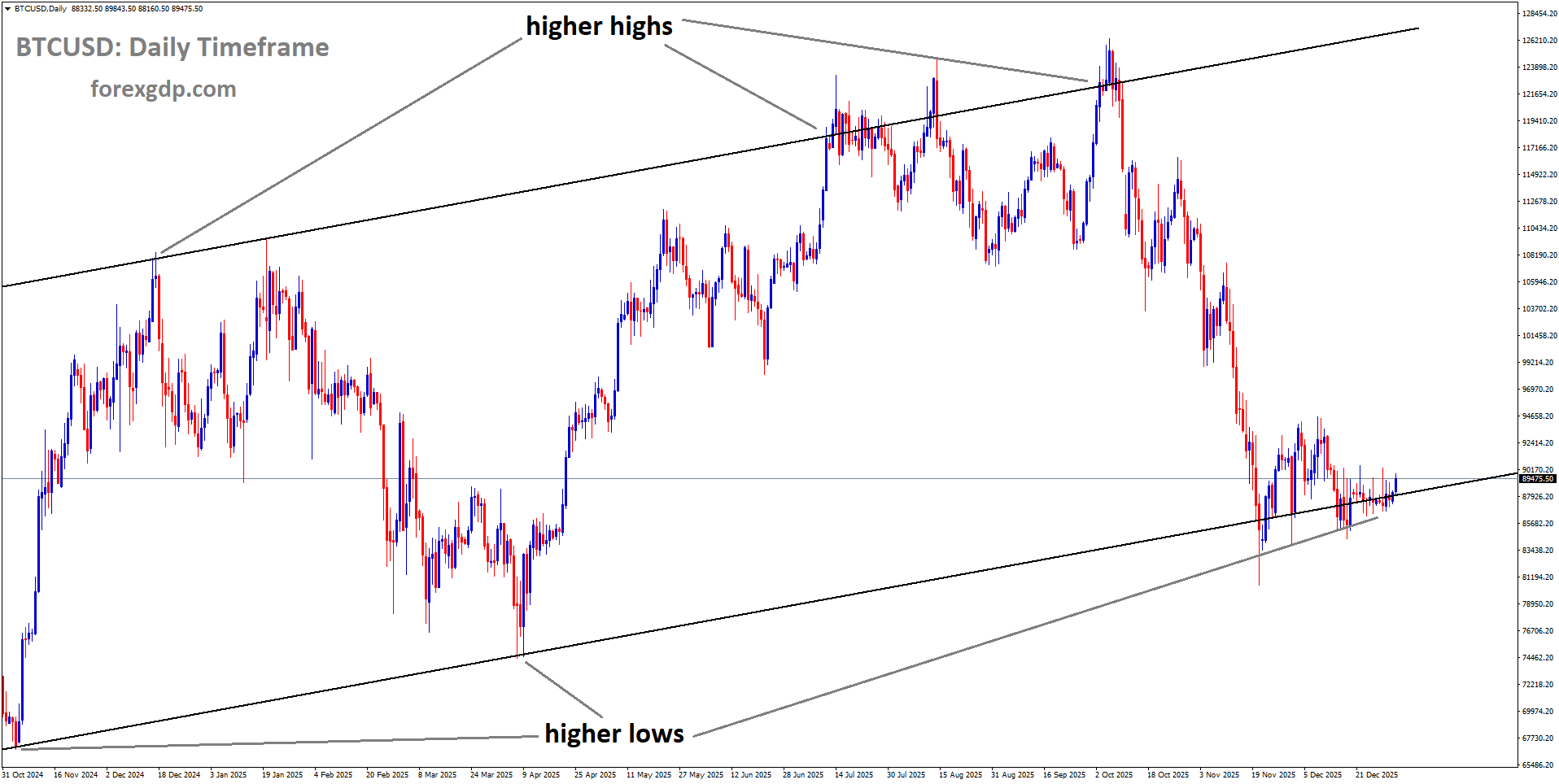

BTCUSD is moving in an Ascending channel, andthe market has reached the higher low area of the channel

BTCUSD Pauses Near the Middle as ETF Activity Loses Momentum

Bitcoin has entered a quiet phase, moving sideways for several weeks as traders and long-term investors pause to reassess the broader environment. Instead of strong rallies or sharp pullbacks, the market has settled into a holding pattern. This kind of behavior often reflects uncertainty rather than weakness or strength on its own.

