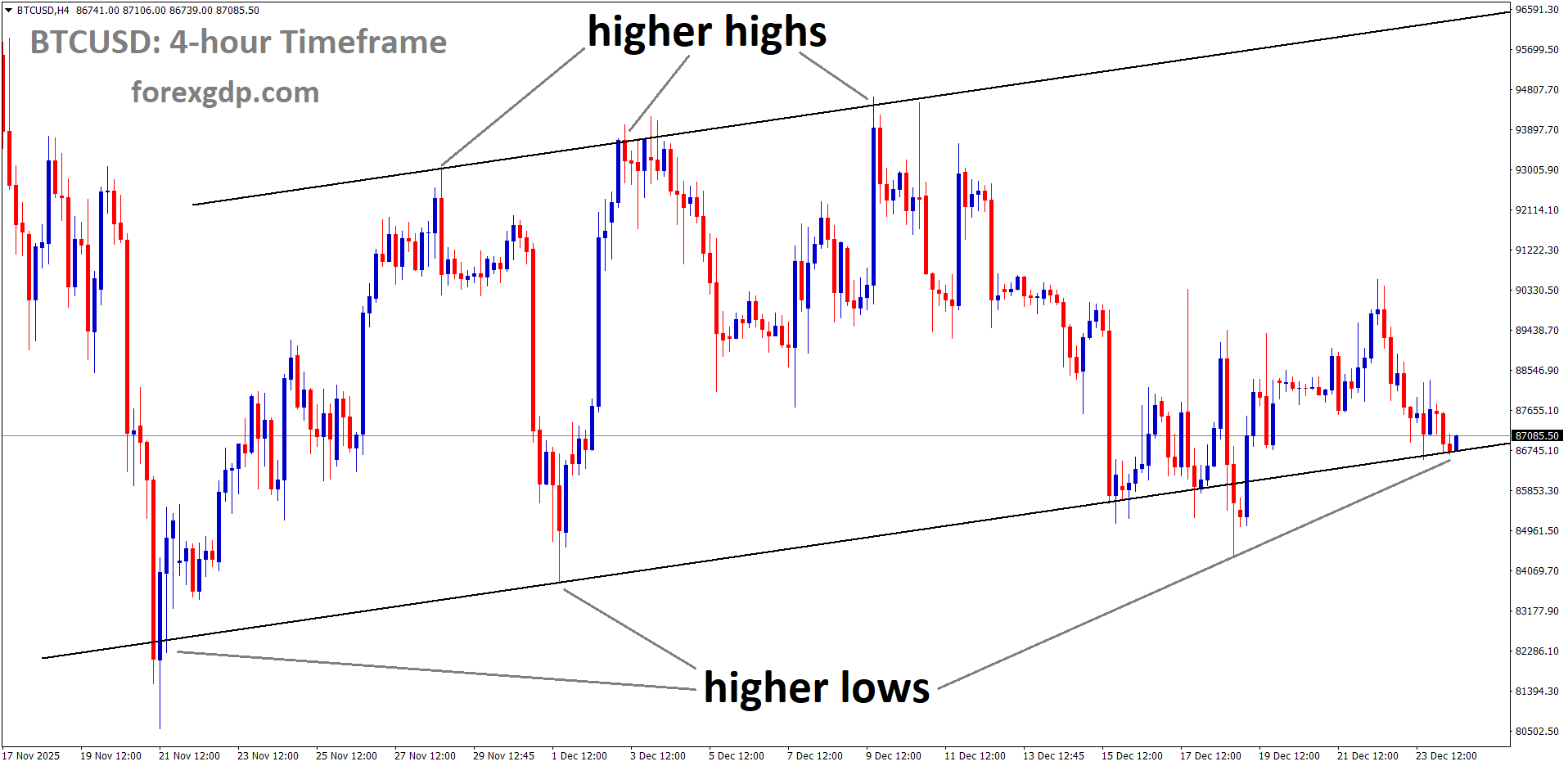

BTCUSD is moving in an uptrend channel, and the market has reached a higher low area of the channel

BTCUSD The Real Story Behind Bitcoin’s Near $100K Moment

Bitcoin hitting a new record can feel like a cultural moment. People talk about it at dinner, it trends online, and it feeds the idea that crypto is entering a new era. So when Bitcoin surged to an October peak of $126,000, many saw it as a powerful psychological milestone—especially because it looks comfortably above $100,000.

But a closer look tells a more sobering story. According to Galaxy Research, that headline number shrinks once you adjust for inflation and the falling purchasing power of the US dollar. In “2020 dollars,” the October high equals about $99,848—which means Bitcoin still missed the real six-figure mark by $152.

