XAUUSD Jumps Higher on Shutdown Fears, Traders Eye New Peak Levels

When the global economy shows signs of weakness or uncertainty, gold always manages to steal the spotlight. This week, the precious metal continued its upward march as investors turned to it for safety amid ongoing U.S. political and economic tensions. Let’s break down what’s driving this move and why the current environment continues to favor gold.

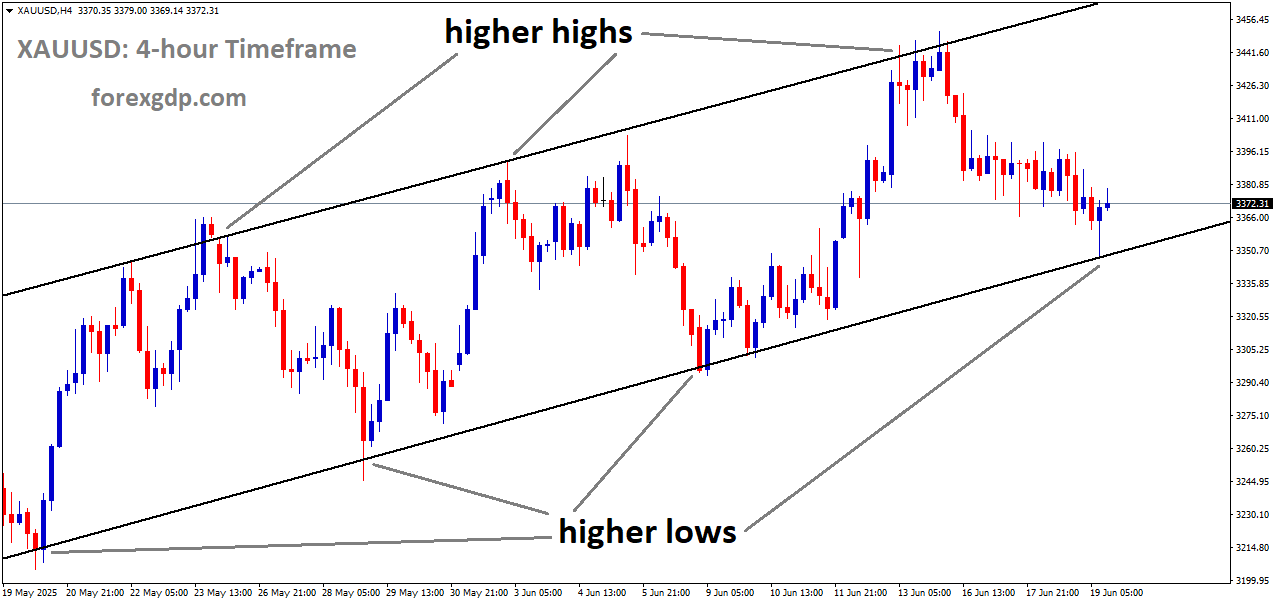

XAUUSD is moving in an uptrend channel, and the market has reached a higher high area of the channel

A Perfect Storm: Why Gold Is Back in Focus

Gold’s recent rally isn’t just about shiny metal fascination—it’s a reflection of deeper market anxiety. With the U.S. government shutdown dragging on, uncertainty has crept into financial markets once again. Whenever Washington struggles to find political agreement, the markets react, and investors often rush toward assets that feel safer—like gold.

The shutdown has also disrupted the regular flow of key economic data. Reports such as employment numbers and jobless claims have been delayed, leaving traders without crucial indicators that typically guide market expectations. In times like these, investors prefer the predictability of tangible assets, and gold naturally becomes their top pick.

On top of that, the Federal Reserve’s tone has turned noticeably softer. Policymakers have hinted that they’re open to keeping monetary conditions loose for longer, citing the need to rely on data rather than rigid policies. With interest rate cuts already being priced into the markets, gold benefits because lower rates make non-yielding assets more attractive.

The Fed’s Cautious Approach Fuels Confidence in Gold

One of the biggest influences on gold right now is the Federal Reserve’s stance. Fed Governor Stephen Miran recently emphasized that data access is crucial for guiding future decisions, but he also stressed the importance of being forward-looking. In other words, even if economic data remains unavailable due to the government shutdown, the Fed will still aim to anticipate conditions rather than overreact to temporary disruptions.

