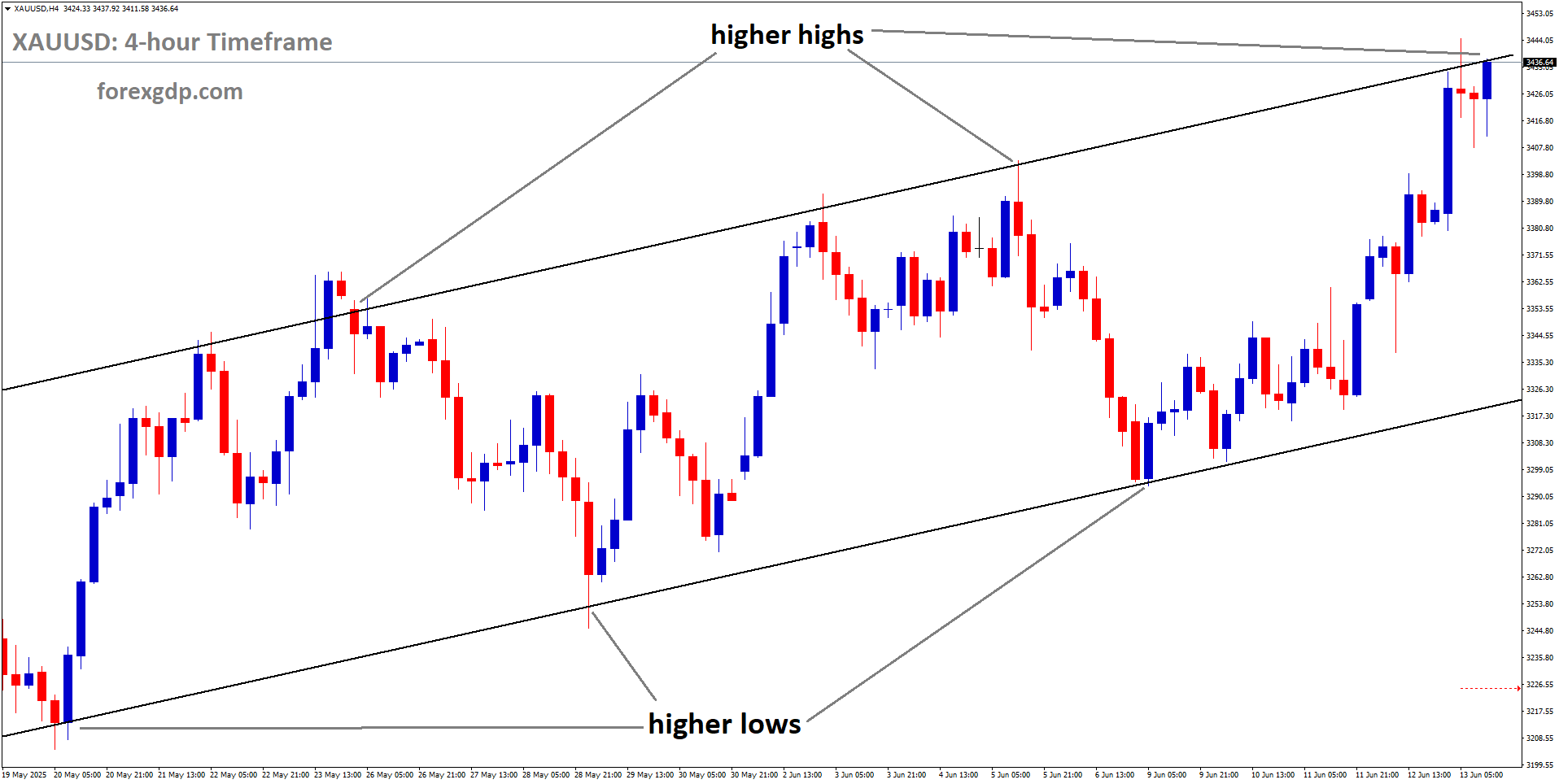

EURUSD reached the retest area of the broken descending channel

EURUSD Holds Firm as Middle East Tensions Lift Safe-Haven Dollar

The EURUSD currency pair continues to trade in a narrow range as traders weigh several important global developments. While the Euro has found enough strength to avoid major losses, it has also struggled to build strong upward momentum. The result is a market that remains cautious, with buyers and sellers reacting to changing economic and political news.

A mix of geopolitical concerns, changing expectations for central bank policies, and easing inflation pressures continues to shape the outlook for both the Euro and the US Dollar. As these factors pull the market in different directions, investors are waiting for clearer signals before making larger trading decisions.

Geopolitical Tensions Keep Demand for the US Dollar Alive

One of the biggest themes influencing the market is the renewed tension surrounding the Strait of Hormuz. This narrow waterway plays a vital role in global energy transportation, making it one of the world’s most closely watched regions.

