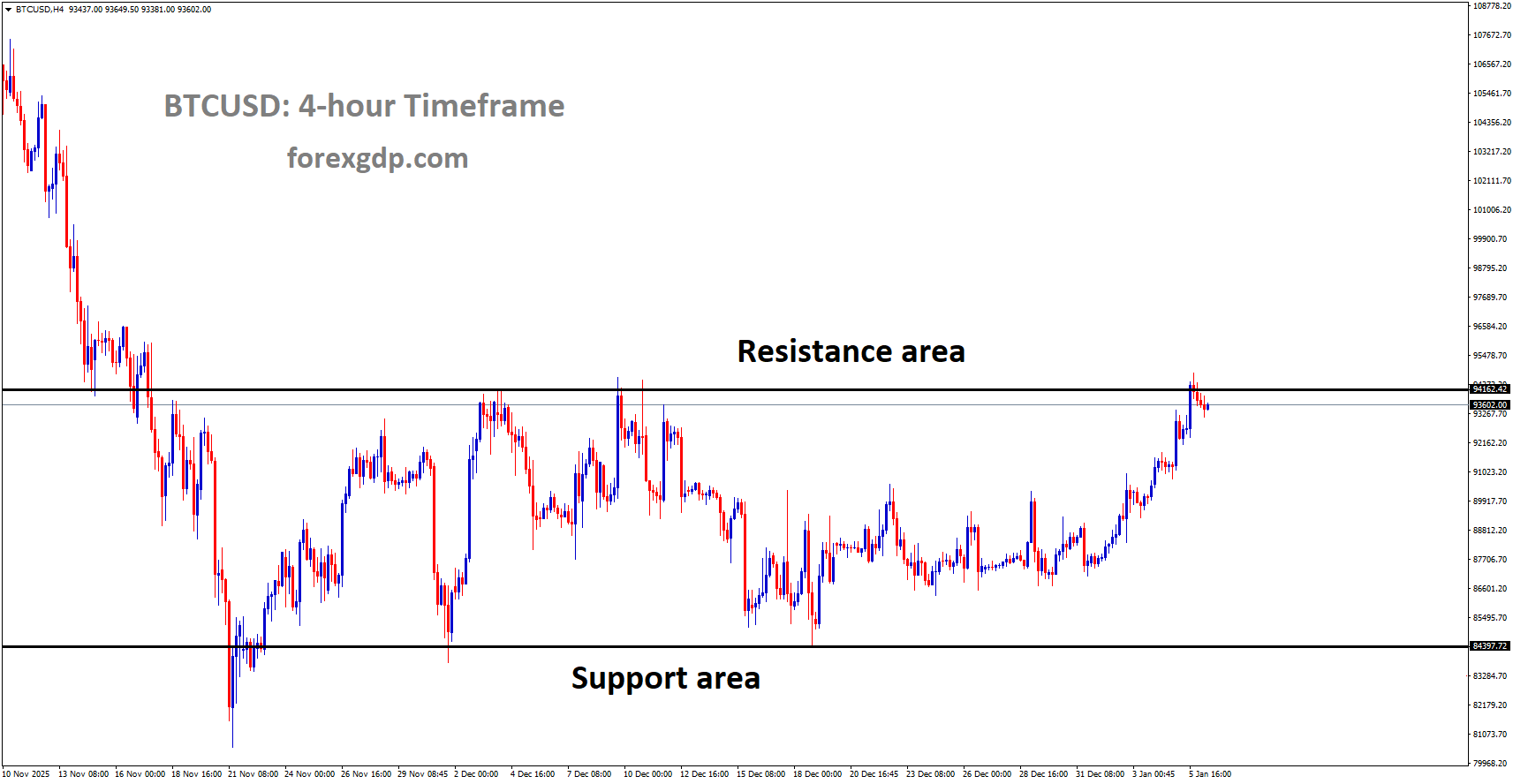

BTCUSD is moving in a box pattern, andthe market has reached the resistance area of the pattern

BTCUSD Institutional Demand Surges Again as Supply Gets Outpaced

Bitcoin is showing fresh signs of strength in 2026. After a period of hesitation at the turn of the year, large institutions are once again stepping in as steady buyers. What makes this moment stand out is not just renewed interest, but the scale of it. Institutional investors are now acquiring more Bitcoin each day than miners are creating, a shift that has often mattered in the past.