That detail may sound small, but it matters. It changes how people understand “all-time highs,” and it’s a reminder that money does not hold the same value year after year.

Why Inflation Changes the Meaning of “All-Time High”

When people say an asset reached a record price, they usually mean it in nominal terms—the raw number you see on a chart that day. The problem is that nominal prices don’t account for what the dollar can actually buy.

If the dollar loses value over time, then a future price needs to be higher just to have the same real-world purchasing power as an older price. In other words, the “number” can go up while the “real value” stays flat—or even falls.

Galaxy Research’s analysis highlights this exact issue. The firm looked at inflation data and adjusted Bitcoin’s peak to reflect the changing value of the US dollar since 2020. After that adjustment, Bitcoin’s October record no longer clears the $100K milestone in real terms.

This is a useful perspective for anyone who tracks Bitcoin as a long-term store of value. It also helps explain why some major milestones feel less meaningful when you zoom out and measure what those dollars are truly worth.

Galaxy Research’s Key Finding on Bitcoin’s Real Peak

The inflation-adjusted analysis was shared by Alex Thorn, Head of Research at Galaxy. The message was straightforward: Bitcoin’s nominal all-time high looks more dramatic than the inflation-adjusted reality.

Here’s the core takeaway:

-

Nominal October peak: $126,000

-

Inflation-adjusted (2020 dollars): $99,848

-

Short of $100K milestone: $152

That gap is tiny, but the larger point is big: in purchasing-power terms, Bitcoin has not yet posted a historical high above six figures.

This kind of adjustment is not about criticizing Bitcoin’s performance. It’s about measuring it in a way that reflects the real economy people live in—where groceries, rent, fuel, and everyday services cost more than they did just a few years ago.

How Much Has the US Dollar Weakened Since 2020?

Inflation has been one of the defining economic themes since 2020. Galaxy Research’s calculation aligns with a widely felt reality: most people notice that everyday items cost more, and savings don’t stretch as far.

The analysis points to an approximate 20% loss in the dollar’s purchasing power since 2020. Put simply, if something cost $100 in 2020, it could cost around $125 today. That means $1 today buys roughly 80% of what $1 bought in 2020.

A Simple Way to Think About It

If you earned and saved money in 2020, the value of those dollars has been quietly reduced by inflation. That does not mean your cash “disappeared,” but it does mean it buys less.

So when Bitcoin (or any asset) hits a new nominal high, part of that rise may simply reflect that the measuring stick—the dollar—has changed.

What the Consumer Price Index Has to Do With Bitcoin

Galaxy’s approach is tied to the Consumer Price Index (CPI), one of the most common ways economists measure inflation. CPI tracks how the prices of a typical basket of goods and services change over time.

Since 2020, CPI data has shown persistent inflation pressures. During the pandemic era, inflation climbed sharply and at one point surged above 9% in mid-2022. While inflation has cooled from those extreme levels, it has remained a continuing concern and has stayed above the Federal Reserve’s long-term 2% target.

In the data referenced in this discussion, the November CPI report showed inflation up 2.7% over the past 12 months. Even if that number is far lower than the peak, it still signals ongoing pressure on household budgets and business costs.

For Bitcoin watchers, CPI matters because it shapes how people think about:

-

protecting savings,

-

holding cash versus buying assets,

-

and whether “record highs” are truly record highs after inflation is considered.

The Bigger Trend: Investors Look for Protection When Money Loses Value

When inflation rises and the dollar weakens, investors often look for assets they believe can hold value better than cash. This idea is sometimes described as a “debasement trade,” meaning people move into assets that might be more resistant to the gradual erosion of fiat currency value.

This doesn’t apply only to crypto. Many investors also consider other assets during inflationary periods, depending on their goals and risk tolerance. But Bitcoin often enters the conversation because it is designed with limited supply, and it has built a reputation—right or wrong—as “digital gold.”

The key point here is not that Bitcoin automatically wins in an inflationary world. It’s that inflation changes investor behavior. It pushes more people to ask:

“Should I hold cash that buys less each year, or should I hold something else?”

Galaxy’s inflation-adjusted look at Bitcoin adds a useful layer to that conversation. It helps people separate excitement over big numbers from the more practical question of real purchasing power.

Why “Real Returns” Matter More Than Headlines

A nominal price milestone is easy to celebrate because it’s clear and simple. But over multiple years, real returns are what determine whether an investment truly improved someone’s financial position.