Recent reports of security incidents involving commercial shipping have increased concerns about stability in the area. These developments have reminded investors that geopolitical risks remain a serious factor in global financial markets.

Whenever uncertainty rises, many investors naturally move toward assets that are considered safer during periods of global tension. The US Dollar often benefits from this behavior because it has long been viewed as a reliable safe-haven currency.

Although the situation has not developed into a larger crisis, the uncertainty has been enough to support demand for the Dollar and prevent the Euro from making stronger gains.

Falling Oil Prices Ease Inflation Concerns

At the same time, another important trend is influencing market sentiment. Oil prices have recently moved lower, helping reduce worries about rising inflation.

Lower energy costs can ease pressure on households, businesses, and economies. As inflation becomes less of a concern, central banks may feel less urgency to keep raising interest rates.

This shift has changed how investors view future monetary policy around the world. Instead of expecting aggressive action from central banks, markets are increasingly looking for a more measured approach.

That change has created a more balanced environment for major currencies, including both the Euro and the US Dollar.

Federal Reserve Expectations Continue to Shift

Recent economic data from the United States has also influenced market sentiment.

A softer-than-expected employment report has raised questions about how aggressively the Federal Reserve may act in the coming months. Slower job growth can be viewed as a sign that the economy is cooling, reducing the immediate need for tighter monetary policy.

Because of this, expectations for additional interest rate increases have weakened.

When markets expect fewer rate hikes, the US Dollar often loses some of the support it previously enjoyed. Investors become less eager to buy the currency if they believe future returns on Dollar-based assets may not rise as quickly as once expected.

This changing outlook has helped prevent the Dollar from strengthening too much, allowing the Euro to remain relatively stable despite ongoing challenges.

European Central Bank Faces a Different Challenge

While the Federal Reserve outlook has become less aggressive, the European Central Bank is also dealing with changing economic conditions.

Recent inflation figures from the Eurozone came in lower than many economists had expected. This has encouraged investors to believe that the ECB may also have less reason to continue tightening monetary policy.

Lower inflation is generally positive for consumers because it reduces pressure on everyday living costs. However, it also changes how markets expect central banks to respond.

If inflation continues to slow, policymakers may choose to take a more cautious approach rather than introducing additional policy tightening.

As a result, enthusiasm for the Euro has become more limited.

Mixed Signals Keep the Euro in a Tight Range

The current market reflects a balance between positive and negative influences.

On one side, reduced expectations for further Federal Reserve tightening have limited the US Dollar’s strength.

On the other, softer inflation data in Europe has reduced optimism about the European Central Bank becoming more aggressive.

Meanwhile, geopolitical uncertainty continues to provide intermittent support for the Dollar whenever global risks increase.

With these competing forces at work, neither currency has been able to establish a clear advantage.

Instead, traders are choosing to remain patient while monitoring incoming economic reports and international developments.

Investors Are Waiting for Stronger Economic Signals

Financial markets dislike uncertainty, and the current environment offers plenty of it.

Rather than reacting aggressively to every headline, many investors are waiting for a clearer picture of where economic growth, inflation, and central bank policies are heading.

Upcoming economic reports from both the United States and the Eurozone will likely play a major role in shaping future expectations.

Employment figures, inflation updates, business activity surveys, and comments from central bank officials will all be closely watched for clues about the next direction of monetary policy.

Until stronger evidence emerges, many market participants are expected to avoid taking large positions.

Global Events Continue to Influence Currency Markets

Beyond economic data, global political developments remain an important factor.

Events in key regions can quickly change investor sentiment, especially when they involve international trade routes, energy supplies, or diplomatic relations.

The recent developments around the Strait of Hormuz are a reminder that geopolitical events can influence currency markets just as much as economic reports.

If tensions rise further, investors may once again seek the relative safety of the US Dollar.

If the situation improves, attention may quickly shift back toward economic fundamentals and central bank decisions.

Why Central Bank Policies Matter So Much

Interest rate expectations remain one of the strongest drivers of currency movements.

When investors believe a central bank will maintain higher interest rates, its currency often becomes more attractive because it may offer better returns.

However, when inflation slows and economic growth begins to soften, expectations for future policy tightening usually fade.

That is exactly what markets are currently experiencing with both the Federal Reserve and the European Central Bank.

Neither institution appears to have a clear path toward aggressive policy changes at the moment, leaving traders with fewer reasons to make strong directional bets.

Summary

EURUSD continues to trade in a balanced environment as several major forces offset one another. Geopolitical tensions in the Strait of Hormuz continue to support demand for the US Dollar during periods of uncertainty, while softer US economic data has reduced expectations for additional Federal Reserve rate hikes. At the same time, weaker inflation in the Eurozone has cooled expectations for further European Central Bank tightening, limiting the Euro’s ability to gain stronger momentum.

