Weekly Forecast Video on Forex, BTCUSD, XAUUSD

Stay ahead in the markets with our detailed analysis of gold and forex trade setups for this upcoming week, Nov 03 to Nov 07.

XAUUSD Extends Its Losing Run as Dollar Strength Weighs Heavily

Gold prices edged lower on Friday as investors shifted their focus toward the Federal Reserve’s cautious tone on future monetary policy decisions. Despite the metal’s underlying long-term strength, short-term sentiment leaned slightly bearish, as a firm U.S. Dollar and stable Treasury yields limited fresh buying momentum.

Gold Loses Shine as the Dollar Holds Firm

Gold began the day on a relatively stable note but gradually slipped as traders reassessed expectations for more interest rate cuts by the Federal Reserve. The recent rate cut, which many hoped would open the door to further monetary easing, instead came with a dose of caution from Fed Chair Jerome Powell. In his post-meeting remarks, Powell made it clear that another rate cut wasn’t guaranteed, emphasizing the Fed’s focus on data before making any policy shifts.

This statement dampened hopes among gold investors who typically benefit when interest rates fall. Lower rates tend to weaken the dollar and reduce yields, making non-yielding assets like gold more attractive. However, with the dollar holding strong and Treasury yields climbing, gold’s appeal as an alternative investment took a hit.

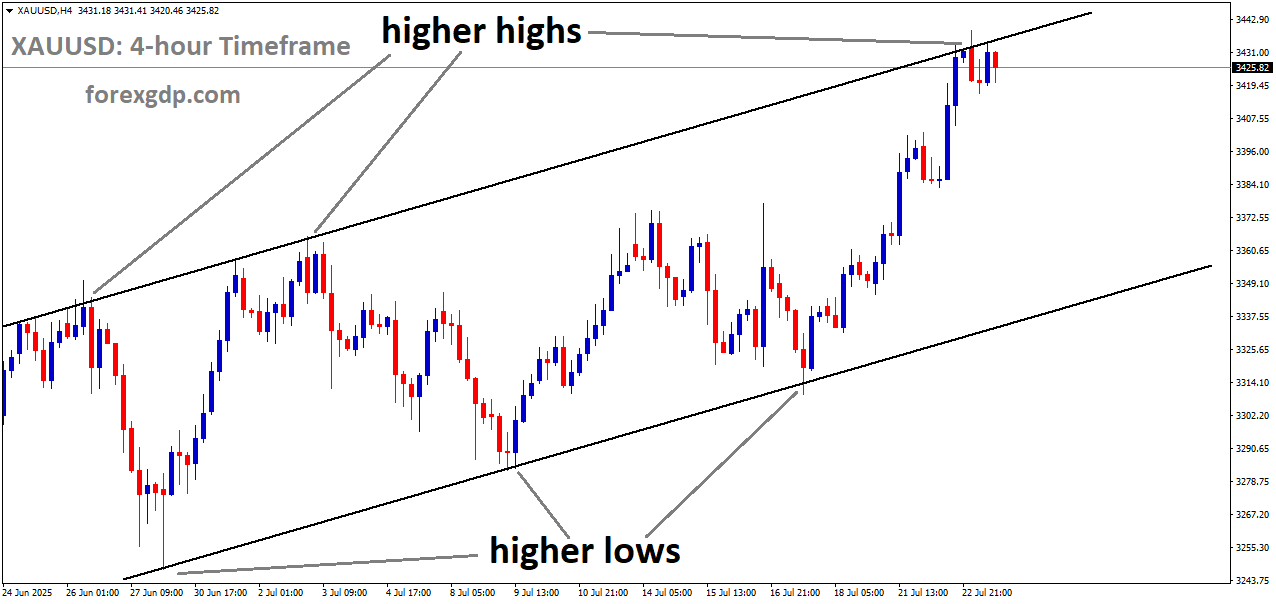

XAUUSD is moving in an uptrend channel

The U.S. Dollar Index (DXY) remained close to its recent highs, supported by stronger yields across the Treasury curve. This combination limited gold’s upward potential and pushed it toward its second straight weekly decline.

Global Politics and Market Sentiment Add to the Pressure

Trade Relations Bring Temporary Relief

While the Federal Reserve’s cautious approach played a major role in gold’s decline, improved global sentiment also contributed. The recent meeting between U.S. President Donald Trump and Chinese President Xi Jinping concluded with unexpectedly positive results, easing some of the trade tensions that had previously fueled demand for safe-haven assets like gold.

The leaders agreed on a one-year trade truce extending through November 2026, with both sides making concessions. The U.S. reduced tariffs on certain Chinese goods, while China rolled back its duties on American agricultural imports and postponed new export restrictions on rare-earth materials.

This sense of cooperation, even if temporary, lowered immediate geopolitical risk and reduced the urgency for investors to flock to gold as a protective asset.

The Impact of the U.S. Government Shutdown

Adding another layer of uncertainty to the mix, the U.S. government shutdown entered its fifth week with no sign of resolution. The prolonged closure has delayed the release of key economic reports, leaving investors in the dark about the true state of the economy.

While shutdowns often create a wave of risk aversion that supports gold, this time, the effect has been muted. The strong dollar continues to dominate market sentiment, offsetting what might have otherwise been a supportive environment for bullion.

President Trump’s push to end the filibuster and move funding bills forward hasn’t gained much traction, and the Senate is set to reconvene next week to resume discussions. The longer the standoff continues, the more likely it could weigh on U.S. economic growth and influence future monetary policy decisions.

What Investors Are Watching Next

The upcoming week is packed with U.S. economic data releases that could shape market direction. Investors will closely analyze private-sector reports for signs of labor market resilience and inflation trends — both critical indicators for the Fed’s next move.

Some of the key data points expected include:

-

ISM Manufacturing PMI: A snapshot of industrial performance and business confidence.

-

JOLTS Job Openings and ADP Employment Change: Important indicators of labor demand and hiring trends.

-

Challenger Job Cuts Report: A gauge of corporate layoffs that reflects business confidence.

-

University of Michigan Sentiment Survey: A measure of consumer optimism that could hint at spending trends.

-

New York Fed Inflation Expectations Survey: A critical insight into how consumers view price stability in the coming months.

These reports will collectively shape expectations for future Fed actions. If inflation appears contained and employment data shows signs of cooling, the central bank may consider another rate cut later in the year. However, stronger numbers could strengthen the case for holding rates steady — a scenario that could further pressure gold prices.

Long-Term Outlook: Still Constructive Despite Short-Term Weakness

Despite gold’s current pullback, the long-term picture remains encouraging for bullish investors. Central banks around the world continue to diversify their reserves by purchasing gold, providing a strong foundation of demand that isn’t influenced by short-term market sentiment.

Additionally, persistent global uncertainties — ranging from geopolitical tensions to the potential for future economic slowdowns — continue to reinforce gold’s reputation as a stable store of value. For long-term holders, short-term dips often represent buying opportunities rather than warning signs.

XAUUSD is moving in an uptrend channel, and the market has reached a higher high area of the channel

Even though current sentiment might appear mixed, the broader uptrend in gold remains structurally intact. The metal’s resilience through fluctuating interest rates, shifting trade dynamics, and changing investor moods underscores its enduring importance in diversified portfolios.

Final Summary

Gold prices may have slipped modestly this week, but the broader story is far from negative. The U.S. Dollar’s strength and the Federal Reserve’s cautious tone have temporarily capped gains, while improved global relations have reduced the urgency for safe-haven demand. Yet beneath this short-term softness lies a sturdy foundation built on central bank buying and long-term uncertainty.

As the markets look ahead to next week’s key U.S. data releases, traders will be watching closely for clues about inflation, employment, and the economy’s overall trajectory. Whether gold continues to drift lower or stages a rebound will largely depend on how these factors shape expectations for the Fed’s next move.

For now, gold may be taking a breather, but its long-term story — one of resilience, value, and global confidence — remains as compelling as ever.

