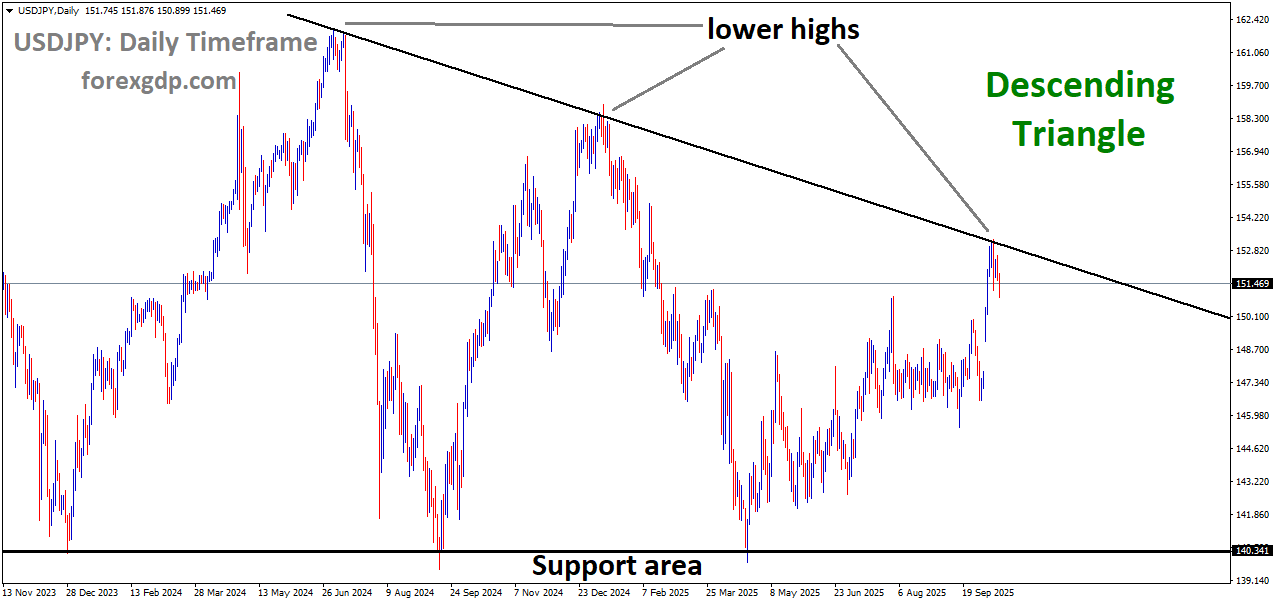

USDJPY is moving in a descending triangle pattern, and the market has reached the lower high area of the pattern

USDJPY Drops Sharply as Fed’s Dovish Outlook Weakens the Dollar

The USD/JPY pair has taken a sharp downturn, hovering close to the 151.00 mark, as the US Dollar continues to lose strength against other major currencies. With the Federal Reserve signaling possible interest rate cuts and Japan experiencing political turbulence, traders are keeping a close eye on how both economic and political factors may influence the market’s next direction.

The Dollar’s Struggle and Fed’s Soothing Tone

The US Dollar has been losing momentum lately, with its overall performance dipping across global markets. The reason behind this isn’t just technical—it’s largely about changing sentiment and expectations from the Federal Reserve.

After years of battling inflation with aggressive rate hikes, the Fed has now shifted its stance toward supporting growth. In September, it introduced its first rate cut of the year, trimming rates by 25 basis points. This move signaled a new phase—one where the focus is on sustaining economic stability rather than tightening financial conditions further.

Traders now believe that this is only the beginning. Market participants expect two more rate cuts by the end of the year, possibly totaling another 50 basis points. These expectations have caused investors to lose some faith in the Dollar’s short-term strength.

Fed Officials Voice Concern Over Labor Market Weakness

Adding to this sentiment, several key Federal Reserve officials, including Chair Jerome Powell, have recently expressed concern about the US labor market. Powell mentioned that “downside risks to the job market have increased,” hinting that the central bank is paying close attention to employment conditions.

