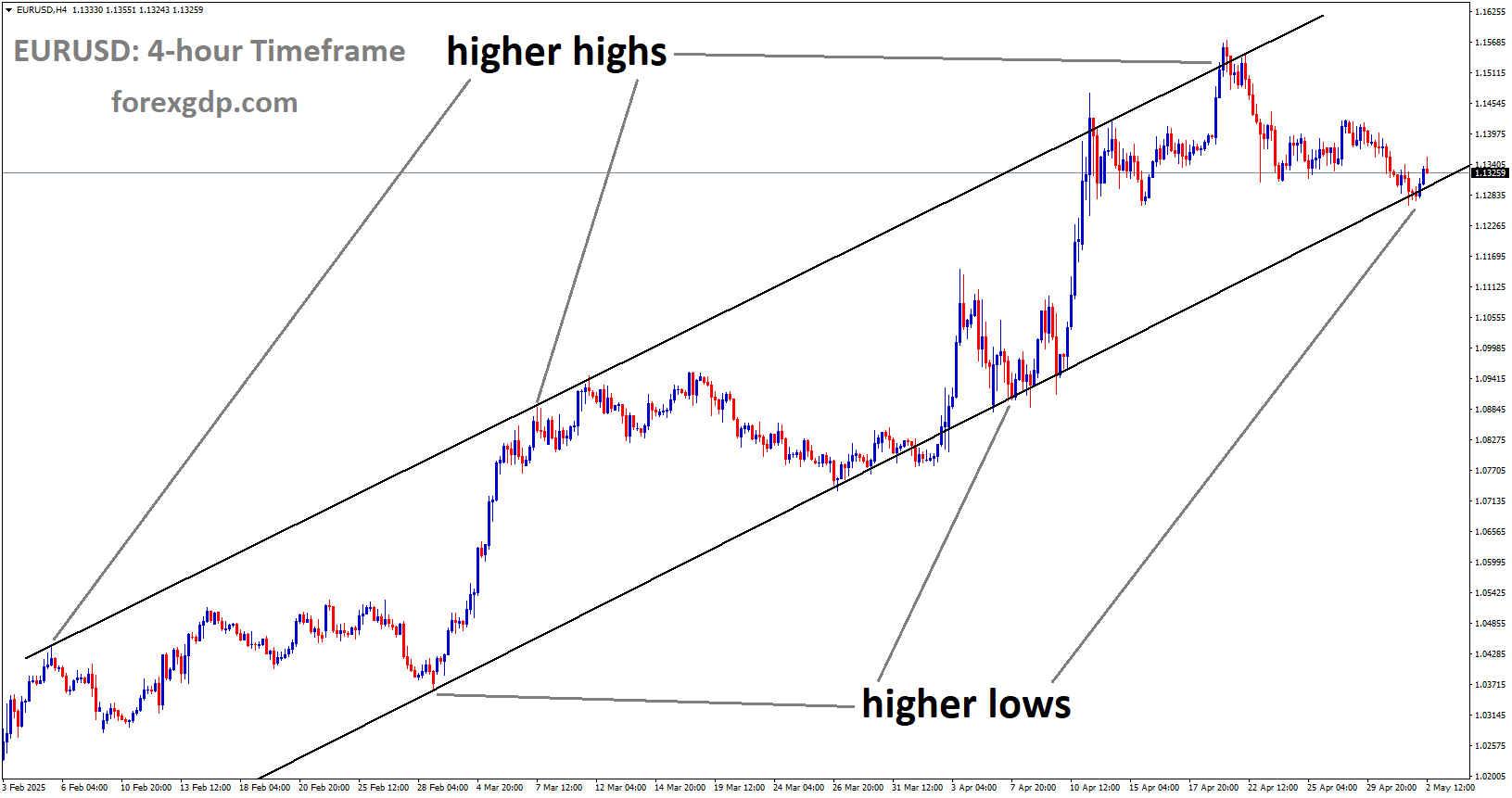

EURUSD is moving in a descending channel, and the market has reached the lower high area of the channel

EURUSD climbs as turmoil over central bank independence hits US currency

The euro continues to show resilience against the US dollar, holding onto its gains even after pulling back from earlier strength. While optimism from the Eurozone has improved, it is the growing uncertainty surrounding the US Federal Reserve that is shaping the broader currency mood. Investors appear increasingly uneasy about political pressure on the central bank, and that discomfort is weighing heavily on confidence in the US dollar.

