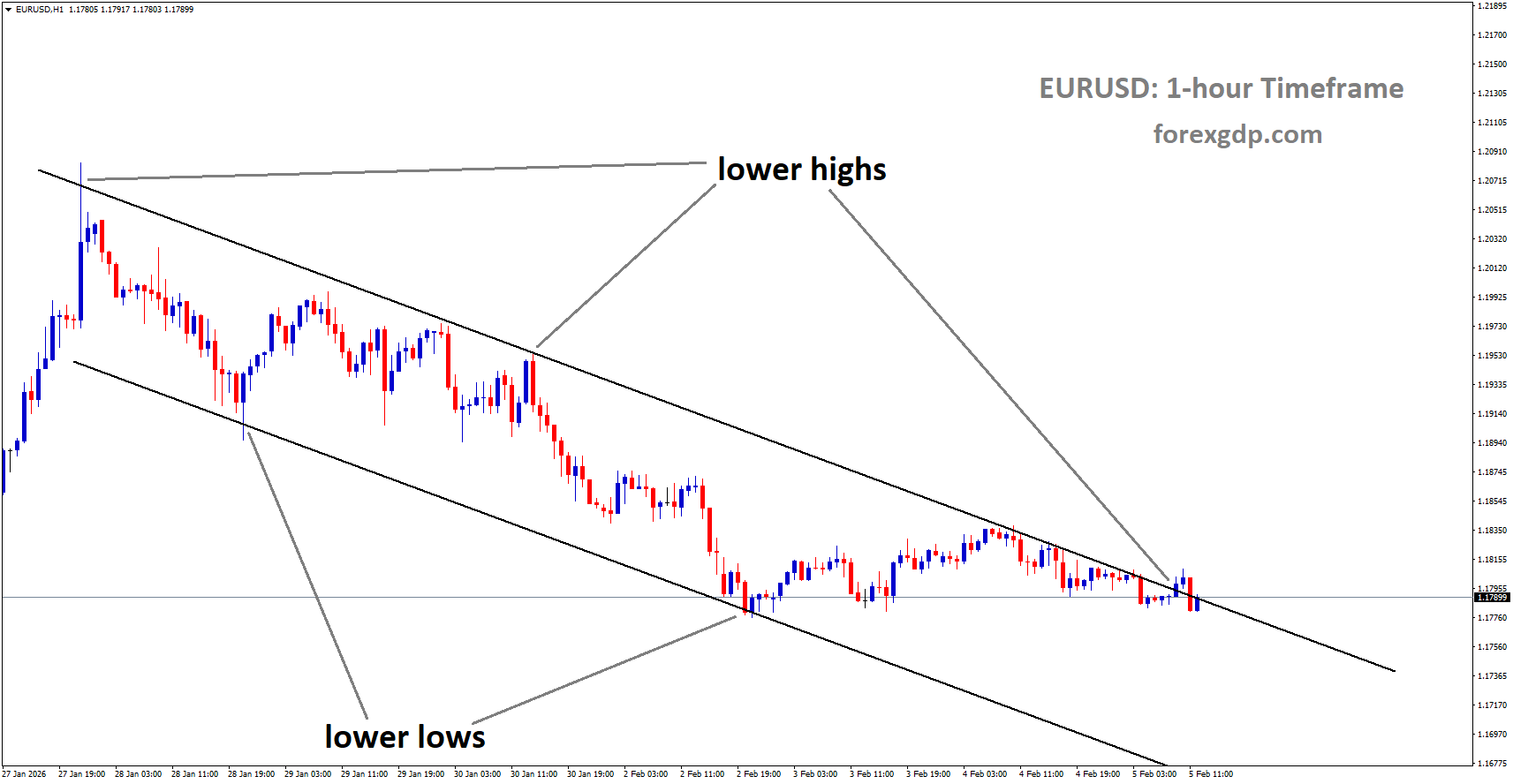

EURUSD is moving in descending channel and market has reached lower high area of the channel

EURUSD Stays Supported as ECB Maintains Cautious Policy Stance

The European Central Bank is once again in the spotlight as it wraps up its latest policy meeting. Investors, businesses, and policymakers across the region are paying close attention, not because a dramatic shift is expected, but because of what the central bank might signal about the months ahead.

