XAUUSD Gains Momentum as Investors Seek Safety from Weak U.S. Data

Gold continues to shine brightly in times of uncertainty. With growing concerns about the U.S. economy, a potential government shutdown, and weakening consumer confidence, investors are turning once again to gold as their trusted safe haven. Let’s explore what’s driving this renewed interest, why it matters, and what it could mean in the coming months.

Why Gold is Back in the Spotlight

Gold has always been seen as a stable asset when the world feels shaky. Whenever there’s confusion in the markets or fear about the economy, investors tend to move away from risky assets and towards something more secure—like gold. Right now, that’s exactly what’s happening.

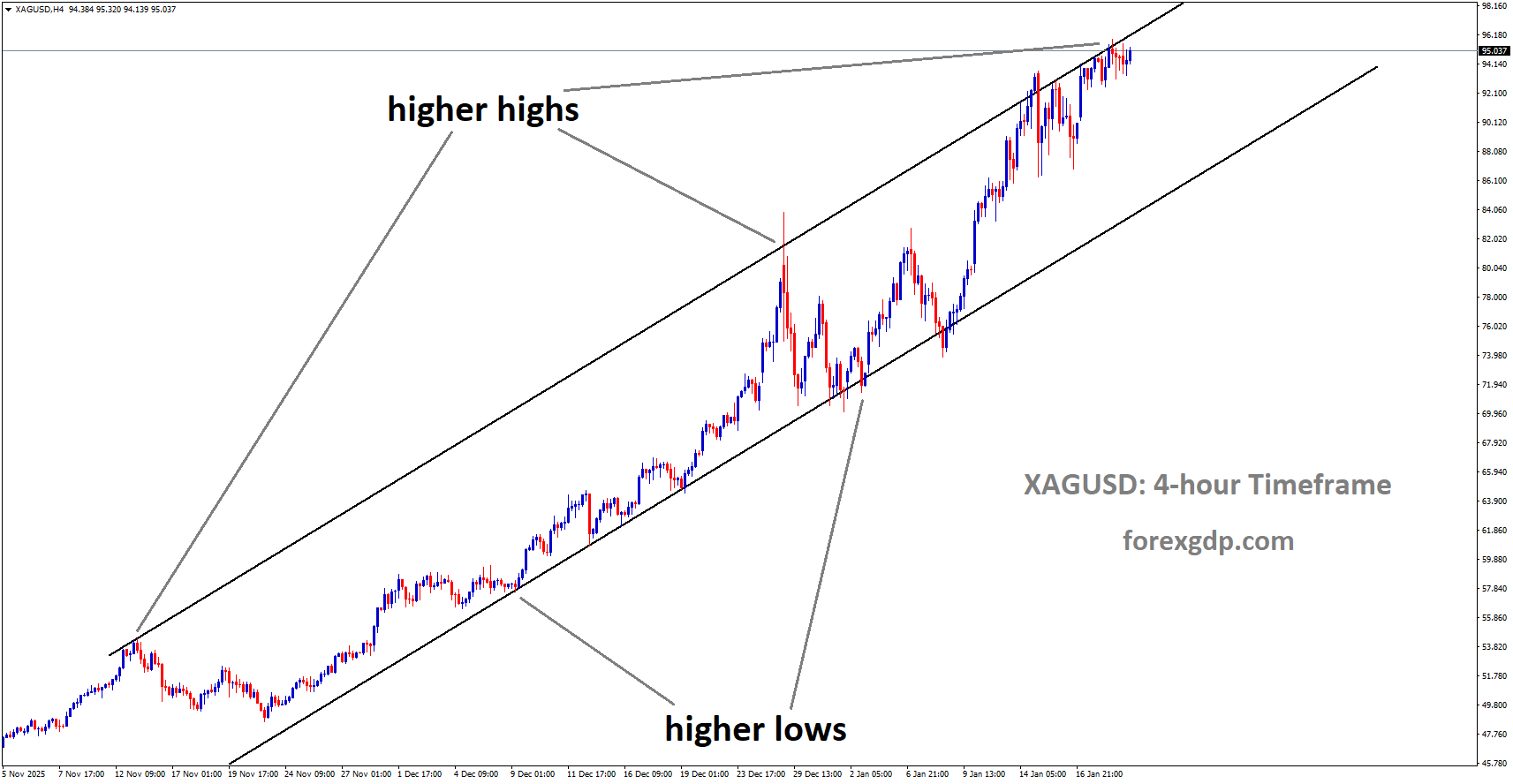

XAUUSD is moving in an uptrend channel, and the market has reached a higher high area of the channel

Recent economic indicators show rising uncertainty in the U.S. A government shutdown that’s dragged on longer than expected, combined with weak consumer confidence, is making both everyday citizens and big investors nervous. The University of Michigan’s latest Consumer Sentiment report dropped to its lowest level since mid-2022. People are clearly worried about how political gridlock and inflation might affect their wallets.

When households start losing confidence in the economy, it sends a powerful signal. It suggests that spending may slow down, companies could cut back on hiring, and economic growth might weaken. For investors, that’s a red flag—and a reason to look for assets that don’t depend on how the stock market performs.

A Perfect Storm for Safe-Haven Demand

Government Shutdown Woes

The ongoing U.S. government shutdown has created a lot of noise in the financial system. Many federal employees are unpaid, and government services are either delayed or suspended. That kind of disruption affects business confidence and the overall flow of money in the economy. Investors are well aware of this—and they’re reacting accordingly.

The longer the shutdown continues, the more it hurts economic growth. Even White House officials have admitted that it’s having a bigger impact than they expected. This kind of political standoff adds layers of risk to an already uncertain environment, pushing investors toward safer options like gold.

Weak Consumer Confidence

Another major concern is how people feel about the future. When the average American becomes less confident about jobs, income, or prices, it tends to slow down economic activity. The University of Michigan survey showed that many households are uneasy about rising prices and the potential fallout from the government shutdown. Inflation expectations for the next year have inched up again, while long-term expectations are holding steady.

This lack of confidence doesn’t just affect consumer spending—it also shapes the broader market sentiment. When people spend less, businesses earn less, and that ripple effect eventually reaches the stock market. As a result, many investors are reducing their exposure to stocks and moving their money into assets like gold that hold value better in uncertain times.

Interest Rate Speculation and Gold’s Outlook

Market Expectations of a Fed Rate Cut

Another big driver behind gold’s strength is the growing belief that the U.S. Federal Reserve might cut interest rates sooner rather than later. Market analysts are estimating a strong probability that a rate cut could happen by the end of the year. That expectation alone is enough to send gold prices upward.

Why? Because lower interest rates typically weaken the U.S. dollar and make non-yielding assets like gold more attractive. When rates fall, the opportunity cost of holding gold—an asset that doesn’t pay interest—decreases. In simple terms, people are more willing to hold gold because it performs better when rates are low.

The Job Market Slowdown

Adding to the mix is growing evidence that the U.S. job market might be losing steam. A recent report indicated that companies cut the largest number of jobs in over two decades. If employment growth continues to slow, it will give the Federal Reserve another reason to consider cutting rates to stimulate the economy.

That scenario tends to benefit gold. As rates fall and job growth weakens, the economy becomes less stable—conditions that usually make investors nervous and push them toward safe assets.