Many participants appear to be waiting for clearer signals before making big decisions. These signals could come from changes in institutional behavior, shifts in liquidity conditions, or broader economic developments. For now, Bitcoin remains steady, suggesting that buyers and sellers are closely matched.

While some may find this lack of movement frustrating, periods like this are not unusual. Sideways markets often act as transitions, allowing sentiment to reset before the next meaningful move. Understanding what is happening behind the scenes can help explain why Bitcoin is currently stuck in neutral.

Institutional Interest Shows Signs of Cooling

One of the clearest trends shaping the current Bitcoin landscape is the softening of institutional demand. Large investors, especially those using regulated investment products, have been reducing their exposure slightly over recent weeks.

Spot Bitcoin exchange-traded funds have recorded net outflows for the third week in a row. By the end of the most recent reporting period, total withdrawals reached just over twelve million dollars. While this figure is not massive, the consistency of outflows over several weeks suggests a cautious approach among institutions.

These investment products are often seen as a window into how professional money managers view Bitcoin. When inflows are strong, it typically signals confidence in future performance. When outflows persist, it points to hesitation or a shift toward safer assets.

This does not mean institutions are abandoning Bitcoin altogether. Instead, it suggests they are taking a wait-and-see approach. Concerns about economic uncertainty, interest rate expectations, and global liquidity may be encouraging them to reduce risk, at least temporarily.

If institutional withdrawals were to accelerate, Bitcoin could face increased pressure. However, the current pace remains mild, indicating more of a pause than a full retreat.

Liquidity Support Brings a Calmer Market Mood

While institutional demand for Bitcoin has softened, broader financial conditions have shown signs of improvement. Toward the end of the year, the U.S. financial system experienced a surge in borrowing and cash management activity, which helped ease short-term funding stress.

The Federal Reserve Bank of New York reported record usage of its Standing Repo Facility. Financial institutions borrowed more than seventy-four billion dollars through this program on the final trading day of the year. This surpassed the previous record and highlighted the demand for reliable, short-term funding during a traditionally tight period.

At the same time, money market funds and other eligible firms placed more than one hundred billion dollars into the Federal Reserve’s reverse repo facility. This marked the highest level since early August.

These two facilities work together in important ways. At year-end, many lenders become more cautious and prefer to hold cash in safe places rather than extend loans. When this happens, available funding in the private market shrinks. The Federal Reserve steps in by offering lending through its repo facilities and accepting excess cash through reverse repos.

This process helps stabilize the financial system. By ensuring that institutions can access liquidity when needed, the central bank reduces stress and prevents sudden disruptions. As a result, overall market sentiment tends to improve, even if only slightly.

How Federal Reserve Actions Influence Bitcoin

In addition to these year-end measures, the Federal Reserve has taken steps to inject more liquidity into the financial system. Beginning in mid-December, the central bank started purchasing a significant amount of Treasury bills each month. The goal of this program is to ease short-term funding conditions and keep borrowing costs in check.

When liquidity increases and borrowing becomes cheaper, investors are often more willing to take on risk. This environment can benefit assets that are considered higher risk, including stocks and cryptocurrencies like Bitcoin.

Although Bitcoin has not reacted strongly yet, these supportive conditions may be helping to prevent a sharper decline. Instead of selling aggressively, many market participants appear comfortable holding their positions while monitoring developments.

It is important to note that liquidity support does not guarantee rising prices. However, it can create a more stable backdrop, reducing the likelihood of sudden shocks. For Bitcoin, this stability has translated into a narrow trading range rather than dramatic swings.

A Market Caught Between Caution and Optimism

Bitcoin’s current behavior reflects a balance between caution and optimism. On one side, institutional investors are pulling back slightly, signaling uncertainty about the near-term outlook. On the other side, central bank actions are easing financial stress and supporting a modest risk-friendly environment.

This push and pull has kept Bitcoin moving sideways. Buyers are not confident enough to drive a strong rally, while sellers lack the conviction to force a major decline. As a result, the market remains stuck in a holding pattern.

Retail investors are also likely influenced by this mixed backdrop. Without clear momentum, many prefer to stay on the sidelines or maintain existing positions rather than make bold moves. News headlines and macroeconomic updates are being watched closely for clues about what might come next.

Periods of indecision can last longer than expected. However, they often end when a new narrative takes hold, whether driven by economic data, policy changes, or shifts in investor sentiment.

What to Watch Going Forward

Looking ahead, several factors could influence Bitcoin’s next move. Institutional fund flows will remain a key signal. A return to consistent inflows would suggest renewed confidence, while larger outflows could indicate growing concern.

