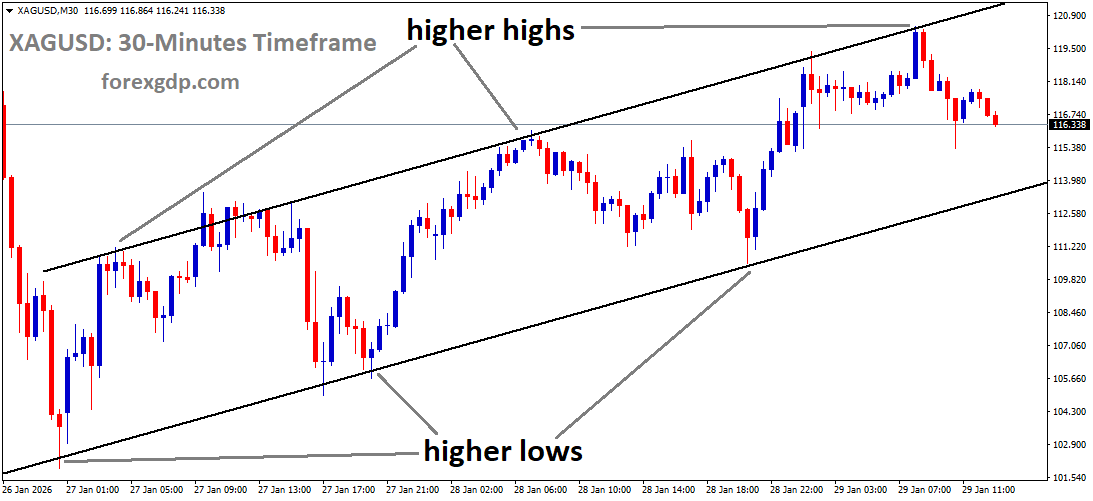

XAGUSD is moving in an uptrend channel, and the market has fallen from the higher high area of the channel

XAGUSD Loses Momentum Following a Historic Surge

Silver has recently taken a pause after reaching new highs, easing slightly as markets digest fast-moving global events. Even with this short-term pullback, interest in the metal remains strong. Investors continue to look at silver as a reliable store of value during times of political tension, economic uncertainty, and shifting currency dynamics.

This movement reflects a broader story unfolding across global markets. From rising geopolitical risks to questions around monetary policy and government debt, silver is once again reminding investors why it has long been considered a safe place to protect wealth.

Geopolitical Tensions Push Investors Toward Safe Assets

One of the biggest drivers behind silver’s recent strength has been rising geopolitical stress. Statements from U.S. leadership urging Iran to return to nuclear negotiations, paired with warnings of harsher consequences if talks fail, have added fuel to global uncertainty. In response, Iran issued strong threats against the United States, Israel, and their allies, raising concerns about potential conflict in the region.

Whenever tensions like these rise, investors tend to seek safety. Precious metals such as silver often benefit because they are not tied to the performance of any single country or political system. As global headlines grow more serious, demand for assets that can hold value during crises naturally increases.

Silver’s appeal in these moments is not only emotional but practical. It has a long history as a hedge against instability, making it attractive when the future feels unpredictable.

Shifting Global Economics Strengthen Silver’s Role

Beyond geopolitics, deeper economic changes are also influencing silver demand. Analysts have pointed out that rising government debt in the United States is becoming a growing concern for investors. At the same time, the global trade system appears to be moving away from a fully connected model toward more regional alliances.

This shift has meaningful consequences. As trade becomes more fragmented, confidence in traditional financial systems can weaken. Investors may start looking beyond assets closely linked to one economy or currency. Silver, along with other precious metals, offers diversification that feels safer in a world where global cooperation is less certain.

Some market observers believe this marks a gradual move away from a U.S.-centered investment approach. Instead, investors are spreading risk more evenly across assets that can perform independently of government policy decisions.

Questions Around Central Bank Independence Add Pressure

Another factor supporting silver demand is growing concern over the independence of the U.S. Federal Reserve. Recent political actions have raised questions about how much freedom the central bank will have in shaping future monetary policy.

Moves by the current administration, including investigations involving senior Federal Reserve figures and discussions around leadership changes, have unsettled investors. When trust in monetary institutions weakens, confidence in long-term policy stability can suffer.

For investors, this kind of uncertainty creates hesitation around assets tied closely to interest rate decisions and central bank guidance. Silver benefits in these moments because it does not rely on promises made by policymakers. Its value is shaped more by supply, demand, and long-standing market trust.