With both currencies facing their own challenges, investors are focusing on upcoming economic reports, central bank guidance, and global political developments. Until clearer signals emerge, the EURUSD pair is likely to remain influenced by shifting market sentiment and changing expectations surrounding the global economy.

GBPUSD Climbs as Softer Fed Outlook Drags the US Dollar Lower

The GBP/USD currency pair continued to strengthen during Tuesday’s Asian trading session, extending its winning streak as the US Dollar remained under pressure. Investors have become less confident that the Federal Reserve will raise interest rates as aggressively as previously expected, following softer economic data from the United States.

GBPUSD reached the lower high area of the descending channel

At the same time, the British Pound has received support from the weaker Dollar, although its own outlook remains mixed. Expectations for future interest rate increases by the Bank of England have also been reduced, creating uncertainty about how much further the Pound can strengthen.

Why the US Dollar Is Losing Momentum

The biggest factor affecting the US Dollar is the changing view of Federal Reserve policy. Recent economic reports have shown signs that the US labor market is cooling. Employment figures for April, May, and June revealed fewer jobs were added than many analysts had expected.

This weaker employment trend has encouraged investors to believe that the Federal Reserve may not need to continue raising interest rates as aggressively as once anticipated. As expectations for tighter monetary policy fade, demand for the US Dollar has softened, helping the Pound gain ground against it.

Lower expectations for future rate hikes have become one of the main drivers behind recent movements in the currency market.

Falling Oil Prices Help Ease Inflation Concerns

Another important development has been the decline in global crude oil prices. Increased production from OPEC+ countries, combined with progress toward a peace agreement involving the United States and Iran, has reduced pressure on energy markets.

Lower energy costs often help reduce inflation because businesses and consumers spend less on fuel and transportation. This has eased concerns that inflation will remain stubbornly high in the United States.

With inflation risks appearing more manageable, investors believe the Federal Reserve has more flexibility when deciding its next policy moves. That has reduced the urgency for additional interest rate increases and added further pressure on the US Dollar.

Federal Reserve Still Maintains a Firm Inflation Focus

Although markets have become less aggressive in their expectations for future rate hikes, Federal Reserve officials continue to emphasize their commitment to controlling inflation.

Federal Reserve Governor Christopher Waller recently delivered comments that reinforced the central bank’s determination to keep inflation under control. He stressed that while forward guidance remains an important communication tool, policymakers must stay flexible because economic conditions can change quickly.

Waller also made it clear that the Federal Reserve remains committed to its long-term inflation objective. He rejected the idea of keeping interest rates artificially low for reasons unrelated to inflation, emphasizing that price stability remains the central bank’s primary responsibility.

His remarks suggest that although the pace of future tightening may slow, the Federal Reserve is not ready to abandon its fight against inflation.

Market Sentiment Reflects a More Hawkish Tone

Investor sentiment following Waller’s speech indicated that many participants still view the Federal Reserve as maintaining a relatively firm policy stance.

While recent economic data has encouraged expectations for fewer rate increases, policymakers continue to signal that inflation remains an important concern. This balance between softer economic conditions and ongoing inflation vigilance has created a more cautious outlook for the US Dollar.

As a result, currency markets continue to react to every new economic release and policy statement as investors search for clearer direction.

US Services Sector Continues to Show Resilience

Despite some signs of slower growth, the broader US economy continues to demonstrate resilience.

The latest report on business activity in the services sector showed that expansion continued during June, although growth moderated slightly. This suggests that while economic momentum has cooled, the services industry remains in healthy territory.

Within the report, employment conditions improved, indicating that hiring activity strengthened after earlier weakness. Meanwhile, price pressures eased compared to previous months, offering another encouraging sign that inflation may gradually move lower.

These mixed economic signals make the Federal Reserve’s next policy decisions more complicated. Stronger employment within the services sector supports economic stability, while easing price pressures reduce the need for aggressive policy tightening.

British Pound Faces Challenges Despite Recent Strength

Although the Pound has benefited from a weaker US Dollar, its own outlook is becoming more complicated.

Investors have significantly lowered expectations for future interest rate increases by the Bank of England. Only a short time ago, markets expected two additional rate hikes this year. Those expectations have now been reduced, with investors assigning only a moderate probability to a single increase.

This shift reflects growing confidence that inflation in the United Kingdom will gradually move toward the Bank of England’s long-term target, reducing the need for repeated policy tightening.

As expectations become more conservative, the Pound may face periods of pressure even while the US Dollar remains weak.

Bank of England Remains Patient

Bank of England Governor Andrew Bailey has maintained a cautious approach when discussing future policy.