Liquidity conditions will also matter. Continued support from the Federal Reserve may help maintain a stable environment, but any changes in policy tone could quickly alter market sentiment.

BTCUSD is moving in a box pattern, and the market has reached the resistance area of the pattern

Global economic developments, including inflation trends and growth expectations, will play a role as well. Bitcoin often reacts to changes in how investors perceive risk across the financial system.

For now, patience appears to be the dominant strategy. The market is taking time to absorb recent developments and reassess expectations for the months ahead.

Summary

Bitcoin is currently moving sideways as the market searches for direction. Institutional demand has softened, with spot Bitcoin ETFs seeing modest but consistent outflows over recent weeks. At the same time, strong liquidity support from the Federal Reserve has helped ease financial stress and maintain a mildly positive risk environment.

These opposing forces have left Bitcoin trading in a narrow range, reflecting widespread indecision rather than strong conviction. While short-term momentum remains limited, supportive liquidity conditions may be helping to stabilize the market. As investors watch institutional behavior and broader economic signals, Bitcoin remains in a waiting phase, poised for its next meaningful move once clarity returns.

EURUSD slides to a new weekly bottom as Eurozone reports disappoint

The euro has come under renewed pressure against the US dollar as the new year begins, with recent economic data highlighting growing challenges across Europe’s manufacturing sector. A series of weaker-than-expected reports has weighed on confidence, pushing the shared currency lower during a quiet holiday trading period. While market activity has been relatively calm, the underlying economic signals have been clear enough to shape sentiment.

At the same time, attention is turning toward the United States, where manufacturing activity continues to show signs of steady expansion. This contrast between slowing momentum in Europe and resilience in the US is becoming a key theme for currency markets as investors reassess the outlook for both economies.

Manufacturing Data Drives the Euro Lower

Manufacturing activity across the Eurozone has shown deeper signs of contraction than previously thought. Updated surveys released at the end of December revealed that factory output and new orders are declining at a faster pace in several major economies. These revisions caught many investors off guard and reinforced concerns about the region’s growth prospects.

The Eurozone-wide manufacturing index was revised downward, confirming that the sector remains under pressure and is contributing less to overall economic growth. This matters because manufacturing has historically been an important pillar of the region’s economy, supporting employment, exports, and business investment.

Germany, often seen as the industrial engine of Europe, delivered one of the most disappointing updates. The revised data showed that factory activity weakened more sharply than initial estimates suggested. Given Germany’s central role in European supply chains, this decline has had a ripple effect on sentiment toward the broader Eurozone.

Other large economies added to the negative tone. Italy and Spain both reported a noticeable slowdown in manufacturing conditions compared to the previous month. These declines suggest that the weakness is not isolated but spread across multiple parts of the region. France stood out as a rare bright spot, with manufacturing activity showing a slight improvement, but this was not enough to offset broader concerns.

A Broader View of the Euro’s Performance

Despite the recent losses, the euro is not far removed from its strongest levels of the past few months. Earlier gains were supported by a period of sustained weakness in the US dollar, driven by a mix of political uncertainty, economic slowdown fears, and shifting expectations around monetary policy in the United States.

Over the past year, the dollar has struggled as investors reacted to unpredictable trade policies, signs of cooling growth, and questions about the future direction of interest rates. These factors allowed the euro to recover significantly from earlier lows, even as Europe faced its own economic challenges.

However, the latest manufacturing data has reminded markets that the Eurozone’s recovery remains uneven. While some sectors, particularly services, have shown resilience, manufacturing continues to lag behind. This imbalance raises concerns about whether growth can be sustained without a stronger industrial rebound.

US Manufacturing Offers a Contrast

While Europe grapples with contracting factory activity, the United States is expected to show a more stable picture. Upcoming manufacturing survey data from the US is likely to confirm that the sector is still expanding, albeit at a moderate pace. This steady performance has helped the dollar regain some footing in recent sessions.

US manufacturing growth may not be accelerating, but it appears to be holding up better than in many other advanced economies. Businesses continue to report stable demand, and supply conditions have improved compared to previous years. This relative strength has made the dollar more attractive in comparison to currencies facing deeper economic headwinds.

Investors are closely watching these US indicators for confirmation that the economy can avoid a sharper slowdown. If the data continues to point to moderate but consistent growth, it could reinforce confidence in the dollar, especially when contrasted with Europe’s manufacturing struggles.

