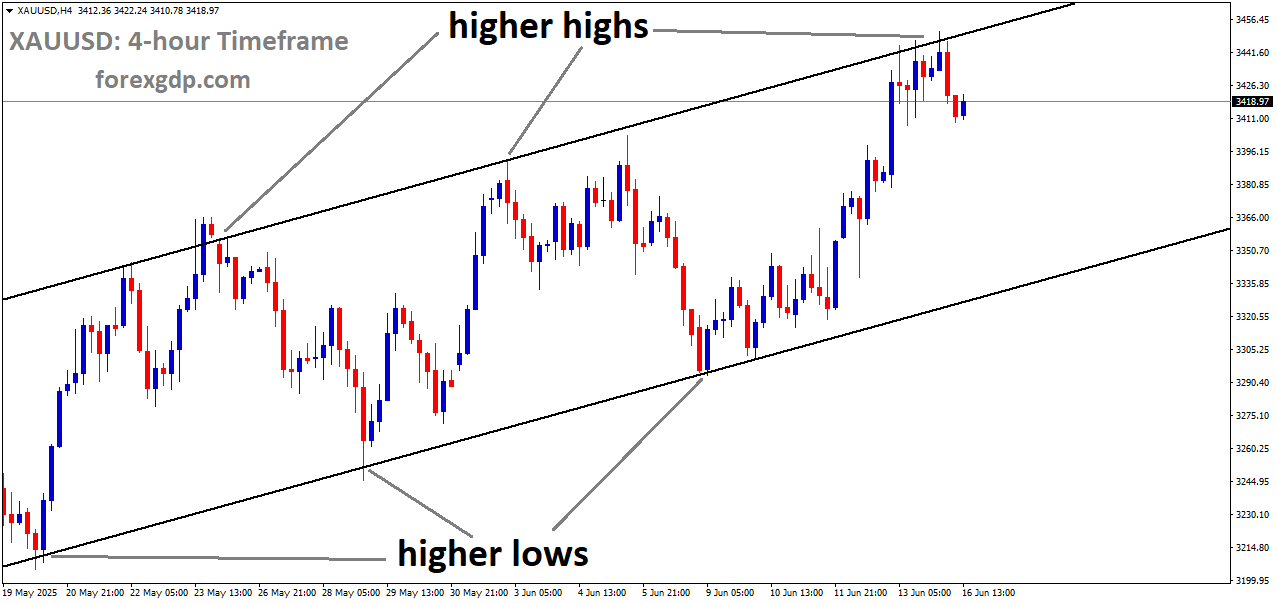

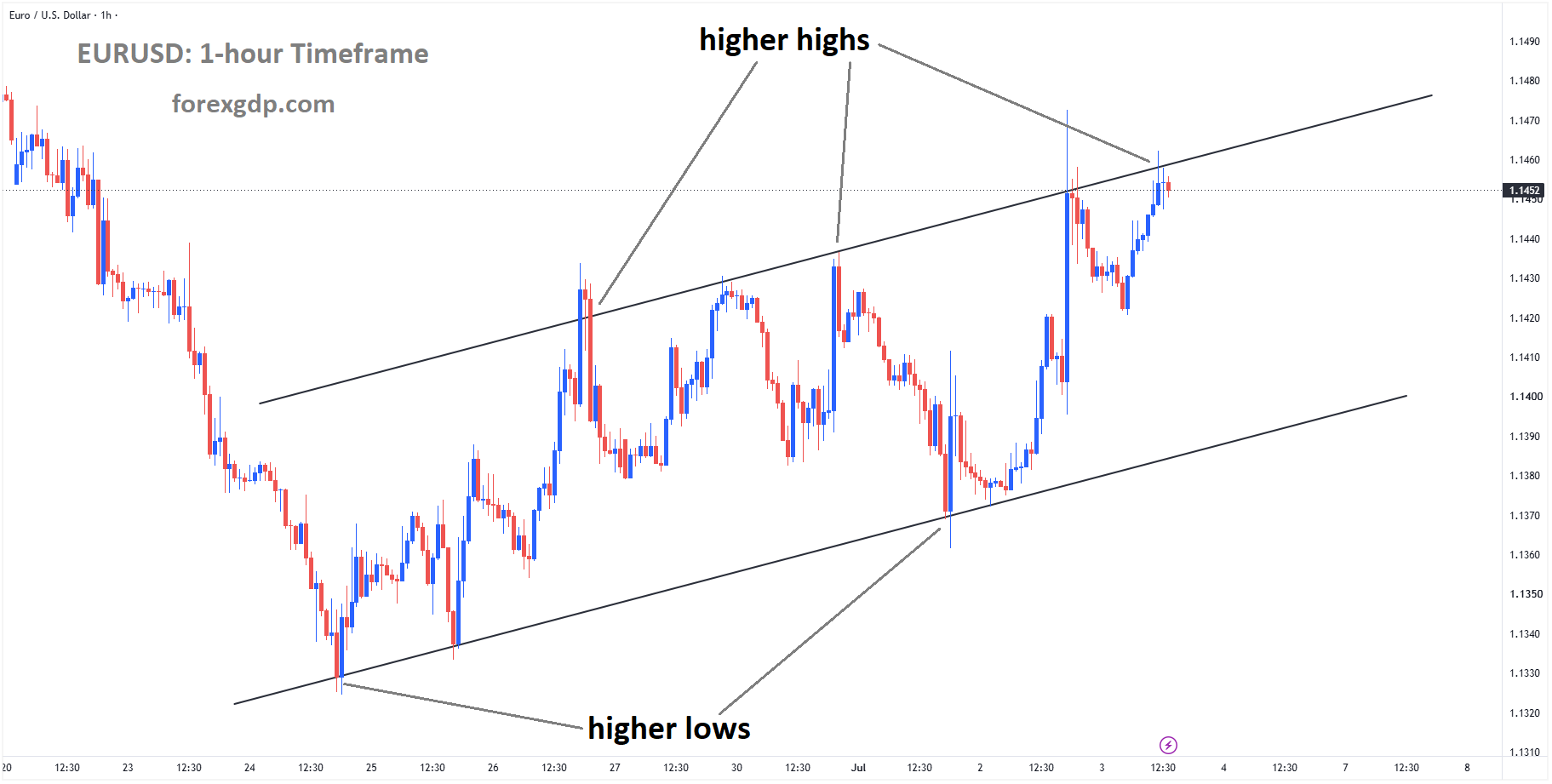

EURUSD reached a higher high area of the ascending channel

EURUSD Advances as Slowing US Labor Market Pressures the Dollar

The Euro strengthened against the US Dollar during Friday’s European trading session as the US currency lost momentum following weaker-than-expected US employment data. Softer labor market figures have prompted investors to reassess expectations for future Federal Reserve policy, giving the Euro additional support.

At the same time, attention is shifting toward upcoming US economic data that could provide fresh clues about the strength of the American economy. In Europe, comments from European Central Bank (ECB) officials suggest that policymakers remain cautious, with inflation developments continuing to play a key role in future decisions.

Weak US Jobs Report Pressures the Dollar

The US Dollar came under pressure after the latest Nonfarm Payrolls (NFP) report showed that job creation slowed more than expected in June. The labor market added significantly fewer jobs than economists had anticipated, while the previous month’s employment figures were also revised lower.

A weaker jobs report often raises concerns that the economy may be losing momentum. When hiring slows, investors begin to question whether the Federal Reserve will need to maintain its current policy stance for as long as previously expected.

This shift in market sentiment reduced demand for the US Dollar, allowing the Euro to move higher during the trading session.

Fed Rate Expectations Begin to Shift

Following the disappointing employment report, investors adjusted their outlook for the Federal Reserve’s next policy decisions.

Before the jobs data, many market participants believed there was a stronger possibility that the Fed could tighten monetary policy again later this year. However, the weaker labor market numbers have reduced confidence in that scenario.