The Dollar’s Changing Strength Supports Hedging Demand

Silver has also gained support as the strength of the U.S. dollar shows signs of easing. When the dollar loses momentum, precious metals often become more attractive to global investors, especially those looking to protect purchasing power.

While U.S. officials continue to express commitment to a strong currency, market sentiment does not always move in a straight line. Investors pay close attention to inflation trends, growth data, and fiscal decisions. Any uncertainty in these areas can lead to increased interest in hedging tools like silver.

Holding silver allows investors to balance risk. If currencies weaken or lose stability, precious metals can help preserve value. This makes silver especially appealing in times when economic signals are mixed or unclear.

Federal Reserve Signals Caution and Flexibility

Recent comments from the Federal Reserve suggest a cautious approach moving forward. Policymakers have noted that job growth is slowing slightly and that unemployment appears to be stabilizing. These signals point to an economy that is no longer overheating but still holding steady.

Rather than committing to a fixed policy path, the central bank has emphasized flexibility. Decisions will be based on incoming data rather than long-term promises. While this approach allows room to respond to economic changes, it also adds uncertainty for investors trying to plan ahead.

Silver tends to perform well in these environments. When future interest rate moves are unclear, investors often prefer assets that do not depend on predictable policy outcomes. Silver fits that role well, offering stability without reliance on central bank direction.

Why Silver Continues to Attract Long-Term Interest

Even with recent pullbacks, silver’s broader appeal remains intact. It serves multiple roles at once. It is a store of value, a hedge against inflation, a shield against political risk, and a way to diversify portfolios.

Unlike assets driven mainly by growth expectations or earnings forecasts, silver responds strongly to fear, caution, and uncertainty. As long as global tensions remain high and economic questions go unanswered, interest in silver is likely to stay firm.

Investors are not necessarily chasing short-term gains. Many are looking for balance and protection. Silver offers both, especially when confidence in currencies and institutions begins to waver.

Final Summary

Silver’s recent retreat comes after a powerful run fueled by global uncertainty rather than short-term speculation. Geopolitical tensions, concerns about rising debt, questions over central bank independence, and shifting currency dynamics have all played a role in strengthening demand.

While prices may fluctuate in the near term, the underlying reasons driving interest in silver remain firmly in place. As investors continue to navigate an unpredictable global landscape, silver stands out as a trusted asset for protection, diversification, and long-term stability.

EURCAD Eyes Canada’s Upcoming Trade Figures and Job Market Signals

Canada’s economic story is entering a more cautious phase. Fresh data releases and recent signals from policymakers suggest that growth is facing new headwinds, even as the broader outlook remains stable for now. Insights from TD Securities’ Global Strategy Team point to softer trade performance, pressure within manufacturing, and a central bank that is increasingly focused on uncertainty rather than urgency.

EURCAD reached the retest area of the broken downtrend channel

Together, these factors paint a picture of an economy that is slowing but not stalling. Businesses, households, and policymakers are all adjusting to a world where growth is uneven and risks are tilted to the downside. Understanding these developments helps explain where Canada may be heading over the next few years.

Trade Data Signals Ongoing Export Challenges

One of the most closely watched releases is Canada’s international merchandise trade report. The latest expectations suggest that the trade deficit will narrow modestly in November, settling near $1.0 billion. While this may appear like an improvement on the surface, the underlying drivers tell a more complicated story.

Exports are facing new obstacles, particularly in the manufacturing sector. Motor vehicle production, which has played a major role in driving export growth in recent months, is now losing momentum. As production slows, exports tied to this industry are expected to follow suit. This reversal comes after a strong earlier period that helped lift manufacturing shipments.

Beyond autos, broader manufacturing conditions are showing signs of strain. A notable decline in hours worked across the sector points to softer demand and reduced activity. When factories cut hours, it often signals caution about future orders and profitability. These trends suggest that the export slowdown is not limited to a single industry but reflects wider challenges across manufacturing.

Manufacturing Faces Broader Headwinds

Manufacturing has long been a backbone of Canada’s trade performance, making its recent weakness particularly important. The pullback in production and hours worked highlights the pressure firms are facing from both domestic and global factors.

On the global side, slower growth in key trading partners is dampening demand for Canadian goods. At home, higher borrowing costs and lingering uncertainty are causing businesses to delay investment and expansion. Together, these forces are creating a tougher environment for manufacturers trying to maintain output levels.