For now, the general expectation is calm. The ECB is widely seen as keeping its current policy settings unchanged, continuing a careful approach that has defined its recent decisions. At the same time, President Christine Lagarde’s comments during the press conference are likely to shape expectations, even if no immediate action follows.

Why the ECB Is Expected to Stay on Hold

The ECB has spent the past year navigating a delicate balance. After acting early to respond to post-pandemic inflation pressures, policymakers now believe their current stance is appropriate for today’s economic conditions. This sense of confidence has been summed up repeatedly by President Lagarde, who has described monetary policy as being in a “good place.”

Holding steady allows the central bank to observe how earlier decisions continue to work through the economy. Monetary policy often affects growth and inflation with a delay, and officials want clearer evidence before making any further moves.

At the last meeting of the Governing Council, policymakers offered no strong hints about upcoming changes. Instead, they reinforced a cautious mindset, choosing patience over prediction. This approach reflects the view that while the overall outlook looks manageable, uncertainty has not disappeared.

A Meeting-by-Meeting Strategy Takes Center Stage

One of the clearest messages expected from the ECB is its commitment to a meeting-by-meeting approach. Rather than setting out a fixed path for policy, the central bank prefers to evaluate fresh data as it becomes available.

President Lagarde has been consistent on this point. She has stressed that confidence in current policy does not mean future decisions are locked in. Economic conditions can change quickly, and flexibility remains essential.

This strategy helps the ECB avoid overreacting to short-term shifts while still remaining responsive to meaningful trends. It also signals to markets that decisions will be based on evidence, not assumptions.

Economic Data Supports a Patient Approach

Recent economic data from the euro area has helped reinforce the ECB’s wait-and-see stance. After a challenging period marked by slow growth and uncertainty, the region’s economy has shown signs of renewed strength.

According to official figures, the European Union recorded modest growth toward the end of last year. While the pace was not spectacular, it marked a positive step and suggested that the economy is finding its footing. On an annual basis, overall output also expanded, pointing to gradual improvement rather than stagnation.

This resilience matters for policymakers. A stable or improving economy reduces the need for urgent intervention and gives the ECB more room to observe how conditions evolve naturally.

Inflation Trends Remain Encouraging

Inflation has been another key factor shaping the ECB’s outlook. After peaking in the wake of global disruptions, price pressures have eased over time, moving closer to levels that align with the central bank’s goals.

Recent data showed that inflation slowed again at the start of the year, in line with expectations. Measures that exclude more volatile components, such as food and energy, also remained steady. This consistency suggests that underlying price pressures are not accelerating.

For the ECB, this is an important signal. Stable inflation supports the idea that current policy settings are doing their job, reducing the need for immediate changes.

Market Reaction Reflects Cautious Optimism

In the currency market, the euro has been trading steadily, reflecting the broader sense of balance around the ECB’s decision. After pulling back from earlier highs, the common currency has found a more stable footing.

This stability suggests that investors are comfortable with the idea of policy continuity. Rather than reacting to speculation, markets appear to be waiting for clear signals from policymakers before making larger moves.

While short-term fluctuations are always possible, the lack of strong volatility highlights how well-telegraphed the ECB’s stance has become.

What Investors Are Listening for Next

Even if the policy decision itself turns out to be uneventful, President Lagarde’s press conference will still matter. Investors will be listening closely for subtle changes in tone or emphasis.

Key questions include how policymakers view recent economic improvements, how confident they are about inflation trends, and what risks they see on the horizon. Any shift in language could influence expectations about future meetings, even if no immediate action is taken.

That said, most observers expect the overall message to remain consistent. The ECB is likely to emphasize patience, flexibility, and close attention to incoming data.