He recently acknowledged that inflation is still expected to return to the central bank’s target over time, although the process may take longer than previously estimated. At the same time, he dismissed expectations of immediate interest rate cuts, signaling that policymakers are not yet ready to loosen monetary policy.

This balanced message reflects the Bank of England’s effort to support economic stability while continuing to monitor inflation developments carefully.

Policy Committee Shows Growing Concern About Inflation

The latest Bank of England policy meeting demonstrated that officials remain divided over the best course of action.

Most policymakers voted to keep interest rates unchanged, preferring to wait for additional economic evidence before making further adjustments. However, a larger number of committee members supported tighter policy compared with earlier meetings, highlighting ongoing concerns about inflation risks.

This growing difference of opinion suggests that future policy decisions will continue to depend heavily on incoming economic data.

Inflation Outlook Still Creates Uncertainty

Although inflation has eased from previous highs, the Bank of England believes price pressures could strengthen again later in the year.

Higher energy costs from previous periods are expected to continue filtering through the economy, potentially causing inflation to rise temporarily before gradually stabilizing.

Because of this uncertainty, many financial institutions now believe that any future interest rate increase could arrive much later than previously expected.

This outlook explains why investors have become less confident about additional policy tightening in the near future.

What Investors Are Watching Next

Looking ahead, traders will closely monitor upcoming economic reports from both the United States and the United Kingdom.

Fresh employment data, inflation readings, and comments from central bank officials will likely play a major role in shaping expectations for future monetary policy.

Any signs that inflation is slowing faster than expected could weaken the US Dollar further. On the other hand, stronger economic performance or more hawkish comments from Federal Reserve officials could help the Dollar recover some lost ground.

Similarly, developments in the UK economy and future guidance from the Bank of England will remain key factors influencing the British Pound.

Summary

The recent strength in GBP/USD has been driven largely by a softer US Dollar as investors reduced expectations for aggressive Federal Reserve rate hikes following weaker employment data and easing inflation pressures. Falling oil prices have also contributed to a more relaxed outlook for inflation, giving markets greater confidence that the Fed may slow its policy tightening.

However, the outlook remains balanced rather than one-sided. Federal Reserve officials continue to stress their commitment to controlling inflation, while the US economy still shows signs of resilience. Meanwhile, the British Pound faces its own challenges as expectations for additional Bank of England rate hikes have become more limited. With both central banks carefully assessing incoming economic data, future movements in GBP/USD will likely depend on how inflation, employment, and overall economic conditions evolve in the months ahead.

USDJPY Slips as Softer US Dollar Lifts the Japanese Yen

The Japanese Yen managed to gain some ground against the US Dollar on Tuesday as the Greenback lost some momentum after its recent rally. While the move was relatively modest, it offered the Yen a brief period of relief after weeks of heavy selling pressure.

USDJPY is breaking the resistance area of the box pattern

Investors are now turning their full attention to the upcoming release of the Federal Reserve’s latest meeting minutes. With few major economic events scheduled before then, many traders are choosing to stay cautious and avoid making large investment decisions until they have more clarity on the US central bank’s outlook.

US Dollar Pauses After Recent Strength

The US Dollar has slowed down following a strong run in recent sessions. After reaching its highest levels last week, the currency has struggled to find fresh buying interest. This pause has allowed other currencies, including the Japanese Yen, to recover slightly.

The US Dollar Index, which measures the value of the Dollar against a basket of major currencies, has been moving within a narrow range. Instead of showing a clear trend, the index has been fluctuating as investors reassess expectations for future monetary policy in the United States.

A weaker-than-expected US employment report released last week played a key role in changing market sentiment. The softer jobs data reduced expectations that the Federal Reserve would rush into raising interest rates again, leading some investors to reduce their bullish positions on the US Dollar.

Japanese Economic Data Offers Limited Help

Although the Yen has benefited from a softer US Dollar, Japan’s latest economic reports have done little to strengthen confidence in the country’s currency.

Fresh data showed that labor cash earnings slowed more than expected during May. Slower wage growth is an important factor because rising wages often support higher inflation and encourage central banks to tighten monetary policy. With wage growth losing momentum, expectations for aggressive policy changes from the Bank of Japan remain limited.

Household spending also remained under pressure. Although the decline was not as severe as analysts had expected, it marked another month of weaker consumer activity, highlighting the challenges facing Japan’s domestic economy.

Another closely watched indicator, the Leading Economic Index, also came in below expectations, suggesting that economic growth may continue to face obstacles in the months ahead.

Taken together, these reports have provided little reason for investors to become more optimistic about the Japanese Yen.

Markets Continue to Question the Bank of Japan

One of the biggest factors influencing the Japanese Yen remains the Bank of Japan’s monetary policy.