While policymakers have not officially changed their stance, financial markets are now pricing in a lower probability of additional tightening in the near future. As expectations soften, the US Dollar often loses some of its strength against other major currencies.

The Federal Reserve continues to emphasize that future decisions will depend on incoming economic data rather than following a fixed path.

Investors Await US ISM Services PMI

The next major event attracting market attention is the release of the US ISM Services Purchasing Managers’ Index (PMI) for June.

The services sector represents a large portion of the US economy, making this report an important measure of overall business activity. Investors will closely watch whether service companies continue to expand or whether signs of slower economic growth become more visible.

A stronger reading could improve confidence in the US economy and support the Dollar. On the other hand, weaker data could reinforce concerns created by the latest employment report and influence expectations for future Federal Reserve decisions.

Because markets remain highly sensitive to economic releases, the ISM Services PMI could become an important driver of currency movements.

ECB Keeps Watching Inflation Carefully

In the Eurozone, investors are also paying close attention to signals from the European Central Bank.

Recent comments from ECB officials indicate that inflation remains under control in some important areas. Policymakers have noted that so-called second-round inflation effects have not yet appeared.

These effects usually occur when higher prices begin pushing wages and business costs upward, creating another wave of inflation. Since this has not happened so far, ECB officials believe there is currently less pressure to take additional policy action.

Even so, the central bank continues to monitor economic conditions carefully, knowing that inflation trends can change over time.

Christine Lagarde Sees More Balanced Risks

ECB President Christine Lagarde recently spoke at the ECB Forum on Central Banking and shared a cautious but balanced assessment of the current economic environment.

