The British Pound showed signs of recovery at the start of the week, rising by about 0.75% against the US Dollar. This move offered some relief after a period of steady decline. However, while the rebound may look encouraging on the surface, the broader outlook remains uncertain. Several major economic events scheduled over the next few days are likely to play a key role in shaping the direction of the currency pair.

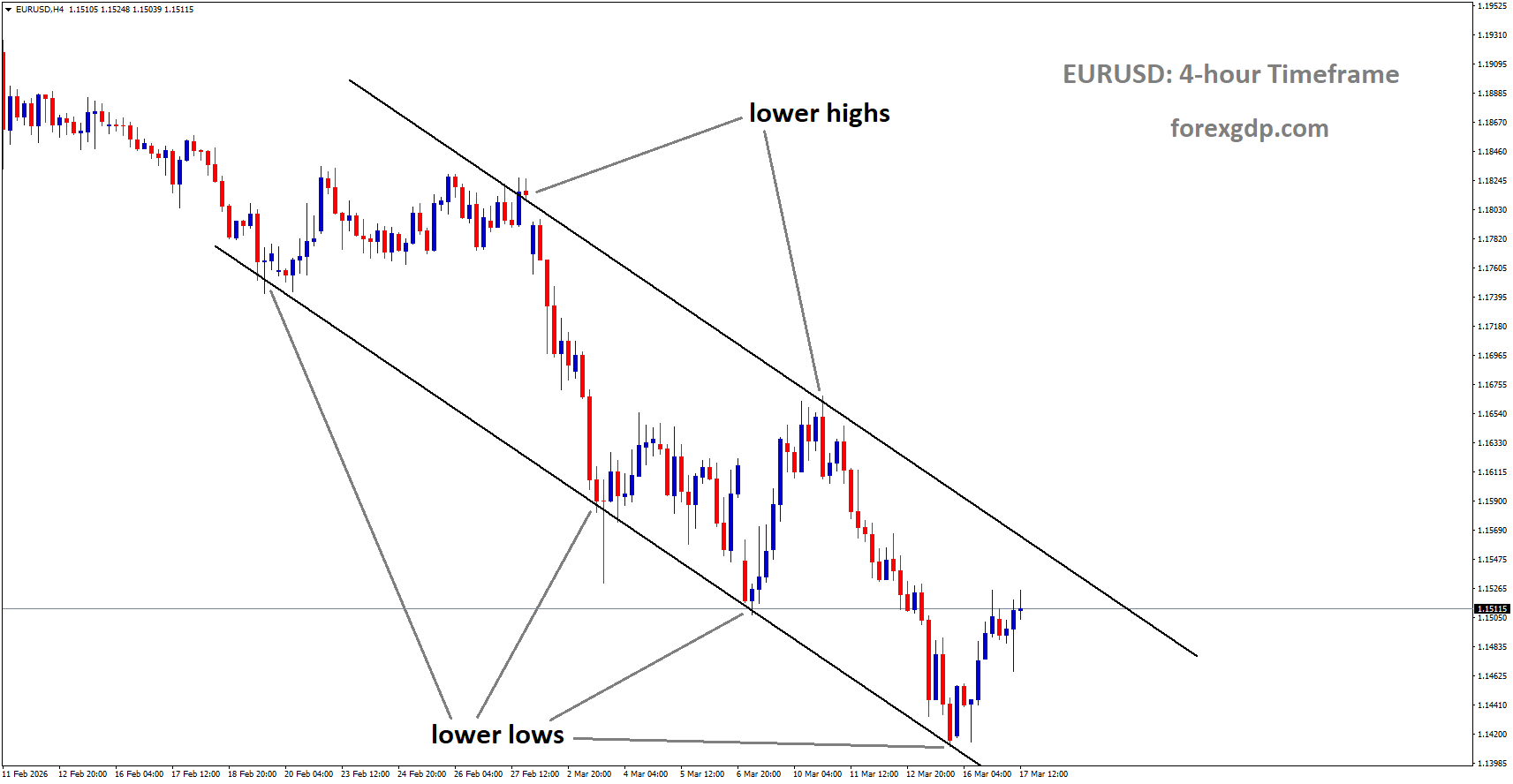

GBPUSD is moving in a descending channel, and the market has rebounded from the lower low area of the channel

Despite the recent uptick, the Pound is still under pressure from earlier losses. Traders and investors are now closely watching central bank decisions and economic data releases that could either support further gains or push the currency lower again.

