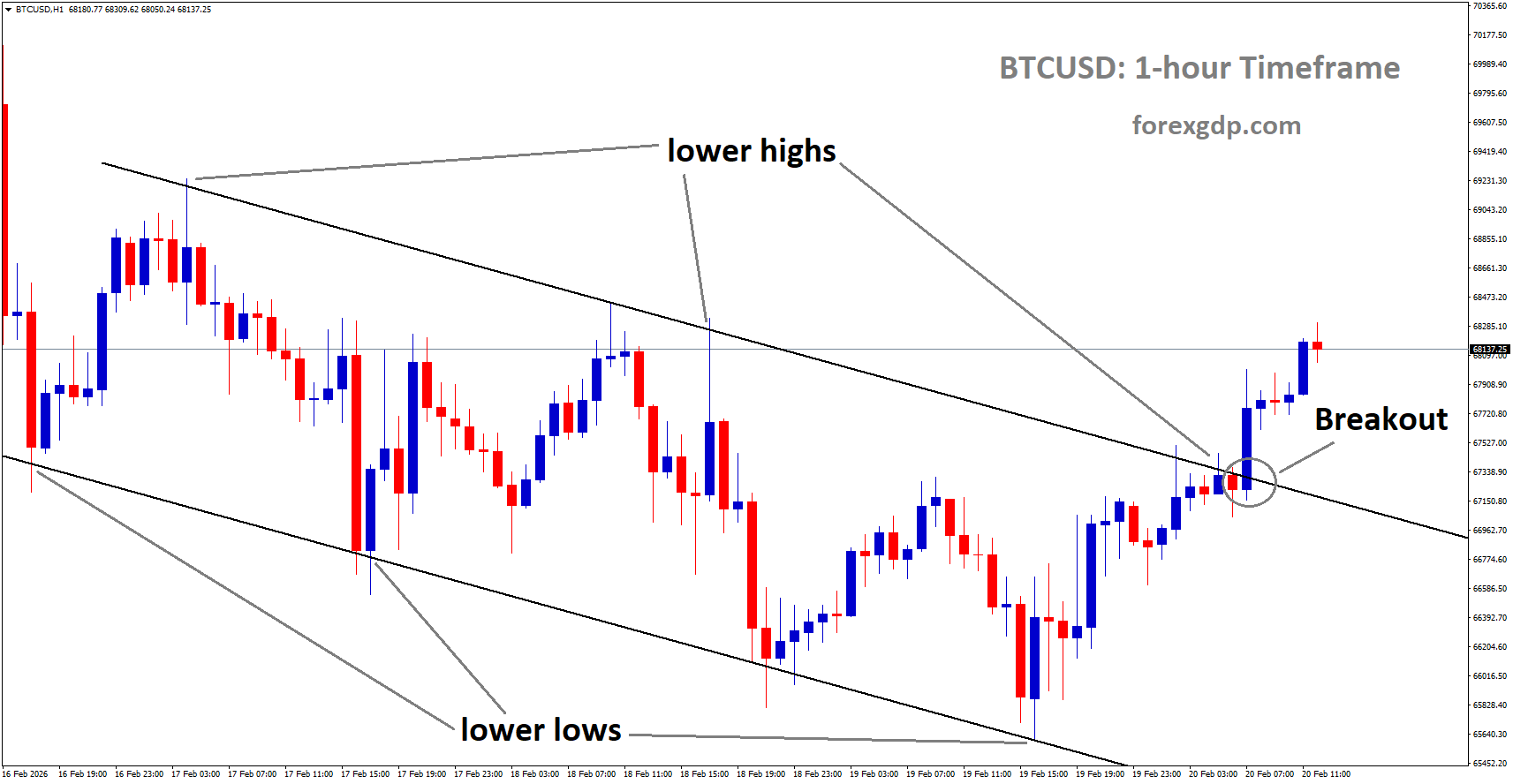

BTCUSD has broken the descending channel in upside

BTCUSD Watches Closely as US Signals a New Direction on Global Trade

The United States has agreed to lower its tariff rate on imports from Indonesia, cutting it from 32% down to 19%. On its own, that might sound like a simple trade-policy adjustment. But when you look at the bigger picture—how similar deals are appearing across Asia, how consumers are feeling the pressure of inflation, and how global markets react to calmer economic signals—it becomes easier to see why this story is getting attention beyond the world of shipping and exports.

