Weekly Forecast Video on Forex, BTCUSD, XAUUSD

Stay ahead in the markets with our detailed analysis of gold and forex trade setups for this upcoming week, Dec 15 to Dec 19.

XAUUSD Holds Firm as Fed Uncertainty Drags On and Global Tensions Rise

Gold (XAU/USD) eased off a seven-week high on Friday after a strong run earlier in the week. After touching a peak near $4,353, the metal drifted lower as many traders chose to lock in profits before the weekend. Even with that pullback, Gold stayed in positive territory for the week and continued to hold most of its recent gains.

XAUUSD is rebounding from the retest area of the broken Ascending channel

By late Friday, Gold was hovering around $4,302, and the mood in the market felt less like a full reversal and more like a pause. When an asset climbs quickly, it’s common for some investors to step aside, take gains, and reassess. That’s especially true heading into a weekend, when unexpected headlines can create sharp moves while markets are closed.

Still, Gold’s underlying story hasn’t changed much. Traders are weighing mixed signals from the US economy, uncertainty around the Federal Reserve’s next steps, and ongoing geopolitical tension. Together, those forces continue to shape the medium-term outlook for the metal.

Why Gold Stepped Back: Profit-Taking After a Strong Week

The most immediate reason for Friday’s dip looked simple: profit-taking. Gold had already moved higher over the week, and some investors likely decided the safest move was to reduce exposure before the weekend.

Profit-taking doesn’t always mean sentiment has turned negative. In many cases, it’s a sign that traders believe a lot of the good news has already been priced in—at least for now. After a rally, markets often need fresh reasons to push higher again. Without major new data releases on Friday, it made sense that Gold would cool off while traders waited for the next catalyst.

At the same time, Gold didn’t fall apart. It held onto most of its gains and remained supported by broader themes that have been building for weeks.

Fed Uncertainty Keeps Investors Watching Inflation Closely

A big part of Gold’s appeal right now is tied to uncertainty around US interest rates. Several Federal Reserve officials shared public comments that highlighted a familiar concern: inflation is still higher than they want, and the path forward is not perfectly clear.

Some policymakers emphasized that inflation remains “too hot,” which suggests they are not comfortable declaring victory. Others argued for patience and said they would rather wait for more evidence before committing to a specific direction. That split matters because it affects expectations about how quickly, or how aggressively, the Fed might change policy next year.

The CPI issue: not enough clear data

One complication is that key inflation data has been limited, especially the Consumer Price Index (CPI), which is one of the most closely watched measures of price growth. When CPI information is scarce or disrupted, it becomes harder to read the real trend. And when the trend is unclear, markets often become more reactive to every new comment from Fed officials.

There’s another wrinkle too: Fed Chair Jerome Powell has warned that parts of the economic data stream could be distorted by a US government closure, which can affect reporting and timing. When traders aren’t sure whether numbers reflect the real economy or temporary noise, confidence drops—and Gold often benefits from that kind of uncertainty.

US Jobs Data Sends Mixed Signals About the Economy

Alongside the Fed talk, recent US labor data has also played a role in shaping demand for Gold. A weaker-than-expected reading on jobless claims recently supported the idea that the economy may be cooling.

For the week ending December 6, initial jobless claims rose to 236,000, up sharply from the previous week’s revised 192,000. That jump caught attention because it suggests more people are filing for unemployment benefits.

But the longer-term picture wasn’t as negative. Continuing claims for the week ending November 29 fell to 1.838 million from 1.937 million, hinting that some parts of the labor market may be stabilizing.

What this means for Gold

When job data softens, some investors start thinking the Fed may eventually have room to ease policy. That expectation can help Gold because the metal often looks more attractive when rates are expected to fall or when economic momentum appears uncertain. Even when Treasury yields rise in the short term, Gold can remain supported if real yields drift lower, since real yields are closely linked to the opportunity cost of holding non-interest-bearing assets like Gold.

The US Dollar Stays Under Pressure

Gold is also influenced by the US Dollar, and the Dollar has not been strongly supportive lately. The US Dollar Index (DXY), which tracks the Dollar against a basket of major currencies, was relatively flat around 98.35 on Friday. Even when it’s not actively falling, a lack of upside momentum in the Dollar can remove a headwind for Gold.

Many global investors buy Gold as a way to reduce currency risk. When the Dollar is strong, Gold can feel more expensive for buyers using other currencies. When the Dollar is soft or directionless, that pressure often fades, which can help keep Gold steadier even during pullbacks.

Geopolitics Remains a Key Support: Russia–Ukraine Talks Stall

Beyond economics, geopolitics continues to play a major role in keeping Gold supported. Markets have been watching Russia–Ukraine peace efforts closely, and recent headlines suggest the talks are not progressing smoothly.

According to statements from the White House press secretary, US President Donald Trump is frustrated with the pace of negotiations and disappointed that Ukraine’s President Volodymyr Zelenskiy has not signed off on a US-backed peace plan. When peace talks appear to stall, markets often price in higher geopolitical risk, and Gold tends to benefit from that shift in sentiment.

Why this matters for the medium term

Even if markets don’t react wildly to each headline, the broader backdrop of ongoing conflict can keep a steady bid under Gold. Investors often turn to Gold when uncertainty rises—not only because of fear, but because the metal is widely seen as a long-term store of value during unstable periods.

What Fed Officials Are Signaling Without Saying It Directly

Fed commentary matters not only for what is said, but also for what it implies about internal debates. Recent remarks from several policymakers highlighted a key tension:

-

Some officials remain concerned inflation is not cooling fast enough and prefer policy to stay restrictive.

-

Others believe it’s better to wait for clearer evidence, especially when data may be incomplete or distorted.

XAUUSD is moving in an uptrend channel, and the market has fallen from the higher high area of the channel

-

Some see a path where inflation comes down next year as certain impacts fade, which could open the door to easing—if the economy behaves as expected.