EURUSD dips sharply as the Dollar surges on the Fed’s confident policy outlook

The Euro has been under pressure recently, falling to a three-month low against the US Dollar. The currency pair EUR/USD continues to struggle as the US Dollar grows stronger, driven by the Federal Reserve’s firm stance on monetary policy. While traders were expecting the recent rate cut from the Fed, the accompanying message made it clear that the central bank isn’t in a hurry to ease further. Let’s take a closer look at what’s going on and why the Euro seems to be losing ground against the Greenback.

The Fed’s Hawkish Stance Strengthens the Dollar

The Federal Reserve recently announced a 25-basis-point rate cut, which wasn’t a surprise for the markets. What caught everyone’s attention, however, was the tone that followed. Instead of signaling more cuts ahead, the Fed made it clear that this move was a cautious adjustment rather than the start of a new easing cycle.

EURUSD is falling from the retest area of the broken Ascending Triangle pattern

Jerome Powell, the Fed Chair, highlighted that inflation is still not fully under control and that the economy remains relatively strong. This hawkish tone – meaning a focus on controlling inflation rather than stimulating growth – gave a significant boost to the US Dollar. Investors now believe that another rate cut in the near term is unlikely, and that confidence is keeping the Dollar firm.

As a result, the US Dollar Index (DXY), which tracks the performance of the Dollar against other major currencies, continues to hover around its recent highs. This shows how much support the currency is getting from the Fed’s cautious yet confident policy direction.

Why the Euro Is Losing Momentum

While the US is showing resilience, the situation in Europe looks more uncertain. The European Central Bank (ECB) decided to hold its interest rates steady for the third consecutive meeting. ECB officials pointed out that inflation in the Eurozone is close to the 2% target, and the economy, while facing challenges, is still showing moderate growth.

However, compared to the Fed’s proactive tone, the ECB’s approach feels more restrained. The central bank continues to emphasize that it will make decisions based on incoming data, rather than setting a clear direction in advance. This “wait and see” attitude creates uncertainty for investors, especially when the US appears to have a stronger plan in place.

As the policy gap between the Fed and ECB widens, the Euro has naturally lost its shine. Investors are finding more confidence in the US economy and the Dollar, making the Euro less attractive in comparison. This divergence in policy direction is one of the main reasons why EUR/USD is seeing continued downward pressure.

Diverging Policies and Their Market Impact

The Fed’s “Hawkish Cut” Explained

The term “hawkish cut” might sound confusing, but it perfectly describes what the Fed has done. The central bank did reduce rates slightly, but it paired that move with a strong message that it remains focused on fighting inflation. This combination signals that the Fed isn’t easing policy to boost growth but rather making a small adjustment while staying alert to inflation risks.

This type of approach keeps investors confident in the US economy’s underlying strength. It also means that the interest rate gap between the US and Europe could continue to favor the Dollar, as US yields remain higher and more attractive to global investors.

The ECB’s Cautious Approach

On the other hand, the European Central Bank’s steady-rate stance reflects its uncertainty about the broader economic outlook. Europe’s growth remains fragile, and the ECB is hesitant to make any aggressive policy changes. It wants to ensure that inflation continues to stabilize before taking any new steps. This measured approach helps maintain short-term stability but lacks the kind of confidence that investors are seeing from the Fed.

As a result, many traders are shifting towards the Dollar, anticipating that it will continue to perform better in the months ahead.

Fed Officials Reinforce the Message

Several Federal Reserve officials spoke after the rate announcement, and their comments reinforced the bank’s firm position. Atlanta Fed President Raphael Bostic mentioned that the Fed’s goals of price stability and employment are currently “in tension,” but he supported the latest cut since policy remains tight. His remarks suggest that the central bank still sees inflation as a concern and wants to maintain control over price growth.

Cleveland Fed President Beth M. Hammack added that she would have preferred to hold rates steady altogether, emphasizing that the Fed isn’t following a fixed path. Both officials agreed with Chair Powell’s view that another cut in December is “far from guaranteed.” These statements helped cement the perception that the Fed is staying firm, which naturally gave the US Dollar even more strength in the global market.

What This Means for Traders and Investors

For currency traders, the widening gap between the Fed and the ECB means one thing – the Dollar remains the safer bet for now. The combination of higher US yields, steady economic performance, and the Fed’s determined tone makes it difficult for the Euro to gain traction.

In the short term, this could mean more downward pressure on EUR/USD unless something changes in Europe’s economic picture. If the ECB hints at policy changes or stronger growth data emerges from the Eurozone, the pair could see some recovery. But for now, the momentum clearly favors the US Dollar.

EURUSD is moving in a descending channel, and the market has reached the lower high area of the channel

Long-term investors might also view this situation as a sign of ongoing policy divergence between the two major economies. While the US seems prepared to maintain its firm approach, the Eurozone remains in a wait-and-watch phase. This difference in confidence and clarity can influence capital flows, potentially keeping the Euro on the back foot for a while.

Final Summary

The Euro’s recent weakness against the Dollar highlights how powerful central bank guidance can be. The Federal Reserve’s hawkish tone, even after a small rate cut, has strengthened the US Dollar and shown that the central bank remains committed to managing inflation carefully. In contrast, the European Central Bank’s steady-rate stance and cautious tone have made investors less confident in the Euro’s short-term outlook.

The divergence between the two major central banks is now more visible than ever. With the Fed signaling control and the ECB staying patient, the market naturally leans toward the US Dollar. Unless Europe delivers stronger economic data or policy changes, the Dollar’s dominance could continue for some time.

In essence, the story of EUR/USD isn’t just about exchange rates—it’s about confidence, clarity, and conviction. And right now, the Fed seems to have all three on its side.

GBP/USD struggles under pressure as UK spending fears meet strong U.S. Dollar demand

The British Pound continues to face heavy pressure in the global currency markets. While many traders were hoping for a rebound, it seems that the Pound Sterling still can’t find solid ground. With growing worries about the United Kingdom’s fiscal situation and strong signals from the U.S. Federal Reserve supporting the U.S. Dollar, the GBP/USD pair remains stuck in a downward trend. Let’s explore why the Pound is struggling, what’s driving the Dollar’s strength, and how these developments might shape the weeks ahead.

Why the Pound Sterling Can’t Catch a Break

The British Pound has been facing one challenge after another. Over the past few weeks, investor sentiment toward the UK economy has weakened considerably. The main reason behind this gloomy outlook is the country’s fiscal position — simply put, the government’s finances don’t look very encouraging.

GBPUSD is moving in a downtrend channel, and the market has reached the lower low area of the channel

Mounting Fiscal Concerns in the UK

The Office for Budget Responsibility (OBR) recently issued new projections that highlight just how difficult things might get. Productivity, one of the key drivers of economic growth, is now expected to decline slightly. Though a small percentage may not sound alarming, it has major long-term implications — it could mean a wider budget deficit in the coming years.

The Institute for Fiscal Studies (IFS) also warns that the government faces a shortfall of billions of pounds. This creates a dilemma for Chancellor Rachel Reeves as she prepares for the upcoming budget. The government must find ways to fill the gap, and there are really only two main options: raising taxes or borrowing more money. Neither choice is popular — tax hikes would hit households and businesses, while increased borrowing could push debt levels even higher.

These fiscal challenges are particularly difficult because they come at a time when the Labour government has pledged not to impose new tax burdens or cut spending in critical areas. This limits the flexibility to respond to the situation effectively. As a result, the markets are skeptical about how the UK will balance its books without compromising growth.

The Strong U.S. Dollar Adds More Pressure

While the Pound is struggling, the U.S. Dollar has been enjoying a period of renewed strength. Much of this has to do with the Federal Reserve’s recent messaging. Investors had been hoping for another rate cut from the Fed before the end of the year, but those hopes are quickly fading.