Even though the central bank has started moving away from years of extremely loose policy, investors remain uncertain about how quickly it will continue making changes. Many believe the pace of future tightening will remain gradual, limiting the Yen’s ability to stage a stronger recovery.

This cautious outlook is largely driven by concerns that Japan’s economy still requires supportive financial conditions. Policymakers are balancing the need to control inflation with the desire to avoid slowing economic growth too much.

As a result, many market participants remain hesitant to expect rapid policy shifts from the Bank of Japan.

Political Influence Adds More Uncertainty

Politics is also playing an important role in shaping expectations for Japan’s monetary policy.

Investors are aware that Prime Minister Sanae Takaichi has consistently supported maintaining accommodative economic policies that encourage growth. This has reinforced the belief that policymakers may prefer a cautious approach rather than implementing aggressive interest rate increases.

The combination of moderate economic growth, slowing wage gains, and political support for easier financial conditions has created uncertainty about how far the Bank of Japan is willing to tighten its policy in the near future.

Because of these factors, many traders continue to view any meaningful recovery in the Japanese Yen with caution.

Attention Shifts to Federal Reserve Meeting Minutes

With Tuesday’s economic calendar offering very few major releases, investor attention has shifted almost entirely toward Wednesday’s publication of the Federal Reserve’s latest meeting minutes.

The document will provide a more detailed look into the discussions held by policymakers during their previous meeting. Investors will carefully examine the minutes for clues about how Federal Reserve officials view inflation, employment, and the broader economic outlook.

Market participants will also look for any signs regarding future interest rate decisions. Even small changes in the language used by policymakers can influence expectations for monetary policy and create movement across global currency markets.

Because of this, many traders are avoiding aggressive positions before the report becomes available.

Investor Sentiment Remains Cautious

Recent market activity highlights how sensitive investors have become to economic data and central bank communication.

The weaker US employment figures have already encouraged many traders to reconsider expectations for future Federal Reserve actions. At the same time, uncertainty surrounding Japan’s policy direction has prevented investors from becoming fully confident in the Japanese Yen.

This combination has resulted in relatively cautious trading, with many participants waiting for stronger signals before making larger investment decisions.

Analysts believe that future currency movements will continue to depend heavily on incoming economic data and official comments from both the Federal Reserve and the Bank of Japan.

Global Central Bank Decisions Continue to Drive Currency Markets

The current environment serves as another reminder that central bank policies remain one of the strongest drivers of currency performance.

Whenever expectations surrounding interest rates change, investors quickly adjust their portfolios. Strong economic data can increase expectations of tighter monetary policy, while weaker reports often encourage hopes for a more patient approach.

In the case of Japan, the challenge remains balancing economic growth with inflation management. In the United States, investors are focused on whether inflation continues to slow enough for the Federal Reserve to maintain a more measured policy stance.

These ongoing developments will likely continue shaping market sentiment in the weeks ahead.

Summary

The Japanese Yen has managed a modest recovery as the US Dollar pauses following last week’s gains. However, weak domestic economic data and continued uncertainty surrounding the Bank of Japan’s policy outlook have limited the Yen’s broader strength.

Meanwhile, investors are largely staying on the sidelines as they await the release of the Federal Reserve’s meeting minutes. The document is expected to offer valuable insight into the central bank’s thinking and could influence expectations for future monetary policy. Until then, cautious trading is likely to remain the dominant theme across the currency market.