While he didn’t directly confirm more rate cuts, other Fed members, like Governor Michelle Bowman and Boston Fed President Susan Collins, have been more open about their support for further easing measures. This has further weakened the Dollar as markets interpret such statements as confirmation that the Fed will continue to take a dovish stance.

In simple terms, when the Fed cuts interest rates or hints at doing so, it makes the Dollar less attractive to investors because returns on US-based assets fall. That’s exactly what’s happening now—traders are moving away from the Dollar, and the Japanese Yen is one of the beneficiaries.

Japan’s Political Scene Adds to Market Jitters

While the US economy is dealing with monetary policy shifts, Japan is facing its own set of challenges—this time in the political arena. Political uncertainty often affects currency strength, and the Yen’s recent movement reflects that.

Reports from Kyodo suggest that Japan’s ruling and opposition parties have been struggling to agree on a date for selecting the next Prime Minister. The vote, which was initially expected to take place on October 21, may now be delayed due to disagreements among party leaders.

Leadership Conflicts Within the LDP

The situation has been made worse by recent internal conflict within the Liberal Democratic Party (LDP), Japan’s long-standing ruling party. The abrupt breakup of the LDP last week has left its leader, Sanae Takaichi, depending heavily on support from other political groups.

This internal turmoil has raised concerns among investors who prefer political stability, especially in an economy like Japan’s, where government policy plays a huge role in managing monetary and fiscal balance. When political uncertainty rises, investors often seek safety in the Yen itself, which tends to gain value during such times as a “safe haven” asset.

How the Two Forces Interact: Dollar Weakness Meets Yen Strength

The interesting part about the USD/JPY pair right now is that both currencies are being influenced by completely different factors. The Dollar is weakening because of softer Fed policies and growing concern about the labor market. The Yen, on the other hand, is finding strength not because of economic growth but due to uncertainty and risk aversion linked to Japan’s political drama.

In the world of currency trading, these two forces can create powerful swings. When the US Dollar drops while the Yen strengthens, the result is exactly what we’re seeing—a noticeable fall in the USD/JPY exchange rate.

Traders who follow global trends know that this combination often leads to high volatility. In simple terms, it means prices can move rapidly as investors react to news from either side—whether it’s a Fed speech, a new employment report, or a headline from Tokyo’s political scene.

What Traders and Investors Are Watching Next

Looking ahead, the focus will remain on two key areas: the Fed’s next decisions and Japan’s political outcome.

On the US side, upcoming economic data—especially job market numbers—will play a major role in shaping expectations. If employment data shows more weakness, it could increase the likelihood of additional rate cuts, putting further downward pressure on the Dollar.

In Japan, much will depend on how quickly the leadership situation stabilizes. A prolonged period of political uncertainty could shake investor confidence, even though the Yen often gains temporarily from such instability. Over the long term, markets prefer clarity and continuity, and any clear resolution in Japan’s political structure could shift sentiment again.

A Broader View: Global Implications of Fed and Japan Dynamics

The developments in both countries don’t exist in isolation—they have ripple effects across global markets.

When the US Dollar weakens, commodities priced in Dollars, such as oil and gold, often experience price adjustments. Emerging markets can also feel the impact since a softer Dollar can make their currencies stronger and capital inflows more attractive.

Similarly, the Japanese Yen plays a critical role in global carry trades, where investors borrow in low-interest-rate currencies (like the Yen) to invest in higher-yielding ones. If Japan’s political or economic situation changes significantly, it could disrupt these investment strategies worldwide.

In essence, what’s happening between the USD and JPY isn’t just about one currency pair—it’s a reflection of how monetary and political forces across two of the world’s largest economies are shaping global financial sentiment.

Final Summary

The recent fall in USD/JPY reflects a combination of weakening confidence in the US Dollar and increasing demand for the Japanese Yen amid political uncertainty in Japan. The Federal Reserve’s cautious stance, centered on labor market risks and potential rate cuts, has made investors reassess their Dollar holdings. Meanwhile, Japan’s unsettled political scene, marked by leadership disputes and delays in choosing a new Prime Minister, has fueled safe-haven buying of the Yen.