Final Summary

The European Central Bank appears set to maintain its current course, reflecting confidence that its policies are well positioned for today’s economic environment. With growth showing signs of improvement and inflation easing in line with expectations, policymakers see little reason to rush into new actions.

President Christine Lagarde is expected to reinforce the ECB’s commitment to a meeting-by-meeting approach, making it clear that future decisions will depend on how the data unfolds. For now, stability is the theme, both in policy and in market response.

As the year progresses, attention will remain focused on economic indicators and official commentary. While change is always possible, the ECB’s steady hand suggests that patience, rather than urgency, will continue to guide its decisions.

GBPUSD in focus after BoE stands pat and governor signals next steps

The Bank of England’s latest policy meeting offered markets and households a clearer look at how policymakers are thinking about the road ahead. While the central bank chose to keep interest rates unchanged, the close vote and the tone of the discussion revealed an institution that is slowly preparing for further easing, even as it remains cautious about lingering inflation risks.

GBPUSD reached the retest area of the broken descending channel

Governor Andrew Bailey’s comments after the meeting helped frame the decision. He acknowledged progress on inflation while stressing that the evidence is not yet strong enough to justify immediate action. The message was measured and careful, reflecting a balancing act between supporting a fragile economy and ensuring that inflation is firmly under control.

A Split Decision at the February Meeting

At its February meeting, the Bank of England held its policy rate steady at 3.75%, a move that had been widely expected. What caught attention, however, was how divided the Monetary Policy Committee had become. The vote was narrowly split, with five members favoring no change and four pushing for a modest reduction.

This close call highlights how finely balanced the debate has become. Some policymakers believe inflation risks are easing fast enough to allow for earlier action. Others argue that patience is still required, warning that cutting too soon could undo the progress already made.

Governor Bailey himself struck a middle ground. He indicated growing confidence that rates will move lower over time, but emphasized that more confirmation is needed before taking that step. This cautious stance reflects the broader mood within the committee: open to easing, but only when the data clearly supports it.

How Policymakers See Inflation and Growth

The Bank’s updated forecasts played a key role in shaping the discussion. Policymakers now expect inflation to return to the central bank’s target earlier than previously thought. Projections suggest inflation will dip below the target in the near term before settling back at the desired level over the medium term.

This shift is important. It signals that the worst of the inflation surge may be behind the UK economy. At the same time, the Bank is mindful that inflation can be stubborn, especially if demand or wage pressures re-emerge.

On the growth side, the outlook remains modest. Economic momentum has faded, with recent data pointing to only limited expansion. While growth is expected to pick up gradually, the pace is likely to remain below historical norms. This weak backdrop strengthens the case for lower rates eventually, but not necessarily right away.

Internal Debate Reflects Rising Uncertainty

The diversity of views within the Monetary Policy Committee underscores how uncertain the current environment remains. Some members believe a longer period of tight policy is still needed to guard against inflation sticking around. They point to risks such as supply disruptions or a slower-than-expected cooling in the labor market.

Others are more focused on the downside risks to the economy. Weaker demand, cautious consumer spending, and soft business investment all argue for providing some relief through lower borrowing costs. These members see the current policy stance as restrictive enough to justify a gradual shift toward easing.

What unites both sides is an acceptance that future decisions will be harder than before. As interest rates move closer to a neutral level, the margin for error shrinks. Each adjustment must be carefully weighed against new data, making policy more reactive and less predictable than in earlier stages of the cycle.

Guidance Points to Gradual Easing, Not a Rush

One of the clearest takeaways from the Bank’s communication is that any future rate cuts are likely to be slow and deliberate. Policymakers continue to describe a gradual downward path, rather than a rapid series of reductions.

This approach reflects lessons learned from past cycles. Moving too quickly could reignite inflation, while waiting too long could deepen economic weakness. The Bank appears determined to avoid both outcomes by staying flexible and data-dependent.

Importantly, officials stressed that each decision will be judged on its own merits. There is no preset schedule for cuts, and no guarantee that easing will happen at every meeting. This conditional guidance is meant to keep expectations anchored while preserving the Bank’s ability to respond to changing conditions.