Global Factors Supporting Gold Demand

Gold isn’t just reacting to U.S. news. There’s a global side to this story too. The World Gold Council recently reported strong demand for gold exchange-traded funds (ETFs), especially in North America and Asia. These inflows show that investors worldwide are actively seeking gold exposure as part of their portfolios.

In North America, many investors view gold as protection against a weakening dollar and political unpredictability. Meanwhile, in Asia, gold demand has long been tied to cultural and financial factors—people in countries like India and China traditionally see gold as a store of value and a symbol of security. When global uncertainty rises, these investors often ramp up their purchases.

The fact that ETFs—one of the easiest ways to invest in gold—are seeing steady inflows is a clear indication that institutional and retail investors alike are positioning for ongoing market volatility.

The Broader Picture: Why Gold Still Matters

It’s easy to think of gold as an old-fashioned investment, but its relevance today is as strong as ever. In times of inflation, currency instability, or political drama, gold often acts as a balancing force in portfolios. It doesn’t rely on corporate earnings, government stability, or interest rates in the same way that other assets do.

XAUUSD is moving in an Ascending Triangle pattern, and the market has fallen from the resistance area of the pattern

In today’s complex global environment, where economies are recovering unevenly and central banks are walking a tightrope between inflation control and growth, gold provides a sense of balance. It’s not just about profit—it’s about protection. For both individual investors and large institutions, gold remains a cornerstone of stability.

Final Summary

Gold’s latest rise is more than just a price move—it’s a reflection of global anxiety and economic shifts. With a prolonged U.S. government shutdown, falling consumer confidence, and an uncertain job market, investors are naturally seeking safety. Add in growing expectations of a Federal Reserve rate cut, and the conditions for gold’s strength become even clearer.

On a global level, steady inflows into gold ETFs and rising demand in Asia show that the precious metal’s appeal crosses borders. As the world navigates unpredictable times, gold continues to stand out as one of the few assets that provide comfort, confidence, and continuity.

While markets may fluctuate and economic headlines may change daily, one thing remains true—gold has always been, and continues to be, the ultimate safe haven when uncertainty takes center stage.

EURUSD Gains Ground as Prolonged U.S. Shutdown Sparks Dollar Sell-Off

The EUR/USD currency pair made a modest comeback, gaining 0.16% as traders reacted to a sluggish U.S. economic outlook and growing concerns about the government shutdown dragging on for more than a month. While the overall market remained quiet due to a lack of major data releases from both the U.S. and Europe, the Euro found support as investors shifted away from the U.S. Dollar amid rising uncertainty.

The Market Mood: A Struggle Between Confidence and Caution

It’s been a turbulent week for financial markets. The U.S. government’s ongoing shutdown—now extending well beyond its usual duration—has created a sense of hesitation among investors. When the government isn’t fully operational, it not only delays important data releases but also heightens fears about the overall economy’s direction.

Despite the uncertainty, the Euro managed to hold its ground. Traders typically flock to the U.S. Dollar during times of crisis because it’s seen as a safe haven. But this time, something different happened. Instead of choosing the Greenback, investors found the Euro a more stable option, especially as concerns about U.S. fiscal health and stock market volatility grew.

Adding to the tension, Wall Street’s major indices slid amid worries that artificial intelligence (AI)-driven stocks may be overvalued. This wave of selling across the U.S. equity markets pushed investors to rethink their risk appetite, indirectly benefiting the Euro.

EURUSD is moving in a descending channel, and the market has reached the lower high area of the channel

Economic Data Paints a Mixed Picture

U.S. Sentiment Takes a Hit

Consumer sentiment in the U.S. turned gloomier, according to the University of Michigan’s November report. The index showed a sharp drop in confidence, suggesting that American households are becoming more skeptical about the near-term economic outlook.

At the same time, the New York Federal Reserve’s survey revealed that short-term inflation expectations eased slightly, though longer-term projections remained steady. This pattern suggests consumers believe inflation might moderate soon, but they’re not entirely convinced it’s under control.

Federal Reserve Vice Chair Philip Jefferson reinforced the cautious tone, noting that the central bank will proceed carefully with future policy adjustments. He emphasized that decisions will depend on upcoming data—which could be delayed due to the government shutdown—and that the Fed wants to avoid overcorrecting the economy.

European Indicators Show Slight Weakness

Across the Atlantic, data from Germany’s trade balance showed a smaller surplus than expected. While still positive, the drop hinted that Europe’s largest economy might be feeling the impact of slowing global trade.

Additionally, retail sales in the Eurozone declined unexpectedly in September. This came as a disappointment following earlier signs of recovery in the services sector. It served as a reminder that while parts of Europe’s economy are stabilizing, consumer demand remains fragile.

Why the Euro Is Holding Steady Despite Weak Data

It might seem counterintuitive that the Euro is performing relatively well when European data looks soft. But markets often behave based on relative strength—that is, how one economy compares to another. Right now, the U.S. economy faces a mix of political gridlock, falling consumer confidence, and fading optimism in the stock market.

That combination makes the Euro slightly more attractive in comparison. Traders believe that while the European economy is slow, it’s not facing the same level of uncertainty as the U.S., especially given the extended government shutdown and mixed signals from the Federal Reserve.

In essence, the Euro’s rise isn’t because Europe is booming—it’s because investors are temporarily losing faith in the Dollar. The shift in preference highlights how sentiment and risk perception play a crucial role in currency movements, even when economic fundamentals look shaky on both sides.

Investor Sentiment and the Path Ahead

Looking ahead, the EUR/USD pair may remain within a narrow trading range as both economies navigate through uncertain times. Market participants are watching for any signs of resolution in Washington, as a continued shutdown could lead to delays in critical economic data, complicating the Federal Reserve’s next policy move.

For Europe, attention remains on how countries manage inflation and sluggish demand. If consumer confidence and spending continue to weaken, it could limit the Euro’s upside potential. However, if the U.S. continues to show signs of instability, the pair could still find support at current levels.

Traders are also monitoring inflation expectations closely. While short-term expectations in the U.S. have slightly declined, the medium-term view remains stable, suggesting that price pressures are easing but not disappearing. This mixed outlook leaves both the Fed and the markets in a wait-and-see mode.

Final Summary

In summary, the EUR/USD pair’s modest rise reflects a blend of global caution, shifting investor sentiment, and ongoing political tension in the United States. The prolonged U.S. government shutdown, fading consumer optimism, and cautious Federal Reserve tone have collectively weighed on the Dollar, giving the Euro some breathing space.

Europe’s economy isn’t showing strong momentum either, with declining trade and retail figures, but it’s currently viewed as a safer bet compared to the uncertainty surrounding U.S. fiscal policy.

As long as the U.S. government remains in gridlock and market confidence stays low, the Euro could continue to attract moderate interest. Still, without significant improvements in economic performance on either side, traders should expect the EUR/USD to remain range-bound, driven more by sentiment and politics than by clear economic strength.

In these kinds of uncertain times, currency markets tend to move not just on numbers, but on trust and perception—and right now, the Euro is benefiting from a rare moment where it looks just a bit steadier than the Dollar.

GBPUSD trades cautiously as US sentiment slips under shutdown pressure

The GBP/USD pair managed to hold onto small gains on Friday, rising slightly even as global markets faced uncertainty. There were no major economic updates from the UK, leaving traders to focus on developments from the United States. The lack of fresh data, combined with the ongoing US government shutdown, kept volatility relatively muted. Despite dipping earlier in the day, the British Pound managed to rebound modestly as investors showed a cautious sense of optimism.