This slowdown matters because manufacturing supports a wide range of jobs and supply chains. When activity weakens, the effects ripple outward, impacting transportation, logistics, and local economies. While the sector is not in crisis, the data suggest it is entering a period of adjustment rather than expansion.

Payroll Employment Offers Important Clues

Alongside trade data, payroll employment figures are another critical piece of the puzzle. Changes in payroll employment provide a clearer view of labor market conditions, especially within industries like manufacturing.

Recent trends indicate that employment growth is cooling, consistent with the decline in hours worked. Employers appear to be holding back on hiring as they assess the outlook for demand and costs. This does not necessarily mean widespread job losses, but it does point to a labor market that is losing some of its earlier momentum.

A softer labor market can have mixed effects. On one hand, it reduces pressure on wages and inflation. On the other, it can weigh on consumer confidence and spending. For policymakers, these signals reinforce the need for caution rather than aggressive action.

Bank of Canada Holds Steady but Shifts Its Tone

The Bank of Canada recently chose to keep its policy rate unchanged, signaling stability in the near term. However, the language in its policy statement revealed a subtle but important shift. The central bank emphasized heightened uncertainty, adopting a more cautious and dovish tone than before.

This shift reflects a growing awareness of the risks facing the economy. While inflation has eased from earlier highs, growth is becoming less certain. The Bank appears more focused on preserving balance than pushing for tighter conditions.

At the same time, the Bank updated its economic projections. Growth expectations for 2025 were revised higher, suggesting confidence in a medium-term rebound. However, forecasts for 2026 remained unchanged, even with the introduction of new fiscal support. This contrast highlights the Bank’s belief that near-term improvements may not fully carry through into later years.

What the Growth Outlook Really Means

The mixed nature of the Bank’s projections underscores the complexity of Canada’s economic outlook. Stronger growth expectations in one year do not guarantee sustained momentum over the long run. Structural challenges, global uncertainty, and shifting demand patterns all play a role.

Fiscal support may help cushion the economy, but it is not a cure-all. Businesses and households are still navigating higher costs and cautious financial conditions. As a result, growth may remain uneven, with some sectors performing better than others.

This is why the Bank of Canada is signaling patience. By holding rates steady and emphasizing uncertainty, it is leaving room to respond as conditions evolve rather than committing to a fixed path.

Why Policy Is Likely to Stay on Hold

Looking ahead, expectations are building that the central bank will maintain its current stance well into the future. The prevailing view is that rates will remain unchanged through 2026, reflecting a balance between cooling inflation and slowing growth.

While the next policy move is expected to be a rate increase in early 2027, that outlook is far from certain. Near-term risks appear tilted toward the downside, meaning economic conditions could weaken more than anticipated. If that happens, the Bank may need to delay or rethink its plans.

This cautious approach is consistent with the Bank’s recent messaging. By acknowledging uncertainty, policymakers are signaling that they are prepared to adapt rather than react hastily.

What This Means for Businesses and Consumers

For businesses, the current environment calls for careful planning. Slower export growth and softer manufacturing activity suggest that demand may remain uneven. Companies may focus on efficiency and cost management rather than aggressive expansion.

Consumers, meanwhile, may notice a more stable but subdued economic backdrop. A cooling labor market could limit wage growth, while steady interest rates provide some predictability for borrowers. Overall, the outlook is one of moderation rather than boom or bust.

Understanding these dynamics can help both groups make informed decisions. The economy is not flashing red, but it is clearly navigating a more challenging phase.

Final Summary: A Period of Caution and Balance

Canada’s economic landscape is defined by cautious optimism mixed with real challenges. Trade data point to modest improvements in the deficit, but underlying export weakness remains a concern. Manufacturing is facing headwinds that extend beyond a single industry, while employment growth is cooling.

At the policy level, the Bank of Canada is choosing patience. By holding rates steady and adopting a dovish tone, it is acknowledging uncertainty while keeping its options open. The road ahead is likely to be steady rather than dramatic, with growth unfolding unevenly across sectors.

In this environment, balance is key. Policymakers, businesses, and households alike are adjusting expectations, preparing for a future that rewards flexibility and careful decision-making.

EURUSD Holds Ground as Dollar Bounces Lack Conviction

The euro and the US dollar have settled into a familiar pattern of hesitation. After weeks of strong moves in both directions, the EUR/USD pair has shifted into a calmer phase, with neither side showing enough momentum to take full control. Traders are watching economic data and central bank signals closely, trying to decide what comes next in a year already filled with policy uncertainty and political noise.