At the same time, the crypto market has moved upward, with total market value rising by about 1.48% over a recent period. No single policy decision “causes” crypto to rise or fall overnight, but macroeconomic shifts can influence investor mood and the amount of money people feel comfortable putting into riskier assets. Tariff changes can be one of those shifts, especially when they hint at softer policy ahead.

This tariff move with Indonesia is also part of a wider trend. Other countries in the region have landed similar tariff levels, which suggests the US may be easing its approach compared to earlier, tougher positions. For investors—crypto investors included—signals like that often matter, because they can reduce uncertainty and help people plan with more confidence.

What the US–Indonesia Tariff Deal Actually Changes

Indonesia and the United States reached an agreement that reduces the US tariff rate on Indonesian goods to 19%. In addition to the lower headline rate, a number of items are reportedly set to receive exemptions, meaning they can enter the US at a 0% tariff rate.

These exempt products include well-known Indonesian exports such as palm oil, rubber, and cocoa, among others. That matters because these industries are central to Indonesia’s economy. When major exports get easier access to the US market, it can support jobs, stabilize business confidence, and strengthen trade relationships.

Indonesia’s senior Economic Minister, Airlangga Hartarto, described the agreement as beneficial for both sides, saying it respects the sovereignty of each country. That kind of language is worth noting. Trade talks can often be tense, and when leaders frame an outcome as balanced, it usually signals that negotiations reached a stable middle ground rather than forcing one side into an uncomfortable compromise.

A White House fact sheet also described the deal as meaningful for multiple areas of the economy—especially agriculture, manufacturing, and digital sectors. In return, Indonesia has agreed to remove barriers on more than 99% of American exports, according to the same fact sheet. In other words, the agreement is not only about lowering US tariffs. It is also about expanding access for US businesses selling into Indonesia.

Why tariff exemptions matter as much as the percentage

A 19% tariff is a big drop from 32%, but the exemptions may be just as important. Exemptions can help certain industries avoid extra costs entirely, which can have a more immediate impact on trade volumes and supply chains. For businesses, a clear exemption can also be easier to plan around than a reduced-but-still-present tariff rate.

Indonesia Isn’t Alone: Similar Tariff Levels Across the Region

This deal is not happening in isolation. Several countries in Southeast Asia are now grouped in similar tariff ranges when exporting to the United States. Indonesia’s new 19% rate puts it alongside countries such as Cambodia, Malaysia, the Philippines, and Thailand. Vietnam also appears in the broader list, with a slightly higher rate of 20%.

More broadly, another recent example is India, which reportedly secured a deal that lowers its tariff rate to 18% from a much higher level previously discussed. Full details are expected after the official agreement is finalized, but the direction of the change is what many observers are focused on.

When you see multiple countries landing in roughly the same neighborhood of tariff rates, it sends a message: the US may be aiming for a more standardized approach, rather than pushing unusually high rates across the board. That matters because markets tend to dislike uncertainty. Even when a tariff rate is not “low,” a stable and predictable structure can be easier for businesses and investors to navigate.

A softer stance can reduce market stress

When trade policy looks less aggressive, it can reduce fears of sudden cost spikes or new barriers that disrupt supply chains. That doesn’t mean every problem disappears. But it can lower the overall tension level, which sometimes supports broader investor confidence.

How Tariffs Connect to the Crypto Market

At first glance, tariffs and crypto might seem unrelated. One is about physical goods and international trade. The other is about digital assets, online networks, and global finance. But they can meet in the middle through something simple: how people feel about the economy and how much spare money they think they have.

There has been growing discussion about how tariff-driven inflation can squeeze households, especially lower-income consumers. When everyday costs rise—food, transport, basic necessities—people have less room to save or invest. That includes investing in higher-risk options like cryptocurrencies.

If tariffs are reduced or structured in a more balanced way, it may ease some inflation pressure over time. That doesn’t mean prices instantly fall, and it doesn’t guarantee relief for every household. But it can support a more stable economic environment, which is often when people start thinking about rebuilding savings and gradually returning to investing.

From a crypto perspective, that matters because crypto markets are heavily influenced by liquidity—how much money is actively flowing into investments. When everyday financial pressure is intense, people usually prioritize essentials. When pressure eases, some investors—especially younger or retail investors—start allocating small portions of their portfolios to assets like Bitcoin, Ethereum, and other major cryptocurrencies.

Why Bigger Investors Watch These Signals Too

Retail investors aren’t the only ones paying attention. Larger investors and institutions often look at broader trends in economic policy. They don’t typically buy crypto because a single tariff rate changed. But they do consider whether the overall environment is becoming calmer or more unpredictable.