Business Surveys Show Cooling Pressures

Recent surveys of UK businesses provide some reassurance that inflationary pressures are easing. Companies are becoming slightly less aggressive in their expectations for wage growth, suggesting that the labor market may be cooling at last.

Firms are also revising down their plans for price increases over the coming year. While these expectations remain elevated, the direction of travel is encouraging. Lower anticipated price growth reduces the risk of inflation becoming entrenched.

Hiring intentions have softened as well. Businesses appear more cautious about expanding their workforce, reflecting uncertainty about demand and the broader economic outlook. This moderation in employment plans supports the view that the economy is slowing rather than overheating.

Market Sentiment and Policy Expectations

Financial markets have taken note of the Bank’s cautious but increasingly open stance on easing. Investors largely expected no change at this meeting and were more focused on the tone of the guidance and the updated forecasts.

The overall reaction suggests that markets see lower rates ahead, even if the timing remains uncertain. The Bank’s acknowledgment that rates are likely to fall further has reinforced this view, while the emphasis on patience has tempered expectations for immediate action.

For households and businesses, this environment means continued uncertainty. Borrowing costs may eventually decline, but relief is unlikely to come quickly. Planning decisions will still need to account for a period of relatively tight financial conditions.

Balancing Risks in a Fragile Economy

The Bank of England’s current challenge is a familiar one: balancing the risk of doing too much against the risk of doing too little. Inflation is easing, but not fully defeated. Growth is weak, but not collapsing. In this narrow corridor, policy choices become more complex.

Governor Bailey and his colleagues appear aware of this delicate balance. Their communication suggests a willingness to adjust policy as conditions evolve, without committing to a fixed path. This flexibility may be crucial in navigating the next phase of the economic cycle.

At the same time, the close votes and open debate within the committee show that consensus is harder to achieve. As new data arrives, opinions may continue to shift, leading to more finely balanced decisions in the months ahead.

Final Summary

The Bank of England’s latest meeting confirmed that interest rates are likely near their peak, but it also showed that the path lower will be careful and measured. A split vote, improving inflation forecasts, and a cautious growth outlook all point toward eventual easing, though not in haste. Policymakers are increasingly confident that rates will fall over time, yet remain focused on ensuring inflation is firmly under control. For now, the message is one of patience, flexibility, and close attention to incoming data as the UK economy navigates a slow and uncertain recovery.

USDJPY Extends Uptrend Driven by Persistent Demand for the Dollar

The USD/JPY currency pair continues to show strong upward momentum as the US Dollar remains in demand across global markets. This move reflects a mix of political developments in the United States, shifting expectations around Federal Reserve policy, and fresh economic data that could shape investor sentiment in the days ahead. At the same time, the Japanese Yen has struggled to attract buyers, weighed down by domestic political and fiscal expectations.

USDJPY is moving in an uptrend channel, andthe market has rebounded from the higher low area of the channel

What is driving this divergence between the two currencies is not a single factor, but a combination of confidence in the US economy and uncertainty surrounding Japan’s near-term outlook.

US Dollar Remains in the Spotlight

The US Dollar has been outperforming most major currencies, and this strength has carried over into the USD/JPY pair. Investors have shown a clear preference for the Greenback, viewing it as a safer and more stable option amid ongoing global policy uncertainty.

One of the main reasons behind this renewed interest is the belief that US monetary policy will remain restrictive for longer than previously thought. While markets once expected early interest rate cuts, that optimism has faded as inflation in the United States continues to cool only gradually. With price pressures still above the central bank’s comfort zone, expectations for quick policy easing have been pushed back.

This shift in outlook has helped the US Dollar extend its recent gains and maintain a firm tone across trading sessions.

Federal Reserve Policy Expectations Support the Dollar

A major driver behind the Dollar’s strength is the growing consensus that the Federal Reserve is unlikely to cut interest rates in its upcoming policy meetings. Investors broadly expect rates to remain unchanged through at least the early part of the year.