This kind of disagreement tends to keep markets on edge. When the Fed speaks with one clear voice, investors can price expectations more confidently. When messages diverge, uncertainty rises, and Gold often becomes more attractive as a defensive holding.

Final Summary

Gold backed away from a seven-week high near $4,353 as traders booked profits ahead of the weekend, but it still held onto most of its weekly gains and stayed supported around $4,302. The bigger drivers remain in place: mixed US economic signals, uncertainty around the Federal Reserve’s next steps due to limited or distorted inflation data, and renewed geopolitical tension as Russia–Ukraine peace efforts appear to be stuck. With the US Dollar showing limited strength and investors still watching inflation and jobs data closely, Gold continues to have a supportive backdrop even as short-term pullbacks appear.

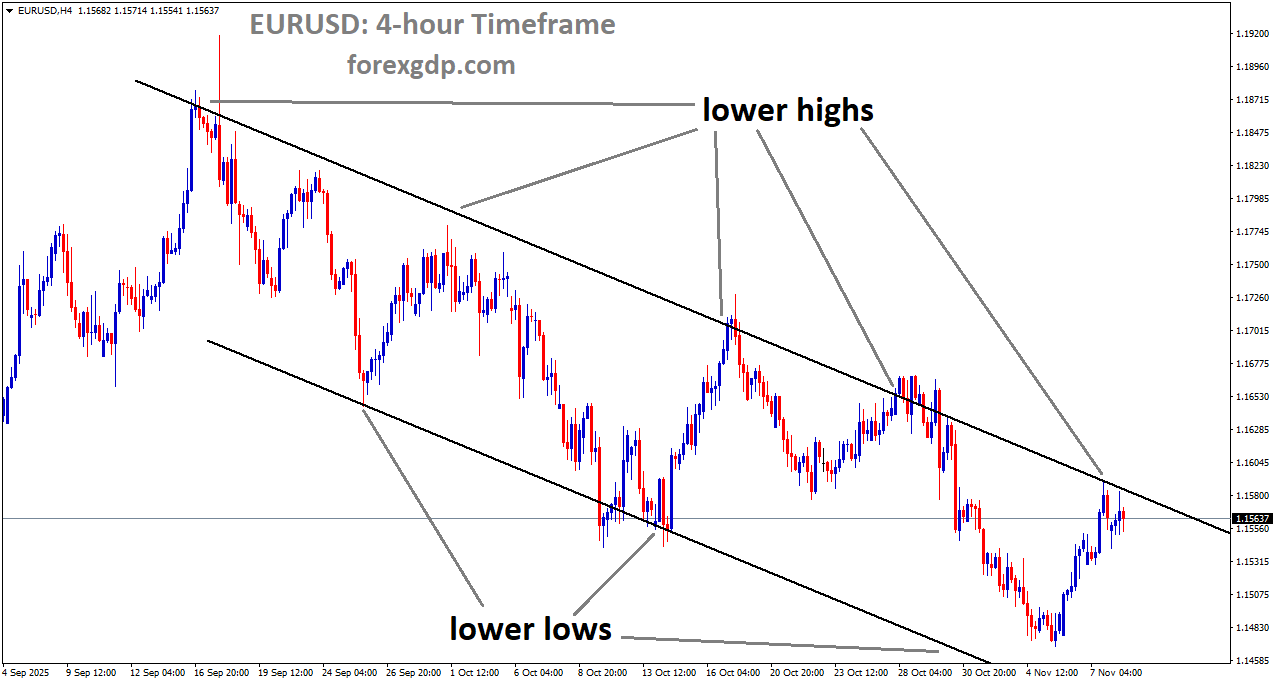

EURUSD trades flat around 1.1740 while Fed leans toward a wait-and-watch stance

EUR/USD stayed firm near 1.1741 on Friday, barely moving as a wave of Federal Reserve officials spoke publicly after Wednesday’s 25 basis point rate cut. Even though the Fed lowered rates, the overall message from policymakers has not been “easy money from here.” Instead, several officials have pushed back against overly dovish expectations and have highlighted ongoing concerns about inflation.

EURUSD is moving in an uptrend channel, and the market has reached a higher high area of the channel

The result is a market that feels stuck between two powerful forces. On one side, the Fed has started to ease. On the other, key voices inside the central bank are making it clear they are not ready to rush into additional cuts. That tug-of-war has helped keep the euro-dollar pair stable, with small swings but no dramatic break in either direction.

Why the Fed Is Talking Tough After Cutting Rates

A rate cut normally signals that a central bank is becoming more worried about growth and more comfortable with inflation. But this time, the tone from Fed officials suggests something different: the cut happened, yet the next steps are far from guaranteed.

A major reason for the caution is the lack of fresh US economic data, which has been delayed due to the US government shutdown. With fewer reliable updates on inflation, jobs, and consumer demand, policymakers are leaning toward a wait-and-see approach. In other words, they want more evidence before deciding whether additional rate cuts are truly needed.

This helps explain why EUR/USD has been slightly tilted to the upside even as some Fed comments sound hawkish. Traders are hearing two messages at once: rates were cut, but the Fed may pause and reassess rather than continue cutting at a steady pace.

Inflation Still the Main Pressure Point

For many Fed officials, inflation remains the central issue. The concern is not just whether inflation is falling, but whether it is falling consistently and in a way that supports the Fed’s long-term goal of 2% inflation. When policymakers feel inflation is still “too high,” they are less likely to commit to a quick series of rate cuts.

That’s why Friday’s commentary mattered. It wasn’t simply background noise. It was a reminder that the Fed’s internal debate is still active, and that future decisions may remain divided.

What Fed Speakers Said and Why Markets Cared

Several notable Fed names shaped the conversation, and their comments helped reinforce the idea that the central bank is moving carefully.

Cleveland Fed President Beth Hammack struck a hawkish tone, saying price pressures have been too high and stressing the Fed’s commitment to reaching its 2% inflation goal. She also pointed out that the decision was complicated and suggested policy is around neutral. That matters because “neutral” is often seen as a point where rates are neither strongly restricting the economy nor strongly stimulating it. If the Fed believes it is close to neutral, it may feel less urgency to cut further.