Recent Movement in GBP/USD

The GBP/USD pair started the week on a stronger note, bouncing back from its previous low near 1.3220. By the end of Monday’s session, it had climbed above the 1.3300 level. This rise followed a stretch of weakness and appears to be more of a temporary correction rather than a clear shift in trend.

Over the past several weeks, the pair has been moving downward from its late-January peak around 1.3870. This broader decline suggests that sellers are still in control. Even though Monday’s movement was positive, it has not yet challenged key levels that would signal a stronger recovery.

For now, the burden remains on buyers to prove that this rebound can continue. Without strong support from economic data or policy signals, the upward move may fade quickly.

Key Events That Could Shape the Market

The coming days are packed with important events that could influence the direction of both the Pound and the US Dollar. These include decisions from major central banks and fresh economic data from the United Kingdom.

Federal Reserve Decision

The first major event is the US Federal Reserve’s interest rate decision. Markets widely expect the Fed to keep its rate unchanged at 3.75%. However, the real focus will be on the central bank’s outlook and communication.

Investors will pay close attention to the Summary of Economic Projections and comments from Federal Reserve Chair Jerome Powell. These elements provide insight into how policymakers view inflation, economic growth, and future rate changes.

If the Fed signals a more aggressive stance on keeping interest rates high, the US Dollar could strengthen. This would likely put renewed pressure on GBP/USD, potentially reversing the recent gains. On the other hand, a softer tone could weaken the Dollar and give the Pound more room to recover.

Bank of England Meeting

The next key event is the Bank of England’s policy decision. Like the Fed, the BoE is also expected to keep its interest rate steady at 3.75%. However, the details behind the decision are just as important as the outcome itself.

One area of focus is the voting pattern within the Monetary Policy Committee. Recent expectations suggest a shift toward a less dovish stance compared to earlier meetings. This means fewer members are likely to support rate cuts, indicating that the central bank may not be in a hurry to ease monetary policy.

A less dovish outlook could provide some support to the Pound. It would signal that the BoE remains cautious about reducing borrowing costs, especially if inflation risks are still present. However, if the tone is softer than expected, it could weaken the currency.

UK Employment Data in Focus

Alongside the BoE decision, the UK will release its latest employment data. This report is another critical piece of the puzzle, offering insight into the health of the labor market.

Unemployment Rate

The unemployment rate, measured by the International Labour Organization (ILO), is expected to remain steady at 5.2%. A stable unemployment rate suggests that the job market is holding up, which is generally positive for the economy.

If the actual figure matches expectations, it may not have a strong impact on the Pound. However, any unexpected rise in unemployment could raise concerns about economic weakness and weigh on the currency.

Wage Growth Trends

Another key component of the report is wage growth, particularly earnings that include bonuses. Forecasts suggest that this figure will slow down slightly, easing to 3.9% year-on-year from 4.2%.

Wage growth is closely watched by central banks because it can influence inflation. Slower wage growth may reduce inflationary pressure, giving the BoE less reason to keep interest rates high for an extended period.

If the data confirms a slowdown in wages, it could limit the Pound’s ability to gain further strength. On the other hand, stronger-than-expected wage growth could support the currency by reinforcing the case for maintaining current interest rates.

What This Means for the Pound

The Pound’s recent recovery is a welcome change for investors, but it does not yet signal a full turnaround. The overall trend still points downward, and the current bounce appears to be driven more by temporary factors than a lasting shift.

The next few days will be crucial. The combination of central bank decisions and economic data will likely determine whether the Pound can build on its recent gains or resume its decline.

Several factors are working against a strong recovery. These include ongoing concerns about economic growth and uncertainty around future monetary policy. At the same time, any weakness in the US Dollar could provide short-term support.

Market Sentiment and Expectations

Market sentiment remains cautious. Traders are not yet convinced that the Pound has enough strength to reverse its broader downtrend. Instead, many are waiting for clearer signals from policymakers and economic indicators.

The Fed’s stance on interest rates will be particularly important. A strong Dollar driven by a hawkish Fed could overshadow any positive developments in the UK. Conversely, a softer Dollar could allow the Pound to stabilize or even extend its recovery.

At the same time, the BoE’s messaging will play a key role. If the central bank shows confidence in the economy and signals patience on rate cuts, it could boost confidence in the Pound.

Final Summary

The Pound Sterling has managed to regain some ground, but the recovery remains fragile. The recent rise appears to be more of a pause in the broader downward trend rather than a clear reversal.