Inflation has proven more persistent than many policymakers anticipated, and this has made the central bank cautious. Rather than rushing to stimulate the economy, officials appear focused on ensuring inflation stays on a clear path toward the long-term target.

This cautious stance has reduced expectations for near-term easing and helped keep the Dollar attractive. When interest rates stay higher for longer, global investors often favor that currency due to better returns on cash and fixed-income assets.

Political Developments Add to Dollar Confidence

Another factor lifting the US Dollar is recent political news. Confidence improved after the nomination of Kevin Warsh as the next Chair of the Federal Reserve. Market participants generally view him as someone who supports policy discipline and central bank credibility.

This nomination has been interpreted as a signal that the Federal Reserve is unlikely to shift toward aggressive easing anytime soon. For investors, that means fewer surprises and a more predictable policy path, both of which tend to support the national currency.

Political clarity, especially around key economic institutions, often plays a quiet but important role in shaping currency trends.

Labor Market Data in Focus

Attention is also turning toward upcoming US labor market data, which could further influence expectations around monetary policy. Investors are closely watching the Job Openings and Labor Turnover Survey for December.

Economists expect employers to report a modest increase in job openings compared to the previous month. If confirmed, this would reinforce the view that the US labor market remains resilient despite tighter financial conditions.

A strong labor market gives the Federal Reserve more room to keep interest rates steady, as it suggests the economy can handle borrowing costs at current levels. For the US Dollar, that resilience is another supportive factor.

Why Job Openings Matter

Job openings data offers insight into labor demand and business confidence. When companies continue to post new positions, it signals optimism about future growth. On the other hand, a sharp decline would raise concerns about slowing economic momentum.

For currency markets, this data helps shape expectations around interest rates, which remain one of the most powerful drivers of exchange rates.

Japanese Yen Faces Domestic Headwinds

While the US Dollar benefits from policy confidence and economic resilience, the Japanese Yen is struggling under a different set of pressures. Investors are increasingly cautious about Japan’s fiscal outlook, particularly in light of political developments at home.

Expectations are growing that Japan’s Prime Minister, Sanae Takaichi, will introduce a large government spending package following the upcoming lower house elections. While fiscal stimulus can support economic growth, it often raises concerns about government debt and long-term financial stability.

These concerns have weighed on the Yen, making it less appealing compared to currencies backed by tighter fiscal and monetary frameworks.

Diverging Policy Paths Shape USD/JPY Direction

The contrast between the United States and Japan could not be clearer. In the US, policymakers are focused on controlling inflation and maintaining policy discipline. In Japan, expectations point toward increased government spending and continued accommodative conditions.

This divergence has created a favorable environment for the USD/JPY pair to move higher. When one country is seen as maintaining higher interest rates and stronger economic fundamentals, while the other leans toward stimulus and looser conditions, currency flows tend to follow that gap.

As long as these differences remain in place, the balance of risks appears tilted toward continued strength in the US Dollar relative to the Japanese Yen.

What Investors Are Watching Next

Looking ahead, market participants will continue to monitor several key factors. Economic data from the United States, especially related to employment and inflation, will remain crucial in shaping expectations for Federal Reserve policy.

At the same time, political developments in Japan and details around any new fiscal measures will influence sentiment toward the Yen. Clear communication from policymakers in both countries will play an important role in guiding market expectations.

Short-term moves may be driven by data releases, but the broader trend will likely depend on how long current policy differences persist.

Final Summary

The USD/JPY pair has extended its advance as the US Dollar continues to outperform on the back of firm monetary policy expectations, political clarity, and a resilient labor market. Investors are increasingly confident that the Federal Reserve will keep interest rates unchanged in the near term, reducing hopes for early easing and supporting the Greenback.

Meanwhile, the Japanese Yen has weakened amid expectations of increased government spending and ongoing domestic uncertainty. The growing gap between US and Japanese policy directions has become a key theme shaping currency movements.

As economic data and political signals continue to unfold, this contrast is likely to remain a central driver of USD/JPY dynamics in the near future.