Similarly, Chicago Fed President Austan Goolsbee pointed out that the risks facing the U.S. economy are fairly balanced but reminded everyone that the central bank’s approach will remain data-dependent. This cautious stance has strengthened market expectations that rate cuts are just around the corner.

When interest rates fall or are expected to fall, gold tends to gain because its appeal as a store of value increases. Unlike bonds or savings accounts, gold doesn’t pay interest, but it also doesn’t lose value when rates drop. This makes it a perfect hedge when investors worry that the Fed might be preparing to loosen policy in a slowing economy.

Political Drama Adds to the Uncertainty

As if the economic data gap and dovish central bank signals weren’t enough, Washington’s political gridlock is adding fuel to gold’s momentum. The ongoing government shutdown shows no immediate sign of resolution. Both Democrats and Republicans are standing firm on their budget positions, and repeated attempts to pass funding bills have failed.

This political impasse is more than just a headline—it has real consequences. It delays government payments, stalls federal services, and creates ripple effects across multiple sectors of the economy. Every additional day of uncertainty reinforces the perception that safer investments are the smarter choice for now.

Meanwhile, global politics aren’t helping either. Reports suggest that China has been engaging in diplomatic negotiations with the U.S., pressing for a relaxation of trade and investment restrictions. While that could eventually ease tensions between the two nations, the lack of clarity in talks means global investors are staying cautious—once again turning to gold for stability.

Economic Signals Paint a Mixed Picture

Economic indicators have done little to calm nerves. The latest U.S. services sector readings showed a mixed performance. While one major index pointed to slow or stagnant growth, another suggested moderate expansion. This uneven data suggests that while some areas of the economy remain strong, others are starting to show signs of fatigue.

Employment data also delivered mixed results. Job openings rose slightly, suggesting ongoing resilience in the labor market. However, private payroll numbers showed unexpected job cuts in some sectors, revealing that companies might be preparing for slower growth ahead. Together, these signals don’t paint a clear picture—something that usually benefits gold, as investors prefer certainty over confusion.

In the bond market, yields on U.S. government debt have fluctuated as traders try to interpret what comes next for interest rates. Lower or volatile yields tend to support gold prices because they reduce the opportunity cost of holding the metal.

Global Investors Seek Stability Amid the Chaos

Gold’s allure goes beyond American politics or economic reports—it’s global. Investors across the world look to gold as a universal store of value when confidence in financial systems wavers. Whether it’s due to inflation fears, currency fluctuations, or political tension, gold offers something that few assets can: a sense of timeless security.

Right now, central banks in several countries are increasing their gold reserves as part of diversification strategies. This institutional demand adds another layer of support for the metal, strengthening its long-term outlook. Retail investors are following suit, taking advantage of every market dip to add gold to their portfolios.

What’s Next for Gold?

Looking ahead, much depends on how quickly the U.S. government can resolve the shutdown and whether the Federal Reserve sticks to its cautious tone. If the shutdown drags on and the economy shows more signs of strain, the Fed could lean even further toward cutting rates, which would likely give gold another boost.

However, even if Washington reaches a deal, it’s unlikely that the economic uncertainty will vanish overnight. Inflation pressures, global trade disputes, and shifting monetary policies will keep gold relevant for the foreseeable future.

XAUUSD is moving in an uptrend channel, and the market has rebounded from the higher low area of the channel

For everyday investors, this means one thing: gold remains a reliable anchor during turbulent times. It might not offer quick returns like riskier assets, but when the world feels unpredictable, owning gold provides peace of mind.

Final Summary

Gold’s steady climb reflects more than just market speculation—it’s a sign of broader unease in the global economy. With the U.S. government shutdown stretching on, key data missing, and the Federal Reserve adopting a softer stance, investors are turning to gold as a shield against uncertainty.

Political tensions, both domestic and international, continue to amplify the demand for safe-haven assets. Mixed economic data and volatile bond markets add another layer of caution, pushing more investors toward stability rather than risk.

In the big picture, gold’s strength reminds us that even in an era of advanced financial instruments and fast-paced markets, traditional assets still have their place. When everything else feels unstable, gold stands firm—quietly reflecting the fears, hopes, and decisions of investors around the world.

EURUSD Holds Firm While Fed Split Balances Out Shutdown Impact

The EUR/USD pair has been moving in a tight range recently, reflecting the uncertainty in global markets as the United States faces a government shutdown. With crucial economic data delayed and Federal Reserve officials expressing mixed views, traders are treading carefully. Let’s dive into the current situation and understand what’s shaping the euro and dollar dynamics right now.