The Fed’s Hawkish Tone Boosts the Dollar

Federal Reserve Chair Jerome Powell recently suggested that another rate cut in December is unlikely. This was a major shift from earlier expectations, where most traders believed a reduction was almost certain. His comments, combined with statements from other Fed officials, painted a picture of a central bank still very focused on fighting inflation.

Beth Hammack, President of the Federal Reserve Bank of Cleveland, made it clear that she wouldn’t have supported the most recent rate cut, saying it’s too soon to relax policy. Similarly, Raphael Bostic from the Atlanta Fed acknowledged that inflation and employment goals are still in conflict. In his view, more progress is needed before the Fed can consider bringing interest rates down to neutral levels.

These remarks reinforced the idea that the Fed will keep monetary policy tight for a while longer. For investors, this means higher yields on U.S. assets — and that naturally draws money into the Dollar, pushing it higher against other currencies, including the Pound Sterling.

The Market’s Mixed Sentiment Toward the UK Economy

The weakness of the Pound isn’t just about the Dollar’s strength. It’s also about how traders perceive the UK’s broader economic direction. Despite inflation easing slightly, the British economy still faces a combination of slow growth, high public spending, and limited fiscal space.

Limited Room for Policy Flexibility

The UK government’s hands are tied in several ways. On one hand, public debt is already elevated, leaving little room for new borrowing. On the other hand, the cost of living crisis continues to weigh on households, meaning tax increases could easily provoke a backlash. This lack of flexibility makes it difficult for policymakers to respond effectively to new economic challenges.

The upcoming budget announcement is therefore highly anticipated. Many analysts believe that Chancellor Reeves will need to make some tough decisions to restore market confidence. But with political pressure mounting, even small policy missteps could have big consequences for the Pound.

Investors Remain Cautious

Traders and investors remain cautious, and that’s reflected in how the Pound has been performing. Many still believe that the Bank of England will eventually need to cut interest rates to support growth, especially if the economy slows further. However, cutting rates too soon could put even more downward pressure on the currency.

This uncertain environment makes it difficult for the Pound to recover in a meaningful way. Each small rebound has so far been short-lived, as concerns about the UK’s fiscal and economic health quickly re-emerge.

The Bigger Picture: What Lies Ahead for the Pound

Looking ahead, much depends on how both the UK government and the Bank of England navigate the coming months. If the budget announcement in November includes credible measures to manage debt and support growth, it could help stabilize market confidence. But if investors sense that fiscal discipline is weakening, the Pound may remain under stress.

At the same time, developments in the U.S. will continue to play a major role. As long as the Federal Reserve maintains its cautious stance and the American economy remains relatively strong, the U.S. Dollar is likely to stay in demand. That means any recovery for the Pound may be slow and uneven.

Final Summary

The British Pound’s ongoing struggles highlight just how interconnected global financial markets have become. On one side, the United States continues to project strength, backed by firm monetary policy and investor confidence. On the other, the United Kingdom faces internal challenges — from fiscal imbalances and weak productivity to limited policy flexibility.

For traders and investors, this combination makes the Pound a difficult currency to bet on right now. The next few months will be crucial. The November budget could either restore faith in the UK’s fiscal management or deepen the doubts that have been weighing on the currency.

In the meantime, the Pound is likely to stay sensitive to any economic headlines — whether they come from Westminster or Washington. While short-term rebounds may occur, the broader picture remains one of caution. Until the UK demonstrates clearer fiscal stability and stronger economic growth, the Pound Sterling may continue to struggle to regain its footing against the ever-resilient U.S. Dollar.

USDJPY Gains Momentum as BoJ Doubts Weigh Heavier Than Tokyo’s Rising Inflation

The Japanese Yen (JPY) has been struggling to gain ground recently, facing consistent pressure against a stronger US Dollar (USD). With global markets shifting focus toward central bank decisions and geopolitical dynamics, the Yen continues to lose its traditional safe-haven shine. Let’s dive into what’s really driving this decline and what traders are paying attention to.

Why the Japanese Yen Is Under Pressure

Bank of Japan’s Policy Uncertainty

One of the major factors behind the Yen’s weakness is the growing uncertainty around the Bank of Japan’s (BoJ) next move. For years, Japan has maintained one of the most accommodative monetary policies among developed nations. While inflation in Tokyo showed an uptick, investors are not convinced the BoJ will tighten policy any further.

USDJPY reached the retest area of the broken uptrend channel

The latest consumer price data from Tokyo showed inflation rising more than expected. Normally, this would push the central bank toward raising interest rates, but Japan’s new Prime Minister, Sanae Takaichi, is expected to support more fiscal stimulus. That has led many market watchers to believe the BoJ might delay any rate hikes, keeping borrowing costs near record lows. This hesitation is one of the key reasons the Yen remains under pressure.

BoJ Governor Kazuo Ueda recently emphasized that there are no preset plans for the timing of future rate hikes. That cautious stance leaves traders uncertain about when the central bank might act again, causing more investors to move away from the Yen.

The Safe-Haven Demand for the Yen Is Fading

US-China Trade Optimism Changes the Sentiment

Traditionally, the Japanese Yen has been a go-to safe-haven currency during times of global tension. But as trade relations between the US and China show signs of improvement, investors have less reason to seek refuge in the Yen.

When markets feel more stable, money tends to flow away from low-yielding safe-haven assets like the Yen and into higher-return investments, especially in the US. The recent signs of cooperation between Washington and Beijing have therefore reduced the Yen’s appeal.

In simple terms, when the world seems a little less risky, traders start selling the Yen to buy assets that might offer better returns. That’s exactly what’s happening now, pushing the Yen further down against the Dollar.

The Federal Reserve’s Hawkish Stance Boosts the Dollar

US Monetary Policy Tilts the Balance

While Japan’s central bank hesitates, the US Federal Reserve has been signaling a more aggressive stance. The Fed’s recent comments suggest it may not be as quick to cut interest rates as markets once expected. Chair Jerome Powell stated that another rate cut at the December meeting isn’t guaranteed, which immediately strengthened the Dollar.

Higher interest rates in the US make Dollar-denominated assets more attractive to investors compared to currencies like the Yen. This interest rate gap between Japan and the US has widened even further, adding to the Yen’s decline.

The Fed’s cautious tone also shows confidence in the strength of the US economy. Investors tend to flock to the Dollar when they believe it offers better returns and stability. As a result, the USD/JPY pair has been trading near its highest levels in months, reflecting both a stronger Dollar and a weaker Yen.

Political and Fiscal Developments in Japan Add to the Pressure

A Pro-Stimulus Government Keeps Monetary Policy Loose

Prime Minister Sanae Takaichi’s government has taken a clear pro-stimulus stance, favoring spending programs aimed at supporting growth. While this might be good news for Japan’s economy in the short run, it also means the BoJ will have little reason to rush into rate hikes.

A mix of aggressive fiscal policies and cautious monetary action tends to keep interest rates low. That environment usually weakens the currency, as investors look for better yields elsewhere.

Many economists believe that as long as Japan continues to rely heavily on government spending and maintains loose monetary conditions, the Yen will struggle to find sustained upward momentum.

Market Caution: Why Traders Aren’t Fully Betting Against the Yen Yet

Despite all the bearish signals, not everyone is confident enough to bet heavily against the Yen. There’s a lingering fear that Japanese authorities could step in to support their currency if it falls too far.

The idea of a potential intervention from the Ministry of Finance keeps some traders from becoming overly bearish. Japan has a long history of stepping into the currency markets when the Yen’s decline becomes too steep, especially if it starts affecting import costs or domestic stability. This fear of government intervention acts as a speed bump for further aggressive Yen selling.

What’s Next for the Yen and Dollar Relationship

Short-Term Pressure, Long-Term Questions

Looking ahead, the Japanese Yen’s outlook depends largely on two key factors: the Bank of Japan’s next move and how long the Federal Reserve maintains its hawkish stance. If the BoJ signals any willingness to raise rates in the coming months, the Yen might recover some strength. But if the Fed stays firm and US data continues to outperform, the Dollar could remain dominant for a while.