Inflation-adjusted thinking helps answer questions like:

-

Did this asset actually increase my ability to buy goods and services?

-

Or did it just rise alongside a weakening currency?

-

How does this “new high” compare to previous highs in real terms?

This is especially important for long-term holders, retirement planners, and anyone measuring performance across several years. A chart might show growth, but inflation can quietly take part of that gain away.

So while Bitcoin’s nominal $126,000 peak was a major moment, the inflation-adjusted reality suggests the story is slightly less dramatic—and also more honest.

Final Summary

Bitcoin’s October peak of $126,000 looked like a clean break into six figures, but Galaxy Research’s inflation-adjusted analysis shows a different picture. Measured in 2020 dollars, that peak equals about $99,848—just $152 short of the real $100,000 milestone. The gap is explained by the US dollar’s reduced purchasing power since 2020, after years of inflation pressure tracked through CPI. The bigger takeaway is simple: when comparing multi-year performance, real value matters as much as the headline number, and inflation can change what “all-time high” truly means.

EURUSD steady around 1.1800 as holiday-quiet trading keeps moves limited

EUR/USD is moving sideways near 1.1800 as the Christmas holiday period approaches and trading activity slows down. With many market participants stepping away from their desks, volumes tend to thin out, and big moves become less common. In this quieter setting, the pair is holding on to recent gains after briefly touching its strongest level in months earlier in the day.

What’s interesting is that the US Dollar is not finding much support, even though recent US economic data looks strong on the surface. At the same time, shifting expectations around interest rates on both sides of the Atlantic are shaping the mood, helping the Euro stay steady and keeping the overall tone mildly supportive for EUR/USD.

EURUSD is moving in an uptrend channel, andthe market has reached a higher high area of the channel

A quiet holiday market is keeping EUR/USD in a tight range

Late December often brings a different kind of trading environment. Many large institutions reduce their activity, and liquidity drops as the calendar moves closer to Christmas. When fewer trades are flowing through the market, prices can still shift, but they often do so in smaller steps and within tighter ranges.

That’s exactly what EUR/USD is showing right now. The pair is hovering around 1.1800, taking a pause after its recent climb. Instead of pushing sharply higher or reversing lower, it’s doing what currencies often do at this time of year: settling into a consolidation phase.

This type of movement is not always about a lack of interest. It’s more about timing. Traders may simply prefer to wait for the new year, when normal volumes return and the market has clearer direction from fresh data, policy signals, and broader risk appetite.

Why the US Dollar is struggling even with strong growth numbers

Normally, strong US economic growth can help the Dollar because it suggests the economy can handle higher interest rates and may attract global investment. Recent numbers showed the US economy expanded at a fast pace in the third quarter, beating expectations and improving on the prior quarter’s growth rate.

But the market isn’t reacting as strongly as you might expect. One reason is that investors are looking beyond the headline growth figure and asking a different question: Is this growth strong enough in the areas that matter most for future policy decisions?

Growth looks solid, but the labor story matters

A key concern for traders is whether strong growth is being matched by strong labor-market momentum. If job growth and wage trends don’t look convincing, the market may doubt that the economy has the kind of broad strength that would keep interest rates higher for longer.

There’s also a sense that the US growth picture is not evenly shared. Some parts of the economy appear to be doing very well, while others are under pressure from inflation and softer employment conditions. That uneven balance can lead investors to think the Federal Reserve may eventually lean toward supporting the economy with easier policy.

Politics and central bank independence are also part of the mix

The US Dollar can also be sensitive to political headlines, especially when they touch on interest rates and central bank decision-making. Comments from President Donald Trump criticizing monetary policy and calling for lower rates have added another layer of uncertainty.

Even if the Federal Reserve remains independent, public pressure and political noise can make markets uneasy. When investors feel less confident about policy stability, the Dollar can lose some of its appeal as a “safe and steady” currency. This has helped keep the broader Dollar index near recent lows, which indirectly supports EUR/USD.

Rate expectations are shaping sentiment more than any single data release

In currency markets, interest rate expectations often matter more than one economic report. Traders are constantly trying to anticipate where central banks are headed, because rate paths influence capital flows and investor demand for a currency.

Right now, the discussion is increasingly focused on whether the Federal Reserve could move toward a more supportive stance in the coming years. Market-based expectations suggest that investors see meaningful chances of rate cuts by 2026, and that view is starting to weigh on the Dollar.

Why markets think the Fed may turn more cautious

Part of the reasoning comes from how growth is being created. A lot of strength appears linked to business investment, including spending tied to artificial intelligence and other major upgrades. That’s positive, but it can also mean the economy is being driven more by corporate investment cycles than by broad consumer strength.