As a result, the USD/JPY pair’s downward movement is less about short-term technical shifts and more about deeper economic and political currents influencing both nations. The coming weeks will likely bring more clarity—especially as the Fed’s next steps and Japan’s political outcome unfold. Until then, traders should stay alert, as this pair could remain highly sensitive to every statement and decision coming from Washington or Tokyo.

EURUSD Finds Support as Eurozone Factories Show Signs of Stability

The Euro continues to hold its ground against the US Dollar this week, maintaining gains around the 1.1650 level after rebounding from recent lows. Despite a slight dip in industrial activity across the Eurozone, the shared currency remains supported by a softer US Dollar and renewed investor confidence. With the Federal Reserve hinting at potential rate cuts, the broader market tone has turned optimistic, allowing the Euro to stay resilient amid global uncertainty.

A Fresh Wave of Confidence in the Eurozone

Recent economic data from Eurostat revealed that Eurozone Industrial Production slipped by 1.2% in August. While this marks a decline, it was far less severe than many economists expected. The drop mainly came from reduced output in capital and consumer goods, but investors took comfort in the fact that the numbers were still better than feared.

EURUSD is moving in a box pattern, and the market has reached the resistance area of the pattern

In fact, this moderate contraction followed a 0.5% gain in July, showing that while industrial momentum has slowed, the region is not facing a dramatic downturn. The Eurozone economy continues to demonstrate stability, particularly as inflation concerns ease and demand within the bloc remains consistent. This relatively mild slowdown has encouraged investors to stay optimistic about the Euro’s medium-term outlook.

The Fed’s Dovish Tone and Its Ripple Effect

Federal Reserve Chair Jerome Powell’s latest remarks have played a major role in shaping the current market sentiment. On Tuesday, Powell shifted focus away from inflation and toward the weakening US labor market, signaling that the central bank is prepared to implement further rate cuts if necessary.

This statement was interpreted as a strong hint that the Fed may reduce interest rates again during its upcoming meeting in late October. Powell also mentioned that the Fed is nearing the end of its bond-reduction process, often referred to as the “Quantitative Tightening” program. This move suggests a potential easing of financial conditions, which tends to weaken the US Dollar and strengthen other major currencies like the Euro.

Market Expectations and Investor Reaction

Following Powell’s speech, the CME Group’s FedWatch Tool showed that traders are now almost fully pricing in a 25-basis-point rate cut in October. Moreover, the likelihood of another cut in December jumped significantly, climbing to nearly 95%. This clear shift in monetary policy expectations has triggered a broad retreat in the Dollar, paving the way for the Euro to advance.

The anticipation of lower US interest rates has also encouraged risk-taking in financial markets. Investors have returned to equities, reducing their demand for the safe-haven Dollar. As a result, the Euro and other major currencies have found fresh support, reflecting a general improvement in market sentiment.

Global Developments Boosting the Euro’s Momentum

Beyond the Fed’s policy stance, other global events have helped shape the Euro’s performance this week. The ongoing trade tensions between the United States and China continue to grab headlines. However, the recent escalation—marked by new tariffs and retaliatory measures—hasn’t shaken markets as much as before. Many traders now believe both sides are likely to reach a practical agreement in the near future, which has tempered the sense of risk and uncertainty.

Meanwhile, in Europe, political developments have provided a subtle lift to the Euro. French Prime Minister Sébastien Lecornu announced a delay to the controversial pension reform until after the 2027 presidential elections. This move is widely seen as an attempt to stabilize the political climate and avoid further unrest, which could have destabilized the Eurozone’s second-largest economy.

The decision also came ahead of a crucial no-confidence vote, and by pausing the reform, the French government has bought itself valuable breathing room. This step has been interpreted positively by investors, who see it as a sign of political pragmatism—something the Euro can benefit from, especially during a time of global policy shifts.

The Changing Tone of the Global Economy

As the narrative shifts away from inflation fears and toward employment stability, global markets are beginning to embrace a more balanced perspective. The US economy, while still strong, shows signs of slowing job growth and cooling consumer sentiment. This has prompted the Federal Reserve to adopt a more cautious and accommodative approach.

In contrast, the Eurozone, despite its minor industrial slowdown, continues to exhibit resilience. Consumer demand remains stable, inflation appears under control, and policymakers are avoiding drastic changes that could unsettle the region. Together, these factors have positioned the Euro as an appealing alternative to the US Dollar for investors seeking both safety and potential growth.