According to Lagarde, second-round inflation pressures have not emerged, although the ECB remains alert to any future changes. She also explained that risks facing the economy appear to be more balanced than they were only a few weeks ago.

Her comments suggest that the central bank is not rushing toward further policy changes. Instead, officials are carefully evaluating new economic information before making any major decisions.

This balanced approach provides investors with greater clarity while keeping future options open if economic conditions shift.

ECB Policymaker Calls for Patience

Pierre Wunsch, a member of the ECB’s Governing Council and head of Belgium’s central bank, echoed a similar message.

According to his recent remarks, he does not currently support additional monetary policy tightening unless stronger inflation pressures begin to develop through second-round effects.

His comments reinforce the broader view within the ECB that there is no immediate need for further action unless inflation starts showing new signs of becoming more persistent.

For investors, this indicates that future ECB decisions will remain closely linked to incoming economic data rather than being driven by short-term market expectations.

Markets Continue to Watch Economic Data Closely

Both the Federal Reserve and the European Central Bank are now entering a period where incoming economic reports will carry even greater importance.

In the United States, employment figures and business activity data will help determine whether the recent slowdown is temporary or part of a broader trend. In Europe, inflation developments will remain the primary focus as policymakers assess whether additional action will eventually become necessary.

As both central banks continue to emphasize a data-dependent approach, investors are likely to react quickly to every major economic release.

Summary

The Euro gained ground against the US Dollar after weaker US employment data reduced confidence in expectations for further Federal Reserve policy tightening. The disappointing jobs report shifted investor sentiment and weakened demand for the Dollar, while attention now turns to the upcoming US ISM Services PMI for further insight into the economy.

Meanwhile, European Central Bank officials continue to signal a cautious approach. Both Christine Lagarde and Pierre Wunsch have stated that second-round inflation pressures have not yet appeared, reducing the urgency for additional policy tightening. With both central banks relying heavily on incoming economic data, future currency movements will continue to depend on how inflation and economic growth evolve in the coming weeks.

GBPUSD Climbs as Weak US Dollar Fuels Pound Strength

The British Pound continued to perform well against the US Dollar on Friday, building on a strong week that has seen the currency post its best weekly performance in about three months. A combination of disappointing US employment figures and growing confidence in the UK’s fiscal direction has helped strengthen demand for the pound while putting pressure on the US Dollar.