EURUSD is moving in an Ascending Triangle pattern

A Week of Calm but Uncertainty for EUR/USD

The EUR/USD pair stayed relatively steady on Friday, ending the week with modest gains. The ongoing US government shutdown has delayed several key economic releases, including the much-anticipated Nonfarm Payrolls report. This absence of fresh data has left traders guessing, leading to light market movement and cautious sentiment.

While the dollar has lost a bit of strength due to the uncertainty, the euro hasn’t gained much momentum either. Without strong catalysts or major economic announcements, most investors are taking a “wait and see” approach. This calm before the storm could change quickly once new data becomes available or the political situation in the US stabilizes.

Federal Reserve Officials Divided on the Path Ahead

One of the biggest sources of market confusion lately has been the mixed messages coming from the Federal Reserve. With inflation still a concern and growth showing signs of slowing, policymakers seem to be pulling in different directions.

The Hawkish View: Inflation Still a Threat

Lorie Logan from the Dallas Fed has been one of the more hawkish voices, emphasizing that inflation in non-housing services remains high and persistent. She also pointed out that tariffs have been contributing to price pressures, warning that these effects could last longer than expected. Her stance suggests that the Fed should stay alert and possibly keep rates elevated for a while to ensure inflation doesn’t rebound.

Logan’s remarks show that some officials are still worried about the “sticky” part of inflation — the kind that doesn’t respond quickly to policy changes. This cautious tone signals that the path toward rate cuts might not be as straightforward as some traders hope.

The Dovish View: Policy Should Look Forward

On the other side of the debate, Fed Governor Stephen Miran took a more dovish approach. He highlighted that access to updated data is crucial for policy decisions and stressed the importance of keeping monetary policy forward-looking. In his view, the Fed should be prepared to adjust based on where the economy is heading, not just current conditions.

Miran’s comments align with those of Chicago Fed President Austan Goolsbee, who believes the risks to inflation and employment are now more balanced. Goolsbee added that while markets have already priced in possible rate cuts, the Fed should continue to rely on data before making any move. Together, these perspectives show a softer tone compared to Logan’s, indicating internal debate within the central bank.

Economic Activity Remains Mixed Amid Data Delays

Even though the flow of new economic reports has slowed because of the government shutdown, a few key updates have still managed to grab attention. The ISM Services PMI and S&P Global PMI both painted a mixed picture of the US economy in September.

The ISM Services PMI showed that the sector nearly stalled, hovering around the neutral level that separates expansion from contraction. Businesses reported modest or weak growth expectations, and hiring remained subdued as firms delayed new additions to their workforce.

On the other hand, the S&P Global PMI revealed that the services sector was still expanding, albeit slightly slower than the previous month. This suggests that while some areas of the economy are cooling, others continue to hold up relatively well.

Together, these results point to a slow but steady economy, where growth is neither too hot nor too cold. It gives the Fed more room to maneuver but also adds to the uncertainty about whether rate cuts are truly on the horizon.

How Traders Are Reacting

With no fresh US employment data and split Fed opinions, market sentiment has been cautious. Many traders are avoiding large positions and instead focusing on short-term moves. Despite hawkish comments from some officials, the euro managed to hold firm against the dollar.

Part of the reason for this stability is that the market already expects the Fed to start easing its policy soon. According to recent market probabilities, most investors anticipate a rate cut at the upcoming Fed meeting later this month. This expectation has helped prevent the dollar from strengthening, giving the euro some breathing space.

However, traders remain sensitive to headlines. Any new developments about the US government reopening or the release of delayed data could quickly shift market dynamics. For now, the EUR/USD seems to be waiting for its next clear direction.

What Could Come Next for EUR/USD

The next few days are likely to remain quiet unless there’s an unexpected breakthrough in Washington. If the shutdown drags on, delayed data will continue to cloud the economic picture, making it harder for both the Fed and investors to make informed decisions.

Once the Nonfarm Payrolls and other reports are finally released, they could spark renewed volatility in the forex market. A strong jobs report might boost the dollar by suggesting the economy is resilient, while weaker numbers could push the Fed closer to cutting rates — helping the euro gain ground.

In Europe, the eurozone’s own economic outlook remains a factor as well. Although inflation has cooled slightly, growth across major economies like Germany and France remains uneven. This means the European Central Bank is also walking a fine line between supporting growth and keeping inflation under control.