Investor Sentiment and Future Outlook

Market participants are closely watching upcoming economic releases, particularly in the United States. Reports such as the New York Empire State Manufacturing Index and speeches from various Federal Reserve officials are expected to provide further insight into the Fed’s direction.

If the dovish tone continues and US data weakens further, the Euro could sustain its current upward trajectory. On the other hand, any unexpected strength in US economic indicators might temporarily slow the Euro’s progress. However, given the current momentum and market positioning, sentiment remains largely in favor of the European currency.

The Bigger Picture: What This Means for Traders and Investors

The recent developments highlight an important shift in global financial dynamics. A weaker US Dollar environment often benefits other major currencies, especially when regional economies show signs of stability. For traders, this environment creates new opportunities to capitalize on changing market sentiment.

The Euro’s recent strength demonstrates how quickly markets can react to central bank communication and shifting global conditions. As the Fed leans toward easing and the Eurozone maintains relative calm, the balance of power in the currency markets may continue to tilt in favor of the Euro for some time.

Moreover, the improved sentiment in Europe—supported by steady policymaking and reduced political risk—offers a layer of confidence that investors have been craving. As inflation pressures ease globally, attention has turned toward sustainable growth and job stability, themes that currently favor the Eurozone over the US.

Final Summary

In summary, the Euro’s recent climb reflects a combination of factors—stronger market sentiment, a softer US Dollar, and cautious optimism within Europe. The Eurozone’s industrial slowdown turned out to be less severe than feared, while the US Federal Reserve’s dovish stance has significantly weakened the Dollar’s appeal.

Investors are now positioning themselves for further Fed rate cuts, a trend that could keep the Euro supported in the near term. At the same time, political stability in Europe and easing trade tensions globally have provided additional confidence.

As the financial landscape continues to evolve, the Euro stands as a symbol of stability amid uncertainty—a currency that, for now, enjoys both fundamental and sentiment-driven support. Whether this momentum lasts will depend on upcoming economic data and central bank actions, but for the moment, the Euro’s steady performance signals that optimism is making its way back into global markets.

GBPUSD Climbs Higher as US Labor Market Worries Weigh on the Dollar

The British Pound Sterling (GBP) managed to gain strength against most major currencies, even though the UK’s recent labor market data pointed toward a slowdown. This move caught many traders by surprise because weaker job data usually pressures a currency lower. However, the Pound’s recovery shows that global market dynamics, especially those involving the US Dollar (USD), continue to play a major role in determining the Pound’s direction.

In midweek trading, the Pound extended its gains against the US Dollar after the greenback faced broad selling pressure. The reason? Concerns over the US labor market and hints from the Federal Reserve (Fed) that further interest rate cuts may be on the way. These developments gave traders a reason to look for alternatives to the Dollar — and the Pound was one of the beneficiaries.

Why the US Dollar Is Losing Its Shine

The US Dollar’s recent weakness has a lot to do with comments made by Federal Reserve officials, including Chair Jerome Powell. During a recent event, Powell admitted that the US job market is stuck in what he described as a “low-hiring, low-firing” phase. In simpler terms, businesses are not hiring aggressively, but they’re also not letting workers go — a sign of economic uncertainty.

GBPUSD is moving in a descending channel, and the market has reached the lower high area of the channel

Powell also acknowledged that while the broader US economy has shown better-than-expected strength, there’s still a mismatch between strong output data and the weak labor market. This contradiction has left policymakers in a tough position. They must decide whether to focus on the slowing job market or on the still-solid growth numbers.

Adding to the dovish tone, other Fed members such as Michelle Bowman and Susan Collins echoed Powell’s caution. Both officials expressed concern about potential job losses and hinted at the need for more rate cuts to support the economy. Collins went as far as saying that “another 25 basis point cut might be appropriate,” further fueling speculation of more monetary easing in the months ahead.

According to market forecasts, traders now expect the Fed to cut interest rates again this year. This growing expectation has weakened the Dollar’s appeal to investors, allowing the Pound Sterling to recover some of its recent losses.