Although positive economic news from Europe has offered some support, it has not been the main driver of recent currency movement. Instead, attention has shifted sharply toward Washington, where developments surrounding the Federal Reserve have raised questions about institutional independence and long-term stability.

Rising Political Pressure on the Federal Reserve

At the heart of the dollar’s weakness is a new wave of political tension involving Federal Reserve Chair Jerome Powell. Reports over the weekend suggested that Powell is facing a criminal investigation related to past testimony before a Senate committee. The issue reportedly centers on statements connected to renovation work at a Federal Reserve building.

Powell responded publicly, describing the situation as unprecedented. He suggested the investigation is part of a broader effort to pressure the central bank into adjusting monetary policy. These remarks have added fuel to investor concerns that political forces may be attempting to influence decisions that are traditionally made independently.

For financial markets, the independence of the Federal Reserve is not a minor detail. It is a cornerstone of trust in US monetary policy. When that independence appears threatened, confidence in the dollar can erode quickly. Investors tend to value predictability and institutional stability, and any hint that policy decisions could be swayed by politics introduces uncertainty.

This episode has also been interpreted as a signal to future central bank leaders. If pressure of this nature becomes normalized, markets may reassess how insulated US monetary policy really is from political agendas.

Global Tensions Add to Market Unease

Beyond domestic US issues, global geopolitical risks are also influencing sentiment. Tensions in Iran escalated over the weekend, with reports indicating that hundreds of protesters were killed during widespread unrest. The situation has drawn international attention, especially as Tehran has issued warnings about potential retaliation if it detects signs of foreign military action.

Such developments tend to push investors into a cautious stance. While the US dollar is often seen as a safe-haven asset during periods of global stress, that role becomes less reliable when confidence in US institutions is already under strain. In this environment, the euro has managed to stay supported, benefiting indirectly from the dollar’s struggles.

Geopolitical uncertainty does not always have an immediate or direct impact on currency markets, but it adds another layer of risk that investors must factor into their decisions. Combined with domestic political noise in the US, these global concerns contribute to a more fragile outlook for the dollar.

Eurozone Sentiment Shows Signs of Recovery

On the European side, recent data points to improving confidence among investors. The latest reading of the Sentix Economic Confidence Index showed a notable rebound compared to the previous month. This improvement marks the strongest showing in several months and suggests that pessimism about the Eurozone economy may be easing.

Investors appear more optimistic about the region’s growth prospects, even as challenges remain. Inflation pressures, energy concerns, and uneven growth across member states have not disappeared, but the overall mood has become less negative.

Despite this encouraging signal, the euro’s reaction has been relatively muted. The improved sentiment has helped prevent losses rather than spark a strong rally. This suggests that while Europe’s outlook is stabilizing, it is not yet the dominant force driving the currency. Instead, the euro is benefiting more from weakness elsewhere than from its own economic momentum.

US Economic Data Sends Mixed Signals

Recent US economic releases have painted a mixed picture. Labor market data suggests that conditions are no longer worsening, but there is little evidence of renewed strength. Employment indicators point to a market that is holding steady rather than accelerating.

At the same time, consumer sentiment has shown modest improvement. Households appear slightly more optimistic about their financial outlook compared to the previous month. This marks a second consecutive uptick in confidence, hinting at some resilience in consumer behavior.