USDCAD Climbs as Global Caution Fuels Demand for the US Dollar

The US Dollar has been gaining ground against the Canadian Dollar, holding steady after a short but strong move higher. While the pair paused before pushing further, the overall tone remains supportive for the greenback. A cautious global mood, sparked by worries around the technology sector and broader economic signals, has kept investors leaning toward safety. At the same time, softer energy markets have reduced support for the Canadian Dollar, adding to the imbalance between the two currencies.

USDCAD is moving in an uptrend channel, and the market has fallen from the higher high area of the channel

This mix of global risk concerns, shifting market sentiment, and uneven economic data has created a calm but tense environment for USD/CAD. Traders are watching developments closely, especially as fresh data from the United States could shape expectations for the weeks ahead.

Global Risk Aversion Supports the US Dollar

One of the biggest forces behind the recent strength in the US Dollar is a clear move toward risk aversion. Investors across the world have grown uneasy after a series of disappointing earnings reports from major technology companies in the United States. These firms have been central to recent market optimism, particularly around artificial intelligence and future growth potential.

When expectations are high, even small disappointments can have an outsized impact. Recent results failed to meet the market’s lofty hopes, leading to sharp declines in tech shares. This weakness quickly spread beyond the sector, dragging down broader equity markets in multiple regions.

European stocks have reflected this cautious mood, posting modest losses as traders reassess their exposure to risk. Futures tied to US equities have shown mixed signals, suggesting uncertainty about how the trading day will unfold. In this kind of environment, investors often look for assets that are seen as more stable, and the US Dollar typically benefits from that shift.

The greenback’s role as a global safe haven remains strong during periods of stress. When confidence fades, demand for the US Dollar tends to rise, even if the concerns originate within the US economy itself. That dynamic has been clearly visible during the latest market pullback.

Tech Sector Fears and AI Bubble Concerns

Beyond individual earnings reports, there is a broader worry growing around the technology sector as a whole. Over the past year, enthusiasm for artificial intelligence has driven massive investment flows into tech-related companies. While innovation continues at a rapid pace, some investors are now questioning whether expectations have run too far ahead of reality.

Concerns about a potential AI bubble have started to surface more frequently in market discussions. These fears do not mean that the technology lacks value, but they suggest that prices and growth projections may have become stretched. When such doubts gain traction, markets can react quickly and sharply.

As technology stocks falter, overall risk appetite tends to shrink. This shift does not stay confined to equities. Currencies linked to global growth and commodities often feel the pressure, while defensive currencies like the US Dollar gain support. The recent behavior of USD/CAD fits neatly into this pattern.

Mixed US Economic Data Keeps Traders Alert

Economic data from the United States has added another layer of complexity to the outlook. Recent reports painted a mixed picture of the economy, offering both encouraging signs and fresh reasons for concern.

On the positive side, business activity in the services sector showed solid momentum. This suggests that large parts of the economy continue to expand at a healthy pace, supporting the idea that overall growth remains resilient.

However, not all the details were reassuring. Employment-related components within these reports pointed to softer conditions. Measures linked to hiring and job creation showed signs of slowing, and a separate private employment report reinforced those concerns. Together, these indicators have revived questions about the strength of the US labor market.

Employment plays a crucial role in shaping economic confidence and consumer spending. Any sustained weakness could eventually feed into slower growth. Because of this, traders are paying close attention to upcoming labor market data, which could confirm or challenge the recent signals.

Upcoming US Labor Data in Focus

Later releases tied to jobless claims and job openings are expected to attract significant attention. These figures can offer timely insight into whether companies are pulling back on hiring or maintaining demand for workers.

If the data suggests growing strain in the labor market, it could weigh on risk sentiment further. Paradoxically, that may still support the US Dollar in the short term, as investors continue to prioritize safety over growth-focused assets.

Canadian Dollar Pressured by Weaker Oil Markets

While the US Dollar has found support from global uncertainty, the Canadian Dollar has faced its own challenges. Canada’s economic calendar has been relatively quiet, leaving external factors to play a larger role in driving the currency.