With major events lined up, including decisions from the Federal Reserve and the Bank of England, as well as important UK employment data, the market is entering a critical phase. Each of these factors has the potential to shift sentiment and drive the next move in GBP/USD.

For now, caution remains the dominant theme. The Pound’s direction will depend heavily on how these events unfold and whether they provide enough support to sustain the current rebound.

USDJPY Ends Winning Run as Pullback Breaks Recent Momentum

The Japanese Yen showed signs of strength at the start of the week, benefiting from a softer US Dollar. After several days of gains in the USD/JPY pair, the trend paused as the currency pair pulled back slightly. This shift comes at an important time, with major economic events lined up in both Japan and the United States that could shape the direction of the market in the coming days.

USDJPY is moving in an uptrend channel, and the market has reached the higher low area of the channel

Recent Movement in USD/JPY

The USD/JPY pair experienced a small decline of around 0.4% on Monday. This drop ended a four-day winning streak that had pushed the pair to multi-week highs. The exchange rate moved back toward the 159.00 level, showing a pause in upward momentum.

Over the past few weeks, the pair had been climbing steadily from its February low near 152.10. This upward movement reflected a strong US Dollar and a relatively weaker Yen. However, the recent pullback suggests that buyers may be losing some momentum, at least in the short term.

The intraday high of 159.75 failed to attract strong follow-up buying. This is often seen as a sign that traders are becoming cautious at higher levels. Even so, the broader trend remains upward, as the pair has continued to form higher lows since February.

Still, the current levels appear somewhat stretched. When a currency pair rises too quickly, it often leads to a temporary pause or correction, as traders reassess their positions.

Bank of Japan Policy Outlook

One of the key factors influencing the Yen this week is the upcoming policy decision from the Bank of Japan (BoJ). The central bank is expected to keep its policy rate unchanged at 0.75% during Thursday’s meeting.

Japan has maintained relatively low interest rates compared to other major economies, especially the United States. This difference in rates has made the Yen less attractive for investors seeking higher returns, which has contributed to its weakness in recent months.

However, there is growing attention on inflation in Japan. Price levels have been running above the BoJ’s 2% target, raising questions about whether the central bank might adjust its policy in the future.

Focus on Governor Ueda’s Comments

While the rate decision itself may not bring surprises, the market will closely watch the press conference by BoJ Governor Kazuo Ueda. His comments could provide clues about the future direction of monetary policy.

If there are any hints about tightening policy or raising rates later this year, it could support the Yen. On the other hand, if the BoJ signals that it will remain cautious and maintain its current stance, the Yen may struggle to gain strength.

Investors are particularly interested in the timing of any potential policy changes. Even small shifts in expectations can have a noticeable impact on currency markets.

Japan’s Trade Data in Focus

Another important event for Japan this week is the release of February trade balance data. This report will provide insight into the country’s export and import activity.

In the previous reading, Japan’s exports showed strong growth, rising by 16.8% compared to the same period last year. This rebound was seen as a positive sign for the economy, especially after earlier periods of weaker performance.

If the upcoming data continues to show strong export growth, it could support the Yen by highlighting the strength of Japan’s external sector. A healthy trade balance often reflects strong demand for a country’s goods and services, which can boost its currency.

However, if the data disappoints, it may add pressure on the Yen, especially at a time when global economic conditions remain uncertain.

US Dollar Under Pressure

While developments in Japan are important, the recent movement in USD/JPY has also been influenced by changes in the US Dollar.

On Monday, the Dollar faced some broad weakness. One contributing factor was easing tensions in the Strait of Hormuz, which reduced demand for safe-haven assets like the US Dollar. When global risks decline, investors often move away from safe currencies and look for higher returns elsewhere.

At the same time, economic data from the United States added to the softer tone. The March reading of the New York Empire State Manufacturing Index came in at –0.2, below expectations of 3.2. This weaker-than-expected result suggested that manufacturing activity is not as strong as hoped.

Although this data point alone is not enough to change the overall outlook, it added some pressure on the Dollar in the short term.

Federal Reserve Decision Ahead

The main event for the US Dollar this week is the Federal Reserve’s policy decision, scheduled for Wednesday. The Fed is widely expected to keep its interest rate steady at 3.75%.

Even though no rate change is expected, the focus will be on the central bank’s updated economic projections and guidance for future policy.

Importance of the Rate Path Outlook

The Fed’s outlook on future interest rates plays a major role in currency markets. If policymakers संकेत that rates will stay higher for longer, it could support the Dollar. On the other hand, any hints of future rate cuts may weaken it.