Overall, both sides of the Atlantic are dealing with challenges, and that balance is what’s keeping EUR/USD trading in a narrow band.

Final Summary

The EUR/USD pair continues to hover around familiar levels as traders navigate a complex mix of political and economic uncertainty. The US government shutdown has temporarily frozen crucial data releases, leaving investors to rely on scattered updates and statements from Federal Reserve officials. Those statements, in turn, have revealed a deep split between hawkish and dovish views within the Fed — one side focused on persistent inflation, the other on future risks and data dependency.

Meanwhile, the latest PMI figures suggest that the US economy is growing slowly but not collapsing, offering a fragile balance between optimism and caution. With markets already expecting a rate cut soon, the dollar has struggled to gain traction, allowing the euro to maintain stability despite limited bullish momentum.

As things stand, the EUR/USD market is in a holding pattern. Everyone — from central bankers to traders — is waiting for more clarity, whether from Washington’s political developments or the return of key economic data. Until then, the pair is likely to remain steady, moving only when the next big headline hits.

GBPUSD Pushes Higher as US Data Freeze and Political Gridlock Pressure the Dollar

The global economic scene is shifting once again, and it’s becoming clear that both the United States and the United Kingdom are moving in different directions when it comes to monetary policy. The latest data from the U.S. shows a slowdown in business activity, while the U.K. economy is also losing some momentum. Despite that, the Pound Sterling (GBP) has managed to gain strength against the U.S. Dollar (USD), and much of that comes down to expectations around how each central bank might act next.

GBPUSD is moving in an Ascending Triangle pattern

U.S. Services Sector Shows Clear Signs of Slowdown

Recent data from the Institute for Supply Management (ISM) revealed that the U.S. Services PMI dropped to 50, indicating a sharp slowdown in business activity. A reading of 50 marks the line between expansion and contraction, so this fall suggests that growth in the services sector has almost ground to a halt.

The services sector represents a major portion of the American economy, which means any weakness here carries significant weight. Businesses across different industries reported moderate or weak growth, with some noting ongoing supply chain issues. What stood out most, however, was the continued contraction in employment. Many firms have delayed hiring or struggled to find qualified staff, which is a worrying sign for overall job market momentum.

Adding to the uncertainty, the U.S. government’s ongoing shutdown has delayed important economic reports, including the Nonfarm Payroll (NFP) data — a key measure of employment health. Without these figures, the Federal Reserve’s next policy decisions are harder to predict.

Federal Reserve Officials Stress Data Dependence Amid Economic Uncertainty

With the NFP report on hold, policymakers at the Federal Reserve are relying heavily on whatever data they can access to shape their decisions. Fed Governor Stephen Miran emphasized that having accurate data is essential for policy guidance, especially now. He also mentioned that inflation expectations remain well anchored and that the “neutral rate” of interest — the point where policy neither stimulates nor restrains the economy — is around 0.5%.

Meanwhile, Austan Goolsbee, President of the Chicago Fed, pointed out that employment indicators from his district suggest a 4.3% unemployment rate. He acknowledged that while markets anticipate a rate cut soon, the Fed must remain “data dependent.” In other words, any future rate moves will depend entirely on how incoming economic figures evolve.

The Fed is clearly in a tight spot. On one hand, inflation has shown signs of cooling, but on the other, growth is faltering. This puts the central bank in a balancing act — trying to support the economy without triggering a resurgence in prices. Market watchers are increasingly expecting a 25-basis-point rate cut, possibly in the next policy meeting.

UK Services PMI Cools, But BoE Holds a Cautious Stance

Across the Atlantic, the U.K. economy isn’t faring much better in the short term. The latest Services PMI from S&P Global fell to 50.8, marking the slowest growth in five months. The service industry — covering everything from finance to hospitality — has been the backbone of the British economy, so a dip here raises concerns about slowing domestic demand.

Even so, analysts expect the Bank of England (BoE) to keep interest rates unchanged for now. While economic growth is softening, inflation remains stubbornly high. The most recent data showed annual inflation around 3.8%, with expectations of a possible rise to 4% soon. That’s still well above the BoE’s target, and it gives policymakers a reason to maintain their current stance instead of easing policy too soon.

By contrast, the Fed seems closer to cutting rates as economic activity in the U.S. cools more noticeably. This growing divergence between the BoE and the Fed is one of the main reasons why the Pound Sterling has been gaining against the U.S. Dollar in recent sessions.