What Investors Are Watching Next

Beyond manufacturing data, several upcoming events are shaping market expectations. One of the most anticipated releases in the US is the monthly employment report, which provides insight into job creation, wage growth, and overall labor market health. Strong employment figures would support the view that the US economy remains resilient.

There is also growing interest in leadership changes at the US central bank. The announcement of a new Federal Reserve chair in the coming weeks is expected to influence expectations around future monetary policy. Any hints about the direction of interest rates or the bank’s stance on inflation and growth could have a significant impact on the dollar.

In Europe, attention remains focused on how policymakers will respond to the ongoing weakness in manufacturing. The European Central Bank faces a delicate balance as it considers how to support growth without reigniting inflation pressures. Continued signs of economic softness could increase expectations for a more accommodative policy stance.

The Bigger Economic Picture

The divergence between Europe and the United States highlights a broader theme in the global economy. While many regions are dealing with the aftereffects of past disruptions, the pace and strength of recovery vary widely. Structural differences, policy choices, and exposure to global trade all play a role in shaping outcomes.

EURUSD is moving in an Ascending Triangle pattern, and the market has fallen from the resistance area of the pattern

For the Eurozone, revitalizing manufacturing will be crucial for achieving more balanced growth. Investments in innovation, energy transition, and supply chain resilience could help support the sector over the longer term. In the short run, however, weak data continues to weigh on confidence.

In the US, steady manufacturing performance adds to a narrative of relative economic stability. While challenges remain, including political uncertainty and shifting global conditions, the current data suggests that the economy is navigating these issues better than many peers.

Final Summary

Recent economic data has placed renewed pressure on the euro, as manufacturing activity across much of Europe has weakened more than expected. Downward revisions in key economies, especially Germany, have highlighted ongoing challenges for the region’s industrial base. In contrast, the United States continues to show moderate but stable manufacturing growth, supporting the dollar.

As investors look ahead, attention will remain on upcoming US economic releases, labor market data, and central bank developments. In Europe, the focus will be on whether policymakers can address persistent manufacturing weakness and restore confidence. The evolving balance between these two economies will continue to shape currency market sentiment in the weeks ahead.

GBPUSD falls under 1.3450 as UK factory activity is revised lower

GBPJPY Pauses Below 211.60, With the Pound Unable to Push Higher

The British Pound has begun the new year with a calm but confident tone against the Japanese Yen. While global markets are easing back into action after the holiday season, Sterling has shown signs of quiet strength. This early movement reflects a mix of improving UK economic signals and softer demand for traditional safe-haven currencies.

Trading conditions remain lighter than usual, which is typical for the first few sessions of January. Even so, investors are paying close attention to how major currencies behave during this slow period, as early trends can offer clues about sentiment for the weeks ahead.

The Pound’s recent performance suggests cautious optimism. Buyers appear willing to step in, but they are doing so carefully, mindful of ongoing global uncertainties and limited market participation.

The Yen Faces Pressure from Changing Market Mood

The Japanese Yen, often viewed as a safe place to park money during uncertain times, has struggled to find support as the year begins. A slightly improved global mood has reduced the demand for safety, encouraging traders to look elsewhere for opportunity.

This shift in sentiment comes at a time when trading activity across Asia is subdued. With key markets closed for New Year celebrations, price movements have been thinner and less decisive. In such conditions, even modest changes in outlook can have a noticeable effect on currency performance.

The Yen’s weakness does not necessarily point to a deeper problem. Instead, it reflects a temporary change in investor focus. As long as markets remain relatively calm and risk appetite holds, the Yen may continue to lag behind peers that benefit more from growth-linked expectations.

Holiday Trading Shapes Early Market Moves

The first days of January are rarely a true reflection of full market strength. Many institutional traders are still returning to their desks, and liquidity remains lower than normal. This environment can exaggerate small moves and limit follow-through.

For the Pound and the Yen, this means early gains or losses should be viewed with caution. Without strong participation, markets may struggle to establish clear direction. Still, these early sessions help set the tone and highlight where interest may emerge once normal trading resumes.

As Asian markets reopen and global participation improves, currency movements are likely to become more balanced. Until then, modest shifts driven by sentiment and expectations will continue to shape price action.

UK Manufacturing Shows Signs of Life

One of the more encouraging developments for the Pound comes from the UK manufacturing sector. Recent survey data points to an improvement in business activity toward the end of last year. This suggests that factories experienced a pickup in orders and output after a softer period.