Taken together, these figures support the idea that the US economy is slowing but not slipping into serious trouble. For policymakers, this balance reduces the urgency to change interest rate policy in the near term. As a result, expectations are growing that the Federal Reserve may opt to keep its policy stance unchanged at its upcoming meeting.

However, even stable economic data may not be enough to lift the dollar if concerns about governance and independence persist. Markets can tolerate weak growth or soft data, but they are far less forgiving when institutional credibility is called into question.

What Investors Are Watching Next

With the economic calendar relatively light in the immediate term, attention is turning to public remarks from Federal Reserve officials. Any comments that address policy direction or respond to recent political developments will be closely examined.

Later in the week, fresh inflation data from the United States is expected to provide further insight into price trends and consumer pressures. These figures could influence expectations around future policy decisions, especially if they diverge from recent trends.

In addition, speeches from multiple central bank officials may help clarify how policymakers are interpreting the current economic landscape. Investors will be listening not only for guidance on interest rates but also for reassurance that policy decisions remain data-driven and insulated from political influence.

Final Summary

The euro’s steady performance reflects more than just improving sentiment in Europe. It is also a response to growing doubts about the US dollar, fueled by political pressure on the Federal Reserve and heightened global tensions. While Eurozone data shows signs of recovery, its impact has been secondary to concerns surrounding US institutional stability.

As markets look ahead, the focus remains on central bank communication, inflation trends, and geopolitical developments. Until confidence in the Federal Reserve’s independence is restored, the US dollar may continue to face headwinds, allowing the euro to remain supported even without a strong push from its own economic fundamentals.

GBPUSD Climbs While Confidence in Fed Leadership Faces Pressure

The Pound Sterling made a strong comeback against the US Dollar during the European trading session on Monday, reversing earlier losses and regaining confidence. The recovery came as the US Dollar weakened sharply following unexpected legal developments involving the head of the Federal Reserve. This sudden shift in sentiment pushed investors to reassess risk, central bank independence, and the future direction of monetary policy in both the United States and the United Kingdom.

GBPUSD is moving in an uptrend channel, and the market has reached the higher low area of the channel

As global markets absorbed the news, attention also turned toward upcoming economic data from both countries. Employment figures from the UK and inflation data from the US are expected to play a key role in shaping market expectations in the days ahead.

Legal Pressure on the Federal Reserve Shakes Investor Confidence

The US Dollar came under pressure after reports emerged that the Department of Justice had opened a criminal investigation into Federal Reserve Chair Jerome Powell. The inquiry is linked to allegations surrounding the management of funds used for the renovation of the Federal Reserve’s headquarters in Washington, as well as statements Powell made during a Senate testimony earlier in the year.

The news caught markets off guard and triggered a swift reaction. Investors grew uneasy about the broader implications of legal action against the central bank’s leadership, especially at a time when economic stability remains fragile. The US Dollar weakened as confidence took a hit, allowing other major currencies, including the Pound Sterling, to recover lost ground.

Powell responded firmly to the allegations, arguing that the investigation was not truly about the renovation project or his testimony. Instead, he suggested it was being used as a pretext tied to disagreements over monetary policy. According to Powell, the threat of criminal charges reflects frustration with the Federal Reserve’s commitment to setting interest rates based on economic data and public interest rather than political pressure.

Rising Concerns Over Central Bank Independence

Market analysts believe the situation has intensified the long-running tension between Powell and President Donald Trump, who has repeatedly criticized the Federal Reserve for not cutting interest rates aggressively enough since returning to office. The escalation of this dispute has raised serious concerns about the independence of the US central bank.

Central bank autonomy is widely seen as essential for maintaining financial stability and controlling inflation. Any perception that political forces are influencing policy decisions can undermine trust in a currency. In this case, fears that the Federal Reserve’s independence could be weakened added to the downward pressure on the US Dollar.

For currency markets, this uncertainty matters. The US Dollar has traditionally benefited from the credibility and stability of US institutions. When that credibility is questioned, investors often look elsewhere, which helped support the Pound Sterling’s rebound.