EURUSD has broken the Ascending channel in downside

This sideways movement reflects a broader pause in global currency markets. Positive news from the Eurozone has offered support to the euro, while the US dollar has struggled to regain strength after an initial boost from the Federal Reserve. For now, both currencies appear caught in a balancing act, with investors waiting for clearer direction.

Eurozone Confidence Data Lifts Sentiment

Fresh data from the Eurozone has provided a welcome dose of optimism. Economic sentiment improved more than expected at the start of the year, suggesting that businesses and consumers are feeling more confident about the months ahead. This improvement was not limited to one sector but spread across industry and services, pointing to a broader recovery in mood.

Industrial confidence showed noticeable improvement compared to the previous month, hinting that manufacturers are seeing better demand conditions or at least fewer headwinds. At the same time, the services sector reported stronger sentiment, outperforming expectations and reinforcing the idea that domestic activity remains resilient.

Consumer confidence, while still in negative territory, held steady rather than deteriorating. This stability matters, as household spending plays a key role in sustaining growth. Together, these indicators suggest that the Eurozone economy is not only avoiding further weakness but may be laying the groundwork for modest improvement.

For the euro, this data has acted as a stabilizing force. Even when upward momentum faded, the currency managed to hold onto its gains, reflecting a growing belief that the worst economic fears may be behind the region.

Federal Reserve Message Loses Its Impact

Across the Atlantic, the Federal Reserve delivered a message that initially sounded firm. Interest rates were left unchanged, and Chair Jerome Powell struck a confident tone when discussing the state of the economy and the labor market. His comments suggested that policymakers see no urgent need to shift course, reinforcing the idea of a steady policy approach in the near term.

However, the market reaction told a different story. While the dollar found brief support following the Fed’s remarks, that strength quickly faded. Investors appear unconvinced that a firm stance will last throughout the year. Expectations for interest rate cuts remain firmly in place, with markets still anticipating multiple reductions before the year ends.

This disconnect between official messaging and market expectations has become a recurring theme. Each time the Fed signals patience, traders respond by focusing on signs of slowing inflation or softer economic momentum. As a result, the dollar has struggled to build lasting rallies, even after seemingly supportive statements.

Policy Talk and Political Noise Add Pressure

Comments from US officials added another layer to the dollar’s story. Treasury Secretary Scott Bessent sought to clarify recent remarks from President Donald Trump, emphasizing that the administration continues to support a strong dollar policy. While these assurances helped limit further weakness, they were not enough to spark a decisive turnaround.

The broader political backdrop continues to weigh on investor confidence. Unpredictable trade policies and repeated criticism of the Federal Reserve’s independence have raised concerns about long-term stability. These factors matter deeply for a currency that relies on trust and credibility to maintain its global role.

So far this year, the dollar has remained under pressure when measured against a broad basket of major currencies. This reflects not just interest rate expectations, but also unease about policy direction and leadership changes expected later in the year.

European Central Bank Outlook Shows Early Shifts

On the European side, interest rate discussions are becoming more nuanced. For months, European Central Bank officials have insisted that monetary policy is well positioned, signaling little urgency to adjust rates. Recently, however, that confidence has begun to show small cracks.

Some policymakers have started to openly discuss the possibility of rate cuts, a notable shift from earlier messaging. These comments suggest that while the Eurozone economy is holding up, officials remain cautious about future growth risks. Political leaders have also weighed in, warning that a weaker dollar could hurt export competitiveness for key European economies.

If the ECB moves closer to a more accommodative stance, the euro could face renewed pressure. For now, though, stronger sentiment data has helped offset these concerns, allowing the currency to consolidate rather than retreat sharply.

US Economic Data in Focus

Attention is now turning to upcoming economic releases from the United States. Data on jobless claims will offer insight into labor market conditions, a critical factor in shaping expectations for Fed policy. A rise in claims could reinforce the argument for rate cuts, while a surprise decline might give the dollar a temporary boost.

Factory orders are also on the agenda, with forecasts pointing to a rebound after a previous contraction. This data will help investors assess the health of the manufacturing sector, which has been sensitive to higher borrowing costs and shifting global demand.

Meanwhile, trade balance figures are expected to show a wider deficit. While trade data does not always move markets immediately, persistent imbalances can influence long-term currency trends, especially when combined with political rhetoric around trade policy.

Together, these releases could provide short-term direction for the dollar, but their impact may be limited unless they significantly alter expectations around monetary policy.