This return of demand comes after months of uncertainty and declining confidence. With supply growth being outmatched by consistent buying, many market watchers see this as an important signal for Bitcoin’s broader direction in the months ahead.

Institutions Are Buying More Bitcoin Than Miners Produce

One of the clearest signs of renewed confidence comes from a metric that tracks how much Bitcoin institutions are buying compared to how much new supply miners add to the network each day. For more than a week, institutions have been net buyers, meaning their purchases exceed the amount of Bitcoin being mined.

Recent data shows that institutional demand has been significantly stronger than new supply. On some days, institutions have absorbed roughly three-quarters more Bitcoin than miners produced. This imbalance suggests that a growing share of available supply is being taken off the market and held by long-term players.

This type of behavior is often watched closely because miners are the primary source of new Bitcoin. When their output is consistently absorbed by buyers with long-term strategies, it can reduce short-term selling pressure and support broader market stability.

Eight Straight Days of Net Institutional Buying

The current buying trend is not a one-day event. Institutions have remained net buyers for eight consecutive days, a stretch that signals commitment rather than short-term speculation. This streak follows a period when demand weakened and confidence dipped after the new year.

The metric tracking this activity includes purchases from corporate treasuries as well as U.S.-based spot Bitcoin exchange-traded funds. Together, these players represent a large and influential segment of the market. Their steady accumulation suggests that Bitcoin exposure is once again being viewed as a strategic asset rather than a risky trade.

Sustained buying over multiple days also shows that institutions are not reacting emotionally to short-term market moves. Instead, they appear to be positioning themselves based on longer-term expectations about Bitcoin’s role in global finance.

Why Institutional Behavior Matters So Much

Institutional investors differ from retail buyers in several key ways. They often move more capital, take longer-term positions, and rely on structured risk management. Because of this, their actions can shape broader market trends.

When institutions step back, liquidity often drops and confidence can fade. When they return, their presence can encourage other investors to re-engage. This effect is not just psychological. Large-scale buying can absorb available supply and change the balance between buyers and sellers.

Institutional involvement also brings visibility and legitimacy. Corporate treasuries and regulated investment products signal that Bitcoin is being treated as a serious asset class. This can attract additional participants who may have been hesitant during periods of uncertainty.

Lessons From Past Institutional Buying Cycles

Looking at past cycles offers useful context. Since 2020, periods when institutional buying has exceeded newly mined Bitcoin have often been followed by strong upward moves over time. On average, Bitcoin has delivered significant gains after this type of demand shift.

Not every cycle looks the same, and results are never guaranteed. Still, the pattern has repeated often enough to keep analysts paying attention. In one notable instance, the shift toward net institutional buying led to a substantial move higher in the months that followed.

What matters most is not the exact outcome, but the signal itself. When large, long-term investors decide that current conditions are attractive, it often reflects deeper confidence in Bitcoin’s future rather than short-lived excitement.

A Market Ready for a Relief Bounce

Bitcoin has spent several months under pressure, with sentiment cooling and activity slowing. Long periods of losses can exhaust sellers and reduce volatility, creating conditions where even modest demand can have a noticeable impact.

The return of institutional buying suggests that some investors see value after the recent downturn. This does not mean a straight line upward, but it does raise the chances of a relief bounce as selling pressure eases and confidence begins to rebuild.

Relief moves are often driven by shifts in sentiment rather than dramatic news events. In this case, the simple fact that demand is once again exceeding supply may be enough to change how investors view the near-term outlook.