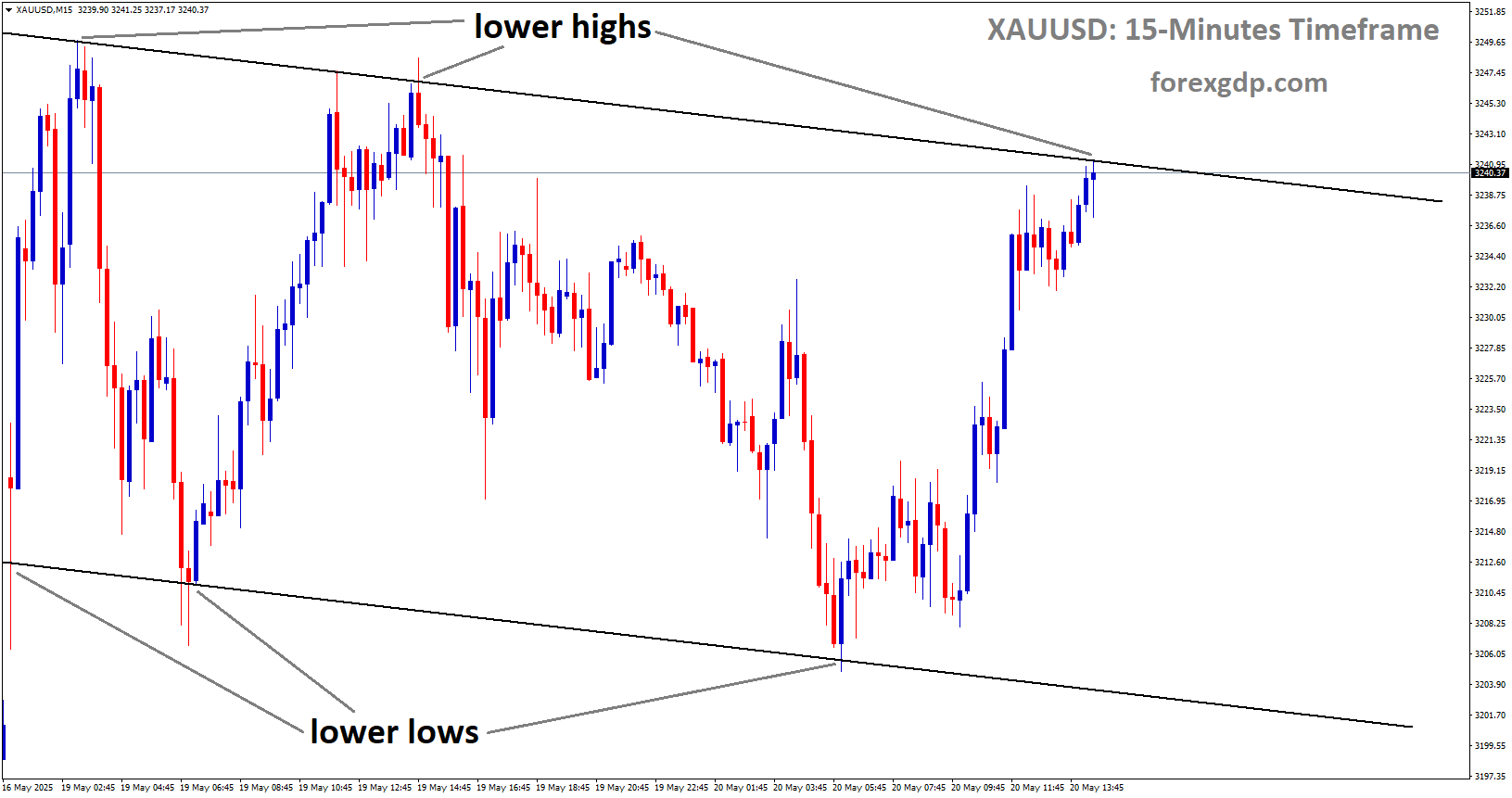

GBPUSD reached the lower high area of the descending channel

The latest economic developments have changed investor expectations for interest rates in the United States. At the same time, political stability and confidence in fiscal management in the United Kingdom have given Sterling additional support. Together, these factors have created favorable conditions for the British currency.

Weak US Employment Report Pressures the US Dollar

One of the biggest reasons behind the recent weakness in the US Dollar is the latest employment report released by the US Bureau of Labor Statistics.

According to the report, the US economy added only 57,000 jobs during June. Economists had expected a much stronger increase of around 110,000 jobs. The lower-than-expected result suggested that the labor market is losing momentum after months of steady hiring.

The report also included a downward revision to May’s employment data. Instead of adding 172,000 jobs as initially reported, the revised figure showed only 129,000 new positions. This revision reinforced concerns that hiring has been slowing more than previously believed.

Another important signal came from the labor force participation rate, which dropped to its lowest level in five years. This means fewer people are actively working or looking for jobs, adding to concerns about the strength of the labor market.

Taken together, these figures painted a softer picture of the US economy and reduced confidence in the US Dollar.

Federal Reserve Rate Expectations Shift

The weaker employment data has significantly influenced how investors view the Federal Reserve’s next policy decisions.

Before the jobs report, many market participants believed there was a stronger possibility that the central bank would continue raising interest rates in the coming months. However, the disappointing labor market figures have reduced those expectations.

Investors now believe the Federal Reserve may take a more cautious approach before making any additional policy moves. As expectations for further tightening eased, demand for the US Dollar also weakened.

Government bond yields also moved lower following the report, reflecting changing expectations for future interest rates. Lower yields generally make the US Dollar less attractive to investors seeking higher returns, contributing to the currency’s recent decline.

This shift in market sentiment has been one of the key drivers supporting the British Pound during the week.

Confidence in UK Fiscal Policy Supports Sterling

While the US Dollar faced pressure from weaker economic data, the British Pound received support from growing confidence in the UK’s economic leadership.

Following recent political developments, investors have been watching closely for signs of how the country’s new leadership will manage public finances. Markets generally prefer governments that demonstrate a commitment to responsible spending and stable economic policies.

Recent comments from Andrew Burnham, who is considered one of the leading candidates to succeed Prime Minister Keir Starmer, have helped reassure investors. Burnham stated that he intends to follow Chancellor Rachel Reeves’ fiscal framework, signaling continuity in the government’s approach to managing public finances.

These remarks have reduced some of the uncertainty surrounding the UK’s political transition. Investors often reward stability, and the commitment to maintaining fiscal discipline has helped improve confidence in the British Pound.

Although political changes can sometimes create uncertainty, clear communication about economic policy has helped ease market concerns for now.

Services Sector Data Remains in Focus

Alongside political developments, investors are also monitoring the latest economic data from the United Kingdom.

The final reading of the June S&P Global Services Purchasing Managers’ Index (PMI) is expected to provide additional insight into the health of the country’s largest economic sector.

Preliminary figures indicated that business activity in the services sector slowed during June compared with the previous month. While the decline suggests businesses may be facing some challenges, the final report will help determine whether conditions have improved or weakened further.