Manufacturing is only one part of the UK economy, but it plays an important role in shaping confidence. When factories report better conditions, it often signals healthier demand and improved supply chains. For investors, this can support the idea that the economy is finding its footing.

The final release of the latest manufacturing survey is expected to confirm earlier findings. Unless the data shows a sharp change from initial estimates, it is unlikely to spark major market reactions. However, steady improvement helps reinforce a positive backdrop for the Pound over time.

Why Manufacturing Data Matters

Manufacturing surveys offer insight into how businesses are performing on the ground. They reflect changes in orders, employment, and production levels. When these indicators move in the right direction, they suggest companies are feeling more confident about the future.

For currency markets, such data helps shape expectations around economic growth and policy decisions. While no single report can define a trend, consistent improvement builds credibility and supports longer-term confidence in a currency.

Limited Impact, But Positive Signals

Despite the encouraging tone from UK manufacturing, the immediate effect on the Pound may be modest. Markets had already priced in signs of improvement, and the holiday-thinned environment reduces the chance of strong reactions.

Still, positive data adds to a broader narrative. It suggests the UK economy ended the year on a firmer note, which could influence investor thinking as activity picks up. Over time, this kind of steady progress can attract longer-term interest, especially if other sectors show similar resilience.

GBPJPY is moving in a box pattern, and the market has fallen from the resistance area of the pattern

The key takeaway is not the short-term reaction, but the underlying message. Stability and gradual improvement tend to matter more than sudden bursts of optimism.

Looking Ahead as Markets Reopen

As global markets return to full strength, attention will shift to how currencies respond to fresh data and renewed trading volume. For the Pound, maintaining a steady tone will depend on continued signs of economic stability and balanced investor sentiment.

The Yen’s path will likely be shaped by broader risk trends. If global confidence remains intact, it may continue to face headwinds. However, any return of uncertainty could quickly restore its appeal as a safe haven.

In the coming weeks, traders will watch how early January themes evolve. Stronger participation and clearer signals will help confirm whether current trends have staying power or simply reflect holiday conditions.

Summary

The British Pound has opened the year with a mild upward bias against the Japanese Yen, supported by improving UK manufacturing activity and a calmer global mood. The Yen has softened as investors show less urgency for safety, while thin holiday trading has kept movements restrained. Although immediate reactions remain limited, the underlying signals point to cautious optimism for Sterling as markets gradually return to full operation.

USDCHF struggles to break higher, stuck below 0.7940 in thin holiday trade

The relationship between the US Dollar and the Swiss Franc has been drawing attention as the new year begins. After a prolonged period of weakness, the US Dollar has shown signs of stabilization against the Swiss Franc, but its recovery has struggled to gain real momentum. Investors are watching closely, weighing political uncertainty in the United States against improving economic signals coming from Switzerland.

This pause in direction reflects a broader sense of caution across global markets. Currency traders, long-term investors, and businesses with international exposure are all trying to understand whether the US Dollar can regain strength or whether deeper structural challenges will continue to limit its appeal. At the same time, Switzerland’s economic outlook appears to be improving, giving the Swiss Franc steady underlying support.

USDCHF is moving in a descending channel, andthe market has rebounded from the lower low area of the channel

Political Pressure and Policy Uncertainty in the United States

One of the biggest forces shaping sentiment around the US Dollar is politics. Ongoing concerns about US trade policies, particularly those linked to former President Donald Trump’s public stance, have created unease among global investors. These concerns go beyond tariffs or trade agreements and touch on broader questions about economic stability, inflation control, and institutional independence.

The US economy has been facing a challenging mix of slower growth expectations and persistent inflation pressures. While inflation has eased from its peak, it remains high enough to limit consumer confidence and complicate policy decisions. This environment has made the US Dollar more vulnerable to shifts in investor mood, especially when combined with sharp political commentary aimed at key institutions.

One of the most sensitive issues has been the public criticism directed at the Federal Reserve. Unprecedented attacks on the central bank and its leadership have raised questions about future independence and policy consistency. For currency markets, credibility and predictability are essential. Any doubt in these areas tends to weaken confidence in a country’s currency over time.

Federal Reserve Policy and the Outlook for Interest Rates

Expectations around US monetary policy continue to play a central role in shaping the Dollar’s performance. The Federal Reserve has already taken steps to ease policy, delivering modest rate cuts in recent meetings. More importantly, its forward guidance suggests that additional easing could come in the future, reinforcing the idea that borrowing costs may continue to decline.