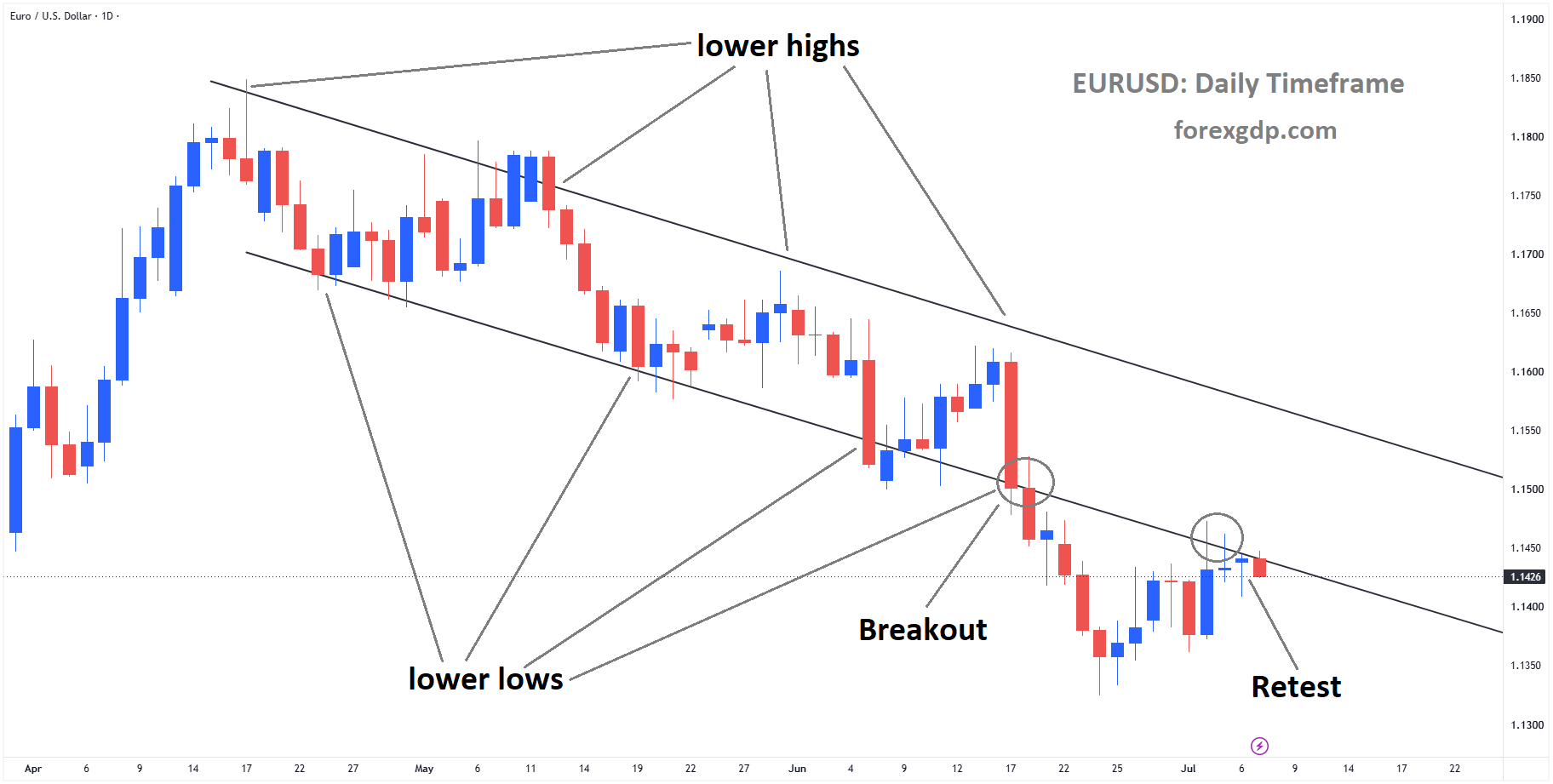

AUDUSD Under Pressure Following Softer June Employment Demand Data

The Australian Dollar started the week on a softer note after fresh domestic data pointed to a slowing economy and a cooling labor market. Recent reports showed that hiring activity continues to lose momentum, while inflation pressures appear to be easing. These developments have increased concerns that higher borrowing costs are beginning to affect business activity and consumer demand.

AUDUSD is moving in a descending channel, and the market has reached the lower high area of the channel

Although the Australian Dollar has faced renewed selling pressure, the downside could remain limited. Expectations that the Reserve Bank of Australia (RBA) may keep its policy firm to tackle inflation, along with a softer US Dollar, could help provide some support in the coming sessions.

Australian Labor Market Shows Signs of Slowing

One of the main reasons behind the Australian Dollar’s weakness is the latest employment-related data. Australia’s ANZ–Indeed Job Ads report revealed that job advertisements slipped by 0.2% in June compared with the previous month. This followed a stronger reading in May, making June the third monthly decline recorded so far this year.

Job advertisements are often viewed as an early indicator of hiring demand. When businesses reduce job postings, it may suggest that companies are becoming more cautious about expanding their workforce. This trend can eventually influence employment growth and consumer spending, both of which play an important role in the overall economy.

While the monthly decline was relatively modest, it adds to the broader picture of slowing economic momentum across Australia.

Hiring Demand Remains Higher Than Before the Pandemic

Despite the recent slowdown, economists point out that Australia’s labor market is not in a weak position overall. ANZ Economist Aaron Luk explained that job advertisements have fallen around 28% from the record highs seen in late 2022. However, they remain comfortably above the levels recorded before the COVID-19 pandemic.

This suggests that although hiring activity has cooled, businesses are still looking for workers at a healthier pace than in previous years. The labor market continues to show resilience even as economic conditions become more challenging.

However, Luk believes that hiring demand is likely to soften further in the coming months. Higher interest rates, slower housing activity, and ongoing global uncertainties are expected to reduce business confidence and hiring intentions.

Cooling Inflation Adds Another Layer to the Outlook

Alongside weaker employment data, fresh inflation figures also indicated that price pressures are beginning to ease.