If trade policy appears to be moving toward negotiation and standardization, some investors interpret that as a “risk-on” signal—meaning they may feel more open to assets that can offer growth, even if they also carry volatility. Crypto is one of those assets.

At the same time, professional investors also react to narrative. A market doesn’t move only on numbers; it moves on stories people believe. A story like “policy pressure is easing” can encourage optimism. And in crypto, optimism can be powerful—sometimes more powerful than people expect.

Crypto Market Movement and What It May Suggest

The crypto market’s total value has recently climbed by about 1.48%, with collective market value around $2.33 trillion. That kind of move, by itself, isn’t unusual in crypto. This is a market that can shift quickly, sometimes within hours. But in context, even small gains can reflect a broader mood: investors may be feeling slightly more comfortable taking positions, or at least holding steady rather than pulling money out.

BTCUSD is moving in a descending channel, and the market has rebounded from the lower low area of the channel

It’s also worth remembering that the crypto market is global. Trade policy decisions in the US can influence global sentiment because the US remains a major driver of financial conditions. When the US signals more cooperative trade relationships, it can ripple outward into stocks, currencies, and digital assets.

Crypto reacts to confidence as much as it reacts to news

Even when a policy change isn’t directly tied to crypto, it can still shape how investors feel about the future. Confidence doesn’t guarantee gains, but it can encourage participation—especially when people have been cautious for a long time.

Final summary

The US decision to reduce tariffs on Indonesian imports from 32% to 19%, along with exemptions for key products, is more than a trade headline. It fits into a wider pattern of similar tariff levels across neighboring countries, suggesting a possible shift toward a less aggressive and more standardized trade approach. While tariffs don’t directly control crypto prices, they can influence inflation pressure, consumer confidence, and overall market sentiment. With the crypto market also posting a modest rise in total value, this kind of policy shift may contribute to a calmer environment where both everyday investors and larger players feel more willing to allocate funds toward higher-risk assets.

EURUSD Steadies Around 1.1750 Before Crucial US Figures and Eurozone Activity Updates

The EUR/USD currency pair is moving in a narrow range, holding steady around the 1.1770 level during the early Asian trading session on Friday. While there is no strong movement in either direction, the market is far from calm. Traders are closely watching political developments in Europe and important economic reports from the United States that could shape the pair’s next move.

EURUSD is moving in an ascending channel, and the market has fallen from the higher high area of the channel

At the center of attention is growing uncertainty around the leadership of the European Central Bank (ECB). At the same time, strong signals from the US economy and the Federal Reserve are giving the US Dollar some support. With major economic data releases scheduled later in the day, investors are staying cautious.

ECB Leadership Speculation Adds Pressure on the Euro

One of the key factors influencing the Euro right now is speculation about the future of ECB President Christine Lagarde. According to reports, Lagarde may leave her position before completing her full eight-year term. This possibility has sparked conversations across financial markets.

If Lagarde steps down early, it could open the door for new leadership at the ECB sooner than expected. Political leaders such as French President Emmanuel Macron and German Chancellor Friedrich Merz may have the opportunity to influence the selection of the next ECB president before the French presidential election in April 2027.

Why Leadership Changes Matter

Leadership at the ECB plays a major role in shaping monetary policy across the Eurozone. The ECB is responsible for controlling inflation, setting interest rates, and maintaining financial stability. Any change at the top can lead to shifts in policy direction or create uncertainty about future decisions.

Investors generally prefer stability and clear guidance. When there is speculation about leadership changes, it can make markets nervous. In this case, the uncertainty is limiting the Euro’s ability to gain strength. Even if economic data from Europe shows improvement, doubts about future ECB leadership may keep traders cautious.

Strong US Data Supports the Dollar

While the Euro faces pressure from political uncertainty, the US Dollar is finding support from solid economic data and firm messaging from the Federal Reserve.

Recent labor market data from the United States has been stronger than expected. A healthy job market suggests that the US economy remains resilient. When employment levels are strong, consumer spending often follows, which can support overall economic growth.

In addition, the latest minutes from the Federal Open Market Committee (FOMC) have added to the Dollar’s strength. The minutes revealed that several Federal Reserve officials are concerned about inflation remaining above their 2% target.

The Fed’s “Two-Sided” Policy Approach

According to the FOMC minutes, policymakers discussed the possibility that interest rates could be increased again if inflation does not slow down as expected. They emphasized a “two-sided” approach to future policy. This means they are prepared to act if inflation stays high, but they are also aware of risks to economic growth.