The Impact of Global Trade Tensions

Another factor dragging down the US Dollar has been renewed tensions between the United States and China. The world’s two largest economies have been trading tariff threats for years, and this time, China reportedly imposed new port fees on US-related shipping firms. These fees affect goods ranging from consumer items to crude oil, signaling that trade friction between the two countries isn’t cooling off anytime soon.

Whenever such tensions rise, investors often move their money into currencies perceived as safer or more stable. Surprisingly, the British Pound benefited this time, as investors saw it as relatively undervalued compared to the Dollar.

Pound Sterling’s Mixed Performance Across the Board

Even though the Pound gained ground against the US Dollar, it wasn’t all smooth sailing. Against other major currencies like the Euro and the Japanese Yen, the Pound’s performance was mixed. The underlying reason is that traders remain cautious about the Bank of England’s (BoE) future moves.

Recent data from the UK labor market showed clear signs of cooling. The unemployment rate ticked higher to 4.8%, while wage growth — excluding bonuses — slowed to 4.7%, marking its lowest point since mid-2022. These figures suggest that job demand is easing and that wage-driven inflation pressures are fading. For the Bank of England, that’s both good and bad news: good because inflation might finally come under control, but bad because the economy may be losing steam.

Market participants have reacted by increasing bets that the BoE will cut interest rates further this year. According to financial reports, traders now anticipate a total of around 46 basis points of rate reductions over the next two policy meetings. This expectation has created some downward pressure on the Pound, even as global factors temporarily pushed it higher.

Bank of England’s Dovish Tone and IMF’s Warning

Bank of England Governor Andrew Bailey recently acknowledged that the UK job market is indeed slowing. Speaking at an international finance event in Washington, Bailey said that the latest labor figures confirm his earlier view that inflationary pressures are easing. However, he avoided commenting directly on whether more rate cuts are coming, leaving markets to speculate.

Interestingly, not everyone agrees with the idea of further cuts. The International Monetary Fund (IMF) has cautioned the BoE against acting too quickly. According to the IMF, price pressures in the UK may remain stronger than in other developed economies for a while. In fact, the IMF expects UK inflation to average around 3.4% in 2025 and 2.5% in 2026 — higher than most of its G7 peers. This means inflation may not fully return to the BoE’s 2% target anytime soon.

This creates a dilemma for policymakers. On one hand, the slowing labor market supports the idea of easing rates to stimulate growth. On the other, persistent inflation suggests that moving too fast could reignite price increases. This balance will likely define the Bank of England’s policy direction in the months ahead.

What Investors Are Watching Next

With the immediate focus shifting away from central bank meetings, traders are now looking toward the upcoming UK economic data. The next major release will be the country’s monthly Gross Domestic Product (GDP) and factory output figures for August. These reports will give investors a better picture of whether the economy is genuinely slowing or just experiencing a temporary soft patch.

If the data shows a contraction in growth, it could strengthen the case for rate cuts later this year. However, if the economy shows resilience, the BoE might hold off on further easing. Either way, these upcoming figures are expected to trigger fresh volatility for the Pound Sterling.

A Broader Look at What’s Driving the Pound

When we step back and look at the bigger picture, the Pound’s movements aren’t just about domestic data. They’re part of a wider story about global monetary policy and investor sentiment.

For example:

-

The US Federal Reserve’s tone heavily influences all major currencies, including the Pound. Any hint of policy easing in the US tends to weaken the Dollar and push other currencies higher.

-

Trade and geopolitical tensions, especially between the US and China, also shape global risk appetite. During uncertain times, investors often move funds across currencies quickly, creating unpredictable price swings.

-

The UK’s own economic health, particularly its inflation and employment trends, remains central to the BoE’s decisions — and those decisions directly affect how the Pound performs globally.

Put simply, the Pound’s rise this week is not just about the UK economy doing well. It’s about a complex mix of global economic shifts, policy expectations, and investor psychology.

Final Summary

The recent rally in the Pound Sterling shows how global sentiment can sometimes overshadow local economic challenges. Despite soft UK job data and rising expectations for interest rate cuts by the Bank of England, the Pound gained momentum thanks to a weaker US Dollar and cautious signals from the Federal Reserve.