The Role of ETFs and Corporate Treasuries

Two major forces are behind the current buying trend: spot Bitcoin ETFs and corporate treasuries. ETFs provide regulated, easy access for large investors who may not want to hold Bitcoin directly. As these funds grow, they can steadily absorb supply without drawing much attention.

Corporate treasuries, on the other hand, tend to make deliberate and infrequent purchases. When companies decide to add Bitcoin to their balance sheets, they often do so with a long-term view. This reduces the likelihood of rapid selling during market dips.

Together, these groups create a base of demand that is less sensitive to short-term fear. Their continued interest helps explain why institutional buying has remained strong even after recent market weakness.

What This Could Mean Going Forward

The fact that institutions are buying more Bitcoin than miners produce is a meaningful shift. It suggests that demand is not only returning but doing so in a sustained way. While short-term fluctuations will always happen, this kind of behavior often supports a more constructive environment.

Investors watching Bitcoin in 2026 are likely paying close attention to whether this trend continues. A longer streak of net buying could reinforce confidence and encourage broader participation. On the other hand, a sudden slowdown would signal renewed caution.

For now, the data points to a market that is gradually rebuilding momentum after a challenging period. Institutions appear willing to step in before sentiment fully recovers, which has historically been a notable pattern.

Final Summary

Bitcoin is seeing renewed institutional interest in 2026, with large investors buying more Bitcoin each day than miners are adding to the supply. This trend has lasted over a week and includes strong participation from corporate treasuries and spot Bitcoin ETFs. Historically, similar periods of net institutional buying have often preceded meaningful recoveries. After months of losses and uncertainty, the return of steady demand suggests Bitcoin may be entering a phase of stabilization and renewed confidence, driven by long-term investors rather than short-term speculation.

EURUSD loses momentum as the Dollar regains footing and Germany CPI takes center stage

The Euro–US Dollar pair has struggled to hold onto recent momentum as fresh economic updates reshaped market sentiment. Traders are weighing weaker signals from the Eurozone against soft data and cautious messaging from the United States, leading to uneven and hesitant trading. With important labor market reports approaching, confidence remains fragile and direction uncertain.

EURUSD is moving in an Ascending Triangle pattern, andthe market has fallen from the resistance area of the pattern

A Softer Eurozone Outlook Weighs on the Euro

The Euro came under pressure after new data showed that the services sector in the Eurozone lost a bit more steam than initially thought. The latest revision to the Services Purchasing Managers’ Index revealed slightly slower growth compared to earlier estimates, signaling that activity in this crucial part of the economy may be cooling.

Services play a major role in the Eurozone’s overall performance, especially as manufacturing has struggled in recent months. When services growth slows, it raises concerns about broader economic resilience. This revision, though modest, was enough to dampen optimism and reduce demand for the common currency after its brief rebound at the start of the week.

Investors are now shifting their attention to upcoming inflation data from Germany. As the region’s largest economy, Germany often sets the tone for broader Eurozone trends. Any surprises in consumer price data could quickly influence expectations around future policy decisions by the European Central Bank and shape the Euro’s near-term direction.

US Economic Data Sends Conflicting Signals

Across the Atlantic, recent economic releases have painted a mixed picture of the US economy. Manufacturing activity showed renewed weakness, with business conditions deteriorating at a faster pace than markets had anticipated. New orders remained subdued, highlighting ongoing challenges for producers as demand stays uneven.

At the same time, price pressures within the manufacturing sector have not eased meaningfully. This combination of slowing activity and stubborn cost pressures complicates the outlook and keeps policymakers cautious. For markets, it creates uncertainty about how quickly the US central bank might move toward further monetary easing.

Comments from Federal Reserve officials added another layer to the discussion. While acknowledging that inflation pressures appear to be gradually easing, policymakers have also warned about potential risks in the labor market. These remarks supported the idea that interest rate cuts could still be on the table, but not without careful consideration of employment conditions.