Global developments—especially around trade relations and economic stability—will also continue shaping market sentiment. Any sudden tension or risk event could temporarily restore the Yen’s safe-haven appeal, but for now, that doesn’t seem to be the market’s focus.

Final Summary

The Japanese Yen’s recent weakness tells a clear story of diverging economic policies and shifting investor sentiment. On one side, Japan’s central bank remains cautious, with the government leaning toward more fiscal spending. On the other, the US Federal Reserve’s hawkish outlook and global optimism are pushing the Dollar higher.

The combination of BoJ uncertainty, easing trade fears, and strong US economic policy has left the Yen vulnerable. While the possibility of official intervention prevents a total selloff, the broader picture still favors a stronger Dollar in the near term.

In essence, unless Japan signals a firmer commitment to tightening policy or global risks suddenly rise, the Yen’s struggle is likely to continue. For traders and investors, the focus will stay on how these central bank narratives unfold—and whether the BoJ decides to step out of its comfort zone anytime soon.

USDCAD Gains Ground While the Fed’s Reserved Tone Pressures the Loonie

The Canadian Dollar has been struggling to hold its ground against the US Dollar, and this week was no exception. The shift in global market sentiment, driven by the Federal Reserve’s cautious remarks, gave a strong push to the Greenback. Meanwhile, Canada’s recent economic data didn’t do much to help the Loonie, with the country’s GDP unexpectedly shrinking in August. Let’s break down what’s happening and why the US Dollar continues to dominate the currency scene.

The Fed’s Cautious Tone Fuels the Dollar’s Comeback

When the Federal Reserve speaks, the world listens. And this week, its tone was cautious, sending a ripple through global markets. The Fed delivered another small rate cut, but Chair Jerome Powell made it clear that more cuts aren’t guaranteed. This statement alone was enough to reignite investor confidence in the US Dollar.

USDCAD is moving in an uptrend channel

For traders, this shift was significant. Many had expected the Fed to continue easing its policy to support growth, but Powell’s comments hinted at a pause. This move reinforced the belief that the US economy remains resilient, and the central bank doesn’t see the need for further stimulus—at least for now.

Adding to this sentiment, Fed officials from Kansas City and Dallas backed Powell’s view. They suggested that the economy is doing relatively well and that inflation is still higher than desired. This united front made markets rethink their earlier predictions of a December rate cut, with expectations dropping sharply within days. The result? The US Dollar Index surged to near three-month highs, reflecting renewed strength and investor confidence.

Canada’s Economic Setback Adds to the Pressure

While the US Dollar gained strength, Canada’s economy faced a setback. Fresh data from Statistics Canada showed that the nation’s Gross Domestic Product shrank by 0.3% in August. Economists had been expecting no change, so this decline came as an unpleasant surprise.

This contraction raised concerns about the overall momentum of the Canadian economy. Even though July’s GDP figure was revised slightly higher, the August decline highlighted the challenges facing Canada’s growth. With weaker demand and sluggish production in several key sectors, the outlook appears uncertain.

At the same time, the Bank of Canada’s recent decision added another twist. The central bank had just cut its benchmark interest rate by 25 basis points, signaling that it might be nearing the end of its easing cycle. While the rate cut was intended to support growth, the market perceived it as a sign that policymakers see limited room for further action. This mixed message—lower rates but hints of caution—kept investors on edge and added pressure on the Canadian Dollar.

Why the US Dollar Continues to Outshine the Loonie

Global Confidence Shifts Toward the US

One major reason the US Dollar remains dominant is global confidence. The US economy continues to show relative stability compared to other major economies. Even with modest growth, strong employment figures and consistent consumer spending have kept the US on a steadier path. In contrast, Canada’s economic data and softer energy exports have weakened investor enthusiasm for the Loonie.

Interest Rate Gap Widens

The difference in interest rate expectations between the US and Canada also plays a huge role. If the Fed holds rates steady while the Bank of Canada remains more open to cuts, investors are naturally drawn to the higher-yielding US Dollar. This “rate differential” attracts capital inflows into US assets, strengthening the Greenback while weighing down the Canadian Dollar.

Market Sentiment and Safe-Haven Demand

Market sentiment has also been shifting toward safety, especially when uncertainty looms over global growth or geopolitical tensions rise. The US Dollar is often viewed as a safe haven—meaning when investors get nervous, they tend to park their money in US assets. This defensive move consistently benefits the Greenback, even when other currencies, like the Canadian Dollar, might offer attractive yields.

Fed Officials’ Voices Add More Weight

Beyond the rate decision, comments from top Federal Reserve members have been shaping market behavior. Kansas City Fed President Jeffrey Schmid mentioned that the current policy is only “modestly restrictive,” hinting that there’s no urgency to cut rates further. He also pointed out that inflation still hasn’t cooled enough to justify aggressive easing. Meanwhile, Dallas Fed President Lorie Logan expressed doubts about another cut in December, saying that the Fed already acted decisively in September.

These insights mattered because they reflect a unified message from policymakers: the Fed isn’t rushing to add more stimulus. For investors, that means the US Dollar could stay stronger for longer.

The Broader Picture for USD/CAD Traders

For those following currency movements, the recent dynamics between the US Dollar and Canadian Dollar highlight a broader theme. While short-term fluctuations are common, the underlying trend shows that global investors are favoring the Greenback due to policy confidence and economic resilience.

Canada’s economic weakness and the Fed’s firm stance create an environment where the US Dollar remains the preferred currency for traders and institutions alike. Unless Canada’s growth rebounds or the Fed surprises markets with a policy shift, the Loonie may continue facing downward pressure in the near term.

Final Summary

The Canadian Dollar’s weakness isn’t just about one piece of data—it’s a story of diverging economic paths. On one side, the United States continues to project confidence, with the Federal Reserve holding a cautious yet steady approach that reassures investors. On the other, Canada’s economy is showing early signs of strain, and its central bank’s limited room to maneuver makes recovery slower.

As the global market continues to digest these developments, the US Dollar seems poised to maintain its edge. The coming weeks will be crucial in determining whether Canada’s economy can bounce back or if the Loonie will stay under the shadow of a stronger Greenback. For now, it’s clear that the balance of power in North American currencies tilts heavily toward the US side.

USD Index Finds Balance as Fed Policy Doubts Keep Traders on Edge

The U.S. Dollar has found a moment of stability after a week of mixed signals from the Federal Reserve and cautious trading behavior from investors. Market participants are taking a step back, assessing the shifting expectations around the next monetary policy move. While some anticipate a potential rate cut later this year, others believe the central bank may continue its “wait and see” approach, depending on how economic data unfolds.

The Calm Before the Next Move: Why Traders Are Staying Cautious

The U.S. Dollar Index (DXY), which measures the strength of the dollar against a basket of major world currencies, has been relatively steady in recent sessions. The reason? Traders are hesitant to take strong positions without clearer guidance from the Federal Reserve (Fed).

According to data from the CME FedWatch Tool, the market now sees around a 71% chance of a rate cut in December, a slight increase from the previous day. This growing expectation of a rate reduction has weakened the dollar’s upward momentum, but it hasn’t been enough to cause a significant decline either. The overall tone in the market remains cautious, as investors prefer to wait for confirmation from upcoming Fed speeches and economic reports before committing to a direction.

USD Index Market price has broken the downtrend channel to the upside

However, this shift in sentiment comes after a notable pullback from earlier, more optimistic expectations. Not long ago, the probability of a December rate cut was close to 90%, but that enthusiasm cooled off after Fed Chair Jerome Powell hinted that policymakers might need to slow down and reassess the situation.

Powell’s Message: A “Wait-and-See” Approach

In his recent post-meeting remarks, Fed Chair Jerome Powell made it clear that the central bank’s job isn’t done yet. He emphasized the ongoing challenge of balancing two key objectives—controlling inflation while supporting employment—especially with limited access to fresh economic data amid the U.S. government’s partial shutdown.