Chicago Fed President Austan Goolsbee, who dissented at the December meeting, defended his position by saying the Fed should have waited for more information—especially on inflation. His point was simple: if the Fed had waited until the first quarter of 2026 for cuts, it could have been more confident that inflation was truly heading lower. Whether or not markets agree, the message is clear: some policymakers would rather move slowly than risk cutting too early.

Kansas City Fed President Jeffrey Schmid also dissented, explaining that not much has changed in the economy since October, when he previously dissented as well. He added that he continues to hear inflation concerns from people across his district. That kind of real-world feedback often carries weight because it suggests inflation anxiety is not limited to economists or market watchers—it’s being felt in daily business and household decisions.

Philadelphia Fed President Anna Paulson offered a different angle. She said she does not see tariffs turning into broad, widespread price increases. Instead, she is more concerned about risks to jobs than inflation. Her comments show that not every Fed voice is focused on inflation in the same way. Some are looking at the labor market and wondering if the bigger risk could shift toward employment.

Taken together, these views help explain why investors are treating the next Fed move as uncertain. The cut has happened, but the follow-through is not guaranteed. The policy debate is still alive, and the lack of timely economic data makes it harder for the Fed to settle that debate quickly.

Europe’s Inflation Picture Looks Mixed

While the US story is about delayed data and a divided Fed, Europe is dealing with mixed inflation signals across key countries.

In Germany, the Harmonized Index of Consumer Prices (HICP)—the inflation gauge closely watched by the European Central Bank—fell 0.5% month over month in November, matching expectations and lining up with October’s reading. On a yearly basis, German HICP held at 2.6%, also in line with forecasts.

Spain, however, told a slightly different story. Spanish HICP rose 3.2% year over year, coming in above estimates and slightly higher than October’s 3.1%. This kind of split matters because the Eurozone is not a single economy. Stronger inflation in one country can complicate the broader picture and can make it harder to talk about inflation trends as if they are uniform.

For EUR/USD traders, mixed inflation data can create a push-and-pull effect. Softer inflation readings can reduce pressure on the ECB, while higher readings can keep inflation concerns alive. When the data sends mixed signals, the euro often takes its cues from whichever story feels more dominant in the moment—especially when US factors are also uncertain.

How the Data Mix Shapes Expectations

When Germany’s inflation looks stable and Spain’s looks hotter, it can lead to several interpretations:

-

Inflation may be easing in some parts of the Eurozone but not everywhere.

-

The ECB may feel comfortable staying cautious rather than pivoting sharply.

-

Markets may focus more on the US side if Europe’s signals remain uneven.

In this environment, EUR/USD can hold steady even when headlines are active, because traders see reasons to hesitate on both sides of the pair.

What Traders Are Watching Next

With the Fed signaling patience and US data delayed, attention naturally shifts to what comes next. Markets tend to react most strongly when they see clear proof that inflation is cooling or that growth is weakening. But when key data is missing or delayed, traders often lean more heavily on central bank commentary—and that can lead to choppy, directionless trading.

At the same time, EUR/USD has stayed resilient. That resilience suggests markets are not fully buying the idea of an aggressive pause, even with hawkish voices speaking up. Instead, many investors appear to be waiting for confirmation from upcoming reports once the data flow returns to normal.

On the European side, inflation remains a story with different chapters in different countries. That means each new release can influence expectations, especially if it supports the idea that inflation is settling closer to levels the ECB can tolerate.

A Note on Key Market Attention Points

Even without diving into market mechanics, it’s fair to say traders are focused on:

-

When US economic releases return and what they show about inflation and jobs

-

Whether Fed officials continue to emphasize inflation risks or start shifting toward growth concerns

-

How Eurozone inflation evolves across major economies like Germany and Spain

Final Summary

EUR/USD remained steady near 1.1741 as Fed officials spoke after a 25 basis point rate cut, with several policymakers stressing that inflation concerns are still real and that the Fed is likely to take a cautious, wait-and-see approach. Delayed US data due to the government shutdown has made the Fed even more hesitant to signal a clear next step. In Europe, inflation readings were mixed: Germany’s figures matched expectations, while Spain’s came in higher, adding nuance to the Eurozone outlook. With uncertainty on both sides, markets are now looking ahead to fresh data and the next round of central bank guidance to clarify the path forward.

GBPUSD retreats with fresh UK data showing another GDP dip

The Pound Sterling has come under pressure after fresh data showed the UK economy shrank again. For many people, the headline matters because it shapes expectations for what the Bank of England does next—and that can influence everything from business confidence to borrowing costs and currency demand.

GBPUSD is moving in an uptrend channel, and the market has reached a higher low area of the channel

The latest update shows the UK’s Gross Domestic Product (GDP) dipped by 0.1% in October, marking the second month in a row of mild contraction. Markets had been looking for a small rise instead, so the surprise has pushed traders to rethink the near-term outlook for the Pound.

What the latest UK GDP report is really saying

When GDP turns negative for back-to-back months, it raises questions about momentum. A single soft month can happen for many reasons. Two in a row makes people pay closer attention, especially when households and businesses are already watching costs and demand.

The October result was especially awkward because it landed soon after a more upbeat set of official forecasts. The UK’s Office for Budget Responsibility (OBR) had recently raised its growth projection for the year, pointing to a stronger overall picture than earlier estimates suggested. This new GDP miss doesn’t automatically erase that upgrade, but it does challenge the idea that growth is moving steadily in the right direction.

If you’re wondering why currencies react so quickly to a small GDP change, it’s because exchange rates don’t just reflect where an economy is today. They reflect where investors think it’s going—particularly through the lens of interest rates.

A mixed set of signals inside the same release

While the overall GDP number disappointed, parts of the report were more encouraging.

-

Industrial Production rose on the month, beating expectations and bouncing back from a sharp drop in the prior reading.