Markets Remain Cautious Ahead of Key Labor Reports

Why Employment Data Matters So Much

With limited conviction coming from recent data, traders are increasingly focused on upcoming US labor market reports. Employment figures are seen as a crucial piece of the puzzle, offering insight into whether the economy is cooling enough to justify looser monetary policy.

Market participants are especially alert to signs of rising unemployment or slowing job creation. Any evidence that the labor market is losing momentum could reinforce expectations of policy easing and influence currency flows. Until those numbers are released, many investors are choosing to stay on the sidelines, contributing to choppy and directionless trading.

Services Data Still in Focus

Alongside labor reports, the final reading of US services activity is also on the radar. Earlier estimates pointed to a slowdown in growth compared to the previous month. While not as market-moving as employment data, services indicators help round out the broader economic picture and can still affect short-term sentiment.

Together, these releases are expected to shape expectations for the US economy in the weeks ahead. Until clearer signals emerge, uncertainty is likely to remain a defining feature of market behavior.

Geopolitical Developments Take a Back Seat

Recent geopolitical headlines have done little to shake investor confidence. Developments involving US actions abroad and diplomatic responses from other global players have been closely monitored but largely absorbed without major market disruption.

For now, economic fundamentals are playing a more dominant role in shaping sentiment. Unless tensions escalate or directly impact trade and energy markets, geopolitics is likely to remain a secondary concern compared to growth, inflation, and central bank policy.

Inflation Expectations in Europe Remain Mixed

Germany’s Data Could Set the Tone

Inflation data from Germany is expected to show a short-term rebound in monthly figures after a previous decline. However, the annual pace of inflation is forecast to slow, reinforcing the idea that price pressures may be easing over the longer term.

This combination highlights the uneven nature of inflation trends across the Eurozone. While short-term fluctuations are common, the broader direction is what matters most for policymakers. A continued slowdown in annual inflation could support expectations that the European Central Bank will maintain a cautious stance moving forward.

For the Euro, these expectations matter. Slower inflation can reduce the urgency for tighter policy, which in turn may limit the currency’s appeal compared to alternatives.

A Market Searching for Clear Direction

The current environment reflects a market caught between competing forces. On one side, weaker economic signals from Europe are weighing on confidence in the Euro. On the other, softer US data and careful messaging from Federal Reserve officials are limiting demand for the US Dollar.

Risk appetite has improved at times, but it remains fragile. Without a strong catalyst, price action has lacked conviction, with traders reacting quickly to headlines but hesitant to commit to a clear trend. This back-and-forth behavior underscores how sensitive markets are to each new data point.

Final Summary

The Euro–US Dollar pair is navigating a period of uncertainty driven by mixed economic signals on both sides of the Atlantic. A downward revision in Eurozone services activity has renewed pressure on the Euro, while weak US manufacturing data and cautious central bank commentary have capped Dollar strength. With major US labor reports approaching and key European inflation data in focus, traders are adopting a wait-and-see approach. Until clearer evidence emerges about growth, inflation, and employment trends, choppy trading and cautious sentiment are likely to remain the norm.

GBPUSD Pulls Back as Traders Turn Away From the Pound

The British Pound has been showing notable strength compared with other major currencies as global market confidence improves. Investors have recently leaned toward assets that are seen as more stable when uncertainty fades, and this shift in mood has helped support the Pound.

GBPUSD is moving in a descending channel, andthe market has reached the lower high area of the channel

Even though the Pound gave back some of its early gains during European trading hours, its overall performance remains resilient. The brief pullback came as the US Dollar regained some ground after an initial dip. Still, many traders see the broader outlook for the Dollar as unclear, which continues to give the Pound room to compete.

Currency markets are currently being driven less by local data and more by global developments and expectations about central bank policy. This environment has created frequent shifts in direction, but the Pound has managed to stay relatively steady amid the noise.