GBPUSD is moving in a descending channel, and the market has rebounded from the lower low area of the channel

While the market tone was generally quiet, traders were paying close attention to every bit of information coming from the Federal Reserve and the US economic landscape. The mild rebound in GBP/USD came as part of a broader trend where traders were hesitant to take bold positions due to uncertainty about future interest rate moves and economic performance in the US.

Fed Officials Signal Patience: No Rush to Cut Rates

One of the key highlights of the day was a statement from Federal Reserve Vice Chair Philip Jefferson. He made it clear that the Fed intends to move carefully when it comes to cutting interest rates. According to him, the policy rate is getting close to what is known as the “neutral level”, meaning it’s neither restricting nor boosting the economy. This cautious stance reflects the Fed’s desire to avoid moving too fast, especially at a time when data gaps caused by the government shutdown make it harder to assess the true state of the economy.

Jefferson also emphasized that the Fed will continue to take a meeting-by-meeting approach, adjusting decisions based on incoming information rather than making long-term promises. This approach is meant to provide flexibility, allowing the central bank to respond appropriately to whatever challenges or surprises arise in the coming months.

The cautious tone from the Fed suggests that while rate cuts might be on the horizon, they are not expected to come quickly or aggressively. For currency traders, this means the US Dollar could remain relatively stable, especially if economic data continues to show signs of resilience. However, any signs of slowing growth could quickly shift sentiment in favor of other currencies, including the British Pound.

Weak US Consumer Sentiment Adds to Economic Concerns

The economic picture in the US became a bit darker on Friday when the University of Michigan released its latest Consumer Sentiment report. The data showed a noticeable drop in confidence, with the index falling to 50.3 in November from 53.6 in October. This decline reflects growing worries among consumers about the potential negative impact of the prolonged government shutdown.

Consumers appear increasingly concerned about the economy’s direction, job security, and future spending potential. Such a decline in sentiment is often seen as an early warning sign that consumer spending, which is a major driver of the US economy, could slow down in the coming months.

Adding to these worries, inflation expectations have become somewhat mixed. While short-term expectations for one year rose slightly from 4.6% to 4.7%, longer-term expectations dropped from 3.9% to 3.6%. This suggests that while consumers are feeling inflation’s effects in the short term, they still believe it might ease over the long run.

The White House’s Take on the Economic Slowdown

Even the White House acknowledged the growing economic strain caused by the shutdown. Economic Adviser Kevin Hassett said in an interview that the government’s partial closure is having a stronger impact than initially expected. He estimated that the US GDP growth for the quarter could drop by as much as 1 to 1.5% as a result of delayed operations and reduced productivity.

This kind of disruption doesn’t just affect government employees—it also creates ripple effects throughout the private sector. Businesses that rely on federal contracts or approvals may face delays, and consumer confidence can weaken as uncertainty rises. For global investors, this adds another layer of caution when dealing with the US Dollar.

The Bigger Picture: Sterling’s Subtle Strength Amid Global Uncertainty

Despite all the noise from the US side, the British Pound has quietly shown signs of resilience. Even without major UK economic releases, the currency has managed to maintain a steady tone, supported by expectations that the Bank of England (BoE) may eventually start easing policy at a slower pace compared to the Fed.

Traders have also been keeping a close eye on how Brexit-related trade flows, inflation trends, and the broader European economy might influence the Pound in the months ahead. For now, the market mood is one of cautious optimism. The Pound’s modest gain reflects a balance between weak global demand for riskier assets and the gradual stabilization of economic expectations in the UK.

While the Dollar has recovered some ground recently, it still looks set to end the week slightly weaker, reflecting a lack of strong momentum in the US economy. The US Dollar Index (DXY), which tracks the currency’s performance against major peers, has slipped modestly this week—suggesting that traders remain uncertain about the longer-term outlook.

Investors Eye the Next Moves

Looking forward, investors will likely continue monitoring two main factors: the Fed’s future communications and any signs of recovery in US economic sentiment. If consumer confidence continues to decline or if government operations remain disrupted for an extended period, the market could start pricing in earlier or deeper rate cuts from the Fed.

On the other hand, any sign of economic resilience—such as stronger job growth or better-than-expected spending data—could quickly shift sentiment back in favor of the Dollar. In contrast, the Pound’s performance will depend largely on how the UK economy responds to global headwinds and whether the BoE maintains its careful stance on monetary policy.

Final Summary

To sum up, GBP/USD ended the week with modest gains, supported by a weaker US Dollar and the Fed’s cautious tone. The key takeaway from recent developments is that both the Federal Reserve and the White House are acknowledging growing economic risks. The Fed’s slow and measured approach to rate adjustments, combined with the impact of the ongoing government shutdown, is keeping traders on edge.

Meanwhile, the British Pound continues to show quiet strength, holding its ground even without strong domestic catalysts. As the markets head into the next week, traders will likely remain focused on US data releases, consumer sentiment trends, and updates from central banks. With uncertainty still lingering on both sides of the Atlantic, the GBP/USD pair may continue to fluctuate within a cautious trading range until clearer economic signals emerge.

In essence, this week’s story has been one of patience, caution, and uncertainty—a mix that’s likely to define currency markets for a while longer.

USDJPY Falls From Recent Highs as Dollar Demand Eases This Week

The US Dollar is losing momentum this week, moving closer to its weekly lows as investors react to disappointing data and shifting global sentiment. The greenback has slipped after facing rejection from higher levels, while the Japanese Yen shows some resilience despite weaker domestic figures. Overall, the currency market remains uncertain, with traders watching closely for fresh insights from upcoming US consumer confidence data.

The Dollar Pulls Back Amid Market Uncertainty

The US Dollar eased lower on Friday, extending its losses for the week as traders turned cautious ahead of the release of the US Michigan Consumer Sentiment Index. After a brief attempt to recover, the currency gave up earlier gains, signaling hesitation among investors who are waiting for clearer economic direction.

USDJPY is moving in a descending triangle pattern, and the market has reached the lower high area of the pattern

The overall sentiment in the market has been risk-averse. Many investors are choosing to stay on the sidelines until they gain a better sense of where the economy is headed. Concerns over slowing consumer confidence in the United States have contributed to the Dollar’s weakness, while a mix of soft employment data and central bank remarks has only added to the uncertainty.

This week’s movement suggests that traders are reassessing expectations around the Federal Reserve’s monetary policy. While earlier optimism hinted at a stronger Dollar, the combination of cooling inflation indicators and weaker labor market signals has pushed investors to reconsider the possibility of future rate hikes.

Japan’s Economic Struggles Add Pressure on the Yen

Weaker Household Spending Dampens Optimism

In Japan, the Yen faced early pressure after data showed that household spending rose at a slower pace than economists expected. The 1.8% year-on-year increase in September fell short of the projected growth, suggesting that domestic demand is still fragile. Consumers remain cautious, likely due to rising living costs and stagnant wage growth.

These numbers reflect the broader challenge Japan faces in maintaining steady economic recovery. While inflation has increased in recent months, it has not translated into stronger household purchasing power. This imbalance continues to weigh on the confidence of policymakers who are striving to create sustainable growth.

Government and Central Bank Under the Spotlight

Japanese policymakers have also been vocal about the nation’s economic path. Earlier this week, Prime Minister Takaichi mentioned that Japan is still only halfway toward achieving stable and sustainable price growth. This statement has raised doubts about whether the Bank of Japan (BoJ) will move forward with its expected interest rate hike in December.