While the IMF warns that inflation in the UK might remain higher than in other major economies, markets continue to expect easier monetary policy to support growth. The upcoming GDP and manufacturing data will be crucial in shaping the next big move for the British Pound.

In the end, the story of the Pound right now is one of balance — between optimism and caution, between inflation control and economic growth. And as global central banks navigate uncertain times, the Pound will likely continue to swing in response to every data release and policy hint that comes its way.

EURGBP Flat While France Faces Policy Uncertainty and UK Jobs Market Softens

The Euro and the British Pound are showing little movement, with the Euro holding firm against the Pound in a calm European trading session. This quiet phase in the market comes as traders carefully assess two major developments: France’s growing political uncertainty and the evolving economic outlook in the United Kingdom.

While the numbers remain steady, the mood among investors is far from relaxed. The situation in France has introduced fresh political tension, while in the UK, economic data continues to paint a mixed picture, fueling speculation about future monetary policy decisions. Together, these factors have kept market sentiment cautious and directionless, leading to a day of stability rather than strong market swings.

EURGBP is moving in a descending triangle pattern, and the market has reached the lower high area of the pattern

France’s Political Pause Adds a New Layer of Uncertainty

The Pension Reform Dilemma

France’s political landscape took a surprising turn when President Emmanuel Macron decided to postpone the controversial pension reform until after the 2027 presidential election. The decision followed months of social unrest and public opposition, reflecting the government’s attempt to ease tension and stabilize the country’s political climate.

However, while this move might temporarily calm domestic issues, it has sparked fresh concerns among investors about the government’s ability to deliver on its fiscal promises. The pension reform was considered a crucial part of Macron’s economic agenda aimed at reducing public spending and ensuring long-term financial sustainability. Delaying it now raises doubts about the government’s credibility in maintaining fiscal discipline.

Impact on Market Confidence

Many investors view the postponement as a short-term relief but a long-term risk. Political analysts suggest that the decision may weaken France’s ability to pass future budgets and sustain fiscal consolidation, especially with growing opposition parties gaining influence. Financial institutions like ING have warned that while the decision reduces the immediate threat of a no-confidence vote, it could hurt long-term market trust in France’s financial management.

Similarly, OCBC analysts highlighted that the situation remains fragile for the Euro. Despite this, they maintain that the broader fundamental outlook still supports the currency, suggesting that long-term investors might consider buying the Euro during dips — though patience will be key.

Economic Pressure Builds

Adding to France’s political strain is the recent economic data from Eurostat showing that industrial production in the Eurozone declined after a brief period of recovery. Industrial activity fell on a monthly basis, indicating a slowdown in manufacturing and production output. On a yearly comparison, growth also weakened, reflecting that the Eurozone economy is still struggling to regain strong momentum.

This softer data underscores the challenges facing European policymakers, who must now navigate not only inflationary pressures but also signs of economic cooling. The combination of slower growth and political uncertainty could keep the Euro’s performance capped in the near term.

UK’s Economic Struggles Point to More Central Bank Easing

Labor Market Loses Momentum

Across the English Channel, the United Kingdom faces its own set of challenges. The latest figures from the Office for National Statistics revealed that the country’s unemployment rate has risen to its highest level since 2021. At the same time, wage growth in the private sector has slowed significantly, showing that businesses are becoming more cautious amid weaker demand and higher borrowing costs.

This softening labor market suggests that the UK economy is starting to feel the pinch from previous interest rate hikes. With hiring activity cooling and wage pressures easing, the Bank of England may find more reasons to shift toward a policy of easing rather than tightening.

Rising Expectations for Rate Cuts

Markets are already reacting to this outlook. According to traders and analysts, expectations for additional rate cuts by the Bank of England have strengthened. Investors are increasingly confident that the central bank will reduce interest rates further before the end of the year to support growth and prevent a deeper slowdown.

This growing belief in monetary easing has added pressure on the British Pound, limiting its ability to gain against other major currencies like the Euro. While rate cuts could help stimulate the economy, they typically make a currency less attractive to investors seeking higher returns. As a result, the Pound may remain under pressure as long as rate-cut expectations persist.