Uncertainty Surrounding the US Dollar

The US Dollar has struggled to find consistent support in recent sessions. One of the main reasons is weaker-than-expected data from the US manufacturing sector. Recent survey results showed that factory activity continues to shrink, marking another month of contraction. This ongoing slowdown has raised concerns about the health of the broader US economy.

Manufacturing is often seen as an early signal of economic momentum. When factories slow down, it can point to softer demand, reduced hiring, and lower investment. As a result, traders tend to reassess their expectations for economic growth and interest rate policy.

Adding to this uncertainty were comments from a senior official at the US central bank. He noted that the labor market is losing momentum and suggested that interest rates may already be close to a neutral level. Such remarks are important because they influence how investors think about future policy moves.

When markets sense that a central bank may continue easing policy, the national currency often faces pressure. In this case, doubts about the strength of the US job market have made it harder for the Dollar to build lasting momentum.

Market Sentiment Shifts After Global Political Developments

Global risk appetite has also played a key role in recent currency moves. Earlier this week, markets were unsettled by unexpected political developments involving Venezuela and the United States. News of US military action and plans to reshape Venezuela’s oil industry caused a brief wave of caution among investors.

During periods of geopolitical tension, traders often move away from riskier assets and toward safe havens. This shift initially weighed on market confidence and slowed demand for currencies tied to global growth.

However, as fears eased and no immediate escalation followed, sentiment improved. With calmer conditions returning, investors felt more comfortable taking on risk again. This change in mood helped the Pound outperform many of its peers earlier in the day, even if some of those gains later faded.

These rapid changes highlight how sensitive currency markets are to headlines. Political news, even when unrelated to the UK or US economies directly, can quickly influence trading behavior.

Limited UK Data Keeps Focus on Central Bank Policy

The economic calendar in the United Kingdom is relatively quiet this week, leaving investors with few fresh data points to analyze. In such situations, attention naturally shifts to expectations about the Bank of England and its future policy decisions.

Inflation in the UK has been cooling in recent months, which has offered some relief to households and businesses. However, price growth remains above the central bank’s target, keeping policymakers cautious. While inflation pressures have eased from earlier highs, they have not fallen far enough to allow for aggressive policy changes.

Because of this, many market participants expect the Bank of England to move slowly when it comes to easing monetary policy. A gradual approach is seen as the most likely path, balancing the need to support economic growth while ensuring inflation stays under control.

Without major domestic data releases, these expectations are likely to remain the main driver of the Pound in the near term. Any shifts in how investors view the Bank of England’s stance could quickly be reflected in currency movements.

Why the US Jobs Report Matters So Much

Looking ahead, the most important event on the calendar is the upcoming US employment report. This release is closely watched because it provides a detailed picture of labor market conditions, including job creation and wage trends.

The US central bank has already taken steps to ease policy in response to signs of labor market weakness. Officials have pointed to rising risks on the employment side as a reason for their decisions. As a result, each new jobs report carries extra weight.

If the data shows further signs of slowing, investors may strengthen their expectations for additional policy support. This could keep pressure on the US Dollar and influence global market sentiment. On the other hand, a surprisingly strong report could temporarily boost confidence in the US economy and support the Dollar.

For currency traders, this makes the employment data a key source of direction. The results will help shape expectations not just for US policy, but also for how other central banks may respond in a changing global environment.

Final Summary

The Pound Sterling has shown resilience as global market sentiment improves, even as short-term movements remain choppy. Uncertainty around the US Dollar, driven by weak manufacturing activity and concerns about the labor market, has limited the Greenback’s ability to gain strength.

At the same time, shifting risk appetite and global political developments have added to market volatility. With limited economic data from the UK, expectations for the Bank of England’s cautious approach remain central to the Pound’s outlook.

As investors await fresh signals from the US jobs report, currency markets are likely to stay sensitive to both economic data and broader global events. In this environment, steady fundamentals and clear policy guidance will continue to play a crucial role in shaping market direction.