The hesitation from the BoJ adds another layer of uncertainty to the Yen’s performance. While many market participants anticipated a policy shift after years of ultra-low interest rates, recent data may prompt the central bank to delay or adjust its tightening plans. As a result, the Yen remains sensitive to any economic updates or policy remarks coming from Tokyo.

Global Currency Traders Remain on Edge

Mixed Signals From the US Labor Market

Across the Pacific, investors in the United States are digesting mixed employment data, which has complicated the overall outlook for the Dollar. While the job market remains relatively strong, signs of cooling wage growth and slower hiring have stirred debates about whether the economy is entering a softening phase.

These developments come after months of aggressive monetary tightening by the Federal Reserve aimed at curbing inflation. Although inflation has moderated, policymakers are walking a fine line between supporting growth and preventing an economic slowdown. Vice Chair Philip Jefferson’s comments later today are expected to shed more light on how the central bank interprets the recent data and what it might mean for interest rates moving forward.

Consumer Sentiment in Focus

The main event of the day for currency traders is the release of the Michigan Consumer Sentiment Index for November. Analysts expect the report to show a fourth consecutive month of decline, reflecting growing concerns among consumers about inflation, job security, and overall financial conditions.

A weaker reading could put additional pressure on the US Dollar by reinforcing the perception that American households are becoming less confident in the economy’s short-term prospects. On the other hand, a stronger result might help the Dollar stabilize, as it would suggest resilience in consumer spending — a crucial driver of US growth.

Japanese Warnings on Currency Volatility

Meanwhile, Japan’s Finance Minister Katayama has once again warned about excessive currency volatility. His remarks came after the Yen dropped to levels that previously triggered government intervention. These statements were intended to calm markets and remind traders that authorities remain vigilant about abrupt movements that could harm economic stability.

Such interventions, whether verbal or direct, play a significant role in influencing investor behavior. They serve as a reminder that policymakers are ready to step in if the currency becomes too weak or volatile, adding an extra layer of complexity to Yen trading.

A Week Marked by Shifting Sentiment

This week has been defined by cautious moves and shifting expectations. The US Dollar appears on track for a modest weekly loss, around 0.6%, as traders reassess their positions amid the evolving economic landscape. The mixed tone of data from both the US and Japan has kept the market in a state of indecision, with no clear trend emerging.

Risk sentiment remains fragile, and many participants prefer to wait for key economic reports before making major decisions. As both countries navigate uncertain paths — the US balancing inflation control with growth, and Japan striving for sustainable price stability — global currency markets are likely to remain sensitive to every policy statement and economic release.

Final Summary

The foreign exchange market has seen an eventful week, dominated by cautious sentiment and conflicting signals from major economies. The US Dollar’s decline reflects investor hesitation, driven by weak consumer confidence expectations and softer employment data. Meanwhile, the Japanese Yen continues to face domestic challenges, with subdued household spending and uncertainty over the Bank of Japan’s next policy move.

Looking ahead, traders will be watching for fresh cues from US consumer sentiment data and remarks by Federal Reserve officials. These insights could determine whether the Dollar finds new strength or continues its downward path. For now, volatility remains the defining feature of the currency landscape, reminding investors that global markets are still navigating a delicate balance between recovery and restraint.

USDCAD Drops as Strong Canadian Hiring Wave Puts Pressure on the Dollar

The Canadian Dollar, often known as the Loonie, gained strength against the US Dollar after Canada released surprisingly strong employment figures. This move helped the CAD snap its six-day losing streak, bringing back some confidence in the currency. The numbers showed that Canada’s job market remains resilient, even as other major economies are slowing down.

According to Statistics Canada, the country added 66,600 new jobs in October, which was a major surprise since analysts had expected a decline. This growth followed another strong month in September, showing that the Canadian economy continues to create jobs at a healthy pace. Even more encouraging, the unemployment rate dropped slightly to 6.9%, while the labor participation rate improved marginally.

USDCAD is moving in an uptrend channel, and the market has fallen from the higher high area of the channel

This surge in job creation came mainly from the services sector and private companies. It indicates that businesses are still confident enough to hire, even amid global economic uncertainty. Wage growth also showed solid improvement, with average hourly earnings rising by 4% compared to last year, suggesting that workers are still benefiting from pay increases. However, total hours worked fell slightly, partly due to temporary labor disruptions and strikes in certain industries.

The strength in employment adds to growing optimism that the Canadian economy remains stable heading toward the end of the year. It also helps reduce fears that Canada could slip into a prolonged slowdown.

Bank of Canada Likely to Stay on Hold for Now

The latest employment numbers could influence the Bank of Canada’s (BoC) upcoming policy decisions. The central bank recently lowered its benchmark interest rate by 25 basis points to 2.25%. That move was widely expected as inflation pressures had begun to ease slightly, and the economy showed signs of softening earlier this year.

However, with the labor market still performing strongly, policymakers may now feel less pressure to cut rates further. The BoC had already hinted that the current level of interest rates might be “about right” if inflation and growth continue along their projected path.

Most analysts believe that the BoC is likely to hold rates steady in its next meeting, rather than rushing to reduce them again. The strong job data supports that view, as it suggests that the economy is healthy enough to withstand the current borrowing costs.

Still, the upcoming inflation numbers will play a major role in shaping the central bank’s next steps. If price growth remains under control, the BoC will likely maintain its cautious stance through the rest of the year. Investors and traders will also keep a close eye on wage data, as sustained wage growth could potentially keep inflation higher for longer.

US Consumer Sentiment Weakens as Inflation Worries Linger

While Canada’s economy showed strength, the situation in the United States looked a bit different. The latest data from the University of Michigan’s consumer sentiment survey revealed that Americans are feeling less optimistic about the economy.

The overall consumer sentiment index fell to 50.3, marking a noticeable decline from the previous reading of 53.6. This drop reflected growing concerns about inflation and the broader economic outlook. Consumers are becoming more cautious about their spending habits, as persistent price increases continue to strain household budgets.

Interestingly, inflation expectations among US consumers presented a mixed picture. The one-year inflation outlook rose slightly to 4.7%, showing that people still expect prices to stay elevated in the short term. On the other hand, the five-year outlook eased to 3.6%, suggesting that Americans believe inflation will gradually come under control over time.

This combination of weak sentiment and sticky inflation has weighed on the US Dollar. Traders are starting to price in a slower pace of economic activity, which could limit the Federal Reserve’s ability to maintain higher interest rates for long.

The Impact on the US Dollar and USD/CAD Exchange Rate

The US Dollar Index (DXY), which measures the Greenback’s value against other major currencies, extended its losses for the third straight day. It slipped to a one-week low, reflecting investors’ growing caution toward the US economy.

This weaker tone in the US Dollar has been a major factor behind the USD/CAD pair’s decline, as the Loonie gained additional support from Canada’s robust employment figures. The combination of a confident Canadian economy and a softer US economic outlook created the perfect setup for CAD to strengthen further.

Currency traders often look at job reports and consumer sentiment data to gauge future monetary policy trends. In this case, the Canadian job data suggests a stable outlook, while the US numbers indicate growing economic unease. This divergence between the two economies adds momentum to the CAD’s rebound.