The Summary of Economic Projections (SEP) will provide insight into how Fed officials view inflation, growth, and the labor market. These forecasts often shape market expectations and influence currency movements.

For the USD/JPY pair, the interest rate gap between the US and Japan remains a key factor. As long as US rates are significantly higher, the Dollar tends to have an advantage. However, any shift in this outlook could lead to changes in the trend.

What This Means for the Yen and Dollar

The current situation highlights a balance of forces affecting both currencies. On one side, the Yen is gaining some support from Dollar weakness and attention on Japan’s economic data. On the other side, the overall trend still favors the Dollar due to higher US interest rates.

The upcoming central bank decisions will be critical in determining the next move. If the Fed maintains a strong stance while the BoJ remains cautious, the USD/JPY pair could continue to stay elevated. However, any surprises from either side could lead to increased volatility.

Traders and investors are likely to remain cautious ahead of these events, which may explain the recent pause in the pair’s upward movement.

Summary

The Japanese Yen has shown modest strength as the US Dollar weakened slightly at the start of the week. After a strong upward run, the USD/JPY pair has taken a step back, reflecting a pause in momentum.

Attention is now focused on key events, including the Bank of Japan’s policy decision, Japan’s trade data, and the Federal Reserve’s rate announcement. While the BoJ is expected to keep rates unchanged, its future outlook remains an important factor for the Yen.

At the same time, the US Dollar faces mixed signals from economic data and shifting global conditions. The Fed’s guidance on future rates will play a major role in shaping market expectations.

With both central banks in focus, the coming days could bring important clues about the direction of the currency pair.

USDCHF Remains Range-Bound Around 0.7900 Before Crucial Fed and SNB Updates

The USD/CHF currency pair is currently moving sideways, reflecting a balance between competing global forces. While the US Dollar has shown moments of strength, the Swiss Franc continues to benefit from its reputation as a safe-haven asset. Investors are closely watching central bank decisions, geopolitical developments, and inflation concerns, all of which are shaping the direction of this currency pair.

USDCHF is moving in an uptrend channel, and the market has fallen from the higher high area of the channel

This delicate balance highlights how sensitive financial markets are to both economic signals and global uncertainty.

Fed Policy Outlook Keeps Markets on Edge

One of the main factors influencing USD/CHF is the expected decision from the US Federal Reserve. Market participants widely believe that the Fed will keep interest rates unchanged in the near term. This would mark another pause following a period of policy adjustments aimed at managing inflation and supporting economic stability.

The expectation of stable interest rates comes at a time when inflation concerns are still present. Rising oil prices, partly driven by tensions in the Middle East, have added pressure to the global economy. Higher energy costs can lead to increased inflation, making it harder for central banks to justify lowering interest rates quickly.

Because of this, the US Dollar has managed to find some support. When interest rates remain steady or higher for longer, it often strengthens the currency, as investors seek better returns on dollar-based assets.

However, the situation is not entirely straightforward. While the Dollar benefits from these expectations, it also faces pressure from changing global conditions.

Oil Prices and Geopolitical Developments Shape Sentiment

Global oil markets have played a major role in influencing investor sentiment. Initially, concerns about supply disruptions pushed oil prices higher. This was largely due to tensions in the Middle East, a region that plays a key role in global energy supply.

However, recent developments have helped calm some of those fears. Reports that oil tankers are safely passing through important shipping routes have eased worries about immediate disruptions. In addition, major economies are expected to release petroleum reserves if needed, which could help stabilize supply.

These factors have reduced some of the urgency in the market, leading to a slight decline in oil prices. As a result, the US Dollar has faced some pressure, since part of its recent strength was tied to rising inflation expectations linked to higher energy costs.

Political actions have also influenced market confidence. Efforts to keep vital trade routes open and maintain the flow of oil have helped prevent panic in global markets. While uncertainty remains, these steps have provided some reassurance to investors.

Still, the overall situation remains fragile. Any sudden escalation in geopolitical tensions could quickly change the outlook and bring volatility back into the market.

Swiss Franc Gains Support from Safe-Haven Demand

The Swiss Franc continues to attract attention during times of uncertainty. Known for its stability, the Franc often strengthens when investors become cautious about global risks.

Ongoing geopolitical tensions, especially in the Middle East, have kept demand for safe-haven assets alive. Even when markets appear calm on the surface, underlying risks can drive investors toward currencies like the Swiss Franc.