Investors Stay on the Sidelines Amid Mixed Signals

Balancing Political and Economic Risks

With France facing political uncertainty and the UK dealing with economic softness, traders are taking a cautious approach. Neither currency currently shows strong momentum, as investors wait for clearer direction from upcoming economic reports and central bank decisions.

The Euro’s short-term outlook remains tied to how France manages its fiscal policy challenges and whether the broader Eurozone economy can regain traction. Meanwhile, the Pound’s performance will largely depend on the Bank of England’s next moves and how the UK labor market evolves in the coming months.

Market Sentiment: A Wait-and-See Mode

For now, both currencies are caught in a balancing act. The Euro benefits from a generally stable economic base and the European Central Bank’s careful approach, but France’s domestic political uncertainty limits enthusiasm. On the other hand, the Pound faces downside risks due to growing expectations of rate cuts, even though lower inflation could provide some relief in the longer term.

Traders are therefore staying in a wait-and-see mode, choosing not to make big bets until the outlook becomes clearer. This cautious sentiment explains the quiet and steady performance of the EUR/GBP pair, with neither side gaining a decisive edge.

What Lies Ahead for the Euro and Pound

Looking forward, the path of both currencies will depend on how the political and economic stories unfold in the coming weeks. In France, any new developments in government policy or budget discussions could impact investor confidence and influence the Euro’s direction. Meanwhile, in the UK, the focus will remain on labor market data, inflation figures, and the Bank of England’s monetary stance.

If the UK continues to show signs of economic cooling, the case for rate cuts will strengthen, potentially weighing on the Pound. On the other hand, if Eurozone data starts to improve and France manages to restore political stability, the Euro could gain an upper hand.

However, given the current uncertainty, both currencies may continue to trade in narrow ranges, with short-term fluctuations driven more by headlines than by solid trends.

Final Summary

The Euro and Pound are treading carefully as investors juggle political and economic crosswinds from both sides of the Channel. France’s decision to delay pension reforms has stirred political unease, raising questions about fiscal discipline and market stability. Meanwhile, the UK’s weakening labor market and slowing wage growth have increased the likelihood of more interest rate cuts by the Bank of England.

With both economies facing challenges — one political and the other economic — traders are hesitant to commit strongly to either currency. As a result, the EUR/GBP pair remains steady, reflecting a cautious market mood. The coming months will reveal whether France can restore confidence and whether the UK can stabilize growth, both of which will be key in determining the future course of the Euro and the Pound.

USDCHF Falls Under Heavy Selling as Investors Turn Bearish on the Dollar

The global currency market is buzzing with renewed excitement and speculation. The US Dollar is slipping lower against most major currencies as investors grow confident that the Federal Reserve will soon start cutting interest rates. Meanwhile, the Swiss Franc remains steady, held back by deflationary pressures in Switzerland. Let’s break down what’s happening, why it matters, and what could come next.

A Shift in Market Sentiment: The Dollar Loses Its Shine

The US Dollar has been losing strength as traders adjust their expectations for the Federal Reserve’s next move. After a long period of aggressive rate hikes to control inflation, recent signals from the Fed suggest that a softer approach is on the way. This change in tone has had an immediate impact, sending the Dollar downward in global trading sessions.

USDCHF is moving in an Ascending channel, and the market has reached the higher low area of the channel

For months, the Dollar benefited from higher interest rates, which attracted global investors seeking better returns. But with inflation now cooling and economic growth slowing, the Fed seems ready to ease monetary policy. As a result, investors are reducing their exposure to the Greenback, moving instead into other currencies and assets that could perform better in a low-rate environment.

What makes this shift particularly interesting is how quickly the mood has changed. Not long ago, markets were focused on trade tensions between the United States and China. Now, attention has turned to the Fed’s comments, especially those from Chair Jerome Powell, which have sparked expectations of rate cuts in the months ahead.

Fed’s Dovish Tone Sparks Talk of Rate Cuts

When Federal Reserve Chair Jerome Powell spoke earlier this week, his words were closely analyzed by traders and economists around the world. He made it clear that the central bank’s main concern right now isn’t inflation—it’s the weakening job market and slowing growth in several key sectors of the economy.