Since the services sector makes up a significant portion of the UK economy, the PMI report is closely watched by investors looking for clues about future economic growth.

Although the report may influence short-term market sentiment, confidence in the government’s fiscal approach has remained one of the stronger sources of support for Sterling this week.

Changing Market Sentiment Shapes Currency Performance

Currency markets often react quickly when expectations for central bank policies begin to change.

The latest US jobs report has shifted attention away from further interest rate increases and toward concerns about slowing economic growth. This change has reduced demand for the US Dollar while encouraging investors to look at alternative currencies with stronger near-term support.

At the same time, the United Kingdom has benefited from improving confidence in fiscal stability despite ongoing political changes. Investors generally favor predictable government policies, especially during periods of global economic uncertainty.

The combination of softer US economic data and greater confidence in UK fiscal management has created a favorable environment for the British Pound.

While future economic reports from both countries will continue to influence market direction, the current balance of factors has clearly favored Sterling over the US Dollar.

What Investors Will Watch Next

Looking ahead, attention will remain focused on incoming economic data and comments from policymakers.

In the United States, investors will continue assessing whether recent labor market weakness is temporary or the beginning of a broader slowdown. Future employment reports, inflation figures, and Federal Reserve communication will all play important roles in shaping expectations.

In the United Kingdom, markets will closely follow economic indicators, business activity reports, and statements from government officials to evaluate whether confidence in fiscal policy remains strong.

Political stability, economic performance, and central bank decisions will continue to be the major themes influencing the direction of both currencies in the weeks ahead.

Summary

The British Pound has enjoyed a strong week as disappointing US employment data weakened confidence in the US Dollar and reduced expectations for additional Federal Reserve interest rate increases. At the same time, reassurance about the United Kingdom’s commitment to responsible fiscal management has strengthened investor confidence in Sterling. As markets continue to monitor economic data and policy developments from both countries, these factors are likely to remain important drivers of the GBP/USD exchange rate.

USDJPY Under Pressure as Japan Signals Currency Action and Dollar Weakens

The USD/JPY currency pair remained volatile during Friday’s Asian trading session as investors weighed growing expectations of possible action by Japanese authorities and changing views on the United States interest rate outlook. While the US Dollar has recently shown signs of weakness, the Japanese Yen has attracted fresh attention as traders closely monitor comments from Japan’s government.

USDJPY reached the resistance area of the box pattern

At the same time, weaker-than-expected US employment figures have encouraged investors to rethink how the Federal Reserve may approach future monetary policy. Together, these developments have shifted market sentiment and increased uncertainty surrounding the direction of USD/JPY.

Japanese Officials Renew Currency Intervention Warnings

One of the biggest factors influencing the Japanese Yen is the increasing belief that Japan could step into the foreign exchange market again if necessary.

Japan’s Finance Minister, Satsuki Katayama, repeated that authorities remain prepared to act whenever required to address excessive movements in the currency market. The minister also emphasized that Japan continues to maintain close communication with the United States regarding foreign exchange issues.

These comments were closely watched because they suggest that policymakers remain concerned about rapid currency fluctuations. Whenever officials publicly discuss intervention, traders often become more cautious, reducing aggressive positions against the Japanese Yen.

The possibility of direct government action has become an important factor for investors evaluating the future direction of USD/JPY.

Thin Trading Conditions Increase Market Attention

Market participants are also paying close attention to trading conditions around the US holiday period.

Holiday trading sessions generally see lower market participation and reduced liquidity. During these quieter periods, even relatively small trading activity can create larger price movements than usual.

Because of this, some investors believe that if Japan decides to intervene in the currency market, lower trading volumes could make such action more effective. Although no official intervention has been confirmed, speculation alone is enough to influence trading decisions.

As a result, traders are becoming more careful and are avoiding taking overly aggressive positions until there is greater clarity.

Weak US Labor Data Weighs on the US Dollar

The US Dollar also came under pressure after the release of disappointing employment data from the United States.

The latest Nonfarm Payrolls report showed that the US economy created only 57,000 new jobs during June. Economists had expected around 110,000 new jobs, making the report a significant disappointment.

Although the unemployment rate edged slightly lower to 4.2% from the previous month’s 4.3%, the sharp slowdown in hiring attracted much more attention.

Employment growth is widely considered one of the strongest indicators of overall economic health. When companies hire fewer workers than expected, it may signal that businesses are becoming more cautious about future economic conditions.

This weaker hiring trend has increased concerns that the US economy may be losing momentum.

Interest Rate Expectations Shift After Employment Report

Following the disappointing labor market figures, investors quickly adjusted their expectations for future Federal Reserve policy.

Before the jobs report, markets believed there was a stronger possibility that the Federal Reserve would continue with a tighter monetary policy. However, weaker employment data reduced confidence that further interest rate increases would be necessary.