This balanced yet cautious stance has given the US Dollar an edge. When markets believe that interest rates may stay higher for longer, the currency often benefits. That is because higher rates can attract foreign investment, increasing demand for the currency.

For the EUR/USD pair, this creates a challenge. A stronger Dollar naturally puts downward pressure on the pair, making it harder for the Euro to rise.

All Eyes on US GDP and PCE Reports

The next major test for the EUR/USD pair will come from important US economic data scheduled for release later on Friday. Traders are particularly focused on two key reports: the flash fourth-quarter Gross Domestic Product (GDP) data and the Personal Consumption Expenditures (PCE) inflation report.

What GDP Tells Us

GDP measures the total value of goods and services produced in a country. It is one of the most important indicators of economic health. If the US economy grew strongly in the fourth quarter, it would reinforce the view that the economy remains solid despite high interest rates.

Stronger GDP data could further support the US Dollar. On the other hand, if the report shows weaker-than-expected growth, it might raise concerns about a slowdown. In that case, the Dollar could lose some strength, giving the Euro a chance to recover.

Why the PCE Report Matters

The PCE report is the Federal Reserve’s preferred measure of inflation. It tracks changes in the prices consumers pay for goods and services. Because inflation remains a top priority for the Fed, this report carries significant weight.

If the PCE data shows that inflation is cooling, it could reduce pressure on the Fed to tighten policy further. This might weaken the Dollar slightly. However, if inflation remains stubbornly high, expectations for a stricter monetary stance could grow, supporting the Greenback once again.

Eurozone PMI Data Also in Focus

While US data is taking center stage, traders are also watching economic releases from Europe. Preliminary Purchasing Managers’ Index (PMI) readings from the Eurozone and Germany are due for release.

PMI data provides insight into business activity in the manufacturing and services sectors. A reading above 50 usually signals expansion, while a reading below 50 suggests contraction.

Signals from Europe’s Largest Economy

Germany, as the largest economy in the Eurozone, plays a critical role in the region’s overall performance. If German PMI data shows improvement, it could offer some support to the Euro. Stronger business activity suggests economic resilience.

However, if the data disappoints, it may add to concerns about slowing growth in the region. Combined with leadership uncertainty at the ECB, weak PMI figures could make it difficult for the Euro to gain traction.

A Market in Waiting Mode

At the moment, the EUR/USD pair appears to be in a holding pattern. Traders are not making bold moves ahead of important data releases and clearer signals from central banks.

On one side, the Euro faces political uncertainty tied to ECB leadership speculation. On the other side, the US Dollar benefits from strong economic data and firm guidance from the Federal Reserve.

This balance of forces is keeping the pair relatively stable. However, the calm may not last long. Once the GDP and PCE data are released, along with Eurozone PMI figures, markets could react quickly.

What Could Happen Next?

Several scenarios are possible:

-

If US data comes in strong and inflation remains elevated, the Dollar may extend its strength.

-

If US growth slows and inflation cools, the Dollar could ease, giving the Euro room to rise.

-

If Eurozone data surprises to the upside and ECB leadership concerns fade, the Euro might find renewed support.

-

If European data disappoints while US data remains solid, pressure on the Euro could increase.

Currency markets often move quickly when expectations shift. That is why traders are watching these upcoming releases closely.

Final Thoughts

The EUR/USD pair is currently stable, but important forces are building beneath the surface. Speculation about potential changes in ECB leadership is creating uncertainty for the Euro, while strong US economic data and firm messaging from the Federal Reserve are supporting the Dollar.

With key reports on US economic growth, inflation, and Eurozone business activity set to be released, the next moves in the currency pair may depend heavily on fresh data. For now, markets remain cautious, waiting for clearer signals before committing to a stronger direction.

GBPUSD Advances on Upbeat UK Economic Data While Markets Await Key US GDP Release

The Pound Sterling moved slightly higher against the US Dollar during European trading hours, hovering near the 1.3470 level. The British currency showed resilience after recovering from earlier losses, supported by stronger-than-expected economic data from the United Kingdom. At the same time, investors are closely watching upcoming economic figures from the United States, especially the latest Gross Domestic Product (GDP) report for the fourth quarter.

GBPUSD has broken the descending channel in upside

Currency markets are currently balancing positive signals from the UK with steady strength from the US Dollar. Both economies are sending mixed but important signals, shaping how traders and investors position themselves.