Why EUR/USD Remains Range-Bound

The current stability in EUR/USD reflects a market that is absorbing mixed signals. On one hand, the Eurozone is showing signs of improving confidence, supporting the euro. On the other, the US economy remains resilient enough to prevent a sharp dollar sell-off, even as rate cut expectations grow.

Neither side has delivered a decisive catalyst. Without a clear shift in central bank policy or a major economic surprise, traders appear content to wait. This has resulted in limited volatility and repeated failures to extend moves in either direction.

From a broader perspective, this pause may be healthy. After months of strong trends, markets often need time to reassess assumptions and reprice risks. The current environment reflects that reassessment in action.

Final Summary

The EUR/USD pair is moving sideways as investors balance encouraging Eurozone sentiment against ongoing uncertainty in the United States. Stronger confidence data from Europe has helped the euro hold firm, while the US dollar has struggled to regain momentum despite supportive messages from the Federal Reserve and US officials.

Market expectations for interest rate cuts, political uncertainty, and questions about central bank independence continue to weigh on the dollar. At the same time, early hints of a softer stance from the European Central Bank introduce potential risks for the euro.

With key US economic data approaching, traders are watching closely for signs that could break the current stalemate. Until then, the currency pair is likely to remain steady, reflecting a market waiting patiently for its next clear signal.

GBPUSD Strengthens as Sterling Outperforms the Dollar

The British Pound has staged a strong comeback against the US Dollar after a brief pullback earlier in the week. Buyers stepped back in quickly, helping the currency pair recover most of its recent losses and move closer to the upper end of its recent range. The rebound reflects a mix of renewed confidence in the UK economy and ongoing doubts surrounding the US Dollar’s outlook.

GBPUSD has broken the Ascending channel in downside

While short-term movements in currency markets are often driven by shifting sentiment, the broader story behind the Pound’s recovery is rooted in contrasting economic narratives on both sides of the Atlantic. The UK continues to show signs of resilience, while the US Dollar struggles to find lasting support despite firm signals from policymakers.

Why the US Dollar Remains Under Pressure

The US Dollar briefly found support after the Federal Reserve delivered a firm message on monetary policy. Officials chose to keep policy settings unchanged and presented a more optimistic view of economic conditions. On the surface, this would normally provide a boost to the currency, as it suggests confidence in growth and a cautious approach to easing.

However, the reaction in currency markets tells a different story. Instead of gaining lasting traction, the Dollar quickly gave back its gains. This suggests that traders and investors are focusing less on official statements and more on the wider political and policy environment shaping the US outlook.

One key factor weighing on the Dollar is uncertainty around future leadership at the Federal Reserve. Markets remain unconvinced that the current policy stance will last. There is a growing belief that the next phase of US monetary leadership could bring a more relaxed approach, which would reduce the Dollar’s appeal over time.

Political Noise and Policy Uncertainty

Beyond central bank decisions, broader political developments continue to cloud the Dollar’s prospects. Shifting trade policies and public criticism aimed at the Federal Reserve have raised concerns about long-term stability and independence. For global investors, confidence is just as important as interest rate policy, and recent events have done little to strengthen trust in the US framework.

Comments from senior US officials have attempted to calm nerves, particularly around currency policy and international coordination. While these remarks briefly steadied the Dollar, they were not enough to change the overall mood. The market response suggests that words alone are no longer sufficient to offset deeper concerns.

UK Data Helps Support the Pound

On the UK side, the Pound has benefited from a steady flow of encouraging economic data. Recent reports point to healthy consumer demand and improving business activity, which have reinforced confidence in the domestic outlook. These signs of strength have made Sterling more attractive at a time when alternatives look less certain.

One notable boost came from data showing rising prices in shops, which added to expectations that inflation pressures remain present. While higher prices can be challenging for households, they also reduce the likelihood of aggressive policy easing in the near term. For the Pound, this has acted as a supportive factor.

Retail activity has also played a role. Strong consumer spending suggests that households remain willing to open their wallets despite ongoing cost pressures. This resilience has helped counter fears of a sharp slowdown and has underpinned positive sentiment toward the UK economy.

Business Activity Adds to Optimism

Business surveys released recently have painted a picture of cautious optimism. Companies appear more confident than in previous months, with improvements seen across several sectors. This momentum has reassured markets that the UK is navigating its challenges better than expected.

Taken together, these factors have helped the Pound regain ground and maintain a constructive tone. While risks remain, the balance of recent data has tilted in favor of Sterling, at least for now.