GBP/USD Gains as Central Bank Paths Diverge

The GBP/USD pair has been moving upward, reflecting the broader divergence in expectations between the two central banks. Investors tend to move capital toward currencies where interest rates are expected to remain higher for longer — and right now, that benefits the Pound.

The U.S. economy’s weakening momentum, coupled with expectations of a Fed rate cut, has reduced the Dollar’s appeal. Meanwhile, the BoE’s steady approach signals relative confidence that inflation, though high, can be controlled without drastic action.

Traders are closely watching upcoming economic indicators from both sides. For the U.S., inflation data, consumer confidence reports, and any updates from the Fed will be crucial. For the U.K., wage growth and inflation trends will determine how long the BoE can maintain its current policy stance.

Short-Term Outlook

In the near term, GBP/USD could continue to find support if market sentiment stays tilted toward the Pound. However, volatility is expected as global investors react to political developments, especially the ongoing U.S. government shutdown, which adds an extra layer of uncertainty.

If the Fed does cut rates while the BoE remains steady, the gap in policy direction could widen further, supporting additional gains for Sterling. But if U.K. economic data worsens or inflation spikes unexpectedly, that narrative could quickly reverse.

Global Investors Brace for Policy Shifts

Markets thrive on clarity, and right now, there isn’t much of it. Both the U.S. and U.K. are navigating complex economic conditions, and their central banks are forced to respond to conflicting signals.

For the Federal Reserve, the challenge lies in keeping inflation expectations stable while preventing the economy from slipping into a deeper slowdown. The delayed NFP report adds frustration, as employment trends are key to shaping the Fed’s outlook.

For the Bank of England, the balancing act is slightly different. Inflation remains high, but growth is slowing. That combination keeps policymakers cautious about any aggressive changes in interest rates. Investors see the BoE as more likely to hold its ground, at least until inflation clearly begins to fall back toward target levels.

In the bigger picture, both central banks are signaling that data will guide their decisions — not market pressure. This cautious, data-driven approach means that volatility in the GBP/USD pair is likely to persist as each new data point shifts market expectations.

Final Summary

The latest developments highlight a world economy in transition. The U.S. services sector’s slowdown, paired with the government shutdown and data delays, has clouded the outlook for growth. Meanwhile, the U.K. economy is slowing but still dealing with sticky inflation, prompting the Bank of England to take a wait-and-see approach.

This divergence between the Fed and the BoE has turned into a key driver for the Pound Sterling’s strength against the U.S. Dollar. Investors see the Fed as leaning toward easing policy sooner, while the BoE remains cautious and focused on inflation control.

In the weeks ahead, market direction will depend heavily on how quickly U.S. economic data rebounds — and whether U.K. inflation begins to ease. For now, Sterling has the upper hand, supported by central bank contrast and investor confidence in its resilience amid global uncertainty.

USDJPY Retreats as Market Optimism Erodes Dollar’s Safe-Haven Appeal

The US Dollar’s recent attempt to recover against the Japanese Yen has hit a wall. After briefly showing signs of strength, the greenback lost momentum, signaling that global market uncertainty and investor sentiment continue to weigh heavily on its direction. The shift reflects growing doubts about the US economy’s near-term resilience and the ongoing debate around future Federal Reserve actions.

USDJPY is moving in an uptrend channel, and the market has rebounded from the higher low area of the channel

The Dollar’s Momentum Slows Down

The week started with the US Dollar showing some life against the Yen. Optimism followed remarks from key US Federal Reserve officials, who hinted that rate cuts might be approached with caution. However, that early confidence didn’t last long. As weak labor data surfaced and concerns about a potential US government shutdown spread, the Dollar’s strength quickly faded.

This drop in momentum wasn’t just about market numbers—it was about confidence. Traders and investors are now questioning how sustainable the Dollar’s recovery really is. With inflation still sticky and economic data sending mixed signals, the greenback’s direction has become unpredictable. The slight rebound seen earlier this week now seems more like a temporary pause in a broader downtrend.

Why the Dollar Lost Its Footing

Weak Labor Data Adds Pressure

One of the biggest setbacks for the US Dollar this week came from disappointing labor market figures. The ADP employment report showed an unexpected slowdown in job growth, suggesting that the labor market—previously considered one of the economy’s strongest pillars—might be softening.