-

On a yearly basis, Industrial Production still contracted, but it was not as weak as many forecasts had predicted.

-

Manufacturing Production increased, though it came in below what economists were looking for after a decline in the previous month.

The takeaway is simple: the UK economy is not falling apart, but it isn’t showing consistent strength either. That “stop-start” feel is exactly what makes the next Bank of England meeting so important.

Why a weak growth streak fuels Bank of England rate-cut expectations

Soft growth often puts pressure on central banks to support the economy. When activity slows, businesses can scale back investment and hiring, and consumers may become more cautious. Lower interest rates can, in theory, help by reducing borrowing costs and improving financial conditions.

Right now, traders are leaning toward the idea that the Bank of England could deliver a quarter-point rate cut at its upcoming policy decision. That expectation has been building, and another negative GDP print adds weight to the argument.

Of course, a rate cut is never based on GDP alone. Policymakers also look closely at inflation trends, wage growth, consumer demand, and financial stability. But when growth data repeatedly comes in weak, it becomes harder to justify keeping policy tight—especially if inflation is no longer accelerating.

Why the Pound often reacts before the Bank of England moves

Currencies tend to move on expectations, not just decisions. If investors become more confident that interest rates are heading lower, they may reduce exposure to that currency ahead of time. That can push the Pound down against other major currencies, particularly those where rate cuts appear less urgent or less likely.

This is why next week’s UK data calendar matters so much. It can either reinforce the case for a cut—or complicate it.

The next set of UK data that could swing the Pound’s outlook

The Pound’s short-term direction is likely to be driven by how the next batch of UK reports shapes the Bank of England narrative. Several high-profile releases are scheduled, and each one speaks to a different part of the economy.

UK labour market data

Jobs data for the three months ending October will be watched closely. Investors will look for signs of cooling hiring, changes in unemployment, and—most importantly—wage pressures. If wage growth stays sticky, the Bank of England may feel less comfortable cutting quickly. If hiring slows and pay growth cools, rate-cut expectations could strengthen.

UK Consumer Price Index

Inflation remains a central theme for any rate decision. The November CPI release will help define whether price pressures are easing in a way that gives policymakers room to reduce rates. A softer inflation print can support the argument for lower rates. A hotter one can delay it.

Early reads on business activity

Preliminary Purchasing Managers’ Index (PMI) data for December offers an early snapshot of how businesses are feeling as the year wraps up. PMIs can influence sentiment because they often hint at whether companies are expanding, holding steady, or pulling back.

Put together, this data set can change the conversation fast. One or two strong surprises could steady the Pound. A run of weaker numbers could keep pressure on it.

The US angle: why American jobs data matters for GBP and the US Dollar

The Pound’s performance isn’t only about the UK. It also depends on what’s happening in the United States, because the US Dollar is the world’s dominant currency and a major driver of global trading flows.

Recently, the Federal Reserve has moved toward a more supportive stance by lowering interest rates and suggesting the pace of future cuts may be limited. That guidance matters because it shapes how investors compare the US Dollar to other currencies, including the Pound.

At the same time, political commentary in the US has added noise to the rate outlook, with calls for additional cuts from the White House after the Fed’s decision. Markets don’t treat political statements as policy, but they can influence expectations at the margins—especially when they align with a broader narrative about growth and inflation.

US Nonfarm Payrolls as the next major test

The next big catalyst for the US Dollar is the Nonfarm Payrolls (NFP) report for November. Jobs data carries extra weight when markets believe a central bank is responding to changes in labour demand.

If the US jobs report shows clear weakness—slower hiring, rising unemployment, or softer wage growth—investors may lean toward a more dovish Fed outlook. That can weigh on the US Dollar. If the report is stronger than expected, it may support the Dollar by reducing the urgency for more cuts.

For GBP watchers, this matters because currency moves are often relative. The Pound can fall because the UK looks weaker, or it can rise if the US Dollar loses ground. Often, it’s a mix of both.

What all of this means for everyday watchers of the Pound

If you’re tracking Sterling for travel, business payments, or general interest, the key theme is uncertainty around growth and rates. The UK economy posting two straight monthly declines doesn’t guarantee a downturn, but it does suggest the recovery is not yet on solid footing. That’s why traders are increasingly focused on whether the Bank of England will start easing policy.

Meanwhile, the US side of the equation is still in play. With the Federal Reserve watching inflation and employment closely, the next jobs report could quickly change market mood—and pull major currencies with it.

Final Summary

The Pound Sterling has weakened after UK GDP fell by 0.1% in October, extending a second straight month of contraction and missing expectations for modest growth. The data adds momentum to market bets that the Bank of England could deliver a quarter-point rate cut at its next meeting. While parts of the output report were mixed—Industrial Production improved, but Manufacturing was softer than hoped—the overall picture points to uneven economic momentum. Next week’s UK labour market figures, inflation data, and early business activity readings will be central to the Pound’s direction. On the global side, attention also shifts to US employment data, especially Nonfarm Payrolls, which could reshape expectations for Federal Reserve policy and influence the US Dollar’s broader tone.

USDJPY rebounds close to 156 as markets balance Fed easing and BoJ tightening hopes

The USD/JPY pair climbed back toward the 156.00 level on Friday, ending a two-day slide. This rebound happened during the European trading hours, and it came at a time when the Japanese Yen was weaker against many major currencies.

What makes the move interesting is that traders are still widely expecting the Bank of Japan (BoJ) to raise interest rates at its policy meeting next week. Normally, rate hike expectations can support a currency. But in the real world, exchange rates are driven by more than one story at a time—and right now, the yen is dealing with mixed signals and shifting market positioning.

USDJPY is moving in an uptrend channel, and the market has reached a higher low area of the channel

At the same time, the US Dollar has been under some pressure after the Federal Reserve lowered interest rates earlier this week. Even with that headwind, USD/JPY still managed to recover, showing how much day-to-day currency moves can be influenced by relative strength, sentiment, and what investors believe comes next.