Powell’s Key Message

Powell emphasized that the Fed will not hesitate to act if economic conditions continue to soften. He signaled that a rate cut of 25 basis points is likely in the upcoming policy meeting, with the possibility of another one before the end of the year. This announcement gave traders a strong reason to expect cheaper borrowing costs ahead, triggering a wave of Dollar selling.

But Powell didn’t stop there. He also mentioned that the Fed is close to finishing its balance sheet reduction process. This program, often referred to as “quantitative tightening,” has been gradually shrinking the Fed’s holdings of bonds and other assets. Ending this process would mean more liquidity in the financial system, another factor that could weigh on the Dollar’s value.

Why It Matters for Investors

Lower interest rates typically make a currency less attractive because they reduce the return investors can earn on assets denominated in that currency. That’s exactly what’s happening now with the US Dollar. Traders are starting to price in not just one, but possibly multiple rate cuts. This makes it less appealing compared to currencies backed by central banks that are keeping rates higher for longer.

At the same time, the market’s growing belief that the Fed is nearing the end of its tightening cycle has also helped push up stocks and bonds, as lower rates usually support asset prices. However, for the Dollar, this environment is proving to be a drag.

Switzerland Faces Deflation: Why the Franc Isn’t Gaining Much

While the US Dollar is sliding, the Swiss Franc—often considered a safe-haven currency—isn’t making major gains either. The reason? Switzerland’s economy is dealing with its own set of challenges, particularly deflation.

Deflation Pressures on the Swiss Economy

Recent data shows that producer prices in Switzerland have been falling for five consecutive months. In September, prices dropped again, signaling persistent weakness in demand and production costs. Deflation means that prices of goods and services are declining over time, which might sound good for consumers but can be harmful to the broader economy.

When prices fall consistently, businesses earn less revenue, and people may delay spending in hopes of getting better deals later. This cycle can lead to slower growth and put pressure on the central bank to act.

SNB’s Dilemma: To Cut or Not to Cut

The Swiss National Bank (SNB) is now facing a tough decision. If deflation continues, it might be forced to cut interest rates again—or even reintroduce negative rates—to stimulate spending and investment. But doing so could limit the Franc’s potential to rise further against other currencies.

For investors, this means the Swiss Franc’s strength has boundaries. While it may still benefit from safe-haven demand in times of global uncertainty, its upside remains capped as long as deflation risks persist and the SNB stays cautious about tightening policy.

Global Currency Landscape: A Balancing Act

The current market situation is a fascinating mix of contrasts. On one side, the US Dollar is losing momentum due to expectations of lower interest rates. On the other, the Swiss Franc, despite its stability, isn’t soaring because of economic pressures at home. This creates an environment where both currencies face limitations, albeit for very different reasons.

For traders and investors, this tug-of-war presents both risks and opportunities. Those who rely heavily on Dollar-denominated assets might face short-term challenges as its value adjusts. Meanwhile, those holding Swiss Francs should be aware that its gains may be limited if Switzerland’s deflationary trend continues.

What stands out most is how interconnected global economies have become. A speech by the Fed Chair in Washington can send ripples across markets in Europe and Asia within hours. Similarly, weak data from Switzerland can influence expectations about safe-haven flows and central bank actions worldwide.

Final Summary

The latest developments in the currency market highlight a significant shift in global monetary sentiment. The US Dollar’s weakness stems from increasing confidence that the Federal Reserve will soon pivot toward rate cuts, prioritizing economic stability over inflation control. Jerome Powell’s remarks have effectively confirmed that the era of tight policy may be nearing an end, pushing traders to reassess their strategies.

At the same time, the Swiss Franc’s limited gains reflect Switzerland’s struggle with deflation, which keeps the Swiss National Bank cautious. The ongoing decline in producer prices underscores the economic challenges the country faces, restraining the Franc’s strength despite the Dollar’s downturn.

In essence, we are witnessing a moment where two traditionally strong currencies are weighed down by their own domestic concerns. The Dollar’s fall and the Franc’s hesitation remind us that currency markets are driven as much by expectations and psychology as by hard numbers. For now, traders are watching closely—waiting to see whether the Fed’s next move or Switzerland’s inflation outlook will reshape the balance once again.