Market Sentiment Favors Further Gains

Looking ahead, many observers believe the Pound could continue to perform well if current conditions persist. The combination of a resilient UK economy and a hesitant US Dollar creates a favorable backdrop for further appreciation. Rather than chasing short-term moves, market participants seem focused on the broader trend.

Analysts note that recent upward momentum reflects genuine demand rather than speculative spikes. This suggests that buyers are comfortable holding the currency, confident that underlying fundamentals offer support. As long as this confidence remains intact, the Pound is likely to stay on firm footing.

That said, markets are rarely one-directional. Periods of consolidation are a natural part of any trend, allowing investors to reassess positions and digest new information. Such phases do not necessarily signal weakness, but rather a pause before the next move.

What Could Change the Outlook

Several factors could influence the next chapter for the Pound and the Dollar. In the US, any clear shift in policy direction or leadership expectations could reshape market sentiment quickly. Similarly, unexpected changes in trade policy or fiscal plans would have a direct impact on the Dollar’s standing.

In the UK, future economic releases will be closely watched. Continued strength in consumer spending and business confidence would reinforce the positive narrative. On the other hand, signs of slowing momentum could prompt a reassessment of Sterling’s recent gains.

Final Summary

The Pound’s recent rebound against the US Dollar highlights the importance of confidence and clarity in currency markets. Despite firm signals from the Federal Reserve, the Dollar remains vulnerable due to political uncertainty and doubts about the long-term policy path. In contrast, the UK has delivered a series of supportive economic signals that have strengthened trust in Sterling.

As things stand, sentiment appears to favor the Pound, with many market participants expecting it to remain well supported in the near term. While short-term fluctuations are inevitable, the broader balance of risks currently leans in favor of the UK currency, provided economic resilience continues and uncertainty surrounding the Dollar persists.

USDJPY Pauses Near Recent Levels as Traders Await Tokyo Inflation Data

The Japanese Yen has shown signs of stability after a recent dip, drawing interest from traders who believe the currency may have fallen too far, too fast. On Thursday, the Yen managed to hold its ground against a softer US Dollar, helped by expectations that Japanese authorities could step in if weakness becomes excessive. A firmer stance from the Bank of Japan has also played a role in keeping the currency from sliding further.

USDJPY is moving in an ascending channel, and the market has reached the higher low area of the channel

Still, the Yen’s recovery has been cautious rather than confident. Deep concerns about Japan’s fiscal position, along with political uncertainty at home and a generally upbeat global mood, have made investors hesitant to fully back the currency. The result is a market that feels torn between short-term support factors and longer-term worries that refuse to fade away.

Why the Japanese Yen Is Attracting Buyers on Dips

The Yen’s recent resilience has not come out of nowhere. A mix of policy signals and official messaging has encouraged some investors to test the waters on the buying side.

Growing Expectations of Official Support

One of the strongest forces supporting the Yen has been speculation around possible action from Japanese authorities. Recent comments from government officials have made it clear that they are watching currency moves closely and are prepared to respond to what they see as extreme or speculative behavior. This message alone has been enough to slow down selling pressure, as traders remain wary of being caught on the wrong side of any sudden intervention.

There has also been quiet coordination between Japanese and US officials in monitoring currency movements. While no direct action has been confirmed, these developments have reinforced the idea that policymakers are uncomfortable with sharp swings and want to maintain stability.

A More Confident Bank of Japan

Another key factor supporting the Yen is the Bank of Japan’s increasingly firm tone. The central bank recently left interest rates unchanged but signaled confidence in the country’s economic outlook by raising its growth and inflation forecasts for the coming years. It also made it clear that further rate increases remain an option if conditions continue to improve.

This shift matters because it contrasts with the Bank of Japan’s long history of ultra-loose policy. Even a cautious move toward tighter conditions has changed how investors view the Yen, making it less attractive to sell aggressively and more appealing as a longer-term hold.

Fiscal Concerns Cast a Long Shadow

Despite these supportive elements, enthusiasm for the Yen remains limited. At the heart of this hesitation are worries about Japan’s fiscal health, which have become more prominent in recent weeks.

Debt Sustainability Under the Spotlight

Japan already carries one of the highest debt levels among major economies, and recent policy proposals have raised fresh questions about how sustainable this situation may be. The government has outlined ambitious spending plans and floated the idea of tax relief aimed at supporting households and boosting growth.