Broader Market Sentiment: Confidence vs. Caution

The difference in tone between the Canadian and US economies is quite striking right now. On one hand, Canada seems to be navigating global headwinds fairly well. Businesses continue to hire, wages are rising, and unemployment is gradually easing. These are all signs that domestic demand remains healthy.

On the other hand, US consumers are showing early signs of fatigue. The drop in confidence suggests that high prices and borrowing costs are starting to weigh more heavily on everyday spending decisions. If this trend continues, it could slow down the world’s largest economy in the coming months.

For global investors, this contrast presents both opportunities and risks. A strong Canadian economy could attract more foreign investment into the country, strengthening the Loonie further. But if the US slowdown intensifies, it might eventually spill over into Canada, given how closely the two economies are linked.

Final Summary

The USD/CAD pair weakened as the Canadian Dollar surged on the back of stronger-than-expected job growth and solid wage data. Canada’s labor market continues to defy expectations, supporting the view that the Bank of Canada may pause further rate cuts for now. Meanwhile, the US economy is showing signs of cooling, with consumer sentiment falling sharply and inflation concerns lingering.

As a result, investors are tilting toward a more positive outlook for the Canadian Dollar in the near term. The mix of solid domestic data in Canada and softening conditions in the US makes the CAD an attractive bet for traders looking for short-term stability.

Overall, the week’s developments highlight a growing economic divergence between the two neighbors. While Canada’s resilience keeps the Loonie supported, the US Dollar faces pressure from cautious consumers and mixed inflation signals. How these trends evolve in the next few months will determine whether the recent shift in USD/CAD momentum turns into a lasting trend.

USDCHF edges up with renewed Dollar demand boosting sentiment

The USD/CHF currency pair has been showing a modest upward trend, reflecting renewed demand for the US Dollar as global traders digest the latest policy signals from both the Federal Reserve and the Swiss National Bank (SNB). Let’s break down what’s driving this move and what it could mean for the coming days.

A Renewed Push for the US Dollar

The US Dollar has gained strength recently as investors react to mixed signals from Federal Reserve officials. Throughout the week, policymakers have offered differing opinions on whether the central bank will continue cutting interest rates or hold steady in the face of inflation pressures.

USDCHF is moving in a descending channel, and the market has fallen from the lower high area of the channel

Chicago Fed President Austan Goolsbee expressed a calm stance, suggesting there’s no immediate rush to lower rates. On the other hand, Cleveland Fed President Beth Hammack took a firmer view, emphasizing that inflation remains the more pressing issue. She argued that maintaining rates at a slightly restrictive level could help balance the central bank’s twin goals—keeping inflation in check while supporting employment.

These comments have fueled speculation that the Fed might hold off on any December rate cuts, strengthening the Greenback as traders reassess their expectations. The tone among Fed officials suggests that while progress on inflation has been made, the battle isn’t over yet.

Market Focus Turns to Upcoming Fed Speeches

Investors are closely watching for more clarity from upcoming speeches by key Fed figures, including John Williams, Philip Jefferson, and Stephen Miran. Their remarks could further shape market sentiment and provide insights into whether policymakers are united or divided on the path forward.

The timing is particularly important because the next few weeks will likely set the tone for early 2025’s monetary strategy. Any hint of hesitation or a hawkish undertone could keep the Dollar supported against other major currencies, including the Swiss Franc.

Meanwhile, traders will also be paying attention to upcoming economic data, such as the University of Michigan’s Consumer Sentiment report, which provides valuable clues about household confidence and spending expectations. Strong consumer optimism could back the case for a resilient economy, making it even harder for the Fed to justify quick rate reductions.

Switzerland’s Steady Outlook and SNB’s Confidence

Across the Atlantic, the Swiss National Bank continues to project a calm, measured approach to monetary policy. SNB Chair Martin Schlegel recently indicated that inflation in Switzerland could see a mild rise over the coming quarters but remains well under control. Importantly, he signaled that interest rates are likely to stay stable for a prolonged period, reflecting confidence in the country’s economic resilience.

Switzerland’s labor market remains firm, with the unemployment rate holding steady at 3.0% in October. This stability underscores the strength of the domestic economy, which has helped maintain the Swiss Franc’s reputation as a reliable safe-haven currency during times of global volatility.

However, the SNB’s preference for keeping rates steady could mean that the policy gap between the US and Switzerland might widen slightly, especially if the Fed delays cutting rates. This potential divergence tends to favor the US Dollar, as higher returns attract investors seeking yield advantage.

Safe-Haven Demand Still Supports the Franc

Despite the current uptick in USD/CHF, the Swiss Franc continues to enjoy strong support from its safe-haven appeal. When global uncertainty rises—whether from geopolitical tensions, inflation worries, or slowing global growth—investors often turn to the CHF as a defensive asset.

For now, though, with global markets relatively stable and US policymakers emphasizing caution rather than easing, the Dollar has managed to regain short-term momentum. This tug-of-war between risk appetite and safety demand is likely to define the USD/CHF trend in the near term.

What Traders Are Watching Next

Looking ahead, the key factors influencing USD/CHF will include:

-

Upcoming US economic data: Reports on consumer sentiment, inflation, and employment will provide insights into whether the Fed’s cautious stance is justified.

-

Fed commentary: Any shift in tone from upcoming speeches could either fuel or cool market expectations for early 2025 rate cuts.

-

Global sentiment: Developments in Europe, Asia, and the Middle East could quickly swing safe-haven flows back toward the Swiss Franc if uncertainty spikes.

For now, the pair’s recent upward movement reflects a balancing act between renewed US Dollar strength and Switzerland’s ongoing economic stability. Traders are adopting a wait-and-see approach until the next wave of policy guidance becomes clearer.

Final Summary

The USD/CHF pair has climbed modestly as investors weigh contrasting messages from US and Swiss central bankers. The Federal Reserve appears cautious about cutting rates too soon, with officials emphasizing the need to keep inflation in check. This stance has bolstered the US Dollar, at least temporarily.

On the Swiss side, the SNB’s steady policy stance and resilient labor market continue to project confidence in the economy, ensuring that the Franc retains its safe-haven reputation.

Overall, the tug between a firm US Dollar and a stable Swiss Franc is likely to keep the USD/CHF pair moving within a controlled range for now. As the global financial narrative evolves, traders will be watching every speech and report for clues on the next big move.

AUDUSD Holds Steady While Traders Question the Fed’s Next Move

The Australian Dollar (AUD) has managed to stay steady against the US Dollar (USD), even as the American economy shows signs of weakening consumer confidence. The AUD/USD pair is hovering near the mid-0.64 range, showing resilience after a sharp drop in US sentiment data. This steady performance suggests that investors are now focusing less on short-term fluctuations and more on what lies ahead in terms of interest rates and global economic direction.

Recently, the University of Michigan’s Consumer Sentiment Index revealed a disappointing picture of how Americans feel about their economy. Confidence slipped notably in November, indicating that people are becoming increasingly concerned about inflation and overall financial conditions. Such figures often act as a reflection of how optimistic consumers are about spending, employment, and income growth — all key drivers of economic health.

AUDUSD is moving in an uptrend channel, and the market has reached a higher low area of the channel

The report also noted that while short-term inflation expectations edged slightly higher, longer-term expectations eased a bit. This mix signals that while consumers remain uneasy about immediate inflation pressures, they do not foresee extreme inflation persisting over the coming years. The result? Traders are beginning to believe that the Federal Reserve (Fed) might soon adjust its monetary policy toward a softer, more supportive stance.