According to the CME FedWatch Tool, expectations for a September rate increase fell noticeably after the report was released. This change reflects growing confidence among investors that the central bank may choose a more cautious approach if economic growth continues to slow.

Interest rate expectations play a major role in determining currency values because higher rates generally attract more global investment. When expectations for future rate increases decline, the US Dollar often loses some of its appeal.

Federal Reserve Maintains Focus on Inflation

Despite changing market expectations, Federal Reserve officials continue to stress their long-term commitment to controlling inflation.

During the European Central Bank’s conference in Sintra, Federal Reserve Chair Kevin Warsh reaffirmed that the central bank remains focused on achieving its 2% inflation objective.

He also acknowledged that inflation risks have started to moderate over the past month, suggesting that recent economic developments have shown some encouraging signs.

These remarks indicate that while inflation remains an important concern, policymakers are also paying close attention to broader economic conditions before making future interest rate decisions.

Investors will likely continue monitoring both inflation and employment data to better understand the Fed’s next move.

Japanese Yen Benefits from Multiple Supportive Factors

The Japanese Yen is currently receiving support from several different sources at the same time.

Growing speculation about possible government intervention has encouraged traders to be more cautious about selling the Yen. At the same time, weaker US economic data has reduced confidence in the US Dollar.

This combination has helped improve sentiment toward Japan’s currency.

Currency markets are often driven by changing expectations rather than confirmed events. Even without actual intervention, repeated warnings from Japanese officials can influence investor behavior and affect market positioning.

As long as these expectations remain in place, the Japanese Yen may continue to receive additional support.

Investors Await Fresh Economic Signals

Looking ahead, traders are expected to remain highly focused on incoming economic data and official comments from both Japan and the United States.

Any new statements from Japanese policymakers regarding exchange rates could quickly attract market attention. Likewise, upcoming US reports on inflation, employment, and overall economic activity will help shape expectations for future Federal Reserve decisions.

Central bank communication will also remain a major driver of investor sentiment in the coming weeks.

With both governments closely monitoring economic conditions, markets are likely to remain sensitive to every major announcement.

Summary

USD/JPY continues to trade in an environment shaped by both Japanese policy expectations and changing views on the US economy. Renewed warnings from Japanese officials about possible currency intervention have strengthened confidence in the Japanese Yen, while disappointing US employment data has weakened expectations for future Federal Reserve rate increases.

As investors continue to assess economic reports and central bank guidance, the balance between US monetary policy and Japan’s currency management efforts will remain one of the key factors influencing USD/JPY in the near term.

USDCAD Retreats as Improved Oil Market Lifts the Canadian Dollar

The USD/CAD currency pair remained under pressure for a second straight trading session as several factors combined to weaken the US Dollar and strengthen the Canadian Dollar. Softer-than-expected US employment data reduced expectations that the Federal Reserve would continue raising interest rates, while a rebound in crude oil prices provided fresh support for Canada’s currency.

USDCAD reached the support area of the box pattern

Although the pair attempted a small recovery during the Asian trading session, selling pressure quickly returned. As a result, USD/CAD stayed close to its recent lows, with investors focusing on changing economic expectations and global developments that continue to influence both currencies.

Weak US Jobs Report Hurts the US Dollar

One of the biggest reasons behind the latest weakness in USD/CAD is the disappointing US Nonfarm Payrolls (NFP) report. The employment data showed that the US labor market added far fewer jobs than economists had expected, raising concerns that hiring activity is slowing.

The report revealed that the US economy created only 57,000 new jobs in June, missing forecasts by a wide margin. Adding to the disappointment, the previous month’s job growth was also revised lower, showing that employment gains had been weaker than initially reported.

While the unemployment rate edged slightly lower, investors focused more on the slowdown in job creation. A softer labor market often signals that economic growth is losing momentum, making it less likely that the Federal Reserve will need to keep interest rates elevated for an extended period.

These developments placed fresh pressure on the US Dollar, which has already been struggling in recent sessions.

Federal Reserve Rate Expectations Continue to Shift

The weaker employment figures led traders to rethink their outlook for future Federal Reserve policy.

Before the latest jobs report, many investors believed the central bank could deliver additional interest rate increases over the coming year. However, the softer labor market data has significantly reduced those expectations.

Investors are now pricing in a much smaller chance of future rate hikes. Instead of expecting multiple increases, markets are leaning toward little or no additional tightening unless future economic data shows a stronger recovery.

Lower expectations for higher interest rates generally reduce demand for the US Dollar because higher rates typically attract global investors seeking better returns. As those expectations fade, the currency often loses some of its appeal.

This shift in market sentiment has become one of the main reasons behind the recent decline in USD/CAD.