UK Employment Data Takes Center Stage

While developments in the US grabbed headlines, investors are also closely watching key economic data from the United Kingdom. The next major focus is the UK employment report covering the three months to November, scheduled for release on Tuesday. These figures are expected to provide fresh insight into the health of the labor market and the future direction of Bank of England policy.

The UK job market has remained under pressure in 2025. Many companies have been cautious about hiring, largely due to higher employer contributions to social security schemes. This has led firms to control costs by slowing recruitment, even as parts of the economy show resilience.

Recent survey data from the Recruitment and Employment Confederation, in partnership with KPMG, painted a mixed picture. Labor demand remained soft, signaling continued caution among employers. At the same time, wage growth showed signs of acceleration toward the end of the year, suggesting that competition for skilled workers has not completely disappeared.

This combination of slower hiring and rising wages presents a challenge for policymakers. On one hand, weaker job creation can weigh on economic growth. On the other, stronger wage growth can add to inflationary pressures, complicating decisions around interest rates.

US Labor Market Shows Mixed Signals

Across the Atlantic, recent US employment data has sent mixed messages. The latest Nonfarm Payrolls report showed a noticeable drop in the unemployment rate, indicating that the labor market remains relatively tight. However, the pace of job creation slowed compared to expectations, suggesting that hiring momentum may be easing.

These conflicting signals have added to uncertainty about the Federal Reserve’s next move. A strong labor market can support consumer spending, but slower hiring may point to emerging cracks beneath the surface. For now, investors remain cautious as they wait for more clarity from upcoming inflation data.

Inflation Remains a Key Concern for the Fed

The next major catalyst for the US Dollar will be the release of Consumer Price Index data. Inflation has been a persistent challenge for the Federal Reserve, remaining above its long-term target for an extended period.

Earlier in the year, the Fed implemented several modest interest rate cuts in an effort to support the labor market. While these moves were aimed at easing economic pressures, they also raised concerns about whether inflation could stay elevated for longer than desired.

Atlanta Federal Reserve President Raphael Bostic recently подчеркed this concern, stating in a radio interview that inflation remains too high and must be brought under control. His comments reinforced the view that the Fed is not yet ready to declare victory over rising prices, even as growth shows signs of slowing.

Bostic’s remarks highlight the delicate balancing act facing policymakers. Cutting rates too quickly could fuel inflation, while holding rates steady for too long could strain the labor market. This uncertainty continues to influence investor sentiment and currency movements.

What This Means for the Pound and the Dollar

The Pound Sterling’s recent recovery reflects more than just a short-term reaction to US headlines. It underscores how political risk, central bank credibility, and economic data can all intersect to drive currency trends.

For now, the US Dollar remains sensitive to developments surrounding the Federal Reserve and upcoming inflation figures. Any sign that inflation is cooling could offer relief, while further political pressure on the Fed may deepen concerns.

Meanwhile, the Pound’s outlook will depend heavily on domestic data, particularly the labor market. Strong wage growth could support the currency, but signs of prolonged weakness in hiring may limit gains.

Final Summary

The Pound Sterling rebounded strongly as the US Dollar weakened following news of a criminal investigation involving Federal Reserve Chair Jerome Powell. The situation has raised serious concerns about political interference and central bank independence in the United States, undermining confidence in the Dollar. At the same time, investors are closely watching upcoming UK employment data and US inflation figures, both of which are expected to shape monetary policy expectations. With inflation still a major concern and labor markets sending mixed signals, currency markets are likely to remain sensitive to economic and political developments on both sides of the Atlantic.

USDJPY Holds Firm Near Annual Peak as Political Tensions Shake Confidence

The USD/JPY currency pair has stayed strong near its highest level of the year, holding firm during the European trading session on Monday. This steady performance comes at a time when both the US Dollar and the Japanese Yen are facing separate political and economic pressures that are shaping investor sentiment.