USDJPY climbs toward 156.50 as traders brace for the US jobs report

The USD/JPY currency pair has edged higher during the European trading session, supported by a modest recovery in the US Dollar. After starting the day on a softer note, the Dollar regained its footing as investors adjusted their positions ahead of important economic data from the United States. Attention is now firmly focused on upcoming labor market reports, which are expected to play a major role in shaping expectations for future US monetary policy.

USDJPY is moving in a descending triangle pattern, andthe market has reached the lower high area of the pattern

At the same time, the Japanese Yen continues to lag against its peers, even after fresh comments from the Bank of Japan suggesting that more interest rate increases could be on the way. This contrast between cautious optimism around the US economy and lingering uncertainty surrounding Japan’s policy outlook has helped keep USD/JPY tilted to the upside.

Shifting Market Mood Supports the US Dollar

Earlier in the session, the US Dollar faced some pressure as investors showed a greater appetite for risk. Market sentiment leaned toward higher-risk assets after traders assessed recent geopolitical developments involving US military actions in Venezuela. While such events can often spark demand for safe-haven currencies, the initial reaction was relatively calm, allowing risk-sensitive assets to attract interest.

As the day progressed, however, the Dollar began to recover. This rebound appeared to be driven less by immediate news and more by positioning ahead of key economic releases. With major US labor market data just days away, many investors chose to reduce exposure to aggressive bets and return to the Dollar as a more balanced option.

The shift highlights how quickly market mood can change, especially when uncertainty is high. Rather than reacting strongly to one single headline, traders are increasingly weighing a broader mix of economic signals, central bank messaging, and global events.

Focus Turns to US Employment Data

The main driver for currency markets in the coming days is the upcoming US employment report. This data is widely seen as a critical indicator of the health of the American economy and a key input for Federal Reserve decision-making. Recent comments from Fed officials suggest that policymakers are paying closer attention to potential weaknesses in the labor market, rather than being overly concerned about stubborn inflation.

This change in tone has added an extra layer of importance to jobs data. A resilient labor market could reinforce the idea that the US economy remains strong enough to handle current interest rate levels. On the other hand, signs of cooling employment conditions may strengthen the case for a more cautious approach from the central bank.

Ahead of the main employment release, investors will also monitor several other labor-related and activity indicators. Private-sector hiring data, services sector business surveys, and reports on job openings are all expected to offer additional insight into employment trends and overall economic momentum. Together, these releases will help shape expectations and could influence currency movements throughout the week.

Federal Reserve Outlook Influences Currency Direction

The Federal Reserve’s current stance has become a central theme in currency markets. While inflation has eased from previous highs, policymakers have made it clear that their decisions will depend heavily on incoming data. Recent remarks indicate growing awareness of downside risks, particularly if the labor market begins to soften more than expected.

This balanced approach has kept markets guessing. Investors are trying to determine whether the Fed will prioritize supporting economic growth or remain focused on ensuring inflation stays under control. As a result, even small surprises in economic data can trigger noticeable market reactions.

For the US Dollar, this environment creates both support and vulnerability. The currency benefits from its role as a global benchmark and a relatively stable option during uncertain times. At the same time, shifting expectations around interest rates can lead to periods of volatility, especially against currencies tied to different policy paths.

Japanese Yen Struggles Despite Hawkish Signals

On the other side of the USD/JPY pair, the Japanese Yen has shown continued weakness. This comes despite comments from Bank of Japan Governor Kazuo Ueda indicating that further interest rate increases are likely if economic conditions develop as expected. According to Ueda, adjusting the level of monetary support is seen as a necessary step toward achieving steady growth and stable inflation.

In theory, such remarks would normally support the Yen. Higher interest rates can make a currency more attractive by improving returns on domestic assets. However, in practice, the Yen has not responded positively. This suggests that markets remain cautious about the pace and scale of any policy tightening from the Bank of Japan.