This steady demand has helped limit gains in USD/CHF, keeping the pair from moving significantly higher. Whenever uncertainty rises, the Franc tends to benefit, acting as a counterbalance to the US Dollar.

At the same time, Switzerland’s economic environment also plays a role. The Swiss National Bank is expected to maintain a very low interest rate policy, which typically would weaken a currency. However, in the case of the Franc, its safe-haven appeal often outweighs this factor.

This unique combination makes the Swiss Franc one of the most resilient currencies during uncertain times.

SNB Intervention Limits Franc Strength

While the Swiss Franc is supported by global uncertainty, its upward movement is not unlimited. The Swiss National Bank (SNB) has made it clear that it is prepared to step in if the currency becomes too strong.

A stronger Franc can create challenges for the Swiss economy. It can make exports more expensive and reduce competitiveness in international markets. Additionally, excessive currency strength can lead to deflation, where prices fall instead of rise, which can slow economic growth.

To prevent these issues, the SNB has signaled its willingness to intervene in foreign exchange markets when necessary. This means selling the Franc or taking other actions to weaken it if it appreciates too much.

This intervention strategy creates a natural cap on how strong the Franc can become. Even if global risks increase, traders remain cautious about pushing the currency too high, knowing that the central bank may act.

As a result, USD/CHF remains in a narrow range, with both currencies facing their own limitations.

A Market Caught Between Stability and Uncertainty

The current behavior of USD/CHF reflects a broader theme in global markets: a constant tug-of-war between stability and uncertainty.

On one side, expectations of steady US interest rates provide support for the Dollar. On the other, geopolitical risks and cautious investor sentiment continue to favor the Swiss Franc.

At the same time, easing concerns around oil supply and efforts by governments to maintain stability have reduced some of the immediate pressure on markets. This has prevented sharp movements in either direction.

Central bank policies also play a key role. While the Federal Reserve appears to be holding steady, the Swiss National Bank is actively monitoring currency strength and remains ready to act if needed.

All these factors combine to create a market environment where large moves are limited, and price action remains relatively stable.

Key Drivers to Watch Moving Forward

Looking ahead, several factors will continue to influence USD/CHF:

Central Bank Decisions

Any changes in tone or policy from the Federal Reserve or the Swiss National Bank could quickly impact the pair. Even small signals can shift market expectations.

Geopolitical Developments

Events in the Middle East and other regions will remain a major driver of safe-haven demand. Escalation or easing of tensions can quickly change investor behavior.

Inflation Trends

Oil prices and broader inflation data will continue to shape expectations around interest rates, especially in the United States.

Market Sentiment

Overall risk appetite plays a big role. When investors feel confident, the Dollar may gain strength. When uncertainty rises, the Swiss Franc often benefits.

Final Summary

USD/CHF is currently moving within a tight range, reflecting a balance between competing global forces. The US Dollar is supported by expectations of stable interest rates, while the Swiss Franc benefits from ongoing demand as a safe-haven currency.

At the same time, easing oil market concerns and efforts to maintain global stability have reduced extreme market reactions. However, risks remain, particularly from geopolitical tensions and inflation pressures.

The Swiss National Bank’s willingness to intervene adds another layer of complexity, preventing the Franc from strengthening too much. Meanwhile, the Federal Reserve’s cautious approach keeps investors focused on future policy signals.

As global conditions continue to evolve, USD/CHF is likely to remain sensitive to both economic data and geopolitical developments, making it an important pair to watch in the coming days.

USDCAD Edges Lower as Canada’s Price Growth Slows Ahead of BoC Meeting

The USD/CAD currency pair started the week on a weaker note, with the Canadian Dollar gaining ground against a softer US Dollar. While economic data from Canada showed easing inflation, markets remained relatively calm, as global geopolitical tensions continued to dominate investor sentiment.

USDCAD is moving in a descending channel, and the market has reached the lower high area of the channel

At the time of writing, USD/CAD is hovering around the 1.3659 level, stepping back after a strong three-day rally that had pushed it to a two-week high. Meanwhile, the US Dollar Index, which tracks the performance of the Greenback against a group of major currencies, has eased slightly after recently touching its highest level in ten months.

Canadian Dollar Finds Support Despite Soft Inflation Data

Recent inflation figures from Canada indicate that price pressures are cooling, but the reaction in currency markets has been limited. The Consumer Price Index (CPI) rose by 0.5% in February compared to the previous month. Although this increase shows a recovery from January’s flat reading, it came in slightly below expectations.