USDJPY is moving in an uptrend channel, andthe market has reached a higher high area of the channel

Recent developments in the United States and Japan have created an unusual situation where both currencies are under strain for different reasons. As a result, traders are closely watching political headlines and upcoming economic data for clearer direction.

US Dollar Holds Ground Despite Political Headwinds

The US Dollar has shown resilience even as it faces renewed uncertainty linked to political and institutional concerns. Reports that US federal prosecutors have brought criminal accusations against Federal Reserve Chair Jerome Powell have drawn significant attention across global markets. The charges relate to alleged mismanagement of funds connected to the renovation of the Federal Reserve’s headquarters in Washington.

Chair Powell has strongly denied the claims. He has stated that the accusations are not genuinely about the renovation project or his testimony, but instead serve as a pretext driven by other motives. His response has added another layer of complexity to an already sensitive situation.

These developments have sparked fresh debate around the independence of the Federal Reserve. Market participants generally view any threat to the central bank’s autonomy as a negative factor for the US Dollar. Confidence in the Fed’s ability to act without political pressure plays a key role in maintaining trust in US monetary policy.

Even with these concerns in the background, the US Dollar has avoided sharp weakness. This suggests that traders are taking a cautious wait-and-see approach rather than reacting emotionally to headlines. Many investors appear reluctant to make bold moves ahead of important economic data scheduled for release.

Federal Reserve Independence Back in Focus

The issue of central bank independence is not new, but it has gained renewed importance following the recent allegations. The Federal Reserve’s credibility depends heavily on the perception that it operates free from political influence. Any suggestion that this independence is under threat can quickly unsettle financial markets.

In this case, investors are weighing the seriousness of the accusations against Powell’s firm denial. Some see the situation as noise that may fade over time, while others worry it could evolve into a longer-term issue if political pressure intensifies.

For now, the market response has been measured. The lack of panic suggests that traders are waiting for more clarity before reassessing their outlook on the US Dollar. Much will depend on how the legal and political process unfolds in the coming weeks.

Inflation Data Looms Large for Market Direction

Beyond political developments, attention is also turning toward key economic data from the United States. The upcoming release of consumer inflation figures is expected to play a major role in shaping short-term market sentiment.

Inflation data often influences expectations around future interest rate decisions. If price pressures show signs of easing or accelerating, it could alter how investors view the Federal Reserve’s next steps. This, in turn, would have a direct impact on the US Dollar’s performance.

Because of this, many traders are choosing to remain cautious. Rather than reacting strongly to political headlines alone, they are waiting for economic evidence that could confirm or challenge current expectations. This cautious stance has helped keep the US Dollar relatively stable despite ongoing uncertainty.

Japanese Yen Weakened by Political Uncertainty

On the Japanese side, the Yen has also been under pressure, largely due to domestic political developments. Reports suggest that Japan’s Prime Minister, Sanae Takaichi, may be considering calling an early snap election. According to sources cited by international media, such an announcement could come as early as February.

The possibility of a snap election introduces uncertainty into Japan’s political landscape. Elections often raise questions about future policy direction, fiscal priorities, and leadership stability. For currency markets, this uncertainty can translate into reduced confidence in the national currency.

Investors tend to dislike unpredictability, especially when it involves changes in government or shifts in policy. As a result, the Yen has struggled to attract support while speculation around the election continues.

Political Timing and Market Sensitivity

The timing of a potential election adds to the market’s sensitivity. With global investors already navigating complex economic conditions, any sudden political move can amplify caution. In Japan’s case, traders are trying to assess whether an early election would strengthen or weaken the current administration’s mandate.

Until there is clarity, many are choosing to stay on the sidelines or reduce exposure to the Yen. This cautious behavior has contributed to the currency’s underperformance, especially when paired against counterparts that are seen as relatively more stable.