Japan has maintained an ultra-loose monetary policy for an extended period, and investors may need more concrete actions before changing their outlook. There is also uncertainty about how higher rates might affect Japan’s economy, which has faced long-standing challenges related to growth and inflation dynamics.

Policy Divergence Keeps USD/JPY in Focus

One of the key themes driving USD/JPY is the difference in policy direction between the Federal Reserve and the Bank of Japan. While the Fed is carefully balancing inflation control with growth risks, the BoJ is only beginning to step away from its long-standing accommodative stance.

This divergence creates a complex backdrop for the currency pair. Even hints of tightening from Japanese policymakers may not be enough to offset the broader appeal of the US Dollar, particularly if US economic data remains relatively firm. As long as investors believe that policy changes in Japan will be gradual, the Yen may continue to struggle to gain meaningful traction.

At the same time, any clear signs of a slowdown in the US labor market could shift this balance. If expectations around US policy soften significantly, the Dollar’s advantage may narrow, allowing the Yen to stabilize or recover.

What Traders Are Watching Next

Looking ahead, market participants are preparing for a busy stretch of economic releases and central bank commentary. Employment data will remain front and center, but broader indicators of economic activity will also matter. Services sector performance, business confidence, and hiring intentions can all influence expectations and currency flows.

In addition, geopolitical developments remain a background risk. While recent events have not triggered major market disruption, any escalation could quickly change sentiment and boost demand for traditional safe-haven assets.

For now, USD/JPY remains sensitive to shifts in risk appetite and policy expectations. Traders are likely to stay cautious, avoiding large commitments until clearer signals emerge from the data.

Summary

The USD/JPY pair has moved higher as the US Dollar recovers from earlier weakness, supported by cautious positioning ahead of important US labor market data. Investors are closely watching upcoming employment reports for clues about the Federal Reserve’s next steps, especially as policymakers show increased concern about potential labor market risks. Meanwhile, the Japanese Yen continues to underperform despite signals from the Bank of Japan pointing to further interest rate increases. Ongoing policy differences, combined with shifting market sentiment, are keeping USD/JPY in focus as traders await clearer direction from economic data and central bank actions.

EURGBP Holds Its Ground While Markets Wait on Germany CPI

The EUR/GBP currency pair has entered a quiet phase as investors pause and wait for fresh economic signals from Europe. With limited new data at the start of the week, market participants are choosing caution over bold moves. Attention is firmly on upcoming inflation figures from Germany, which could influence expectations around future monetary policy in the Eurozone.

EURGBP is moving in a descending triangle pattern, andthe market has fallen from the lower high area of the pattern

At the same time, the British Pound continues to show resilience. Support comes from the Bank of England’s careful and measured approach to interest rate changes. This contrast between a relatively stable UK outlook and a more uncertain Eurozone backdrop is keeping the pair locked in a narrow range, with neither side gaining a clear advantage.

A Calm Market Ahead of Key Eurozone Data

Currency markets often slow down when traders are waiting for important data, and that is exactly what is happening now. Investors are reluctant to commit to strong positions before seeing Germany’s latest inflation numbers. As the largest economy in the Eurozone, Germany plays a major role in shaping views on regional inflation trends and future policy decisions.

Inflation data matters because it directly affects how central banks respond to economic conditions. If price pressures appear stronger than expected, policymakers may be more cautious about easing policy. If inflation shows signs of cooling, it could open the door to a more supportive stance for economic growth. Until these figures are released, uncertainty remains high.

This sense of waiting has resulted in limited movement in EUR/GBP, reflecting a market that is balanced but undecided.

Why the Pound Sterling Remains Supported

One of the key reasons the Pound has remained steady is the clear communication from the Bank of England. At its most recent policy meeting, the central bank reinforced its view that any future easing of monetary policy will be slow and carefully managed.