The Federal Reserve’s Balancing Act: What Comes Next?

For months, the Federal Reserve has been trying to balance two competing goals — controlling inflation and keeping the economy stable. The latest dip in consumer confidence adds more pressure on the Fed to consider rate cuts sooner than expected. Some investors now believe that a rate reduction could happen before the end of the year, as slowing sentiment and job market concerns weigh on economic momentum.

The cautious remarks from Fed Chair Jerome Powell suggest that the central bank is not yet ready to commit to any decision. Powell has repeatedly emphasized the need for more data before determining whether policy changes are necessary. This uncertainty is what currently drives the volatility in the US Dollar, which has pulled back slightly as traders wait for clearer signals.

In addition, the US job market has shown some early signs of cooling. According to recent employment reports, companies announced over 150,000 job cuts in October — a sign that businesses are preparing for slower growth. These developments feed into the broader expectation that the Fed might soon shift from fighting inflation to supporting the economy through monetary easing.

Australia’s Calm Approach: Stability Over Aggression

While the US faces policy uncertainty, Australia’s Reserve Bank (RBA) continues to maintain a more measured stance. In its latest meeting, the RBA decided to keep its Official Cash Rate unchanged, signaling that it prefers to observe the economic trend before making any major adjustments. Governor Michele Bullock highlighted that although inflation remains above the desired level, there was no discussion of cutting rates anytime soon. This decision reflects the central bank’s commitment to ensuring stability rather than reacting hastily to global market swings.

However, Australia’s economic performance still depends heavily on external factors, particularly demand from China — its largest trading partner. Concerns over slower Chinese growth and reduced commodity demand have kept the Australian Dollar’s upward movement limited. Despite this, the AUD continues to attract some support from investors seeking currencies tied to strong resource-driven economies.

Another factor supporting the Aussie is the general belief that Australia may navigate global headwinds better than some Western economies. With relatively stable employment figures and ongoing government spending in infrastructure and services, Australia’s domestic outlook remains more optimistic compared to regions facing deeper inflation shocks.

Market Sentiment: A Wait-and-Watch Phase

Right now, both the Aussie Dollar and the US Dollar are caught in a period of uncertainty. The markets are trying to assess which central bank — the Fed or the RBA — will move first and how aggressively. Traders often describe this phase as a “wait-and-watch” period, where neither side gains strong momentum.

On one hand, the weakening of US consumer sentiment has pushed traders to believe in a softer Federal Reserve, which usually leads to a weaker US Dollar. On the other hand, Australia’s cautious policy tone and dependence on China’s demand are keeping the AUD from rallying too strongly. This tug-of-war creates the sideways trading pattern seen in the AUD/USD pair.

In global markets, investor sentiment often shifts quickly based on the next major report or statement from policymakers. For now, the combination of mixed inflation expectations, weakening job data, and cautious central banks means that volatility could continue for some time. Most traders are avoiding big directional bets until they get stronger signals from either economy.

Looking Ahead: What Could Shape the Next Move

Several key factors could influence how the AUD/USD performs in the coming weeks:

-

Federal Reserve statements and data releases: If upcoming US inflation and employment data show continued weakness, expectations for a rate cut will strengthen. This would likely weigh on the US Dollar.

-

Chinese economic performance: Any sign of improvement in China’s growth or stimulus efforts could benefit the Australian Dollar, given the close trade links between the two nations.

-

Global risk sentiment: When global investors feel more confident about growth, they tend to move away from the safe-haven US Dollar toward higher-yielding currencies like the AUD.

While predicting exact market movements is impossible, it’s clear that the tone of central banks and the health of global demand will remain the most important factors guiding currency traders in the near future.

Final Summary

The AUD/USD pair remains steady despite growing uncertainty in the US economy and shifting central bank policies. Weak US consumer confidence and mixed inflation expectations have increased speculation that the Federal Reserve might soon ease its monetary stance. Meanwhile, the Reserve Bank of Australia continues to emphasize patience and stability, preferring to monitor inflation trends before making any changes.

Both economies are facing their own challenges — the US with slowing sentiment and job cuts, and Australia with dependence on China’s economic outlook. As a result, the market is now in a delicate balance, waiting for clearer direction from policymakers.

In the weeks ahead, traders will be watching how inflation, employment, and global demand evolve. The Aussie Dollar’s ability to stay firm amid uncertainty shows that investors still view it as a relatively stable option in a world of fluctuating currencies. However, sustained momentum for the AUD/USD pair will likely depend on how soon confidence returns to the global economy and how central banks respond to the changing economic climate.

NZDUSD Extends Decline on Expectations of RBNZ Rate Cuts

The New Zealand Dollar (NZD) continues to face headwinds, slipping to its weakest level in six months against the US Dollar (USD). This decline reflects a combination of local economic uncertainty, potential policy changes from the Reserve Bank of New Zealand (RBNZ), and broader shifts in global trade and investor sentiment. Let’s break down what’s driving this movement and what could come next for the Kiwi currency.

RBNZ’s Policy Expectations Weigh Heavily on the Kiwi

One of the biggest reasons behind the recent fall of the New Zealand Dollar is growing speculation about monetary policy easing by the RBNZ. After a weaker-than-expected jobs report, markets are now fully pricing in a 25-basis-point rate cut in November.

NZDUSD is moving in a descending triangle pattern

Why a Rate Cut Matters

When a central bank lowers interest rates, it typically makes the country’s currency less attractive to investors seeking higher returns. Lower rates can stimulate spending and borrowing, but they also tend to weaken the national currency in the foreign exchange market.

This expectation of a rate cut has caused traders to pull back from the NZD, leading to continued selling pressure. Many investors are looking for clues on how long the RBNZ may maintain its cautious stance, especially as economic growth slows and inflation pressures ease.

Economic Indicators Point to Slowdown

Recent economic data has painted a mixed picture for New Zealand. The job market is cooling, and consumer spending remains soft, suggesting that domestic demand is weakening. This aligns with the central bank’s ongoing efforts to balance inflation control with economic stability. With inflation gradually retreating toward target levels, the RBNZ now has more room to consider easing policy without risking runaway price growth.

China’s Slowing Trade Adds More Pressure

New Zealand’s economy is heavily tied to China’s performance, particularly through exports of dairy and agricultural goods. Recent trade data from China indicates a slowdown in exports and a modest rise in imports, signaling that demand in one of New Zealand’s key trading partners is softening.

China’s Trade Figures Tell the Story

China’s latest trade balance figures showed exports falling 0.8% year-over-year in October, compared to a sharper decline earlier in the year. Imports rose slightly, suggesting that while domestic demand in China is recovering, global appetite for Chinese goods remains uneven. The country’s overall trade surplus expanded less than expected, which can ripple through global markets — and New Zealand often feels the effects first.

Because China is such a vital part of New Zealand’s trade network, any slowdown in Chinese demand or production tends to reduce demand for New Zealand’s exports. This dynamic puts additional downward pressure on the NZD, especially when global investors are already in a risk-off mood.

A Silver Lining: Easing Trade Tensions

On a more positive note, recent signs of improving relations between the United States and China could offer some relief. Washington has announced plans to suspend certain tariffs on Chinese imports related to the shipbuilding sector. This step might reduce friction in global trade, indirectly benefiting export-driven economies like New Zealand’s.