USD/JPY Supported by Relative Weakness on Both Sides

What makes the current situation unusual is that both the US Dollar and the Japanese Yen are facing their own challenges at the same time. Yet, the USD/JPY pair has remained firm. This reflects a balance of relative weakness rather than clear strength from either currency.

In simple terms, the pair is being supported because neither side has a strong enough negative trigger to cause a sharp move. The US Dollar is weighed down by concerns over institutional credibility, while the Yen is pressured by domestic political uncertainty.

This dynamic has resulted in a steady trading environment, with the pair holding close to its recent highs. Traders appear content to wait for clearer signals before making decisive moves.

What Traders Are Watching Next

Looking ahead, market participants will be closely monitoring several key factors. In the United States, any new developments related to the accusations against the Federal Reserve Chair could influence sentiment quickly. Statements from officials or progress in the legal process may either calm or intensify concerns.

At the same time, upcoming inflation data will likely shape expectations around monetary policy. Clear signs of changing price pressures could shift the balance for the US Dollar.

In Japan, attention remains fixed on political headlines. Confirmation of a snap election, along with details about its timing and platform, could have a meaningful impact on the Yen’s outlook.

Summary of Current Market Dynamics

The USD/JPY pair has remained strong near its yearly peak as both currencies face separate but significant challenges. In the United States, allegations against the Federal Reserve Chair have raised concerns about central bank independence, while investors await important inflation data for further guidance. In Japan, speculation around a potential snap election has added political uncertainty, weakening confidence in the Yen.

With major developments unfolding on both sides, traders are adopting a cautious approach. Until clearer signals emerge from economic data and political decisions, the pair is likely to remain influenced by shifting sentiment rather than decisive trends.

USDCHF Weakens as Global Uncertainty Fuels Demand for the Franc

The USD/CHF currency pair moved lower at the start of the week as the Swiss Franc gained strength and the US Dollar lost momentum. A mix of rising geopolitical tensions, cautious investor behavior, and fresh concerns around US monetary leadership pushed traders toward safer assets. In uncertain times like these, the Swiss Franc often attracts attention, and this period has been no exception.

USDCHF is moving in an uptrend channel, and the market has reached the higher low area of the channel

As global headlines turned more serious, investors reassessed risk and adjusted their positions. The result was a stronger Franc and a softer Dollar, ending the pair’s short-term upward move and shifting market focus toward safety and stability.

Safe-Haven Demand Rises Amid Geopolitical Tensions

One of the main drivers behind the stronger Swiss Franc has been a renewed rise in geopolitical uncertainty. Political developments in the Middle East triggered concern across global markets, encouraging investors to reduce exposure to riskier assets.

The situation intensified after strong warnings were issued by US leadership toward Tehran regarding the handling of protests. At the same time, Iranian officials responded by cautioning against any form of foreign intervention. These exchanges raised fears of escalation, which often leads investors to seek currencies known for stability.

The Swiss Franc has long held a reputation as a safe haven during times of global stress. Switzerland’s political neutrality, strong financial system, and consistent economic policies make its currency attractive when uncertainty rises. As tensions made headlines, demand for the Franc increased, placing downward pressure on USD/CHF.

Arctic Security and Greenland Add to Market Unease

Geopolitical concerns were not limited to the Middle East. Developments in Europe also contributed to a cautious market mood. Several European countries, including the United Kingdom and Germany, began discussing an expanded military presence in Greenland to strengthen Arctic security.

Germany is reportedly considering proposing a joint NATO mission in the region, while UK Prime Minister Keir Starmer has called on allies to increase their focus on the High North. These discussions gained more attention after renewed remarks from US leadership suggesting American ownership of Greenland.

Although these events are still in the discussion phase, they highlight growing strategic competition in the Arctic. Markets tend to react not only to actions but also to rising geopolitical rhetoric. As global power dynamics shift, investors often prefer to stay defensive, again supporting demand for the Swiss Franc.