Cooling Inflation Adds More Pressure on the Dollar

The latest employment report is not the only factor affecting expectations for US monetary policy. Inflation concerns have also eased in recent weeks.

Lower energy costs had already helped reduce worries that inflation would remain stubbornly high. With inflation pressures becoming more manageable, investors believe the Federal Reserve has less urgency to maintain an aggressive policy stance.

The combination of slower job growth and easing inflation creates a stronger argument for a more cautious approach from the central bank.

As a result, traders have continued reducing bullish positions in the US Dollar, adding further downward pressure on the currency.

Oil Price Recovery Supports the Canadian Dollar

While the US Dollar faced several challenges, the Canadian Dollar received support from a recovery in crude oil prices.

Canada is one of the world’s largest oil exporters, making the Canadian Dollar closely linked to movements in the energy market. When oil prices rise, Canada’s export outlook generally improves, which often benefits the country’s currency.

After recently falling to multi-month lows, crude oil prices managed to recover as geopolitical concerns returned to the market. The rebound gave additional strength to the Canadian Dollar, making it more attractive against its US counterpart.

This stronger Canadian Dollar added another layer of pressure on the USD/CAD pair.

Middle East Tensions Lift Oil Prices

The latest recovery in crude oil prices was partly driven by rising geopolitical tensions in the Middle East.

Iran’s military leadership warned that any interference by the United States in the Strait of Hormuz would receive a swift response. The Strait of Hormuz is one of the world’s most important oil shipping routes, with a large share of global energy supplies passing through the area every day.

Whenever tensions increase in this region, markets become concerned about potential disruptions to oil supplies. Even if no actual disruption occurs, the possibility alone is often enough to push oil prices higher.

The improvement in oil prices following these developments provided further support for the Canadian Dollar.

USD/CAD Faces Pressure from Multiple Directions

The current weakness in USD/CAD is not being driven by a single event. Instead, several factors are working together at the same time.

On one side, the US Dollar is losing momentum because investors expect fewer Federal Reserve rate hikes after weaker employment data and easing inflation concerns.

On the other side, the Canadian Dollar is benefiting from recovering oil prices and renewed demand for commodity-linked currencies.

When both currencies move in opposite directions simultaneously, the result is stronger selling pressure on the USD/CAD pair.

This combination has made it difficult for the pair to sustain any meaningful recovery despite occasional attempts to bounce higher during intraday trading.

Holiday Trading Calls for Extra Caution

Although market sentiment currently favors the Canadian Dollar, traders are also aware that trading activity may remain less active due to the US holiday period.

Lower market participation often reduces liquidity, which can lead to larger-than-normal price swings. During these periods, even relatively small orders can create noticeable market movements.

Because of this, investors are approaching new positions carefully while waiting for normal trading volumes to return.

Market participants will also continue monitoring upcoming economic reports, central bank comments, and geopolitical developments that could influence both the US Dollar and the Canadian Dollar in the days ahead.

Final Summary

USD/CAD remains under pressure as weaker-than-expected US employment data has reduced confidence in further Federal Reserve interest rate increases. At the same time, easing inflation concerns have added to the US Dollar’s weakness.

Meanwhile, a recovery in crude oil prices, supported by renewed geopolitical tensions in the Middle East, has strengthened the Canadian Dollar. With both currencies moving in opposite directions, USD/CAD continues to face selling pressure. As markets navigate lighter holiday trading conditions, investors will remain focused on upcoming economic data and global events that could shape the pair’s next move.

NZDUSD Rises as Positive China PMI Report Lifts New Zealand Dollar

The NZDUSD currency pair moved higher during Friday’s Asian trading session as the New Zealand Dollar gained support from encouraging economic news out of China. At the same time, weaker-than-expected employment data from the United States reduced confidence in a near-term interest rate increase by the US Federal Reserve, putting pressure on the US Dollar.

NZDUSD is rebounding from the higher low area of the ascending triangle pattern

Although trading activity may remain quieter due to the US Independence Day holiday, investors continue to focus on economic developments that could shape the outlook for both currencies in the weeks ahead.

China’s Services Sector Continues to Support the New Zealand Dollar

Fresh economic data from China provided a positive boost for the New Zealand Dollar. According to the latest report from RatingDog, China’s Services Purchasing Managers’ Index (PMI) eased slightly to 54.1 in June from 54.4 in May.

While the reading was marginally lower than the previous month, it still reflected strong growth in the country’s services sector. In fact, it marked one of the strongest expansions in services activity seen in almost three years.

This was an encouraging sign for investors because China’s domestic demand and service industries continue to show resilience despite broader economic challenges. A healthy services sector often signals steady business activity and consumer spending, helping improve confidence in the overall economy.