Strong UK Retail Sales Boost the Pound

One of the main drivers behind the Pound’s recent strength is the latest Retail Sales data from the UK. The Office for National Statistics reported that Retail Sales rose by 1.8% in January compared to the previous month. This increase came as a surprise to many economists, who had expected only a modest rise of around 0.2%.

Retail Sales are an important measure because they reflect how much consumers are spending. When people spend more money in shops and online, it usually signals confidence in the economy. Strong consumer spending can also support overall economic growth.

The January figures showed that UK consumers were more active than expected. This suggests that households may be feeling more comfortable despite ongoing concerns about inflation and the job market. As a result, the stronger spending data provided support to the Pound.

However, while the Retail Sales report was impressive, it may not completely change the broader outlook for monetary policy in the UK. Inflation has eased in recent months, and the labor market has shown signs of weakening. These factors still play a key role in shaping expectations about future decisions from the Bank of England.

Business Activity Improves in February

In addition to Retail Sales, the latest Purchasing Managers’ Index (PMI) data also gave the British currency a lift. The UK’s Composite PMI, which measures activity in both the manufacturing and services sectors, rose to 53.9 in February. This was slightly higher than January’s reading and better than market expectations.

A PMI reading above 50 indicates expansion, meaning business activity is growing. The February data suggests that the UK economy continues to expand at a steady pace.

Manufacturing Sector Shows Solid Growth

The manufacturing sector played a key role in the improved PMI reading. The Manufacturing PMI rose to 52.0, slightly above the previous figure. This points to stronger factory output and improved business conditions within the sector.

Manufacturing has faced several challenges in recent years, including supply chain disruptions and higher costs. A stronger reading may signal that some of these pressures are easing. Increased production can also lead to higher employment and more investment, which are positive signs for the broader economy.

Overall, the combination of strong Retail Sales and improving business activity has helped the Pound regain some ground. These data releases suggest that the UK economy may be more resilient than some had feared.

Bank of England Outlook Remains Balanced

While recent data has been positive, expectations around the Bank of England’s next steps remain cautious. Strong consumer spending and business activity could, in theory, reduce the likelihood of quick interest rate cuts. When an economy performs well, central banks often feel less pressure to ease policy.

However, the broader picture still shows cooling inflation and signs of softness in the labor market. Inflation has slowed in recent months, moving closer to more manageable levels. At the same time, employment conditions have weakened in the three months ending in December.

These mixed signals mean that policymakers are likely to take a careful approach. The Bank of England will continue to weigh economic growth against inflation risks before making any major decisions. For now, the positive data has supported the Pound, but future moves will depend on upcoming reports.

US Dollar Holds Firm Ahead of GDP Data

While the Pound has gained some strength, the US Dollar remains broadly firm. Investors are waiting for the preliminary US GDP data for the fourth quarter, which is expected to show that the economy expanded at an annual rate of 3%.

Although this pace would be slower than the previous quarter’s growth, it still represents solid expansion. A strong GDP reading would confirm that the US economy continues to perform well despite higher borrowing costs.

The US Dollar Index, which measures the Greenback against a basket of major currencies, has been trading near a multi-week high. This reflects ongoing demand for the US currency.

Federal Reserve Signals Patience on Rate Cuts

Another reason behind the Dollar’s strength is the latest meeting minutes from the Federal Open Market Committee. The minutes showed that policymakers are not in a hurry to cut interest rates.

Inflation in the United States remains above the Federal Reserve’s 2% target. Although price pressures have eased from their peak, they are still higher than desired. As a result, officials believe it is too early to begin lowering rates.

When investors expect interest rates to stay higher for longer, the US Dollar often benefits. Higher rates can attract foreign investment, increasing demand for the currency.

This cautious stance from the Federal Reserve has helped the Dollar outperform many of its peers in recent sessions.

Market Focus Shifts to Economic Data

With strong data coming from both sides of the Atlantic, currency markets are reacting to every new release. Traders are paying close attention to how economic growth, inflation, and central bank policies evolve.

In the UK, recent figures suggest that consumer spending and business activity are holding up better than expected. This has provided short-term support for the Pound. However, concerns about inflation trends and labor market weakness remain.

In the United States, steady economic growth and the Federal Reserve’s patient approach to rate cuts continue to support the Dollar. The upcoming GDP report is expected to offer further clarity on the strength of the US economy.

What This Means for the Pound and the Dollar

The current situation shows how closely currency movements are tied to economic performance and central bank decisions. Strong economic data tends to support a country’s currency, especially if it reduces the likelihood of interest rate cuts.