If trade tensions continue to ease, global risk sentiment could improve, potentially supporting currencies like the NZD that tend to benefit from a more optimistic global outlook.

The Strong US Dollar and Market Caution

While the NZD struggles, the US Dollar has held firm, benefiting from global risk aversion and cautious investor behavior. When markets become uncertain, investors tend to flock to the USD as a safe haven, pushing it higher against other currencies.

Investor Focus on US Economic Data

Traders are now watching the release of the Michigan Consumer Sentiment Index, a key measure of how American consumers feel about the economy. Strong consumer confidence can signal steady economic growth, which supports the USD. However, upcoming data releases have been delayed due to a potential US government shutdown, adding an extra layer of uncertainty.

Despite these challenges, the greenback remains supported as investors stay cautious about taking risks in volatile markets. The combination of solid consumer spending, slower inflation, and the Federal Reserve’s measured policy approach has kept the US Dollar resilient.

Fed Policy and Rate Cut Speculations

Interestingly, some recent reports have hinted at potential changes in US monetary policy later this year. The Challenger Job Cuts report revealed an uptick in planned layoffs, which could prompt the Federal Reserve to consider lowering interest rates in December. According to market data, traders are now pricing in about a 67% chance of a rate cut, up from 62% just a day earlier.

If the Fed does decide to ease policy, it might temporarily weaken the USD. However, the dollar’s strength often persists due to its role as a global reserve currency, especially when other economies — like New Zealand — are facing their own growth challenges.

What Could Happen Next for NZD/USD

The NZD/USD pair is currently in a fragile state, and the next few weeks could determine its short-term direction. The key factors to watch include the RBNZ’s policy meeting in November, updates from China’s economic data, and the tone of upcoming US economic releases.

If the RBNZ follows through with a rate cut and signals that more easing may come, the Kiwi could remain under pressure. On the other hand, if the central bank takes a more balanced approach — emphasizing stability rather than aggressive easing — the currency might find some room to recover.

Meanwhile, any improvement in US-China trade relations or signs of stronger Chinese demand could help New Zealand’s export sector regain some momentum, offering a potential lifeline to the NZD.

Market Sentiment Will Play a Big Role

Currency markets are not just about numbers and policies — they’re driven by perception and emotion as much as data. When investors feel uncertain about global growth, they tend to prefer safer assets like the US Dollar. Conversely, when confidence returns, riskier currencies like the NZD often rebound quickly.

So, the Kiwi’s path forward will largely depend on how traders interpret the balance between economic risks and opportunities in both local and global markets.

Final Summary

The New Zealand Dollar’s recent fall to a six-month low against the US Dollar underscores the complex web of global and domestic forces shaping currency markets today. With expectations of a rate cut from the RBNZ, weaker local data, and China’s trade slowdown, the NZD has faced significant pressure. At the same time, the US Dollar’s strength, supported by cautious investor sentiment, has kept the pair subdued.

Yet, there are still bright spots ahead. Any sign of recovery in Chinese demand, progress in global trade discussions, or a more measured tone from the RBNZ could give the NZD a chance to bounce back. For now, traders and investors alike will be keeping a close eye on how both central banks — in New Zealand and the US — navigate the months ahead.

As the global economic picture continues to evolve, the NZD/USD story remains one of shifting momentum, cautious optimism, and the constant balancing act between growth and stability.

EURGBP Rises as Market Reacts to BoE’s Softer Policy Outlook

The Euro (EUR) climbed against the British Pound (GBP) after the Bank of England (BoE) took a softer approach to its monetary policy. This shift has sparked renewed interest in the Euro, with investors turning cautious on the Pound. Let’s dive into why this happened, what it means for both currencies, and what could be next for the Euro-Pound relationship.

The Bank of England’s Softer Tone Changes the Game

The Bank of England decided to keep its benchmark interest rate steady at 4%, but the real story lies in its tone. Out of the nine members on the Monetary Policy Committee (MPC), five voted to hold rates, while four wanted an immediate rate cut. That narrow 5-4 split signals something big — the BoE is getting increasingly dovish, meaning it’s leaning toward cutting rates in the near future.

EURGBP is breaking the lower high area of the descending triangle pattern

Why the Change in Attitude?

Governor Andrew Bailey acknowledged that inflation in the UK is cooling off faster than expected. That’s an important shift because inflation has been the key reason behind high interest rates. Bailey suggested that monetary policy “will not need to remain this restrictive for too long,” hinting strongly that rate cuts could arrive sooner rather than later.

This softer outlook immediately weighed on the British Pound. Investors interpreted it as a sign that the BoE is ready to ease up on its tight policy, making the Pound less attractive compared to other currencies, like the Euro.

The UK’s Economic Outlook and Upcoming Budget

While monetary policy is one piece of the puzzle, the UK government’s upcoming Budget is another major factor shaping the Pound’s direction. Scheduled for November 26, this budget could have a lasting impact on how the market views the UK economy.

Fiscal Challenges Ahead

Chancellor Rachel Reeves faces the difficult task of addressing a budget shortfall estimated between £20 and £30 billion. To manage this, analysts expect the government to take a fiscally cautious approach — likely involving tax increases and limited public spending.

Although this strategy might help balance the books, it also carries a downside. Higher taxes and lower government spending could slow down economic growth. That, in turn, would strengthen the argument for the Bank of England to cut interest rates sooner to support the economy. The combination of fiscal restraint and dovish monetary signals could keep the Pound under pressure for a while.

The European Central Bank Holds Its Ground

While the Bank of England edges toward easing, the European Central Bank (ECB) is standing its ground — for now. The ECB recently kept its deposit rate unchanged at 2%, maintaining a cautious but stable stance.

President Christine Lagarde noted that inflation in the Eurozone is easing, with price pressures moderating and the region’s economy expanding modestly. However, she also made it clear that the ECB’s policy is data-dependent. In other words, they’ll keep watching economic numbers closely before making any major moves.

A Balanced and Flexible Approach

Lagarde described the ECB’s current policy stance as “in a good place,” but also emphasized that this position isn’t set in stone. If inflation starts rising again or growth falters, the central bank is ready to act. This measured approach gives the Euro a sense of stability — something investors value during times of uncertainty in other economies, like the UK.

A Growing Monetary Policy Gap Between the UK and the Eurozone

The real story behind the recent Euro rebound lies in the growing policy gap between the Bank of England and the European Central Bank. While both central banks have paused rate hikes, their tones couldn’t be more different.

The BoE’s dovish bias — reflected in the split vote and Bailey’s remarks — points toward an earlier move to cut rates. In contrast, the ECB’s “wait-and-see” attitude shows more patience, suggesting it’s not in a hurry to ease policy just yet. This divergence is what’s driving investors toward the Euro and away from the Pound.

Investor Sentiment Shifts

In simple terms, when one central bank sounds eager to lower rates while another stays patient, traders tend to move their money toward the more stable option. That’s what’s happening here. The Euro looks more dependable compared to the Pound, which faces a mix of political, fiscal, and monetary challenges.

What This Means for the Future of EUR/GBP

The Euro’s recovery against the Pound could have lasting effects if the Bank of England continues down its dovish path. With inflation easing and the UK government tightening its fiscal belt, there’s increasing pressure on the BoE to support growth by cutting rates.

Meanwhile, the European Central Bank’s approach is providing confidence to Euro investors. By holding steady and avoiding premature moves, the ECB is giving the Euro an edge in stability — a key factor that could sustain its current strength against the Pound.