Growing Chinese Demand Benefits New Zealand

China remains New Zealand’s largest trading partner, making Chinese economic performance highly important for the Kiwi currency.

The latest report also highlighted that services exports expanded for the second straight month. Even more encouraging was that export growth reached its fastest pace since October 2024. This suggests that demand for Chinese services continues to improve, creating optimism about regional economic growth.

Whenever China’s economy shows signs of stability or improvement, the New Zealand Dollar often benefits because stronger Chinese demand can support New Zealand’s exports, particularly agricultural products and raw materials.

As a result, investors responded positively to the latest Chinese PMI figures, helping lift the Kiwi during Friday’s session.

RBNZ Rate Outlook Remains a Key Focus

Attention also remains on the Reserve Bank of New Zealand (RBNZ) and its future policy direction.

ASB Bank recently revised its expectations for the central bank’s next meeting. The bank no longer expects the RBNZ to raise interest rates in July. Instead, it believes policymakers will likely leave the Official Cash Rate unchanged at the upcoming meeting.

However, ASB still expects the central bank to begin gradually increasing interest rates later this year, starting in September. Under its current outlook, the bank forecasts a series of measured rate increases extending into early 2027.

This revised forecast suggests that while policymakers may choose patience in the short term, they still see room for tighter monetary policy if economic conditions continue improving.

Investors will continue monitoring future inflation data, employment figures, and economic growth to assess whether the RBNZ follows this expected path.

Weak US Jobs Data Weighs on the Dollar

The biggest driver behind the US Dollar’s weakness came from the latest US employment report.

The US Labor Department announced that Nonfarm Payrolls increased by only 57,000 jobs in June. Economists had expected a much stronger increase of around 110,000 jobs.

The lower-than-forecast hiring numbers raised concerns that the US labor market may be losing momentum after remaining resilient for an extended period.

Employment data plays a major role in shaping Federal Reserve policy decisions. A slowing job market may reduce inflation pressures over time, making policymakers less likely to increase interest rates aggressively.

Because of this, investors reacted by reducing expectations for another near-term rate hike, which weakened demand for the US Dollar.

Unemployment Rate Offers Mixed Signals

Although job creation disappointed expectations, the unemployment rate offered a more positive picture.

The unemployment rate declined to 4.2% in June compared with 4.3% in May. This indicates that the labor market has not weakened across every measure.

However, financial markets appeared to place greater emphasis on the slower pace of job creation rather than the lower unemployment rate.

Investors often look beyond a single indicator and assess the broader trend. In this case, the weaker payroll growth suggested that hiring activity may be slowing enough to influence future Federal Reserve decisions.

Federal Reserve Expectations Shift

Following the release of the employment report, traders adjusted their expectations regarding future US interest rates.

Before the jobs report, markets believed there was a stronger chance that the Federal Reserve would raise interest rates in the coming months. After the weaker employment numbers were released, those expectations eased noticeably.

This shift reflects growing uncertainty about how quickly the US economy is expanding and whether additional policy tightening will be necessary.

For currency markets, changing expectations around Federal Reserve decisions often have a significant impact on the US Dollar. When investors believe fewer rate increases are likely, the Dollar generally loses some of its appeal against other major currencies.

Holiday Trading Could Keep Markets Quiet

Friday’s trading session may experience lighter market activity because US financial markets are closed for the Independence Day holiday.

With fewer American participants in the market, trading volumes are often lower than usual. While economic headlines can still influence prices, reduced liquidity sometimes leads to slower market movements.

Even so, investors remain focused on upcoming economic releases and central bank commentary that could provide fresh direction once normal trading resumes.

What Investors Will Watch Next

Looking ahead, traders will continue monitoring economic data from both New Zealand and the United States.

Any further signs of improving Chinese economic activity could continue supporting the New Zealand Dollar due to the close trade relationship between the two countries.

At the same time, future US employment reports, inflation figures, and Federal Reserve comments will play an important role in shaping expectations for US monetary policy.

On the New Zealand side, investors will also closely follow upcoming Reserve Bank of New Zealand meetings to see whether policymakers maintain their cautious approach or begin tightening policy later this year.

Summary

The New Zealand Dollar strengthened against the US Dollar after stronger Chinese services activity boosted confidence in regional economic growth. China’s resilient services sector continues to provide important support for New Zealand’s export-driven economy.

Meanwhile, weaker-than-expected US employment growth reduced expectations for a near-term Federal Reserve interest rate increase, placing additional pressure on the US Dollar. Although the unemployment rate improved slightly, investors focused more on slowing job creation and its potential impact on future monetary policy.

As markets move forward, attention will remain centered on Chinese economic performance, Reserve Bank of New Zealand policy decisions, and upcoming US economic data, all of which are expected to influence the direction of the NZDUSD pair.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!