For the Pound Sterling, positive Retail Sales and PMI figures have helped offset earlier losses. These reports suggest that the UK economy still has momentum. However, future gains will depend on whether this strength continues and how the Bank of England responds.

For the US Dollar, solid growth expectations and a cautious Federal Reserve provide a firm foundation. If GDP data confirms ongoing expansion, the Dollar could remain well supported.

At the same time, any unexpected shifts in inflation or employment trends could quickly change the outlook.

Final Thoughts

The Pound Sterling has edged higher thanks to stronger UK consumer spending and improved business activity. These positive signs have boosted confidence in the British economy, at least in the short term.

Meanwhile, the US Dollar remains steady as investors await fresh GDP data and assess the Federal Reserve’s cautious stance on interest rates. With both economies showing resilience, currency markets are likely to remain sensitive to new economic updates.

In the days ahead, attention will remain focused on growth figures, inflation trends, and signals from central banks. These factors will continue to shape the path of the Pound, the Dollar, and the broader foreign exchange market.

GBPJPY Remains Subdued Below 209.00 Before Crucial UK Data Releases

The GBP/JPY currency pair has moved lower for a second straight session, reflecting growing pressure on the British Pound. During Friday’s Asian trading hours, the pair hovered near the 208.60 area as investors reacted to changing expectations around interest rates in the United Kingdom.

GBPJPY is moving in a box pattern, and the market has fallen from the resistance area of the pattern

At the heart of the recent weakness is the belief that the Bank of England (BoE) may reduce interest rates as early as March. This shift in outlook has weighed on the Pound Sterling, especially as fresh economic data from both the UK and Japan adds new layers to the story.

Why the Pound Sterling Is Under Pressure

The British Pound has been facing challenges due to rising expectations that the Bank of England will soon begin cutting interest rates. Financial markets have grown more confident that policymakers could take action at their March meeting.

This change in mood comes after a softer set of economic data from the UK.

UK Labor Market Shows Signs of Cooling

One of the key triggers for the shift in expectations was the latest UK labor market report. The unemployment rate rose to 5.2% in the three months leading up to December. At the same time, wage growth showed signs of slowing.

When unemployment increases and wage growth eases, it often signals that the economy is losing momentum. For central banks like the Bank of England, this can be a sign that interest rates may need to be lowered to support economic activity.

Slower wage growth also helps reduce inflation pressure. If workers are not seeing strong pay increases, businesses may feel less need to raise prices. This adds to the argument for rate cuts.

Inflation in the UK Continues to Cool

Another important factor is inflation. Recent data showed that UK inflation dropped to its lowest level in nearly a year. This decline has strengthened expectations that the Bank of England could move toward a more supportive stance.

Catherine Mann, a member of the BoE’s Monetary Policy Committee, welcomed the January inflation data. She described the headline Consumer Price Index (CPI) reading as encouraging. However, she also pointed out that core inflation remains slightly elevated.

Core inflation excludes more volatile items like food and energy. Even though it has come down, it is still above the central bank’s ideal level. This suggests that while inflation is easing, policymakers may remain cautious about moving too quickly.

Still, the overall trend toward lower inflation is giving markets confidence that a rate cut is possible in the near future.

Upcoming UK Data in Focus

Investors are also keeping a close eye on upcoming UK economic releases. Retail Sales figures and the S&P Global Purchasing Managers’ Index (PMI) reports are due later in the day.

These reports provide insight into consumer spending and business activity. If retail sales show weakness, it could reinforce the idea that the UK economy needs support. Similarly, weaker PMI data would point to slowing growth in manufacturing and services.

On the other hand, stronger-than-expected results could slow down expectations of immediate rate cuts. For now, however, sentiment appears tilted toward a more cautious economic outlook.

The Japanese Yen and Inflation Trends

While the Pound has been under pressure, the Japanese Yen has also faced its own challenges.

Recent inflation data from Japan showed that price growth is slowing. This has limited the Yen’s strength, even as the Pound struggles.

Japan’s Inflation Slows in January

Japan’s National Consumer Price Index rose by 1.5% year-over-year in January. This was lower than the previous reading of 2.1%, showing that inflation has cooled.

Core CPI, which excludes fresh food, increased by 2.0% compared to the previous year. This marked a decline from the earlier 2.4% figure and was in line with market expectations.

Another measure of inflation, which excludes both fresh food and energy, climbed by 2.6%. While still elevated, this too was lower than the prior month’s 2.9%.

The overall message from Japan’s inflation data is clear: price pressures are easing.