Long-Term Perspective

If this policy divergence continues, the EUR/GBP pair may remain tilted in favor of the Euro. The UK’s slower growth outlook and cautious fiscal policy could further weigh on Sterling. On the other hand, the Eurozone’s steady but careful approach to monetary management is likely to maintain its relative appeal.

However, the balance could shift if the Eurozone faces unexpected economic headwinds. Both regions are dealing with post-pandemic challenges, fluctuating energy prices, and slowing global trade — all of which could affect their respective currencies in the months ahead.

Final Summary

The recent rise of the Euro against the British Pound highlights how different monetary policies can shape currency markets. The Bank of England’s dovish tone and close voting split signal that interest rate cuts may not be far off, putting pressure on the Pound. Meanwhile, the European Central Bank’s patient and steady stance offers more reassurance to investors, boosting the Euro’s appeal.

As the UK prepares for its next budget and faces a growing fiscal gap, Sterling’s outlook remains uncertain. The Euro, backed by a more stable economic narrative and a cautious ECB, seems positioned to maintain its strength in the short term.

In essence, the divergence in central bank strategies — one leaning toward easing, the other staying firm — is reshaping the landscape for the Euro and the Pound. For now, the Euro’s edge looks secure, but as always, the global economic story is far from over.

BTCUSD Battles for Momentum as Traders Watch Closely

Bitcoin has seen a tough week, falling more than 8% and dipping below $100,000 for the first time since late June. This decline has left many investors wondering what’s driving the drop and whether this is the start of a deeper correction or just a temporary pause before another big move upward.

The biggest reason behind this downturn seems to be selling pressure from long-term Bitcoin holders—the so-called “OGs” of the crypto world. These are investors who have held onto their coins for months or even years and are now cashing out for profits. Over the past month, the amount of Bitcoin that was previously inactive for 180 days or more has suddenly become active again, suggesting that many experienced investors are moving their funds, likely to sell.

BTCUSD is moving in a box pattern, and the market has reached the support area of the pattern

What’s interesting is that this selling doesn’t seem tied to any major global event or policy change. Stocks and other risk assets have been performing relatively well, which means Bitcoin’s drop is more of a crypto-specific event rather than a reflection of the broader financial market. Analysts believe this could be part of a natural market cycle, where old holders take profits while new investors wait for better prices to enter.

Despite the short-term weakness, it’s worth noting that Bitcoin has a history of bouncing back—especially in November. Historical data shows that this month has often been one of Bitcoin’s best, averaging over 40% gains in previous years. So, while things look shaky now, there’s still hope for a strong rebound before the year ends.

Why Institutional Investors Are Also Pulling Back

Another factor putting pressure on Bitcoin is the recent decline in institutional interest. Large investors, such as funds and corporations that buy Bitcoin through spot ETFs (Exchange-Traded Funds), have been pulling money out at an alarming rate. This week alone saw over $660 million in total outflows, marking two straight weeks of reduced demand.

Tuesday was particularly rough, with more than $570 million leaving Bitcoin ETFs in a single day—the biggest withdrawal since early August. This indicates that many institutional investors are losing confidence or choosing to lock in profits rather than risk further downside.

However, not all institutions are stepping away. Michael Saylor, the head of MicroStrategy, announced that his company bought another 397 BTC, bringing their total holdings to over 641,000 coins. This shows that while some large players are retreating, others are doubling down and treating this dip as an opportunity.

The tug-of-war between these opposing strategies—profit-taking by some and accumulation by others—has created a mixed sentiment in the market. Many smaller investors are watching closely to see which group wins out before making their next move.

The Bigger Picture: Global Events and Market Sentiment

While Bitcoin’s price movements often seem isolated from the global economy, recent developments in the U.S. and China are subtly influencing investor confidence.

The U.S. government’s record-long shutdown, which has stretched beyond five weeks, has raised serious concerns about economic stability. Analysts estimate that the prolonged shutdown could shave up to 2% off the U.S. GDP for the quarter. The political deadlock in Congress has only deepened worries, especially as several attempts to pass a funding bill have failed.

At the same time, there’s a bit of positive news from the U.S.–China trade front. China announced plans to lift some tariffs on American agricultural goods and reduce others starting mid-November. This small gesture has improved global trade sentiment slightly. The U.S., on its part, has also eased some tariffs on Chinese imports related to pharmaceuticals and agricultural products.

Even so, these optimistic signals have not yet translated into a bullish mood for crypto markets. Traders remain cautious, unsure of how much the global economic backdrop will affect Bitcoin’s long-term performance. For now, investors are more focused on internal crypto dynamics, such as selling trends, institutional flows, and historical market cycles.

Are We Heading Toward Another Crypto Winter?

The big question on everyone’s mind is whether Bitcoin’s recent slide is just a temporary correction or the start of a more prolonged downturn—what the crypto community calls a “crypto winter.”

Data from blockchain analytics firms indicates that Bitcoin’s fundamentals have weakened in recent weeks. The price drop below the psychological mark of $100,000 has triggered nervousness, as this level has historically acted as a floor during strong market cycles. If Bitcoin fails to stabilize soon, there’s a chance of a deeper decline as investors lose confidence.

However, it’s important to remember that Bitcoin has always gone through cycles. Periods of rapid growth are often followed by corrections, during which weak hands sell and stronger investors accumulate. This natural rhythm has been part of Bitcoin’s story for over a decade, and it often leads to new highs once the dust settles.

In many previous cycles, long-term holders selling at the top were followed by months of consolidation before the next major rally. With increasing adoption from financial institutions, countries, and corporations, Bitcoin’s long-term foundation remains much stronger than it was in earlier cycles.

A Glimpse of Hope: November’s Historical Strength

Despite the current negativity, there’s good reason to remain optimistic. Historically, November has been Bitcoin’s strongest month. Data from past years shows that BTC tends to deliver an average return of around 42% during this period.

BTCUSD is moving in an uptrend channel, and the market has reached the higher low area of the channel

Even though October turned out to be disappointing, losing nearly 4%, the last quarter of the year (Q4) has traditionally brought significant gains. On average, Bitcoin’s Q4 performance has been close to 78%, fueled by holiday season optimism, institutional activity, and renewed investor confidence.

If history repeats itself, the coming weeks could see Bitcoin recover strongly from its current slump. Many investors are holding out hope that November’s momentum, combined with increasing adoption and positive long-term sentiment, could bring the next big breakout.

Final Summary

Bitcoin’s recent dip below $100,000 has stirred concern across the crypto community, but the broader picture is more nuanced. The sell-off seems largely driven by long-term holders taking profits, while institutional investors are also pulling back after a strong summer rally. However, influential figures like Michael Saylor continue to show faith in Bitcoin’s long-term future by increasing their holdings during the dip.

At the same time, global economic uncertainties—ranging from the U.S. government shutdown to shifting trade relations—have added to the cautious mood. Yet, Bitcoin’s history reminds us that downturns often precede powerful recoveries. November, in particular, has a strong track record of boosting BTC’s performance, and many in the market are still optimistic about a potential rebound before the year ends.

In short, while the short-term picture looks cloudy, Bitcoin’s long-term story remains bright. The market may be cooling off now, but the foundations being built through institutional adoption, increasing use cases, and global awareness could set the stage for Bitcoin’s next major rally in the months ahead.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!