On a yearly basis, inflation slowed to 1.8%, down from 2.3% previously. This reading is just under the market forecast and suggests that inflation is moving closer to the Bank of Canada’s target of around 2%.

Core Inflation Shows Mixed Signals

Monthly Growth Picks Up

Core inflation, which removes volatile items like food and energy, increased by 0.4% month-over-month. This marks a faster pace compared to January, when it rose by 0.2%.

Annual Rate Continues to Ease

However, on an annual basis, core inflation slowed to 2.3% from 2.6%. This mixed picture suggests that while short-term price pressures may be rising slightly, the broader trend still points toward moderation.

Overall, the data indicates that inflation is gradually stabilizing. This gives the Bank of Canada some room to remain patient when it comes to adjusting interest rates.

Bank of Canada Likely to Stay Cautious

With inflation easing and staying close to target levels, expectations are growing that the Bank of Canada will keep its interest rates unchanged in the near term. The central bank is widely expected to hold its benchmark rate steady at 2.25% in its upcoming policy decision.

Why Policymakers May Wait

There are several reasons why the Bank of Canada may choose a cautious approach:

-

Inflation is not rising sharply, reducing the urgency for tightening policy

-

Economic conditions remain uncertain

-

Global risks continue to influence market behavior

A recent survey of economists shows that most expect the central bank to keep rates unchanged for an extended period, possibly into 2026.

Weak Jobs Data Adds Another Layer of Uncertainty

While inflation data suggests stability, the labor market tells a different story. Recent employment figures have disappointed, raising concerns about the strength of the Canadian economy.

If job growth continues to weaken, the Bank of Canada may need to rethink its current policy stance. A softer labor market could push the central bank toward a more supportive approach, especially if economic activity slows further.

This creates a delicate balance for policymakers, who must weigh stable inflation against potential risks to growth.

Oil Prices Create a Policy Dilemma

Rising Oil Prices Support the Economy

One of the key factors influencing Canada’s outlook is the recent rise in oil prices. Supply disruptions, particularly through the Strait of Hormuz, have pushed crude prices higher.

For Canada, this can be a positive development. As a major oil exporter, higher energy prices can boost national income and support economic growth.

But Inflation Risks Remain

At the same time, rising oil prices can increase inflation by raising the cost of goods and transportation. This puts the Bank of Canada in a difficult position.

On one hand, stronger oil prices help the economy. On the other hand, they can push inflation higher, which may require tighter monetary policy.

Given these opposing forces, the central bank is likely to adopt a “wait-and-see” approach, carefully monitoring how these trends evolve.

Geopolitical Tensions Take Center Stage

Beyond economic data, global geopolitical developments are playing a major role in shaping market sentiment. The ongoing tensions related to the US-Iran conflict continue to create uncertainty across financial markets.

Investors are closely watching these developments, as they have the potential to impact:

This uncertainty is one of the main reasons why markets have shown a muted reaction to recent economic data. Traders are more focused on global risks than on short-term indicators.

US Dollar Weakens Ahead of Federal Reserve Decision

The US Dollar has also come under pressure, contributing to the decline in USD/CAD. After reaching a recent high, the Greenback has eased slightly as investors reassess the outlook for US monetary policy.

Federal Reserve Expected to Hold Rates Steady

The Federal Reserve is widely expected to keep interest rates unchanged in its upcoming meeting, with the benchmark rate likely to remain within the current range.

However, the key focus will be on the central bank’s forward guidance. Investors are eager to understand how policymakers view the economy and whether any changes in policy are expected in the coming months.

Market Focus on Future Signals

Several elements will be closely watched:

-

Comments from Federal Reserve Chair Jerome Powell

-

Updated economic projections

-

The “dot plot,” which shows individual policymakers’ rate expectations

Recent shifts in market expectations suggest that traders are becoming less confident about potential rate cuts this year. This change in outlook is influencing the US Dollar’s performance.

Final Summary

The USD/CAD pair is currently under pressure as the Canadian Dollar benefits from a softer US Dollar and supportive oil prices. While Canada’s latest inflation data points to easing price pressures, it has not significantly moved markets, as global geopolitical tensions remain the dominant factor.

The Bank of Canada appears set to maintain its current policy stance, balancing stable inflation with concerns about weaker employment data. At the same time, rising oil prices add both opportunity and risk, creating a complex environment for decision-makers.

Meanwhile, attention is also on the US Federal Reserve, where investors are looking for clues about the future direction of interest rates. As global uncertainty continues, currency movements are likely to remain sensitive to both economic data and geopolitical developments.