Australia’s Melbourne Institute Monthly Inflation Gauge declined by 0.4% in June after falling 0.3% in May. This marked the second consecutive monthly decline, suggesting that inflation may be gradually moving in a more comfortable direction.

Lower inflation can provide some relief for households and businesses that have been dealing with rising living costs over the past few years. However, it also reflects slower demand across the economy, which may be another sign that tighter monetary policy is having the intended effect.

Investors continue to monitor inflation closely because it remains one of the most important factors influencing future decisions by the Reserve Bank of Australia.

China’s Inflation Data Remains in Focus

Another important factor influencing the Australian Dollar is the upcoming inflation data from China.

China is Australia’s largest trading partner, making its economic performance highly important for the Australian economy. Strong demand from China supports Australian exports, while weaker economic conditions can reduce demand for Australian goods and services.

Because of this close relationship, investors often react to Chinese economic data when evaluating the outlook for the Australian Dollar.

If China’s economy shows signs of improving, it could provide additional support for Australia’s export sector. On the other hand, weaker-than-expected figures could increase concerns about global demand and weigh further on market sentiment.

Reserve Bank of Australia Keeps Inflation Fight Alive

Even though recent economic data has softened, expectations surrounding the Reserve Bank of Australia continue to provide some support for the Australian Dollar.

Investors are still reviewing the RBA’s latest meeting minutes and recent comments from Governor Michele Bullock. The central bank has repeatedly emphasized that inflation remains a key concern despite signs of gradual improvement.

Officials have highlighted ongoing issues such as persistent inflation, strong domestic demand, and capacity constraints within the economy. These factors suggest that policymakers are not yet ready to declare victory over inflation.

As a result, many market participants continue to believe that the RBA could maintain a firm policy stance if inflation does not slow as expected.

A Softer US Dollar Could Offer Support

While domestic economic data has placed pressure on the Australian Dollar, external factors may help limit further weakness.

The US Dollar has recently shown signs of easing, allowing other major currencies to recover some lost ground. A weaker US Dollar often provides support for currencies like the Australian Dollar by making them relatively more attractive in global markets.

This balance between softer Australian economic data and a less dominant US Dollar has created a more mixed outlook for the currency.

Rather than moving in one clear direction, investors are weighing domestic economic weakness against the possibility that the RBA could continue maintaining tighter monetary policy.

Investors Remain Focused on Upcoming Economic Reports

Looking ahead, traders and investors are expected to closely monitor several important economic releases that could shape expectations for both Australia and global markets.

Inflation data, employment reports, and central bank communication will all play an important role in determining the future direction of monetary policy. Any signs that inflation remains persistent could strengthen expectations that interest rates may stay higher for longer.

At the same time, further evidence of slowing economic activity could increase concerns about growth and place additional pressure on the Australian Dollar.

The balance between controlling inflation and supporting economic growth remains one of the biggest challenges facing policymakers.

Final Summary

The Australian Dollar weakened after fresh economic data pointed to slower hiring activity and easing inflation pressures. Falling job advertisements and softer inflation readings suggest that higher borrowing costs are beginning to cool Australia’s economy, although the labor market remains stronger than it was before the pandemic.

At the same time, expectations that the Reserve Bank of Australia will continue focusing on inflation, combined with a softer US Dollar, may help prevent a deeper decline in the currency. Investors will now turn their attention to upcoming inflation data from China, future Australian economic releases, and signals from the RBA to better understand the path ahead for the Australian Dollar.

NZDUSD Retreats as Geopolitical Concerns Drive Demand for the US Dollar

The NZDUSD currency pair remained under pressure for a second straight session as investors continued to favor the US Dollar. Growing geopolitical concerns in the Middle East, combined with changing expectations for central bank policies, have shifted market sentiment and encouraged traders to move toward safer assets.

NZDUSD is falling from the retest area of the broken ascending channel

While the New Zealand Dollar is receiving some support from expectations surrounding the Reserve Bank of New Zealand (RBNZ), the broader strength of the US Dollar has made it difficult for the currency to gain momentum. At the same time, global investors are closely watching developments from both the US Federal Reserve and the RBNZ as they prepare for important policy decisions.

Renewed Middle East Tensions Lift Demand for the US Dollar

One of the biggest reasons behind the stronger US Dollar is the return of geopolitical uncertainty in the Middle East. Investors often seek safer currencies during periods of rising global tensions, and the US Dollar usually benefits from this shift.

Recent reports highlighted fresh security concerns in the Strait of Hormuz, one of the world’s most important shipping routes for energy supplies. According to Bloomberg, citing a US official, Iran launched at least two missiles toward commercial vessels traveling through the area.