Powell stated that while inflation has shown signs of easing, it’s still not at levels that would allow the Fed to confidently loosen monetary policy. At the same time, the labor market remains resilient, though some signs of cooling have emerged. This mix of factors has made decision-making more complex.

He also reminded the public that any further rate cuts would depend heavily on incoming data. In simple terms, Powell doesn’t want the Fed to move too fast and risk stimulating inflation again, but he also doesn’t want to keep rates high for too long and harm job growth. His message to markets was straightforward: patience is key.

Inside the Latest Fed Decision

Earlier this week, the Federal Reserve announced a 25-basis-point rate cut, lowering the benchmark rate to a range between 3.75% and 4.00%. The decision reflected the Fed’s cautious approach—enough to provide some economic relief, but not so aggressive that it could reignite inflationary pressures.

What caught traders’ attention was that the decision wasn’t unanimous. Two members of the committee voiced different opinions. Fed Governor Stephen Miran wanted a larger 50-basis-point cut to address slowing economic momentum, while Kansas City Fed President Jeffrey Schmid preferred to keep rates unchanged. This split highlights the ongoing debate inside the central bank about how quickly the U.S. economy is cooling and how much stimulus is appropriate at this stage.

The lack of full agreement among policymakers adds another layer of uncertainty for traders, as it signals potential divisions within the Fed about the path forward. When central bankers themselves are not fully aligned, investors tend to become more cautious, leading to subdued market movements like we’re seeing now.

Global Politics Add to Market Uncertainty

Adding to the cautious sentiment are recent developments on the international stage. A meeting between U.S. President Donald Trump and Chinese President Xi Jinping concluded with some noteworthy progress on trade relations. The United States agreed to reduce tariffs on Chinese goods, while China made several commitments, including limiting fentanyl exports, increasing purchases of U.S. agricultural products, and lifting restrictions on rare earth exports.

While these steps are seen as positive for global trade relations, markets remain skeptical about how long the truce will last. Both sides have a history of trade disputes resurfacing, and investors are wary of making long-term bets based on temporary diplomatic progress.

The easing of trade tensions did bring some relief to global markets, but traders continue to keep one eye on Washington and Beijing for signs of either renewed cooperation or fresh conflict.

What Traders Are Watching Next

At this point, the market’s focus is firmly on the Federal Reserve’s next moves. Traders are closely monitoring upcoming speeches from Fed officials, as even small hints about future policy can cause significant currency movements.

Key upcoming events include:

-

Economic data releases, such as inflation and employment reports.

-

Public comments from Fed members about the strength of the economy.

-

Geopolitical updates, particularly around trade or fiscal policy developments.

If inflation data continues to trend lower and job growth remains stable, the Fed could be more comfortable with a rate cut later in the year. However, if inflation unexpectedly rises again, the central bank might decide to hold off on any additional easing. This delicate balance between caution and confidence is what’s keeping markets in limbo right now.

The Bigger Picture: What It Means for the U.S. Dollar

The dollar’s near-term outlook largely depends on how investors interpret the Fed’s tone in the coming weeks. A clear signal of rate cuts could weaken the dollar, as lower interest rates typically make the currency less attractive to investors seeking higher yields. On the other hand, if the Fed remains firm and data points to continued economic strength, the dollar could find renewed support.

Global investors are also factoring in the broader economic environment—including slowing growth in Europe and ongoing uncertainty in Asia—which may keep the dollar relatively stable even without strong domestic data. In other words, the dollar might continue to act as a safe haven while other regions struggle with their own economic challenges.

Final Summary

Right now, the U.S. Dollar Index is caught in a period of calm, with traders waiting for the next major cue from the Federal Reserve. Despite growing expectations for a rate cut in December, Fed Chair Jerome Powell’s cautious tone has reminded markets that policy decisions will depend on data, not speculation.

The latest 25-basis-point rate cut offered modest relief but did little to eliminate uncertainty. Meanwhile, global factors—from trade relations to political negotiations—are adding layers of complexity to the dollar’s outlook. For now, investors are watching, waiting, and weighing every word coming from the Fed for hints about what’s next.

In short, the U.S. dollar may not be making bold moves at the moment, but beneath the surface, the financial world is bracing for the next shift in direction—one that could set the tone for global markets in the months ahead.

USDCHF Extends Gains as Fed Moderation and SNB Dovish View Support the Dollar

The USD/CHF pair has been showing steady strength recently, holding near its two-week high as the US Dollar benefits from renewed market confidence and a shift in investor sentiment. The tone from the Federal Reserve has been more cautious, keeping traders alert to what might come next, while the Swiss National Bank (SNB) continues to favor a supportive policy stance to maintain economic stability.

This mix of contrasting central bank positions has set the tone for USD/CHF’s recent performance, giving the pair a bullish edge in the near term. Let’s take a closer look at what’s really driving this move and why traders are paying attention.

USDCHF reached the retest area of the broken uptrend channel

The Federal Reserve’s Careful Approach Keeps the Dollar Firm

The Federal Reserve’s latest policy decision has played a major role in strengthening the US Dollar. The Fed decided to cut interest rates by 25 basis points, bringing them down to the 3.75%-4.00% range, as widely expected by markets. However, what really caught the market’s attention was Jerome Powell’s follow-up statement.

Powell made it clear that further rate cuts are not guaranteed, saying that another reduction in December is “not a foregone conclusion.” This simple remark had a big impact on how traders view the future of US monetary policy.

Why the Market Reacted Strongly

Investors had been expecting a more aggressive path of rate cuts, especially with ongoing global economic uncertainty. But Powell’s comments reminded everyone that the Fed isn’t in a rush to ease too much. Instead, it prefers a data-driven approach, meaning future moves will depend heavily on inflation, employment, and growth trends.

This cautious stance immediately lifted US Treasury yields, with the 10-year note reaching its highest level in three weeks. When yields rise, the US Dollar typically strengthens, as higher returns attract foreign investors. This has been a key factor in keeping the USD/CHF pair supported, giving it the upward push we’ve seen lately.

Global Factors Adding Support to the Dollar

Apart from domestic monetary policy, global developments have also contributed to the Dollar’s strength. One of the biggest positive factors has been the temporary trade truce between the United States and China.

The two nations have agreed on a one-year ceasefire, which includes a rollback of some US tariffs and China’s promise to increase purchases of American agricultural goods. This news has brought a sense of relief to global markets and improved investor sentiment.

How This Impacts USD/CHF

When tensions between the US and China ease, global risk appetite generally improves. This leads investors to shift money into assets they see as safe yet profitable — and the US Dollar fits that description perfectly. The result? The Greenback gains strength, while currencies like the Swiss Franc, which usually benefit during uncertain times, lose some of their defensive appeal.

In this environment, it’s not surprising that USD/CHF has been moving higher, as traders lean toward the Dollar for both safety and yield advantages.

The Swiss National Bank’s Dovish Stance Keeps the Franc Under Pressure

While the Fed focuses on a careful and moderate path, the Swiss National Bank (SNB) has maintained its expansive monetary policy. Recent remarks from Petra Tschudin, a member of the SNB Governing Board, confirmed that the central bank remains ready to intervene in currency markets if needed.

SNB’s Ongoing Commitment to Stability

Tschudin reiterated that the SNB is fully prepared to step in if the Swiss Franc appreciates too much, as a stronger Franc can hurt exports and weaken inflation. She also noted that the bank could even reintroduce negative interest rates if necessary — a clear signal that the SNB remains dovish and focused on ensuring financial stability.

Interestingly, she highlighted that the exchange rate itself is less important than how it affects inflation. With inflation remaining within the SNB’s comfort zone, there’s little urgency to tighten policy.

