in expansion territory. On the surface, that could have helped the Dollar.

But the details were less comforting. New orders eased, which can hint at slower demand ahead. Even more importantly, the employment index contracted again—marking the sixth straight month of contraction in that part of the survey. That doesn’t scream “crisis,” but it does support the idea that hiring conditions are weakening underneath the headline numbers.

So while the US services sector is still growing, the job-related parts of the data continue to send caution signals. And right now, markets are especially sensitive to labor market clues because they directly influence what the Fed might do next.

What Markets Are Watching Next: Jobless Claims and Inflation

Thursday’s US weekly Jobless Claims report is the next important checkpoint. Expectations point to a small rise in claims, which would fit the narrative of a labor market that is gradually losing steam. Even if the change is not dramatic, traders will watch whether the number continues to creep higher, because that trend can reinforce the case for rate cuts.

The bigger focus for the week, though, is Friday’s Personal Consumption Expenditures (PCE) Price Index. This inflation report matters because it is closely watched by the Fed and will be the last major inflation reading before the next policy meeting. If inflation shows further cooling, it could strengthen the argument for a near-term rate cut. If it stays sticky, it could complicate the picture and force markets to rethink how quickly the Fed can ease.

For EUR/USD, these releases matter because the pair is being pulled by expectations around central bank timing. If the Fed looks more likely to cut soon while the ECB looks steady, the policy gap can continue to lean in the Euro’s favor.

Why The ECB-Fed Policy Gap Matters for EUR/USD

At the heart of the current move is a familiar theme: central banks don’t always move together. Investors are increasingly pricing in a Fed cut at the next meeting and expecting additional cuts in the year ahead. Meanwhile, the ECB is widely expected to hold rates steady in December, and markets don’t see urgent signs of cuts on the horizon.

That divergence can matter even when day-to-day data is messy. When one central bank appears to be moving toward easier policy faster than the other, the currency tied to the “less dovish” central bank can benefit. In this case, that dynamic has supported the Euro, even as some Eurozone data has underwhelmed.

Summary

EUR/USD is holding near a five-week high because the US Dollar has weakened on rising expectations of Federal Reserve rate cuts. Eurozone retail sales stalled in October, which briefly weighed on the Euro, but stronger services data and steady signals from the ECB have helped keep the common currency supported. Markets are now watching US Jobless Claims and Friday’s PCE inflation report for clues that could confirm—or challenge—the idea that Fed policy is about to turn more accommodative.

GBPUSD climbs as the greenback softens on growing Fed rate-cut expectations

The Pound Sterling has been one of the stronger major currencies in the days following the UK budget announcement. Against the US Dollar, it has stayed close to its best levels in more than a month, supported by two forces moving in Sterling’s favor at the same time: a softer US Dollar and steady demand for the British currency after the government’s fiscal update.

During Thursday’s European session, the GBP/USD pair traded near the 1.3350 area, holding onto recent gains. The broader story is that traders are leaning more strongly toward lower US interest rates soon, while the UK’s budget message gave the Pound a confidence boost—at least for now.

Why the US Dollar Has Lost Ground Recently

A big reason GBP/USD is holding up is that the US Dollar has struggled across the board. When investors start to believe that the Federal Reserve is done tightening and is about to reduce rates, the Dollar often loses some of its appeal. That’s because higher interest rates can make a currency more attractive to hold, while lower expected rates can do the opposite.

GBPUSD has broken the descending channel on the upside

This week, expectations for a near-term Fed rate cut strengthened further. Many traders now see a 25 basis point cut as highly likely at the next policy meeting. The shift in thinking didn’t happen randomly—it reflects growing concern that the US labor market is cooling faster than expected.

The labor market signal traders are watching

One of the most talked-about data points was the latest ADP private payrolls report, which showed job losses for November rather than the modest job growth economists expected. In plain market logic, weaker hiring tends to reduce inflation pressure over time and gives the Fed more room to ease policy.

There’s also a broader theme shaping expectations: businesses are adapting to global changes in how work gets done, including greater use of Artificial Intelligence across many industries. Whether this is a temporary adjustment or a lasting shift, traders are treating it as another reason the job market could stay softer than before—and that matters a lot for interest rate forecasts.