Why the Yen Is Struggling Even With a BoJ Rate Hike in View

One of the key drivers behind the day’s price action is broad yen underperformance. That can sound confusing when investors are also talking about a BoJ rate hike next week. But a weaker yen does not automatically mean traders have abandoned the rate hike idea. Instead, the market may be reacting to uncertainty about how aggressive the BoJ can really be over time.

Inflation expectations are supporting a more hawkish BoJ

The core reason behind stronger confidence in a BoJ rate increase is the belief that inflation in Japan is moving in a direction that allows policymakers to pursue a more normal interest rate path. Investors are focused on the idea that inflation can hold near the central bank’s 2% goal in a more sustainable way.

If inflation stays close to target without falling back sharply, it gives the BoJ more room to lift rates and adjust policy settings. That expectation has been one of the main pillars supporting “hawkish” bets on Japan in recent months.

Ueda’s comments added caution to the longer-term outlook

Even so, traders are not looking only at whether a hike might happen next week. They also care about what the BoJ might do after that.

BoJ Governor Kazuo Ueda recently signaled that the central bank is still open to raising rates, but he also pointed out a major limit: there is uncertainty about how far rates can ultimately go. That kind of message matters a lot in currency markets because it shapes the long-term interest rate gap between Japan and other countries.

In other words, markets can price in a near-term hike while still doubting that Japan will move to a high-rate environment anytime soon. When that doubt grows, it can reduce support for the yen—even if the next policy step looks more hawkish on paper.

The Fed Cut Rates, and That Shifted the Dollar’s Tone

While Japan’s policy outlook is one side of the equation, the other side is the United States. This week, the Federal Reserve reduced interest rates by 25 basis points, taking the policy rate down to a 3.50%–3.75% range.

That decision put some pressure on the US Dollar because lower interest rates can reduce the return investors earn from holding dollar-based assets. But the market reaction was not just about the cut itself—it was also about the guidance that followed.

Forward guidance mattered as much as the cut

The Fed also signaled that it still expects one more rate cut in 2026. Before the announcement, some investors had expected the Fed to lean more cautious and suggest no further cuts ahead. Since that did not happen, traders adjusted expectations and repositioned.

This kind of shift is important for USD/JPY because the pair is highly sensitive to how investors compare US and Japanese interest rate paths. Even when the dollar is generally softer after a Fed cut, USD/JPY can still bounce if the yen is weaker at the same time or if markets believe Japan’s tightening cycle will be limited.

What Traders Are Watching Next in the US

With the latest central bank moves mostly known, attention now turns to upcoming US economic data. These reports can quickly reshape expectations about whether the Fed may stay on a steady path or shift its thinking again.

The next major spotlight is the US Nonfarm Payrolls (NFP) report for November, due on Tuesday. On the same day, investors will also track US Retail Sales data for November and preliminary S&P Global Purchasing Managers’ Index (PMI) figures for December.

Why Jobs Data Has a Big Impact on USD/JPY

Among the upcoming releases, the employment report may have the strongest influence on short-term market expectations. That is because job trends provide a direct clue about whether the US economy is cooling, holding steady, or re-accelerating.

Labour demand is the key message investors want

Investors will focus closely on what the jobs numbers suggest about labor demand. Strong hiring can indicate that companies still feel confident and that growth is holding up. Slower hiring can suggest that conditions are easing, which may support the idea of more rate cuts down the road.

For the dollar, this matters because rate expectations often move in response to employment momentum. A surprisingly strong jobs report can make markets more cautious about future cuts, potentially supporting the dollar. A weaker report can do the opposite and add pressure to the greenback.

For USD/JPY specifically, the relationship can become even more interesting when it overlaps with the BoJ story. If the US data comes in soft while the BoJ looks ready to hike, the pair could face different forces pulling in opposite directions. If the US data is strong while Japan’s rate outlook looks limited beyond the next meeting, the dollar side may regain the advantage.

Summary

USD/JPY rebounded toward 156.00 on Friday as the Japanese yen weakened broadly, even though markets still expect the Bank of Japan to raise interest rates next week. Confidence in BoJ tightening is supported by the view that inflation can remain near the 2% target, but Governor Ueda’s comments also highlighted uncertainty about how far rates can rise over time. Meanwhile, the US Dollar has been pressured after the Federal Reserve cut rates by 25 basis points to 3.50%–3.75% and pointed to another potential cut in 2026. Next, traders will focus on key US data—especially Nonfarm Payrolls, Retail Sales, and PMI figures—to judge labor demand and reassess the outlook for Fed policy, which can quickly influence the direction of USD/JPY.

USDCAD pressured as central bank paths diverge between Canada and the US

The Canadian Dollar has stayed on solid ground against the US Dollar as markets sort through two very different messages from North America’s central banks. On one side, the Bank of Canada (BoC) is signalling patience and stability. On the other, the US Federal Reserve has moved again, trimming interest rates and putting fresh pressure on the Greenback.

USDCAD is moving in an uptrend channel, and the market has reached the higher low area of the channel

By Friday, that contrast was still shaping currency trading. The USD/CAD pair hovered around 1.3760, marking its weakest point since mid-September. It also put the pair on track for a third straight weekly drop, helped by broad softness in the US Dollar and steady demand for the Canadian currency.

What’s driving the move isn’t one single headline. It’s the growing gap between what investors think the BoC will do next and what they think the Fed might do next. And with new data just around the corner, traders aren’t treating this week’s decisions as the end of the story—more like the start of the next chapter.

Bank of Canada Signals Rates May Stay Put for a Long Time

The BoC kept its policy rate unchanged at 2.25%, which was widely expected. But what mattered more than the decision itself was the tone behind it. Policymakers suggested the current level is “about the right” setting, pointing to inflation sitting near target and an economy that still shows signs of resilience.

That kind of messaging naturally supports the Canadian Dollar. When a central bank looks comfortable with its current stance and doesn’t hint at near-term cuts, investors tend to see the currency as relatively stable. In a market that constantly compares one country’s outlook to another’s, “steady” can be a competitive advantage—especially when the other central bank is actively cutting.