While these measures may be popular with voters, they also increase concerns about rising deficits. Investors are keenly aware that any sign of fiscal strain can undermine confidence in a country’s currency, especially over the long term.

Tax Policy Adds to Investor Unease

Plans to potentially pause or adjust consumption taxes have added another layer of uncertainty. Such moves could reduce government revenue at a time when spending demands are already high. For currency traders, this creates a dilemma: short-term stimulus may support growth, but long-term fiscal pressure could weaken the Yen’s foundations.

As a result, many market participants are choosing caution, preferring to wait for clearer signals before committing to stronger Yen positions.

Political Uncertainty Weighs on Sentiment

Politics has also played a role in keeping Yen buyers on the sidelines. With a snap election approaching, the domestic outlook has become harder to predict.

Elections and Policy Direction

Elections often bring uncertainty, and this case is no exception. Investors are trying to assess what a potential shift in political power could mean for economic policy, government spending, and Japan’s relationship with global markets. Until there is more clarity, risk-averse traders may prefer to reduce exposure or stay neutral.

Impact on Safe-Haven Appeal

The Yen is traditionally seen as a safe-haven currency, benefiting during times of global stress. However, when uncertainty is centered at home rather than abroad, that appeal can weaken. With global markets generally in a positive mood, there has been less demand for defensive assets, further limiting the Yen’s upside.

US Dollar Weakness Adds Another Dimension

The Yen’s recent performance cannot be fully understood without looking at the other side of the equation: the US Dollar. The Dollar has struggled to gain momentum amid expectations of easier monetary policy and growing political noise in the United States.

Federal Reserve Signals and Market Expectations

The US central bank recently chose to keep interest rates unchanged after cutting them several times last year. While the decision itself was widely expected, the presence of dissenting voices within the Fed highlighted internal debate about the future path of policy.

Investors now largely believe that rates will stay on hold for the near term, with the possibility of further reductions later on. This outlook has limited the Dollar’s ability to rebound in a meaningful way.

Questions Around Central Bank Independence

Additional pressure on the Dollar has come from concerns about the independence of the Federal Reserve. Ongoing political developments and public commentary about future leadership changes have unsettled some investors. When confidence in a central bank’s autonomy is questioned, it can weigh heavily on a currency.

These issues have kept the Dollar on the defensive, indirectly giving the Yen some breathing room even as domestic challenges persist.

Key Data Events in Focus

Looking ahead, traders are turning their attention to upcoming economic data that could influence short-term direction for both currencies.

US Labor Market Signals

Regular updates from the US labor market are closely watched as indicators of economic health. Any surprise in employment-related data could shift expectations around future policy decisions, potentially moving the Dollar and, by extension, the Yen.

Inflation Data from Tokyo

Inflation figures from Japan’s capital are also expected to draw interest. These numbers offer an early glimpse into national price trends and can shape views on how aggressively the Bank of Japan might act in the months ahead. Stronger inflation could support the case for tighter policy, while weaker data might revive doubts.

Final Summary

The Japanese Yen is caught between forces pulling it in opposite directions. On one side, firm messaging from the Bank of Japan and the possibility of official intervention have helped stabilize the currency and attract selective buying. On the other, deep-rooted concerns about fiscal sustainability, political uncertainty, and a favorable global risk environment continue to cap gains.

Meanwhile, a struggling US Dollar has provided some indirect support, though not enough to spark a decisive shift in sentiment. As traders await fresh economic data from both Japan and the United States, the Yen’s path forward remains uncertain, shaped by a delicate balance between policy confidence and structural concerns.

EURGBP trades steadily as attention shifts to upcoming Eurozone growth figures

The Euro–Pound exchange rate has shown a modest upward move during early European trading, reflecting a calm but watchful mood in the market. With limited economic data coming out of the United Kingdom this week, traders are paying closer attention to signals from central banks and upcoming economic reports from the Eurozone. These factors are shaping short-term sentiment and guiding expectations for both currencies.

EURGBP is moving in an ascending channel, and the market has reached the higher low area of the channel

A Quiet Start for the Pound Amid Limited UK Data

The British Pound has lacked clear direction in recent sessions, mainly because there have been few major economic releases from the UK to influence market thinking. When data is scarce, investors often turn to expectations and forward-looking statements from policymakers instead of hard numbers. This has been the case lately, with the Pound trading without strong domestic momentum.

Attention is now firmly on the next policy decision from the Bank of England. Market participants broadly expect the central bank to keep its current policy stance unchanged at its upcoming meeting in early February. This expectation has been widely shared among economists and analysts, leaving little room for surprise in the short term.