Meanwhile, households—especially those in lower- and middle-income groups—may still feel squeezed by the effects of inflation and a less supportive job market. If consumer demand softens, it becomes harder to maintain fast growth over time, and that can feed expectations of a more accommodative Fed.

In other words, the market is not only asking how fast the economy grew, but also how sustainable that growth looks and who is powering it.

The Euro is holding up as the ECB keeps its options open

On the European side, the European Central Bank has kept its key interest rates unchanged. Comments from ECB President Christine Lagarde have signaled confidence that the central bank is in a workable position, while still leaving room to respond if conditions change.

This stance matters because it supports the idea that Europe is not rushing into cuts. Even if the Eurozone is not booming, markets currently see only a limited chance of an early rate cut in 2026. That contrast—between a Fed that markets think could ease and an ECB that appears more patient—helps explain why EUR/USD is maintaining a constructive tone.

A cautious ECB can still support the currency

It’s easy to assume that a cautious central bank automatically weakens a currency, but that’s not always true. If the market believes a central bank is unlikely to cut soon, that can be supportive—especially if the other side of the pair is expected to become more accommodative.

In this case, the Euro benefits from the perception that the ECB is not under immediate pressure to change course quickly. That doesn’t guarantee a strong rally, but it can help limit downside moves and encourage buyers to stay engaged on dips.

What to watch as the year ends

With the holidays close, traders are often reluctant to take large new positions. That’s why EUR/USD may continue moving in a calm, range-bound way for now. Still, the story underneath remains important, because it can shape how the pair behaves once normal market activity returns in early January.

Here are a few themes likely to stay in focus:

US policy messaging and rate expectations

Any shift in how investors view the Fed’s future path can quickly influence the Dollar. Even without new major data, changes in sentiment can move currencies.

How balanced US growth really is

If markets continue to feel that growth is strong in corporate areas but weaker for consumers, that may keep pressure on the Dollar and support EUR/USD.

The ECB’s tone going into 2026

If European policymakers continue signaling patience, the Euro may remain resilient, especially if US rate expectations stay tilted toward future cuts.

Summary

EUR/USD is steady near 1.1800 as holiday-thinned trading keeps the pair in a narrow range. Despite strong US growth data, the US Dollar is struggling to gain lasting support, with investors paying close attention to labor-market momentum and the sustainability of demand. Political pressure around interest rates has also added uncertainty, limiting Dollar strength. Meanwhile, the ECB’s decision to keep rates unchanged and its flexible “options open” messaging has helped the Euro hold firm. As the year closes, the overall balance of rate expectations continues to support a calm consolidation phase, with a mildly constructive bias for the Euro.

GBPUSD Rallies While the Dollar Slips on Growing Rate-Cut Expectations

The Pound Sterling has pushed higher against the US Dollar, rising to around 1.3535, its strongest level in roughly three months. This move has caught attention because it comes even after the United States reported surprisingly strong economic growth. Normally, a solid growth headline would be supportive for the Dollar. But this time, the market reaction has been different.

GBPUSD is moving in a descending channel, andthe market has reached the lower high area of the channel

A big reason is that traders are still leaning toward the idea that the Federal Reserve could cut interest rates in 2026, even if the US economy looks healthy on the surface. As a result, the US Dollar has struggled to find support, and the Pound has been able to extend its gains during the European trading session on Wednesday.

Why the US Dollar Is Weak Even After Strong GDP Data

On Tuesday, the US Bureau of Economic Analysis released preliminary figures showing the US economy expanded at an annualized 4.3% pace in the third quarter, a faster rate than the 3.8% seen in the previous quarter. That is a strong number by any standard, and at first glance it suggests momentum is holding up well.

But markets don’t trade on growth alone. They trade on what growth means for inflation, jobs, and—most importantly—interest rates. Right now, investors appear to believe that even with solid GDP, the bigger story is still about where the Fed is heading next.

One clear sign of this thinking is the broader performance of the Dollar. The US Dollar Index (DXY), which measures the Dollar against a basket of six major currencies, slid to an 11-week low near 97.75 during the same period. That tells you the weakness isn’t just about the Pound being strong—it’s also about the Dollar being broadly soft.

What traders are pricing in for the Fed

Interest-rate expectations are a major driver of currency moves. According to market pricing reflected in the CME FedWatch tool, traders see a 70.6% chance that the Federal Reserve will reduce interest rates by at least 50 basis points in 2026. This is a larger amount of easing than what Fed officials have hinted at in their own projections, which pointed to a more limited pace of cuts next year.