A major takeaway from the BoC meeting is that markets are increasingly comfortable with the idea that rates could remain unchanged well into 2026. In other words, Canada may be entering a longer “pause” period than many traders were assuming earlier in the year.

Could the BoC Eventually Turn Toward Higher Rates?

While the base case still leans toward a long hold, some analysts are beginning to talk more openly about what could bring rate hikes back into the conversation.

Economists at the National Bank of Canada have suggested that the BoC could keep rates steady through at least the first half of next year. At the same time, they adjusted their expectations for when hikes might begin, pointing to the fourth quarter of 2026 rather than early 2027.

That shift may sound small, but it reflects an important idea: if the labour market tightens again and inflation stays firm, the BoC may eventually need to lean in the other direction. This doesn’t mean hikes are around the corner, but it does suggest that the long-term risk isn’t only about cuts.

They also highlighted the kind of conditions that could change the timeline:

-

If unemployment continues to decline and inflation remains stubbornly strong, the BoC could tighten sooner than expected.

-

If labour-market conditions weaken or trade uncertainty returns, rate hikes could be pushed further out.

Trade policy is one of those wild cards that can move markets quickly. The upcoming 2026 USMCA review is already on some analysts’ radar. Anything that threatens confidence in cross-border trade can affect investment, hiring plans, and overall economic momentum—factors central banks watch closely.

Canada’s CPI Becomes the Next Major Test for Market Expectations

With the BoC decision now absorbed, the next big event for Canadian Dollar traders is Canada’s Consumer Price Index (CPI) report due Monday. Inflation data is often the fastest way to reset expectations because it goes straight to the heart of central bank decision-making.

If CPI shows inflation staying comfortably controlled, it strengthens the argument for the BoC to stay on hold without needing to react quickly. If inflation comes in firmer than expected, it can revive the idea that the BoC might eventually have to tighten—especially if economic activity remains resilient.

In practical terms, this CPI release could influence how markets price Canada’s interest-rate outlook into 2026. Traders aren’t just thinking about next month; they’re constantly trying to map out the path ahead. Even small changes in that path can shift currency demand.

Federal Reserve Cuts Rates Again, Adding to US Dollar Pressure

While Canada stayed steady, the Federal Reserve moved in the opposite direction. The Fed lowered interest rates by 25 basis points this week, bringing the target range for the federal funds rate down to 3.50%–3.75%.

Rate cuts often weaken a currency because they reduce the return investors can earn from holding assets priced in that currency. That’s one reason the US Dollar has struggled, especially when compared against currencies backed by a more stable policy outlook.

The Fed’s message wasn’t overly dramatic. Policymakers acknowledged that risks remain on both sides of their dual mandate—keeping inflation under control while supporting maximum employment. They also stressed that future decisions will depend on incoming data rather than a fixed path.

Still, markets took the overall tone as less hawkish than some had expected. That matters, because in currency trading, the “surprise” is often more important than the headline. If investors were bracing for tougher language and didn’t get it, the US Dollar can lose momentum quickly.

Inside the Fed: Not Everyone Agreed on the Cut

An interesting detail from this week was the internal disagreement. Chicago Fed President Austan Goolsbee dissented against the rate cut, and on Friday he explained why. He said he preferred waiting for more clarity—especially on inflation—before easing further.

Goolsbee’s comments reflected a cautious mindset shaped by the inflation shocks of recent years. He indicated he still believes rates can come down meaningfully over the next year, but he’s wary about moving too quickly and cutting too aggressively upfront.

He also noted that most incoming data still points to stable economic growth, with the labour market showing only moderate cooling. That suggests the Fed’s next moves may not be automatic. The central bank may remain flexible, weighing each new report carefully before committing to additional cuts.

What This Policy Split Means for USD/CAD in the Near Term

With the BoC leaning toward a prolonged pause and the Fed cutting rates, the policy gap has become a key theme for the USD/CAD pair. When one side is holding and the other is easing, the currency backed by the steadier stance often gains an edge—at least until the data changes the story.

For now, traders are watching two main forces:

-

Canadian data, especially inflation, to confirm whether the BoC can stay comfortably on hold.

-

US data, to determine whether the Fed is likely to keep cutting or slow down and reassess.

This is why the market keeps repeating one phrase: “guided by incoming data.” It’s not just central bank language—it’s the reality traders are operating in right now.

Summary: The Canadian Dollar Benefits From Steady Policy and Shifting US Expectations

The Canadian Dollar has remained supported as markets compare the BoC’s steady stance with the Fed’s latest rate cut. Canada’s central bank signalled comfort with current policy settings, reinforcing expectations of a long pause that could stretch into 2026. Meanwhile, the Federal Reserve’s move lower—and a tone markets read as less hawkish than expected—has weighed on the US Dollar. Attention now turns to Canada’s CPI report and upcoming US data for the next clues on where policy goes from here.

USDCHF Hovers Around 0.7950 with Investors Betting on Deeper Fed Cuts Next Year

USD/CHF is struggling to find its footing, and the main reason is simple: traders are starting to believe the US Federal Reserve could turn more dovish in 2026 than officials are currently signaling. That gap between what markets expect and what the Fed has communicated is keeping the US Dollar on the defensive, and it’s making the Swiss Franc look relatively steady by comparison.

USDCHF is moving in a symmetrical Triangle pattern, and the market has reached the higher low area of the pattern

During Friday’s European session, the pair hovered near 0.7950 and still looked fragile. While day-to-day moves can be driven by headlines and short-term positioning, the bigger story here is about where interest rates might be headed next year and how investors are preparing for that possibility.

Why Fed expectations are weighing on the US Dollar

The US Dollar often strengthens when investors think US interest rates will stay high for longer. It can also weaken when markets expect rate cuts, because lower rates generally make a currency less attractive to hold. Right now, a lot of attention is on what the Fed might do in 2026.