That said, expectations beyond this meeting are more mixed. Many observers believe that the central bank could begin easing policy later in the year if economic conditions allow. However, recent developments in the UK economy may complicate that path. Inflation has proven more persistent than expected, and consumer spending has shown resilience. These signs of strength suggest that policymakers may prefer to move cautiously rather than rush into changes.

As a result, while the Pound has lacked immediate drivers, it has not been without underlying support. Stronger domestic data can help limit downside risks and may act as a stabilizing force in the weeks ahead.

Eurozone Data Takes Center Stage

While the UK calendar has been relatively light, the focus is shifting toward the Eurozone. Investors are closely watching upcoming economic figures, particularly early estimates of economic growth and inflation from key member states. Data from Germany, the region’s largest economy, is expected to draw special attention.

These reports are important because they offer insight into how well the Eurozone economy is holding up amid ongoing global uncertainty. Growth figures can influence expectations about future policy decisions, while inflation data remains central to the outlook for interest rates.

The European Central Bank has maintained a steady policy approach for some time, aiming to keep inflation close to its long-term goal. Recent trends suggest that price pressures are broadly aligned with that objective, allowing policymakers to pause and assess incoming information rather than act quickly.

Still, the Eurozone faces its own set of challenges. External risks, including trade tensions and political developments outside the region, continue to hover in the background. These factors can affect confidence and, by extension, the common currency.

Central Bank Signals and Market Expectations

Central bank communication has played a key role in shaping current market sentiment. In the UK, policymakers have been careful to balance optimism about recent economic resilience with caution about declaring victory over inflation. This balanced tone has reinforced the view that any future policy adjustments will be gradual and data-dependent.

Surveys of economists suggest a strong consensus that the Bank of England will remain on hold at its next meeting. However, expectations for later in the year are less unified. Some analysts see room for gradual easing if inflation continues to cool, while others point to strong consumer demand as a reason for patience.

On the Eurozone side, officials have echoed a similar message of flexibility. Members of the European Central Bank have emphasized the importance of keeping all options open, especially in an environment marked by shifting global conditions. Rather than committing to a fixed path, policymakers appear focused on responding to changes as they arise.

Recent public comments from ECB officials have highlighted concerns about global trade and geopolitical uncertainty. These issues could affect economic growth and inflation in unpredictable ways, making flexibility a key part of the central bank’s strategy.

Global Risks and Their Impact on the Euro

Beyond domestic data and central bank policy, global developments are also influencing the Euro. Renewed trade tensions and political demands from abroad have raised questions about potential disruptions to economic activity in the region. Even when such risks do not materialize immediately, they can weigh on sentiment and limit enthusiasm for the currency.

The European Central Bank has acknowledged these uncertainties in its recent communications. Internal discussions have underscored the need to be prepared for sudden changes in the economic outlook, whether due to external shocks or shifts in global demand.

For currency markets, this means that the Euro may remain sensitive to headlines and developments beyond Europe’s borders. While stable policy and controlled inflation provide a degree of support, external risks can still create periods of volatility.

Balancing Forces in the Euro–Pound Relationship

The current relationship between the Euro and the Pound reflects a balance of competing forces. On one hand, the absence of fresh UK data has limited the Pound’s ability to gain momentum. On the other, solid economic indicators and cautious central bank messaging have helped prevent significant weakness.

Meanwhile, the Euro is navigating its own set of influences, from upcoming economic data to broader global concerns. As a result, movements in the exchange rate have been measured rather than dramatic, with traders taking a wait-and-see approach.

In the near term, upcoming data releases from the Eurozone could provide clearer direction. Stronger-than-expected figures may bolster confidence in the region’s outlook, while weaker results could reinforce concerns about growth. For the Pound, attention will remain on inflation trends and signals from the Bank of England about the pace of any future policy changes.

Final Summary

The Euro–Pound exchange rate has edged slightly higher amid a calm trading environment shaped by limited UK data and steady central bank expectations. The Bank of England is widely expected to maintain its current policy stance in the near term, with future decisions likely to depend on how inflation and consumer activity evolve. At the same time, the Euro is influenced by upcoming economic reports and lingering global risks, including trade-related uncertainties.

Both currencies are supported by cautious but flexible central bank approaches, which have helped keep movements contained. As new data emerges and global developments unfold, traders will be watching closely for signals that could tip the balance and set a clearer direction for the pair.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!