After a modest rate cut late last year, policymakers emphasized that inflation is still running above their long-term target. Because of this, they are unwilling to rush into aggressive policy changes. Instead, decisions will depend heavily on how inflation behaves over time.

This cautious approach has reassured investors. Even though some rate cuts are expected in the coming months, the overall pace is likely to be gradual. That expectation helps limit downside pressure on the Pound, as markets do not anticipate a sharp shift toward looser policy.

Market Expectations and Investor Confidence

Investors broadly believe that the Bank of England will remain data-driven and conservative. While there is room for some easing, it is expected to happen slowly and only if inflation continues to move in the right direction.

This outlook creates a sense of stability around the Pound. Compared to currencies facing more uncertain policy paths, the UK’s clear messaging offers a degree of confidence. As a result, the Pound continues to attract support even during periods of low market activity.

Ongoing Challenges for the Euro

On the Euro side, the picture is less reassuring. Several factors are weighing on sentiment, starting with ongoing geopolitical tensions in Eastern Europe. The conflict between Russia and Ukraine continues to create uncertainty, particularly around energy supply and costs. These issues remain a long-term risk for the Eurozone economy.

In addition to geopolitical concerns, recent economic data suggest that growth across the region is losing momentum. Business activity indicators have softened, pointing to slower expansion as the year came to a close.

The services sector, while still growing, has shown signs of cooling. When combined with weaker performance in other areas, this trend suggests that the Eurozone economy is struggling to build strong forward momentum.

Slowing Growth and Its Impact on the Euro

Slower economic growth makes policymaking more complicated for the European Central Bank. On one hand, inflation remains an issue that cannot be ignored. On the other, weak growth increases pressure to support the economy.

This balancing act adds uncertainty for investors. Without a clear signal on whether the ECB will prioritize fighting inflation or supporting growth, the Euro remains vulnerable to shifts in sentiment driven by incoming data.

Germany’s Inflation Data Takes Center Stage

The next major focus for markets is Germany’s Consumer Price Index release. These figures are closely watched because they often influence expectations for Eurozone-wide inflation trends.

If inflation in Germany shows stronger-than-expected growth, it could lead investors to reassess how quickly the ECB might move toward easier policy. In that scenario, the Euro could find some short-term support as markets factor in a less flexible central bank stance.

However, any boost from higher inflation data may be limited. Broader economic conditions across the Eurozone remain fragile, and concerns about growth are unlikely to disappear overnight.

What Strong or Weak Data Could Mean

A stronger inflation reading could delay expectations for policy easing, offering temporary relief for the Euro. On the other hand, weaker data would reinforce concerns about slowing demand and could increase pressure on the ECB to act.

Either outcome has the potential to influence EUR/GBP in the near term, but the overall direction will likely depend on a wider set of economic indicators rather than a single data release.

A Market Caught Between Competing Forces

The current state of EUR/GBP reflects a market caught between competing narratives. The Pound benefits from steady central bank guidance and relative economic stability. The Euro faces headwinds from geopolitical risks and signs of slowing growth, but could still react positively to inflation surprises.

With no decisive catalyst yet, investors are choosing patience. Trading activity remains subdued as participants wait for clearer signals that could justify a stronger directional move.

This period of consolidation highlights how sensitive currency markets are to expectations around policy and growth. Even small changes in outlook can shift sentiment quickly once new information becomes available.

Final Summary

EUR/GBP is currently moving sideways as investors wait for meaningful economic updates, particularly from Germany. The Pound remains supported by the Bank of England’s cautious and transparent approach to monetary policy, which has helped maintain confidence despite expectations of gradual easing.

Meanwhile, the Euro continues to face uncertainty from geopolitical tensions and slowing economic activity across the Eurozone. Germany’s inflation data may offer short-term direction, but the broader outlook remains mixed.

Until clearer macroeconomic signals emerge, EUR/GBP is likely to remain in a holding pattern, reflecting a market that is cautious, data-focused, and unwilling to make strong commitments without fresh evidence.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!