Although two ships reportedly suffered serious damage, there were no reported casualties. In a separate incident, the UK Maritime Trade Operations confirmed that a tanker traveling south was hit by an unidentified projectile, causing a fire on board.

These developments have reminded investors that geopolitical risks remain high. Whenever uncertainty increases, traders often reduce exposure to riskier currencies and move toward assets viewed as more stable, providing additional support for the US Dollar.

Federal Reserve Expected to Stay Patient

Another important factor influencing the currency market is the changing outlook for the US Federal Reserve.

Recent economic data from the United States showed signs that the labor market is gradually cooling. Employment reports for April, May, and June revealed that fewer jobs were created than many economists had expected. This has reduced concerns that inflation could quickly accelerate again.

Because of these softer labor market figures, many investors now believe the Federal Reserve is likely to leave interest rates unchanged during both its July and September policy meetings.

The expectation of steady interest rates reflects the belief that the central bank has enough time to observe incoming economic data before deciding whether additional policy adjustments are necessary.

A more cautious Federal Reserve reduces uncertainty in financial markets and has helped maintain confidence in the US Dollar even without additional policy tightening.

Lower Oil Prices Ease Inflation Concerns

Oil prices have also played an important role in shaping investor expectations.

Global oil markets recently experienced a notable decline following increased production from OPEC+ members and signs of improving relations between the United States and Iran. Higher oil supply and reduced geopolitical fears surrounding energy production have eased pressure on fuel prices.

Lower energy costs can help reduce overall inflation because transportation, manufacturing, and many consumer goods become less expensive when oil prices fall.

As inflation concerns ease, central banks generally face less pressure to tighten monetary policy aggressively. This has contributed to expectations that the Federal Reserve can afford to remain patient while monitoring future economic developments.

Although falling oil prices often support global economic growth, they have not been enough to weaken the US Dollar, especially as investors continue to prioritize safety amid ongoing geopolitical uncertainty.

Focus Turns to the Reserve Bank of New Zealand

Attention is also centered on the Reserve Bank of New Zealand, which is expected to announce its latest monetary policy decision.

Economists at ING believe the central bank may deliver a 25-basis-point interest rate increase, raising the official cash rate to 2.50%.

This expected move is being described as an “insurance” rate hike rather than the beginning of a lengthy tightening cycle. The goal would likely be to provide additional support for price stability while keeping future policy options flexible.

Even if the rate increase takes place, analysts do not expect it to trigger a major rally in the New Zealand Dollar.

Instead, many believe it could be a single adjustment rather than the start of several consecutive increases. If investors view the move as a one-time decision, any positive impact on the NZD may prove limited.

Why the New Zealand Dollar Remains Under Pressure

Several factors continue to challenge the New Zealand Dollar despite expectations of higher domestic interest rates.

Global investors remain cautious due to rising geopolitical tensions. In uncertain periods, demand usually shifts toward safer currencies such as the US Dollar instead of smaller, growth-sensitive currencies like the New Zealand Dollar.

In addition, expectations that the RBNZ may only deliver one rate increase reduce enthusiasm among investors looking for stronger long-term returns from the currency.

The combination of a resilient US Dollar, cautious market sentiment, and limited expectations for future New Zealand policy tightening has kept pressure on NZDUSD.

Investors Watching Central Banks Closely

The coming days will be particularly important for currency markets.

The RBNZ’s policy announcement will provide valuable insight into how officials view inflation, economic growth, and future interest rate decisions. Investors will carefully examine not only the rate decision itself but also the accompanying statement for clues about what may happen next.

Meanwhile, traders will continue monitoring comments from Federal Reserve officials for any changes in their outlook on inflation, employment, and monetary policy.

Economic reports from both countries will remain important in shaping expectations for future central bank actions.

Global Events Continue to Influence Currency Markets

Currency markets rarely move because of a single event. Instead, they react to a combination of economic data, central bank decisions, and international developments.

The latest geopolitical tensions have reminded investors that unexpected global events can quickly influence financial markets. At the same time, changing expectations for interest rates continue to shape demand for major currencies around the world.

For traders and investors, staying informed about both political events and economic trends remains essential, as these factors often work together to determine market direction.

Summary

NZDUSD remains under pressure as the US Dollar continues to benefit from renewed geopolitical tensions and cautious investor sentiment. Fresh incidents in the Strait of Hormuz have increased demand for safe-haven assets, while expectations that the Federal Reserve will keep interest rates unchanged have supported confidence in the US currency.

At the same time, attention is turning toward the Reserve Bank of New Zealand, with many analysts expecting a modest interest rate increase. However, because this move is widely viewed as a possible one-time adjustment, its ability to provide lasting support for the New Zealand Dollar appears limited. As central bank decisions and global events continue to unfold, investors will remain focused on the factors shaping the outlook for both currencies.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!