Economic Data Isn’t All Weak, But the Fed Focus Remains Clear

To be fair, not every US indicator has been disappointing. A notable example is the latest reading from the ISM Services PMI, which surprised to the upside. Services activity appeared to improve rather than slow, a sign that parts of the economy are still holding up.

So why does the US Dollar still look tired?

Because right now, markets are prioritizing the direction of interest rates more than a single strong report. Even if some areas of the economy remain resilient, investors tend to focus on whether the overall trend is cooling enough for the Fed to cut. And lately, the balance of evidence—especially around employment—has kept rate-cut expectations alive.

Sterling’s Post-Budget Boost: What’s Supporting It

Sterling’s strength hasn’t come only from a weaker Dollar. It has also been helped by the market’s reaction to the UK budget announced on November 26. Many investors saw it as less disruptive than feared, especially for households.

There was a sense of relief that the budget did not introduce a major new tax burden for everyday consumers. On top of that, the Labour Party’s commitment to avoiding additional borrowing for day-to-day spending helped calm some concerns about fiscal stability. In currency markets, anything that reduces uncertainty—especially around government finances—can support the local currency.

That doesn’t mean the UK suddenly has a perfect economic outlook. But in the short term, reduced fiscal drama can be enough to lift sentiment, particularly if markets had been positioned for worse.

Why Some Analysts Think the Rally May Fade

Not everyone believes Sterling’s rise will last. Goldman Sachs, for example, has warned that the rally could be temporary. Their view is based on two main concerns: a softer trend in UK economic data and the growing belief that the Bank of England may cut rates faster than many expect.

In other words, Sterling may be enjoying a post-budget bounce, but if the economy continues to lose momentum, that support can fade. Currency investors are always trying to look ahead. If they think UK interest rates will fall more quickly, that can reduce Sterling’s appeal, especially compared with other currencies.

UK data and sentiment: the key risk

The UK economy has faced regular questions about growth strength and household resilience. If incoming data continues to show weakening demand, softer consumption, or a cooling labor market, it becomes easier to argue that the Bank of England will shift toward a more supportive stance—and that usually means lower rates.

Bank of England Expectations: Cuts Are Back in the Spotlight

One of the biggest themes hanging over Sterling is what the Bank of England will do next. Many market participants expect a quarter-point cut at the December 18 policy meeting.

The argument is straightforward: if UK job market conditions keep deteriorating, policymakers may decide that rates are restrictive enough and that the next step should be easing. When traders begin to price in rate cuts, the currency may struggle to keep rallying unless there’s another strong reason for it to rise.

A note of resistance inside the BoE

Still, it’s not a one-way story. Bank of England rate-setter Megan Greene recently signaled that she would only support cuts if labor market conditions and consumer spending weaken further. That kind of pushback matters because it shows there is still debate inside the BoE.

For Sterling, this internal disagreement can create short bursts of support. If markets think some policymakers remain cautious about cutting too soon, then expectations for rapid easing can soften a bit—at least until new data forces the issue.

What Could Move GBP/USD Next

With GBP/USD holding near recent highs, the next direction may depend on how the next round of US data shapes rate expectations—especially data tied to consumer confidence and inflation.

On Friday, traders will be watching the preliminary Michigan Consumer Sentiment Index and inflation expectations. These reports matter because they can influence the Fed’s thinking. If consumers expect inflation to remain high, the Fed may feel less comfortable cutting quickly. If inflation expectations cool and confidence weakens, it can strengthen the case for easier policy.

There’s also a release of the US Personal Consumption Expenditure (PCE) Price Index for September. Even though PCE is a major inflation gauge, this particular release may not change much in practice because it is delayed and refers to an older period. Markets tend to react most strongly to fresh data that could change what the Fed does next, not numbers that describe the past.

Final Summary

Sterling has remained firm near recent highs against the US Dollar, supported by a post-budget lift in UK sentiment and a broader pullback in the Dollar. The key driver on the US side is growing confidence that the Federal Reserve will cut rates soon, encouraged by signs of weakening labor demand. On the UK side, the budget calmed some immediate fiscal worries, but major banks like Goldman Sachs believe Sterling’s strength may not last if UK data continues to soften and the Bank of England begins cutting rates more aggressively. The next big test for GBP/USD is whether incoming US confidence and inflation-expectations data reinforces the market’s view of easier Fed policy—or challenges it.