What This Means for USD/CHF Traders

When one central bank (like the Fed) takes a cautious but relatively firm stance, and another (like the SNB) stays dovish, the currency pair between them tends to move in favor of the stronger policy side — in this case, the US Dollar.

So, as long as the SNB maintains its expansive stance and the Fed keeps its cautious confidence, USD/CHF is likely to stay supported. Traders are now waiting for upcoming Fed official speeches and economic data to gauge whether the momentum will continue heading into the next policy meeting.

Broader Market Mood and Investor Outlook

The recent developments in both the US and Switzerland highlight the importance of central bank communication in shaping market trends. Investors today are paying more attention than ever to tone and guidance — not just the decisions themselves.

With inflation stabilizing and economic growth remaining steady, the US economy continues to look resilient compared to many of its global peers. This gives the Fed more flexibility, while the SNB remains focused on protecting Switzerland’s export-driven economy from external shocks.

Key Factors to Watch in the Coming Weeks

-

Fed Officials’ Comments: Any signals about future rate paths could cause short-term moves in USD/CHF.

-

US Economic Data: Strong job numbers or higher inflation could further boost the Dollar.

-

Global Trade Sentiment: If the US-China truce holds, confidence in the Dollar could remain high.

-

SNB Policy Adjustments: Any surprise intervention or policy tweak could impact the Franc’s direction.

Traders will continue to watch how these factors evolve as they plan their next moves.

Final Summary

The USD/CHF pair has held firm near its recent highs thanks to a combination of a strong US Dollar and a dovish Swiss National Bank. The Fed’s cautious yet confident tone has reinforced investor belief in the Dollar’s resilience, especially with higher Treasury yields offering attractive returns. Meanwhile, the SNB’s commitment to maintaining loose policy ensures that the Franc remains under moderate pressure.

As things stand, the overall bias for USD/CHF remains slightly bullish, backed by policy divergence, improving global sentiment, and steady US economic data. While short-term fluctuations are inevitable, the pair’s underlying support looks stable as long as the Fed stays patient and the SNB remains ready to act when needed.

In simple terms — for now, the Dollar has the upper hand, and unless the Swiss National Bank surprises markets with a sharp policy shift, the USD/CHF pair is likely to stay on the higher side of its range in the near term.

EURCHF stays strong near recent peaks as fading fear weakens the Franc

The Euro has been showing strong performance against the Swiss Franc in recent sessions, and the momentum doesn’t seem to be fading anytime soon. The EUR/CHF pair is holding close to its two-week highs as investors react to changing global market sentiment, easing inflation pressures, and fresh comments from central banks. Let’s dive deeper into what’s really driving this trend and what it means for traders and investors keeping an eye on the Euro and Swiss Franc.

The Euro Gains Strength as Inflation Edges Toward the ECB’s Target

For months, inflation in the Eurozone has been the central topic in every economic discussion. Now, new data suggests that price growth is finally coming under control, moving closer to the European Central Bank’s (ECB) ideal level.

According to preliminary figures from Eurostat, core inflation—which excludes volatile items like food and energy—rose modestly in October. Although this increase might sound minor, it’s actually a positive sign. It shows that inflation is stabilizing rather than spiraling out of control, giving the ECB more confidence that its policies are working.

EURCHF reached the retest area of the broken Ascending channel

The overall inflation rate also moved down slightly, aligning closely with expectations. This steady moderation indicates that the ECB’s earlier rate hikes are doing their job, cooling price pressures across the Eurozone. For the first time in a while, investors are starting to believe that the ECB might be able to keep interest rates steady without having to tighten further.

ECB Keeps Its Policy on Hold

The European Central Bank decided to leave interest rates unchanged during its most recent policy meeting. This move was widely anticipated, but what’s more important is the message behind it. By keeping rates steady, the ECB signaled that inflation is now close enough to its 2% goal that it doesn’t need to make drastic moves.

For the markets, this “wait and see” stance adds a sense of stability. It means the ECB isn’t panicking, and that confidence is spilling over into the Euro, pushing it higher against the Swiss Franc.

Why the Swiss Franc Is Under Pressure

On the other side of the equation, the Swiss Franc—traditionally viewed as a safe-haven currency—is starting to lose some of its appeal. When global uncertainty fades, investors often move away from safe assets like the Franc and turn to higher-yielding or riskier investments, such as the Euro. That’s exactly what’s happening now.

Fading Safe-Haven Demand

Throughout times of global tension or financial instability, the Swiss Franc tends to strengthen as investors flock to safety. But recently, that demand has been fading. With the global economy showing resilience and fears around inflation and recession cooling off, traders are less inclined to hold the Franc.

As risk appetite improves, the Euro becomes more attractive relative to the Franc. The result? A steady rise in EUR/CHF levels as money flows away from Switzerland’s traditionally conservative currency.

Positive Domestic Data Fails to Boost the Franc

Interestingly, Switzerland’s own economy isn’t performing poorly. Retail sales data from September showed an encouraging rebound, signaling that local consumer spending is healthy. Yet, this hasn’t been enough to counter the downward pressure on the Franc.

Why? Because market sentiment is being driven more by global risk appetite and central bank outlooks than by Switzerland’s domestic numbers. Even solid retail figures can’t outweigh the broader shift away from safe-haven assets when investors feel optimistic about global growth.

SNB’s Flexible Stance Keeps Markets Guessing

While the Eurozone celebrates steady inflation progress, the Swiss National Bank (SNB) is staying flexible. In a recent statement, SNB Governing Board Member Petra Tschudin reaffirmed that the bank’s monetary policy remains accommodative. She made it clear that the SNB is ready to step in if needed—either by intervening in the currency markets or even bringing back negative interest rates.

That’s a strong reminder that the SNB won’t hesitate to act if the Franc strengthens too much or if inflation trends threaten its targets. In other words, Switzerland’s central bank still has tools on the table to maintain price stability, and it’s not afraid to use them.

Why SNB’s Intervention Policy Matters

The SNB’s willingness to intervene keeps the Franc from appreciating too quickly. By stepping into the currency market when needed, the bank helps Swiss exporters stay competitive. After all, a strong Franc makes Swiss goods more expensive overseas—a challenge for a country that relies heavily on exports.

Tschudin also emphasized that the SNB isn’t fixated on the exact value of the Franc itself, but rather on how its movements affect inflation and overall economic stability. That flexible, data-driven approach gives the bank room to adapt as global conditions evolve.

The Broader Picture: Confidence in Europe vs. Caution in Switzerland

When you look at the bigger picture, it’s clear that the recent EUR/CHF trend reflects diverging outlooks between the Eurozone and Switzerland. The Eurozone is entering a more stable phase, with inflation cooling and the ECB confident enough to pause its tightening campaign. Meanwhile, Switzerland’s central bank remains cautious, keeping all options open in case conditions shift again.

Investors are responding to that contrast. Confidence in Europe’s recovery is pushing the Euro higher, while the Franc’s safe-haven demand fades in an improving global environment.

This doesn’t mean the Franc is weak—it just means it’s less in demand right now. In calmer times, investors prefer to chase opportunities rather than hide in safe assets, and that’s exactly what’s fueling this Euro rally.

Final Summary

The current strength of the Euro against the Swiss Franc is a reflection of changing global sentiment and central bank positioning. The Eurozone’s inflation data shows steady progress toward the ECB’s 2% target, reinforcing the bank’s decision to hold rates steady. At the same time, the Swiss Franc is losing some of its traditional safe-haven shine as investors become more confident about global growth and risk assets.

Switzerland’s economy remains fundamentally sound, but the SNB’s cautious tone and readiness to intervene suggest that the bank is still keeping a close watch on developments. Meanwhile, the Euro continues to benefit from improved stability and investor confidence in the region’s recovery story.

For traders and investors, this shift signals that the Euro’s upward momentum may persist as long as global risk appetite remains strong and inflation continues to moderate. In short, the balance of confidence is currently tipping toward the Euro, while the Swiss Franc, for now, takes a back seat in the global currency race.