Government Measures and Cost of Living

The slowdown in inflation comes after government efforts to ease the cost of living for households. Measures aimed at reducing energy bills and other living expenses appear to be having an effect.

Lower inflation can reduce the need for tighter monetary policy. For the Bank of Japan, which has maintained an ultra-loose policy stance for years, easing price pressures may allow it to remain cautious about making major changes.

As a result, the Japanese Yen has softened somewhat, limiting how far GBP/JPY can fall. Even though the Pound is under pressure, the Yen is not gaining strong momentum.

How Rate Expectations Shape Currency Moves

Currency markets are highly sensitive to interest rate expectations. When traders believe a central bank will cut rates, the currency often weakens. This is because lower interest rates typically reduce the return on investments in that currency.

In the case of the UK, rising expectations of a March rate cut have reduced demand for the Pound. Investors may look for higher returns elsewhere if they believe UK interest rates will soon fall.

Meanwhile, Japan’s inflation slowdown does not currently point to aggressive tightening from the Bank of Japan. This means the Yen’s gains may remain limited for now.

The balance between these two forces—Pound weakness and modest Yen softness—has kept GBP/JPY under steady pressure without triggering a dramatic move.

What Traders and Investors Are Watching Next

Looking ahead, several factors could influence the direction of GBP/JPY:

-

Further UK economic data: Retail Sales and PMI reports will offer clues about the health of the economy.

-

BoE commentary: Any new remarks from policymakers could either strengthen or weaken rate cut expectations.

-

Japan’s policy signals: Updates from the Bank of Japan regarding inflation and monetary policy will also matter.

-

Global economic trends: Broader risk sentiment and global growth expectations can affect both the Pound and the Yen.

If UK data continues to disappoint, expectations for a March rate cut may grow even stronger. That would likely keep the Pound under pressure. On the other hand, signs of resilience in the UK economy could help stabilize the currency.

For Japan, sustained moderation in inflation may reduce speculation about policy tightening, which could limit gains for the Yen.

Final Summary

The GBP/JPY pair has declined for a second consecutive session as expectations of a Bank of England rate cut weigh heavily on the Pound Sterling. Softer UK labor market data and cooling inflation have strengthened the belief that policymakers may reduce rates in March.

Although a BoE official welcomed recent inflation improvements, core price pressures remain slightly elevated, keeping some uncertainty in the outlook. Meanwhile, Japan’s latest inflation figures show slowing price growth, which has softened the Yen and limited deeper losses in the currency pair.

As investors await fresh UK economic data and further guidance from central banks, GBP/JPY remains sensitive to changing interest rate expectations. The coming days will be crucial in shaping the next move for both the British Pound and the Japanese Yen.

AUDUSD Weakens with Slower Australian Economic Momentum in Focus

The Australian Dollar has come under pressure after fresh economic data showed that business activity in Australia slowed in February. At the same time, the US Dollar found support from stronger-than-expected labor market numbers in the United States. Together, these developments have pushed the Australian Dollar lower against its US counterpart.

AUDUSD is moving in a descending channel, and the market has reached the lower high area of the channel

Recent reports show that while Australia’s economy is still growing, the pace of expansion has cooled compared to the start of the year. Meanwhile, the US economy continues to show resilience, especially in the job market. This difference in momentum between the two economies is shaping currency movements and influencing investor sentiment.

Australia’s Business Activity Slows in February

New data from S&P Global’s Purchasing Managers’ Index (PMI) reveals that business activity in Australia continued to expand in February, but at a slower rate than in January.

The Composite PMI, which measures overall business conditions in both the services and manufacturing sectors, dropped to 52.0 in February from 55.7 the month before. Although this marks the seventeenth straight month of expansion, the lower number suggests that growth is losing speed.

A reading above 50 indicates expansion, while a figure below 50 signals contraction. So, while Australia’s economy is still growing, the latest data points to a moderation in activity rather than strong acceleration.

Services Sector Loses Momentum

The services sector, which makes up a large part of Australia’s economy, also showed signs of slowing. The Services PMI fell to 52.2 in February from 56.3 in January.

This suggests that businesses in areas such as finance, hospitality, and professional services are still expanding, but not as strongly as before. Slower growth in services can have a noticeable impact on the broader economy because it affects employment, consumer spending, and overall business confidence.

Companies reported softer demand and ongoing cost pressures. Even though inflation has cooled compared to previous peaks, price pressures remain present. This creates a challenging environment for businesses that must balance higher costs with cautious consumer spending.

Manufacturing Activity Eases

The manufacturing sector also experienced a slight slowdown. The Manufacturing PMI edged down to 51.5 from 52.3 in January.