Many traders are positioning for more easing than the Fed has officially projected. Based on probabilities tracked by the CME FedWatch tool, markets are assigning a meaningful chance that the Fed could deliver at least two rate cuts through October 2026. That kind of expectation tends to press down on the Dollar, especially if it grows stronger over time.

What complicates the picture is the contrast with the Fed’s own messaging. The Fed’s dot plot—an interest rate projection summary from policymakers—suggested the federal funds rate could drift lower to around 3.4% by the end of 2026, implying a more limited pace of cuts than some investors are anticipating. When market pricing and central-bank guidance are not aligned, currencies can become choppy, and USD/CHF is a good example of that tension.

What markets thought the Fed would do

Before the latest policy decision, some participants expected the Fed to pause its easing cycle. That expectation matters because a “pause” would hint that the central bank is comfortable staying restrictive for longer, which typically supports the Dollar. But the Fed ultimately delivered a 25-basis-point rate cut, bringing the policy rate down to a 3.50%–3.75% range.

Even when a move is widely expected, the direction of the next steps often matters more than the step that just happened. If traders believe the Fed will keep cutting in the future, they may continue to sell the Dollar into rallies.

The US Dollar Index is trying to stabilize

One way to see the pressure on the Dollar is through the US Dollar Index (DXY), which compares the Greenback against a basket of major currencies. The index recently touched a fresh seven-week low near 98.15, showing that selling pressure is not limited to one currency pair.

That broader weakness can spill into USD/CHF because the pair is heavily influenced by overall Dollar sentiment. When the Dollar is losing support across the board, USD/CHF often has a hard time sustaining recoveries, even if the Swiss Franc is not aggressively strengthening.

Switzerland holds steady as the SNB keeps rates at 0%

While the US side of the story is about shifting expectations, Switzerland’s latest update was about staying the course. The Swiss National Bank (SNB) held its interest rate at 0%, which matched what most investors anticipated. That decision helped keep the Swiss Franc relatively calm after an earlier burst of volatility.

The SNB also repeated an important point: the threshold for returning to negative rates remains very high. This matters because negative rates were a defining feature of Swiss monetary policy for years, and markets still pay close attention to any hint that the SNB might consider going down that road again. By emphasizing that negative rates are not an easy option, the SNB helped reduce fears of extremely aggressive easing.

At the same time, the central bank maintained a dovish tone by acknowledging that its stance could support inflation and economic growth in the coming quarters. In other words, Switzerland is not trying to create a “tight money” environment right now. It is aiming for stability, and that steadiness can make the Swiss Franc feel like a calmer alternative when US rate expectations are shifting.

Why SNB messaging matters for USD/CHF

USD/CHF is not only about the Dollar. It is also about how investors view Switzerland as a financial safe place. When global uncertainty rises or risk appetite fades, the Swiss Franc often attracts demand because of Switzerland’s reputation for stability. Even without dramatic SNB action, the Franc can gain strength if markets become cautious.

In this case, however, the Franc has been broadly stable, and the main push on the pair is coming from the Dollar side rather than a surge in Swiss Franc buying.

All eyes now turn to US Nonfarm Payrolls

The next major catalyst for USD/CHF is the US Nonfarm Payrolls (NFP) report for November, scheduled for release on Tuesday. Jobs data can shift market expectations quickly because it influences how traders think about growth, inflation, and the Fed’s next moves.

A strong NFP number can support the Dollar if it suggests the economy remains resilient and inflation pressures could persist. That would make additional rate cuts feel less urgent. On the other hand, weaker employment data can add fuel to the idea of faster or deeper cuts in the future, which could keep the Dollar under pressure.

What investors are really looking for in NFP

It’s not just about the headline job gain number. Markets often react to the overall mix of details: hiring momentum, the unemployment rate, and wage growth. Even if job creation looks solid, cooling wage trends can still point to easing inflation pressure. And if unemployment ticks higher, traders may interpret it as a sign that the labor market is losing some strength.

Because rate expectations are such a key driver right now, NFP has the potential to push USD/CHF in either direction, depending on how the data lines up with the current narrative.

What this means for everyday traders and investors

If you follow USD/CHF closely, the current environment can feel tricky. The pair is being pulled by expectations about where US policy is going over a long horizon, while Switzerland is sending a message of stability and caution. That creates a situation where small changes in Fed-related assumptions can have outsized impact.

For longer-term investors, this is a reminder that currency moves often come from relative policy paths, not just single decisions. The Fed cutting rates while the SNB holds steady changes the interest-rate gap between the two countries, and that gap is one of the forces that can influence currency demand over time.

For shorter-term traders, scheduled data like NFP becomes even more important because it can reshape market pricing quickly—especially when the market and the central bank are not perfectly aligned.

Summary

USD/CHF remains under pressure as traders lean toward a more dovish Fed outlook for 2026 than policymakers have projected so far. The Fed’s recent 25-basis-point cut and the ongoing debate about how many cuts could follow have weighed on the US Dollar, with the broader Dollar Index also reflecting that weakness. Meanwhile, the Swiss National Bank kept rates at 0% and reinforced that negative rates are a high bar, helping the Swiss Franc stay relatively steady. The next big focus is the US Nonfarm Payrolls report, which could reshape expectations for the Fed’s future moves and set the tone for where USD/CHF goes next.

AUDUSD Holds Firm as Markets Await Fresh Business Surveys and Key US Inflation Data

The Australian Dollar is ending the week on solid ground against the US Dollar, with AUD/USD still looking supported as the greenback remains under pressure. After a busy few days of central bank decisions, traders are now stepping back, reassessing what those signals really mean for interest rates in the months ahead, and positioning for the next round of major economic updates.

AUDUSD is moving in a box pattern

On Friday, the pair hovered near 0.6656, settling after a brief dip toward 0.6632. That small pullback didn’t last long, and the broader tone suggests buyers are still comfortable stepping in when the price softens. If the current trend holds through the final sessions, AUD/USD is set to record a third straight weekly gain, helped by a growing gap between Australian and US monetary policy paths.