One of the most important of these factors is the price of oil. As a major energy exporter, Canada’s currency often moves in line with trends in the oil market. When oil prices fall or struggle to recover, the Canadian Dollar tends to lose momentum.

Recently, oil markets have been weighed down by easing supply concerns. Reduced geopolitical tension and improved supply outlooks have taken some pressure off the market, limiting the upside for crude prices. Even though oil has shown signs of stabilizing after a dip, it remains weaker than recent peaks.

This softness has acted as a headwind for the Canadian Dollar, making it harder for the currency to mount a sustained recovery against its US counterpart.

Limited Domestic Drivers in Canada

With few major economic releases from Canada this week, traders have had little fresh information to reassess the country’s outlook. In the absence of strong domestic signals, the Canadian Dollar has been more sensitive to shifts in global sentiment and commodity markets.

As long as oil prices remain under pressure and risk appetite stays fragile, the Loonie may continue to struggle to attract strong buying interest.

Broader Market Mood Shapes USD/CAD Direction

The current behavior of USD/CAD reflects a broader story unfolding across global markets. Confidence has been shaken by tech sector disappointments, while mixed economic data has made the outlook less clear. In response, investors are choosing caution over risk.

This environment favors currencies seen as stable and liquid, especially during times of uncertainty. The US Dollar fits that role well, benefiting from its status and from ongoing demand as a reserve currency.

Meanwhile, currencies tied to growth and commodities face a tougher path. Without a clear improvement in sentiment or a rebound in key supporting factors like oil, the Canadian Dollar remains on the defensive.

Final Summary

USD/CAD remains supported as global markets navigate a period of uncertainty. Risk aversion, driven by concerns over the technology sector and fears of overstretched expectations around artificial intelligence, has boosted demand for the US Dollar. Mixed signals from US economic data have kept traders cautious, with labor market indicators drawing particular attention.

At the same time, the Canadian Dollar has struggled due to softer oil markets and a lack of strong domestic catalysts. With global sentiment still fragile, the balance of forces continues to favor the US Dollar, keeping USD/CAD steady as investors wait for clearer signals on growth, employment, and market stability.

XAGUSD Shows Signs of Stability After Sharp Market Pullback

Silver has staged a partial recovery after a dramatic sell-off that rattled precious metal markets. The rebound comes as investors digest strong signals from the US Federal Reserve and shifting geopolitical developments that have reduced the immediate need for safe-haven assets. While silver has clawed back some ground, the broader mood around the metal remains cautious, shaped by interest rate expectations, currency strength, and uncertainty on the global stage.

XAGUSD is moving in an uptrend channel, andthe market has reached a higher low area of the channel

This period has highlighted how sensitive silver can be to central bank messaging and international diplomacy. Unlike gold, silver often sits at the crossroads of investment demand and broader economic sentiment, making it especially reactive when markets reassess risk.

Federal Reserve Signals Weigh on Precious Metals

The biggest pressure on silver has come from the Federal Reserve’s clear message that it is not ready to ease policy further without convincing proof that inflation is cooling. One of the most influential voices behind this stance has been Fed Governor Lisa Cook, who has openly stated she would not support additional rate cuts unless inflation shows more consistent signs of easing.

Her comments reflect a growing concern inside the central bank that progress on lowering inflation may be stalling. Rather than focusing on potential weakness in the labor market, Fed officials are prioritizing price stability. This approach has reshaped expectations across financial markets, pushing investors to rethink how soon borrowing costs might come down.

For silver, this matters a great deal. Higher interest rates tend to reduce the appeal of non-yielding assets like precious metals. When investors can earn returns elsewhere, holding silver becomes less attractive, especially during periods of uncertainty about future policy direction.

Leadership Expectations Add to Market Uncertainty

Adding another layer of complexity, investors are also watching developments around potential changes in Federal Reserve leadership. The nomination of Kevin Warsh as a possible Fed chair has drawn attention due to his known preference for a smaller central bank balance sheet and a more restrained approach to rate cuts.