EURGBP Dips After ECB’s Steady Stance, UK Budget Troubles Weigh on Pound

The relationship between the Euro and the British Pound has always been dynamic, influenced by changing economic conditions, political shifts, and central bank decisions. Recently, the Euro has shown surprising resilience, giving back early gains but still managing to stay firm against the British Pound. Let’s break down what’s really happening behind this shift, why the Pound seems weaker, and what could be next for both currencies.

A Confident European Central Bank: Standing Firm on Its Policy

The European Central Bank (ECB) recently decided to keep interest rates unchanged, signaling a sense of confidence in how its policies are shaping the Eurozone’s economic outlook. According to ECB President Christine Lagarde, the bank believes its monetary stance is “well-calibrated.” In simple terms, the ECB feels that the balance between promoting growth and keeping inflation under control is finally in a good place.

EURGBP is moving in a descending triangle pattern n and the market has reached the lower high area of the pattern

No Rush for Rate Cuts

Unlike other major central banks that are leaning toward more rate cuts, the ECB appears comfortable holding steady for now. Several members of the ECB’s Governing Council have supported Lagarde’s cautious optimism, noting that while inflation has eased, it’s still close enough to the target that no drastic changes are needed.

The Eurozone’s latest inflation figures back up this decision. Recent data showed a slight dip in annual inflation to around 2.1%, moving closer to the ECB’s 2% target, which is generally considered healthy for long-term stability. Meanwhile, core inflation—which excludes volatile food and energy prices—has remained steady, reflecting underlying stability across the region.

This steady economic environment has given investors more confidence in the Euro, strengthening its position against the Pound and other major currencies.

The UK’s Fiscal Troubles: A Heavy Weight on the Pound

On the other side of the channel, the United Kingdom faces a less optimistic situation. The Office for Budget Responsibility (OBR) recently downgraded its productivity growth forecasts for the next five years. This revision might sound like a technical issue, but in reality, it has major implications for the UK’s economy.

Widening Fiscal Gap and Economic Strain

Lower productivity means lower long-term growth potential, and that directly impacts government revenue. The OBR estimates that this could widen the fiscal gap by billions of pounds, creating new challenges for policymakers already struggling to balance the budget. This shift has also raised doubts about the country’s ability to maintain stable fiscal health without further borrowing or spending cuts.

Investors tend to respond cautiously to such news. When government debt looks riskier or when growth projections weaken, confidence in the country’s currency tends to drop. That’s exactly what’s happening with the British Pound right now—it’s under pressure as markets reassess the UK’s economic outlook.

Pressure on the Bank of England

Adding to the tension is the Bank of England (BoE), which faces a tricky balancing act. With inflation still above comfortable levels but growth showing signs of strain, the BoE may soon find itself forced to cut interest rates again to stimulate the economy. However, such moves usually weaken a currency, since lower interest rates tend to make investments in that currency less attractive to foreign investors.

As a result, the Pound continues to face headwinds, while the Euro benefits from a more stable policy environment and growing confidence from the ECB.

The Diverging Paths of the Euro and Pound

One of the clearest trends in recent months has been the growing policy divergence between the ECB and the BoE. This simply means that the two central banks are moving in opposite directions when it comes to their economic strategies—and the currency market has taken notice.

Confidence vs. Caution

The ECB’s steady tone and signs of controlled inflation have given the Euro a solid foundation. Investors like predictability, and the ECB’s message that “we’re in a good place” has resonated strongly.

Meanwhile, the Bank of England’s more cautious stance reflects the uncertainty clouding the UK economy. The country’s ongoing fiscal challenges, sluggish productivity, and hints of future rate cuts all make the Pound less appealing in comparison.

Investor Sentiment and Market Behavior

Currency markets are heavily driven by sentiment. When investors believe one region’s economy is more stable than another’s, they move their money accordingly. Right now, the Eurozone is seen as slightly more stable than the UK, at least from a policy perspective. This shift in confidence explains why the Euro continues to outperform the Pound despite some fluctuations.

Even though the Euro gave back some early gains recently, it remains in a strong weekly uptrend. That means, despite day-to-day dips, the bigger picture still favors the Euro over the Pound for now.

The Road Ahead: What Could Change the Trend

While the Euro currently enjoys the upper hand, the currency market never stands still. Future movements will depend on how both the ECB and the BoE respond to changing economic realities in the months ahead.

For the Eurozone

The key will be inflation and growth data. If inflation continues to edge closer to 2% without falling too low, the ECB will likely hold its position. However, if growth slows or inflation drops significantly, discussions about rate cuts could resurface—something that might limit the Euro’s gains.

For the United Kingdom

The UK’s challenge lies in restoring confidence. Any improvement in productivity, fiscal management, or consumer confidence could help stabilize the Pound. Similarly, if the BoE signals that it can maintain rates for longer or that inflation pressures are easing, it might give the Pound some breathing room.

But as of now, policy divergence remains the dominant theme. The Euro is supported by confidence, while the Pound is weighed down by uncertainty.

Final Summary

In simple terms, the Euro’s current strength against the British Pound comes down to a tale of two very different central bank philosophies. The European Central Bank is projecting confidence, signaling stability, and benefiting from steady inflation and improving economic conditions. Meanwhile, the Bank of England faces mounting fiscal challenges, weak productivity, and pressure to support the economy with rate cuts—all of which keep the Pound under pressure.

Investors and traders are responding accordingly, favoring the Euro in what looks like a continuing short-term uptrend. While daily movements might show fluctuations, the broader trend still suggests that the Euro could remain stronger than the Pound as long as Europe’s steady policy and improving outlook continue to contrast with the UK’s uncertain fiscal path.

In short, the balance of confidence is tilted toward the Eurozone—for now. But as always in the currency market, the story can shift quickly. The next few months will reveal whether this divergence deepens or begins to narrow once again.

BTCUSD Breaks Higher with Growing Institutional Interest and Softer Trade Pressures

Bitcoin is once again back in the spotlight, drawing serious attention from both institutional investors and retail traders. After a sharp downturn that left many questioning its future, Bitcoin’s recovery has sparked a fresh wave of optimism across the crypto world. This rebound isn’t just about numbers—it’s about renewed confidence, increasing institutional interest, and improving global conditions that together hint at a more stable and sustainable phase ahead.

The Return of Institutional Confidence

For months, Bitcoin’s journey has been shaped by volatility and uncertainty. But recently, something interesting has changed. Data shows that large investors—often called “whales”—are quietly returning to the market. These are institutions and wealthy individuals who typically buy and hold large amounts of Bitcoin. Their renewed activity is a strong signal that confidence in the market is improving.