So even though GDP growth looked impressive, it did not meaningfully shake the belief that the Fed could turn more supportive later. And when the market believes interest rates may fall, that tends to weigh on the currency.

The GDP story: strong growth, but uneven benefits

Another reason the Dollar isn’t gaining traction is that investors are looking beyond the headline number. The GDP report showed that businesses have been investing heavily, particularly in equipment and Artificial Intelligence (AI). That kind of spending can boost growth and productivity over time, but it doesn’t always translate into broad-based improvements for households right away.

Some economists have described the current trend as a K-shaped recovery, meaning different groups experience the economy very differently. In this view, higher-income households continue spending comfortably—especially on leisure and recreational activities—while low- and middle-income households face more pressure.

Inflation has remained a key factor in that divide. Even if price growth has cooled from earlier extremes, the impact of higher living costs still lingers, and many households remain sensitive to changes in employment conditions. The labor market, in particular, is a focus because job growth and wage strength are central to how long the Fed can keep policy tight without risking a slowdown.

In short, the US can post strong GDP growth while still leaving markets unconvinced that rates need to stay high for longer. That’s the kind of backdrop that can keep the Dollar under pressure.

Pound Sterling Supported by a Steady Bank of England Message

While the Dollar has been weakening, the Pound has also had its own reasons to look steadier. Sterling has held firm since the Bank of England’s policy decision last Thursday, which kept the tone of monetary easing cautious and gradual.

The BoE cut interest rates by 25 basis points to 3.75%, and the decision was notably close, with a 5–4 vote split. A tight vote like that often signals uncertainty inside the central bank, and it can also suggest that policymakers are not fully aligned behind a rapid series of cuts.

Importantly, the BoE indicated that any further easing would likely be slow and measured, rather than aggressive. That stance matters for currency markets. A central bank that is cutting rates quickly usually puts more downward pressure on its currency. But a central bank that trims cautiously—especially when inflation is still above target—can help its currency stay supported.

Inflation is cooling, but still above target

UK inflation has eased in recent months, which gives the BoE some room to gradually reduce rates. Headline inflation was reported at 3.2% year-over-year in November, down from the 3.8% peak seen during the July-to-September stretch. That cooling trend is helpful, but it’s still well above the BoE’s 2% target, which explains why the central bank has avoided sounding too relaxed.

At the same time, the BoE has acknowledged that the UK labor market remains on the softer side. That weakness is one of the reasons rate cuts are still on the table at all. If hiring remains sluggish or unemployment trends higher, policymakers may feel more pressure to support growth with lower borrowing costs.

What investors expect from the Bank of England in 2026

Looking ahead, markets are now debating how far and how fast the BoE will go. Traders are trying to balance two realities: inflation is easing, but not yet where the BoE wants it; and the labor market appears weak enough to justify additional policy support.

According to a Reuters report, investors are currently expecting the BoE to deliver at least one additional 25-basis-point rate cut in the first half of 2026. That expectation isn’t extreme, but it is meaningful. It suggests the market sees gradual easing continuing—without assuming the BoE will rush into a series of reductions.

For the Pound, this “slow-cut” outlook can be supportive. If the UK is expected to cut rates only modestly while the US market increasingly prices in a more dovish Fed path, Sterling can benefit from the relative shift in expectations.

The next key moment: US Jobless Claims

With GBP/USD hovering near recent highs, traders will be watching incoming US data for a clearer signal on the labor market. The next major release on Wednesday is US Initial Jobless Claims, due at 13:30 GMT.

Jobless claims may sound like a small weekly number, but they can influence the bigger narrative. If claims rise meaningfully, it strengthens the argument that job creation is slowing, which can reinforce expectations for future Fed rate cuts. If claims come in lower than expected, the Dollar could get a short-term boost, especially if traders believe the labor market remains resilient.

Either way, the market mood has already been set: investors are treating the Dollar cautiously, and the Pound is taking advantage of that weakness.

Summary

Sterling has moved up toward 1.3535, supported by a softer US Dollar and steady expectations that the Federal Reserve could cut rates in 2026. Even a strong 4.3% US GDP reading has not been enough to shift sentiment, partly because investors see signs that growth benefits are uneven and job creation may not be strong enough to keep policy tight for long. On the UK side, the Bank of England’s gradual easing message, following a 25-basis-point cut to 3.75%, has helped the Pound stay resilient. Attention now turns to US Initial Jobless Claims at 13:30 GMT, which could shape near-term direction by influencing how traders view the US labor market and the Fed’s next steps.