Even the possibility of such a shift has influenced sentiment. Markets are forward-looking by nature, and any sign that future policy could remain tight for longer tends to support higher yields and a stronger currency. Both of these outcomes usually create headwinds for silver and other precious metals.

While no immediate policy changes have occurred, the discussion alone has been enough to keep investors cautious. Silver’s earlier plunge reflected how quickly markets can react when expectations around interest rates harden.

Easing Geopolitical Tensions Reduce Safe-Haven Demand

Beyond central bank policy, geopolitics has also played a key role in silver’s recent moves. Safe-haven demand for precious metals tends to rise during periods of global tension, but that support weakened after Iran confirmed it would hold talks with the United States in Oman.

The confirmation of diplomatic engagement signaled a possible reduction in near-term geopolitical risk. As a result, investors scaled back their defensive positions, leading to reduced demand for assets traditionally seen as protection during uncertain times, including silver.

There was a brief moment when reports suggested the talks could collapse, which helped silver regain some momentum. However, officials from both sides later clarified that discussions would go ahead as planned, even if the agenda remains unclear. This back-and-forth reinforced the idea that while uncertainty still exists, the immediate threat level has eased.

Unclear Agenda Keeps Investors on Edge

Although talks between Iran and the United States are set to proceed, uncertainty surrounds what will actually be discussed. Iranian officials have indicated they want negotiations to focus strictly on the nuclear program. In contrast, Washington has shown interest in expanding the scope to include missile development, regional activities, and human rights issues.

This mismatch in priorities leaves plenty of room for disagreement. For silver investors, that uncertainty cuts both ways. On one hand, unresolved issues could reignite safe-haven demand if talks break down. On the other, the mere continuation of dialogue reduces the sense of urgency that typically drives strong inflows into precious metals.

For now, markets appear to be leaning toward cautious optimism, which has limited silver’s ability to stage a stronger recovery.

A Stronger US Dollar Adds Pressure

Another major factor influencing silver has been the strength of the US dollar. Hawkish signals from the Federal Reserve have supported the greenback, making it more expensive for buyers using other currencies to purchase dollar-denominated commodities.

When the dollar rises, demand for silver often softens outside the United States. This currency effect can be powerful, especially during periods when interest rate expectations shift quickly. Investors are also mindful that higher yields increase the opportunity cost of holding assets that do not generate income, further dampening enthusiasm for silver.

The combination of a firm dollar and reduced expectations for near-term rate cuts has been a tough environment for precious metals to navigate.

Why Silver Reacts So Sharply

Silver’s recent volatility underscores its unique position in the market. It is often grouped with gold as a safe-haven asset, yet it also has strong ties to industrial demand. This dual role can amplify price swings when economic and political signals change.

When fears of inflation or conflict rise, silver can benefit alongside gold. When those fears ease and monetary policy remains tight, silver can fall faster as investors rotate into yield-bearing assets. This dynamic helps explain why silver experienced such a steep drop before finding some support.

What Investors Are Watching Next

Looking ahead, silver’s direction will likely depend on a few key developments. Clear evidence that inflation is easing could soften the Federal Reserve’s stance, improving the outlook for precious metals. On the geopolitical front, any setback in diplomatic talks could quickly revive safe-haven demand.

At the same time, sustained strength in the US dollar and persistently high yields would continue to challenge silver’s recovery. Investors are balancing these forces carefully, knowing that sentiment can shift quickly with new data or headlines.

Final Summary

Silver’s recent rebound follows a sharp sell-off driven by firm Federal Reserve messaging and a reduction in geopolitical risk. Hawkish comments from US policymakers, combined with expectations of tighter policy for longer, have weighed heavily on precious metals. Meanwhile, confirmation of diplomatic talks between Iran and the United States has reduced immediate safe-haven demand.

Despite a modest recovery, silver remains sensitive to changes in inflation expectations, currency movements, and global politics. As markets look for clearer signals from central banks and world leaders, silver is likely to stay volatile, reflecting the constant push and pull between risk appetite and caution.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!