While the sector remains in expansion territory, the pace of growth has clearly softened. Manufacturers are facing a mix of global and domestic challenges, including slower demand and lingering cost concerns.

Taken together, the weaker readings across services and manufacturing suggest that Australia’s economy is entering a more moderate growth phase. This shift has weighed on the Australian Dollar, as investors often prefer currencies tied to stronger economic momentum.

US Dollar Strengthens on Solid Job Market Data

While Australia’s growth showed signs of cooling, the US Dollar gained support from encouraging labor market data.

The US Department of Labor reported that Initial Jobless Claims fell to 206,000 for the week ending February 14. This was lower than both the previous week’s revised figure of 229,000 and market expectations of 225,000.

Initial Jobless Claims measure how many people are filing for unemployment benefits for the first time. A lower number typically indicates a strong labor market, as fewer people are losing their jobs.

The latest drop suggests that the US job market remains solid despite concerns about economic slowing in other areas. A healthy employment environment supports consumer spending, which is a major driver of the US economy.

Because of this, the US Dollar has attracted renewed buying interest. When economic data from the United States beats expectations, the Dollar often strengthens as investors see fewer reasons for aggressive policy easing.

Attention Turns to Upcoming US Data

Market participants are now looking ahead to key US economic releases, including preliminary fourth-quarter Gross Domestic Product (GDP) data and Personal Consumption Expenditures (PCE) figures.

GDP data will offer a broader view of how the US economy performed at the end of last year. Strong growth could further support the Dollar, while weaker figures might raise questions about future policy direction.

The PCE index, on the other hand, is closely watched as a preferred measure of inflation by US policymakers. If inflation remains elevated, it could influence expectations about interest rates in the months ahead.

These upcoming reports are expected to provide fresh direction for currency markets and could determine whether the US Dollar maintains its current strength.

Federal Reserve Minutes Add to Rate Speculation

Adding another layer of complexity, the minutes from the Federal Open Market Committee (FOMC) January meeting have revived discussions about possible future interest rate moves.

According to the meeting summary, most policymakers favored keeping interest rates unchanged for now. However, there was clear awareness of persistent inflation risks.

While only a few officials supported the idea of cutting rates, the broader message suggested that policymakers remain cautious. They indicated they would consider easing policy if inflation continues to moderate as expected.

At the same time, the possibility of further tightening was not entirely ruled out if inflation proves more stubborn than anticipated. This balanced yet cautious tone has kept investors alert.

For currency markets, expectations around interest rates are extremely important. Higher or stable rates in the United States compared to other countries can make the US Dollar more attractive to global investors seeking returns.

Why the Australian Dollar Is Under Pressure

The recent weakness in the Australian Dollar reflects a combination of domestic and international factors.

On the domestic front, slower PMI readings signal that Australia’s economic momentum is cooling. While the economy is still expanding, the softer pace raises concerns about how strong growth will be in the coming months.

Sticky inflation pressures also create uncertainty. If price growth remains elevated while economic activity slows, policymakers may face difficult decisions. This uncertainty can weigh on the national currency.

On the international side, the stronger US labor market and cautious stance from the Federal Reserve have boosted the US Dollar. When the Dollar gains strength, other currencies, including the Australian Dollar, often struggle in comparison.

The contrast between a moderating Australian economy and a resilient US labor market has been a key driver behind the recent currency moves.

What This Means for the Broader Economy

Currency movements do not just affect traders. They have wider implications for businesses, consumers, and policymakers.

A weaker Australian Dollar can make exports more competitive overseas, which may help certain industries. However, it can also increase the cost of imported goods, adding pressure to inflation.

For the United States, a strong Dollar can lower the cost of imports but may reduce the competitiveness of American exports abroad.

Central banks in both countries will continue to monitor economic data closely. Growth trends, employment figures, and inflation readings will all play a role in shaping future policy decisions.

Final Thoughts

The Australian Dollar has softened as new data shows that business growth in Australia slowed in February. Although the economy continues to expand, the pace has clearly moderated across both services and manufacturing sectors.

At the same time, the US Dollar has gained strength following better-than-expected jobless claims data, highlighting the resilience of the American labor market. Upcoming US GDP and inflation figures are likely to provide further direction for the currency markets.

With policymakers in both countries carefully watching inflation and growth trends, the balance between economic momentum and price stability will remain central to future movements. For now, the combination of slower Australian growth and stronger US data has tilted the scales in favor of the US Dollar.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!