Why AUD/USD Is Finding Support This Week

In currency markets, it often comes down to one simple question: where can investors earn better returns with less risk? Interest rates are a major part of that story, and right now, Australia and the United States are moving in different directions.

The Reserve Bank of Australia (RBA) chose to keep its cash rate unchanged at 3.60%, extending its pause for the third meeting in a row. The message from the RBA remained careful and measured. It’s not rushing to declare victory over inflation, and it’s not eager to shift policy without clearer evidence from the data.

The Federal Reserve, however, moved the other way. It delivered another 25 basis point rate cut, bringing the federal funds rate down to the 3.50%–3.75% range. It was the Fed’s third cut this year, reinforcing the view that the United States is now in a phase of gradual easing, even if officials are still keeping their options open.

That difference matters because it changes expectations about where rates are heading next—and those expectations can move currencies just as much as the rate decisions themselves.

Monetary Policy Divergence Is Doing the Heavy Lifting

One of the biggest drivers behind the Aussie’s resilience is the widening divergence between the RBA and the Fed.

RBA: Patient, cautious, and guided by the data

Markets are increasingly leaning toward the idea that the RBA will stay on hold for a while. Inflation risks have not completely faded, and that makes the central bank hesitant to start cutting too early. Some traders are even building a longer-term scenario where Australia’s next meaningful move could be a hike much later on—potentially in 2026—if inflation proves stubborn.

That doesn’t mean a rate hike is around the corner. But it does suggest the market isn’t expecting quick and steady rate cuts from the RBA the way it often would when growth slows. This “higher for longer” thinking—whether fully correct or not—can be supportive for the Australian Dollar.

Fed: Easing has begun, even if officials aren’t fully aligned

In the US, the market continues to expect more easing ahead. Even with limited forward guidance, traders are still leaning toward the possibility of two additional cuts next year. That expectation keeps the US Dollar from regaining its footing, especially when investors start comparing rate outlooks across major economies.

Put simply: if the Fed is cutting while the RBA is holding, the interest-rate gap can shift in a way that helps AUD/USD stay supported.

Fed Officials Signal Caution Despite the Rate Cut

Even though the Fed cut rates again, the tone inside the central bank is not completely unified. Recent comments from Fed officials highlighted ongoing debate about whether easing is happening too soon.

Two regional Fed presidents—Austan Goolsbee (Chicago Fed) and Jeffrey Schmid (Kansas City Fed)—dissented against the latest cut. Their views offered a reminder that while the Fed is moving toward easier policy, some policymakers remain uneasy about inflation and the broader strength of the economy.

Goolsbee suggested he would rather wait for more clarity, especially on inflation trends, before taking additional steps. He pointed to economic data that still show steady growth and only moderate signs of cooling in the labor market. In other words, from his perspective, the economy may not yet require more support.

Schmid took a similar stance, arguing that conditions have not changed much since the prior meeting. He also noted that monetary policy may only be modestly restrictive—if restrictive at all—because the economy still shows momentum and inflation remains higher than desired.

This kind of pushback can matter. When investors hear dissent and caution, they may start questioning how fast rate cuts will really come. Still, the fact remains that the Fed has already moved three times this year, and that shift is weighing on the US Dollar overall.

What Traders Are Watching Next Week

With the week’s major central bank events now behind us, attention is quickly shifting to incoming economic data. For AUD/USD, next week is important because it brings several high-impact reports from both Australia and the United States—exactly the kind of information that can reshape rate expectations and drive currency moves.

Australian and US PMIs will set the early tone

On Tuesday, markets will watch preliminary S&P Global PMI readings from both Australia and the US. These surveys offer a timely snapshot of business conditions and can influence sentiment quickly because they arrive earlier than many other indicators.

-

If Australia’s PMI data shows steady demand and resilience, it can reinforce the idea that the RBA can afford to stay patient.

-

If US PMIs soften, it can strengthen the market’s belief that the Fed will keep easing.

Neither outcome is guaranteed, but together these reports can shape the mood early in the week.

US Nonfarm Payrolls, Retail Sales, and CPI take center stage

The bigger spotlight will likely remain on the United States, where several major releases are scheduled:

-

Nonfarm Payrolls (NFP) reports for October and November: Jobs data is one of the most closely watched signals for the Fed. Strong hiring can suggest the economy is still running hot, while softer results may support the case for further rate cuts.

-

Retail Sales on Tuesday: Consumer spending is a key engine of the US economy. A strong reading can signal confidence and growth, while weakness may point to a slowdown.

-

Consumer Price Index (CPI) on Thursday: Inflation remains the deciding factor for many central banks, and CPI is one of the Fed’s most important reference points. If inflation proves sticky, expectations for future cuts could cool. If it continues to ease, the market may lean more strongly toward additional rate reductions.

For AUD/USD traders, these releases aren’t just headlines. They directly influence how investors think about the Fed’s next steps—and that can quickly shift the balance between the Aussie and the greenback.

What This Means for AUD/USD Moving Forward

Right now, the Australian Dollar is benefiting from two key forces working together: a softer US Dollar and a growing contrast in rate expectations between the RBA and the Fed. The pair’s ability to stabilize after brief dips also suggests market confidence hasn’t disappeared, even after a week filled with major policy decisions.

Still, next week’s data will be crucial. If US inflation or jobs data surprises in a way that changes expectations for rate cuts, the US Dollar could find support again. On the other hand, if the US numbers point to slowing momentum and easing price pressures, the greenback could remain under pressure, keeping AUD/USD supported.

Summary

AUD/USD is holding firm as the US Dollar remains weak and markets digest the latest signals from both central banks. The RBA’s steady stance contrasts with the Fed’s third rate cut this year, widening the policy gap and helping the Aussie stay supported. With that chapter largely closed, traders are now focused on next week’s key data, including Australian and US PMIs, US Nonfarm Payrolls, Retail Sales, and CPI—reports that could reshape interest-rate expectations and set the tone for the pair’s next move.