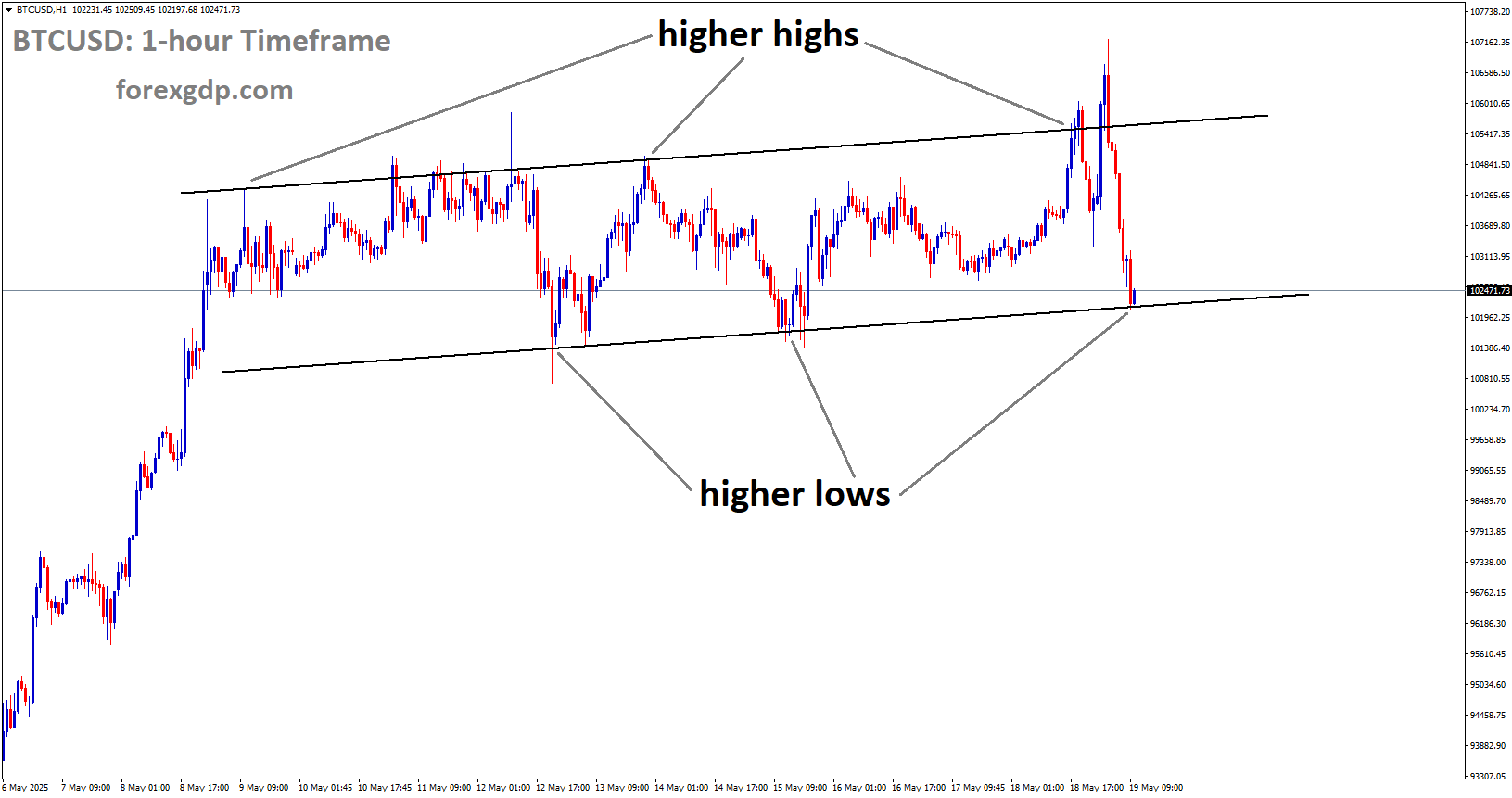

BTCUSD is moving in a box pattern

Analysts have noticed that many of these large holders began accumulating Bitcoin after a long period of market liquidation. This indicates that the worst of the selling pressure might be over. When big players start adding Bitcoin to their portfolios, it usually suggests that they believe prices are undervalued and that better days are ahead.

According to Farzam Ehsani, CEO of VALR, these investors are not reacting impulsively—they’re acting strategically. He explained that this current phase of accumulation looks much more disciplined compared to previous speculative rallies. Instead of chasing short-term momentum, they’re focused on long-term positioning. That’s a sign of a maturing market where major investors are thinking ahead rather than following hype.

A Healthier and More Balanced Market

One of the biggest takeaways from this recovery is how balanced the market appears compared to earlier cycles. During previous rallies, sudden bursts of leverage and speculative trades often caused wild price swings. This time, things look different. The recent uptrend has been largely driven by real buying demand rather than leveraged bets.

Market data shows that the levels of open interest—the number of active contracts between buyers and sellers—are balanced. This means neither the bullish nor the bearish side has overwhelming control. When funding rates and volatility stay neutral, it creates the foundation for a healthier market environment. In simple terms, Bitcoin’s recent movements appear to be based on genuine investor interest rather than risky trading behavior.

This balanced atmosphere could set the stage for longer, more sustainable growth. When speculation cools and accumulation takes over, Bitcoin often builds the strength it needs for its next big move.

Global Economic Stability is Fueling Optimism

The global financial environment is also playing a huge role in Bitcoin’s recovery. Over the past few months, we’ve seen easing tensions in major geopolitical issues and growing optimism around economic policy decisions. These changes have helped create a more favorable backdrop for all risk assets—including cryptocurrencies.

The easing of trade tensions between major economies, such as the U.S. and China, has lifted overall investor sentiment. In addition, the possibility of the Federal Reserve lowering interest rates has made investors more willing to seek higher-yield opportunities. As a result, both stock markets and digital assets have benefited from renewed risk appetite.

Interestingly, Bitcoin’s behavior has also evolved. It’s no longer just viewed as a speculative digital currency—it’s starting to move in tandem with traditional financial instruments like gold and equities. The fact that Bitcoin is showing strength while maintaining a strong correlation with major global assets highlights its growing importance as a macroeconomic player. It’s becoming a kind of “digital barometer” of market sentiment—sensitive to liquidity conditions but also capable of outperforming traditional stores of value.

Confidence Returns to the Market

Recent comments from U.S. Treasury Secretary Scott Bessent about progress in trade negotiations further boosted confidence. Investors began rotating their capital back into riskier assets, including Bitcoin, after a shaky start to October. These developments have reduced fear in the market and reminded investors that opportunities still exist even in uncertain times.

However, analysts are quick to note that Bitcoin’s sustainability depends on continued global stability. If policymakers follow through on their commitments and the current trend of accumulation persists, the foundation for long-term growth could solidify further.

Signs Pointing Toward a Long-Term Bull Market

While short-term volatility is always part of Bitcoin’s story, many indicators now suggest that a more extended bull market may be developing. The recent halt in large-scale selling, a steady increase in wallet activity, and improved liquidity conditions are all positive signs.

More importantly, the market seems to have gone through a necessary “reset.” The excess leverage that fueled unsustainable rallies in the past has largely been flushed out. What remains now is a leaner, more disciplined environment where investors are entering positions with patience and strategy.

Still, traders remain cautious. Global events—from political instability to shifting trade dynamics—can quickly influence sentiment. For instance, ongoing discussions between the U.S. and Venezuela, or rising tensions in the Middle East, can easily affect investor confidence. Yet despite these uncertainties, Bitcoin’s steady rebound stands as a reflection of its resilience and its ability to adapt in a constantly changing economic landscape.

The Bigger Picture: Bitcoin’s Evolving Role

Bitcoin’s evolution over the years has been nothing short of remarkable. From being dismissed as a speculative bubble to becoming a globally recognized asset class, its journey tells a story of adaptation and endurance. Today, Bitcoin is not just about price—it’s about participation, adoption, and the changing attitude of global investors.

BTCUSD is moving in an uptrend channel

Institutional players, who were once hesitant, are now shaping the direction of the market. This shift toward professional participation gives Bitcoin more credibility and helps stabilize its long-term outlook. As more traditional investors treat it like a serious asset rather than a passing trend, Bitcoin’s role in the global financial system continues to strengthen.

Final Summary

Bitcoin’s latest comeback isn’t just a temporary rally—it’s a sign of maturity. The combination of renewed institutional interest, improved macroeconomic stability, and healthier market behavior signals a new phase for the world’s largest cryptocurrency.

The days of wild speculation might be giving way to a more measured, confident approach where large investors lead the charge. With the global economy finding its footing and capital slowly returning to risk assets, Bitcoin is positioned to benefit from the broader wave of optimism.

Still, challenges remain. Market sentiment can change quickly, and external factors like geopolitical shifts can always disrupt progress. Yet, one thing is clear: Bitcoin has once again proven its strength, bouncing back from one of its toughest periods and reminding the world why it remains the most powerful name in digital finance.

This phase could very well be the start of something bigger—a steady, sustainable climb that redefines Bitcoin’s place in the global economy for years to come.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!