Adding to this outlook is the approaching leadership transition at the Federal Reserve. With the current chair’s term ending later this year, markets are already speculating about the direction a new appointment might take. Many investors believe a replacement could lean toward a more accommodative policy stance, which would likely support economic growth but limit upside potential for the US Dollar.

These expectations have kept Dollar rallies short-lived. Even when positive economic data emerges, investors tend to view it through the lens of future policy easing. As a result, optimism about growth often competes with assumptions that lower rates are on the horizon, balancing out the currency’s reaction.

Mixed Signals from Recent US Economic Data

Despite political and policy-related uncertainty, recent economic data from the United States has not been uniformly weak. In fact, some indicators suggest the economy retains a degree of resilience. Labor market data has been particularly encouraging, with fewer Americans filing for unemployment benefits than expected toward the end of the year. This points to ongoing strength in employment, which remains a cornerstone of consumer spending.

The housing sector has also offered signs of improvement. Pending home sales have risen at their fastest pace in several years, suggesting renewed interest among buyers. Housing activity is closely watched because it reflects consumer confidence and access to credit, both of which are sensitive to interest rate changes.

Still, these positive signals have not been enough to shift the broader narrative. Investors are increasingly selective, waiting for clearer confirmation that economic strength can be sustained without reigniting inflation. This cautious approach explains why attention has turned to upcoming business activity data, particularly from the manufacturing sector.

Manufacturing Data and Market Expectations

The release of new manufacturing survey results has become a key short-term focus. These reports provide insight into business conditions, new orders, employment trends, and overall confidence within the industrial sector. Current expectations point to a mild slowdown, suggesting that manufacturing growth may be losing some momentum.

While this data is important, many investors see it as part of a larger puzzle rather than a decisive signal. The most influential labor market report, covering employment trends for December, has been delayed and is now expected next week. This report is widely viewed as critical for shaping expectations about the Federal Reserve’s next steps.

Until then, markets are likely to remain cautious, with limited conviction in either direction. This wait-and-see approach has contributed to the US Dollar’s recent sideways movement against the Swiss Franc.

Switzerland’s Economic Outlook Gains Strength

On the other side of the equation, Switzerland has delivered a more optimistic set of signals. The country’s leading economic indicators have improved more than expected, reaching their strongest levels in over a year. These indicators are designed to provide early insight into future economic activity, making their recent rise particularly noteworthy.

The improvement suggests that Swiss economic growth could pick up in the coming quarters. Stronger performance in manufacturing and construction has played a major role in this positive trend. These sectors are essential to Switzerland’s export-driven economy and often serve as early drivers of broader growth.

However, Swiss economists remain cautious. While supply-side indicators such as production and output look solid, some demand-related measures are less convincing. Consumer confidence and certain spending indicators have shown signs of weakness, indicating that growth may not be evenly distributed across the economy.

Even so, the overall message from Switzerland has been more encouraging than that from many other advanced economies. This relative strength has helped support the Swiss Franc, particularly during periods of global uncertainty.

Why the Swiss Franc Remains a Safe Haven

Beyond domestic data, the Swiss Franc continues to benefit from its long-standing reputation as a safe-haven currency. During times of political tension, economic uncertainty, or market volatility, investors often seek stability. Switzerland’s strong institutions, low public debt, and consistent policy framework make its currency attractive in such environments.

This safe-haven status means the Swiss Franc does not rely solely on growth data for support. Even when economic indicators are mixed, global risk sentiment can play an equally important role. As long as uncertainty persists around US policy and global growth, demand for the Swiss Franc is likely to remain steady.

Summary: A Delicate Balance Between Caution and Optimism

The current dynamic between the US Dollar and the Swiss Franc reflects a delicate balance. In the United States, political uncertainty, expectations of further monetary easing, and questions around central bank leadership are limiting confidence in the Dollar, even as some economic data remains encouraging. Investors are looking for clearer signals, particularly from upcoming labor market reports, before committing to a stronger view.

In Switzerland, improving leading indicators and solid performance in key industries point toward better growth ahead, even as some demand-side risks linger. Combined with the Swiss Franc’s safe-haven appeal, this has helped maintain its strength during a period of global uncertainty.

As markets move forward, attention will remain focused on economic data releases and policy signals from both countries. Until clearer trends emerge, cautious trading and limited conviction are likely to define the relationship between these two major currencies.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!