Swiss National Bank Outlook Supports the Franc

Beyond global politics, domestic factors in Switzerland have also helped support the Franc. Recent inflation data showed a modest increase, offering insight into the Swiss National Bank’s policy direction.

Swiss inflation rose to 0.1% year over year in December 2025. While this marked the first increase in several months, it remained near the lower end of the central bank’s target range. This data reinforced expectations that the SNB is likely to keep interest rates unchanged in upcoming meetings.

Stable Policy Expectations Boost Confidence

A steady policy outlook can be just as powerful as aggressive tightening when it comes to currency strength. Investors value predictability, and the SNB’s cautious and measured approach continues to inspire confidence. With inflation slowly improving alongside signs of economic recovery, markets see little urgency for policy shifts.

This sense of stability makes the Swiss Franc appealing, especially when compared to currencies facing political or institutional uncertainty. As long as inflation remains controlled and growth gradually improves, the Franc is likely to retain its defensive appeal.

US Dollar Weakens on Federal Reserve Concerns

While the Swiss Franc benefited from both global and domestic support, the US Dollar faced its own challenges. Investor sentiment toward the Dollar weakened after reports emerged of a criminal investigation involving the Federal Reserve.

According to media reports, federal prosecutors have opened an investigation into Federal Reserve Chair Jerome Powell. The probe reportedly focuses on the renovation of the central bank’s headquarters in Washington and whether accurate information was provided to Congress about the project.

Institutional Uncertainty Weighs on Confidence

Even though the investigation does not directly relate to monetary policy decisions, it introduces an element of uncertainty around the leadership of the US central bank. Markets tend to react negatively when trust in institutions is questioned, especially those responsible for financial stability.

As traders digested the news, many adopted a more cautious stance toward the US Dollar. This hesitation contributed to the currency’s broader weakness and added pressure on USD/CHF.

Labor Market Data Reinforces Cautious Outlook

Economic data from the United States also played a role in shaping market expectations. The latest jobs report showed slower-than-expected growth in employment, reinforcing the view that the US economy may be losing some momentum.

Nonfarm Payrolls increased by 50,000 in December, below both the previous month’s revised figure and market expectations. While the unemployment rate edged lower to 4.4%, the overall picture suggested a cooling labor market.

Rate Cut Expectations Gain Traction

Slower job growth has strengthened expectations that the Federal Reserve may move toward further interest rate cuts. Lower rates can reduce the appeal of a currency by narrowing yield advantages, especially when compared to currencies backed by stable policy outlooks.

As traders priced in a more accommodative stance from the Fed, the US Dollar faced additional headwinds. Combined with political and institutional concerns, this shift in expectations added to the pressure on USD/CHF.

How Risk Sentiment Shapes Currency Flows

The recent movement in USD/CHF highlights how sensitive currency markets are to changes in global sentiment. When uncertainty rises, investors often prioritize capital preservation over returns. This behavior tends to benefit safe-haven currencies like the Swiss Franc while weighing on the US Dollar during periods of domestic or political strain.

At the same time, the Dollar’s traditional safe-haven status can be challenged when uncertainty originates from within the United States itself. In such cases, investors may look elsewhere for stability, shifting flows toward currencies backed by neutrality and steady governance.

Final Summary

USD/CHF moved lower as a combination of global tensions and domestic concerns reshaped investor sentiment. Rising geopolitical risks, from the Middle East to the Arctic, increased demand for the Swiss Franc as a safe haven. Switzerland’s stable inflation outlook and predictable central bank policy further strengthened confidence in the currency.

On the other side, the US Dollar weakened amid concerns surrounding Federal Reserve leadership and signs of slowing job growth. Expectations of future rate cuts added to the cautious tone, prompting traders to reassess their exposure.

Together, these factors created a clear shift in market dynamics, favoring the Swiss Franc and pushing USD/CHF lower as investors navigated a more uncertain global landscape.