Weak job creation not only shakes confidence in the broader economy but also fuels speculation that the Federal Reserve will be under pressure to ease monetary policy sooner than expected. Investors tend to react quickly to labor data since employment levels play a major role in shaping interest rate decisions.

Government Shutdown Fears Spark Uncertainty

As if weak labor data weren’t enough, renewed worries about a possible US government shutdown added another layer of volatility. Political gridlock in Washington has historically rattled financial markets, and this time is no different. A prolonged shutdown could slow government spending, reduce productivity, and further dent investor confidence.

Markets hate uncertainty, and the combination of unstable political developments and shaky economic indicators has created the perfect storm. Many investors are now retreating to safe-haven assets, leaving the Dollar struggling to find solid ground.

Fed Officials’ Mixed Messages Keep Traders Guessing

Cautious Tone from the Federal Reserve

On Thursday, Dallas Federal Reserve President Lorie Logan shared that while inflation remains a concern, the central bank must be “very cautious” with rate cuts. Her words initially gave the US Dollar some support, as they suggested that the Fed may not rush into easing monetary policy. However, that optimism faded quickly once broader economic realities set in.

The message from the Fed remains mixed—on one hand, officials emphasize patience in cutting rates, but on the other, weak data pushes markets to believe that easing is inevitable. Traders are now pricing in the possibility of rate cuts as early as October or December, depending on how incoming data unfolds.

BoJ Governor’s Remarks Add to the Confusion

Adding to the uncertainty, comments from the Bank of Japan’s Governor, Kazuo Ueda, hinted at cautiousness regarding global economic conditions. While his remarks were not overtly hawkish or dovish, they left traders unsure about Japan’s next policy steps. This uncertainty has influenced Yen movements, but it hasn’t been enough to stop the Yen from gaining against a weakening Dollar.

Market Eyes on Upcoming US Economic Data

Services PMI Data in the Spotlight

Traders now turn their attention to the release of September’s final US Services PMI figures. These data points are critical as they provide insight into how the country’s service sector—one of the biggest components of the economy—is performing. A strong reading could offer temporary support for the Dollar, while a weaker one might reinforce fears of an economic slowdown.

Beyond the headline numbers, investors will be paying close attention to sub-indexes like new orders and employment levels. Any signs of weakness there could amplify expectations of future Fed rate cuts.

Jefferson’s Speech Could Set the Tone

Later today, markets will also be tuning in to a speech by Federal Reserve Vice Chair Philip Jefferson. His comments will be closely scrutinized for clues on the central bank’s next move. If Jefferson echoes Logan’s cautious tone, it could calm markets temporarily. But if he hints at possible rate cuts or acknowledges economic risks more openly, the Dollar might face renewed downward pressure.

Global Economic Uncertainty Clouds the Outlook

The broader global picture isn’t helping the Dollar either. Economic growth in major economies remains uneven, inflation trends are diverging, and geopolitical tensions continue to add instability. This environment has led investors to seek safer, more stable assets, and for now, the Yen appears to be benefiting from that sentiment.

Japan’s relatively stable inflation and conservative monetary stance give it an advantage in times of uncertainty. Meanwhile, the US faces not only internal challenges like political infighting but also external pressures from global trade and inflation concerns.

The Dollar’s recent movements against the Yen, therefore, reflect more than short-term market noise—they reveal deeper structural concerns about where the US economy is heading next.

What Traders Should Watch Next

Investors should keep an eye on upcoming US economic reports, especially inflation and employment data. These figures will heavily influence the Federal Reserve’s next steps. If inflation continues to moderate while job growth weakens, the Fed might feel pressured to act sooner with rate cuts. However, any sign of stubborn inflation could delay those cuts and offer the Dollar a brief reprieve.

In the near term, the Dollar’s path remains uncertain. While it might find temporary relief from positive data or supportive Fed comments, the overall sentiment leans toward caution. Until there’s more clarity on the US economy’s direction, volatility in USD/JPY is likely to continue.

Final Summary

The US Dollar’s recent attempt to recover against the Japanese Yen has been met with resistance, driven by weak labor data, political tensions, and ongoing uncertainty around Federal Reserve policy. Despite occasional bursts of optimism, traders remain cautious as mixed signals from both the Fed and the Bank of Japan create confusion in the market.

With key economic data and speeches from Fed officials on the horizon, the Dollar’s next move depends on how these developments shape expectations around interest rates. For now, the market mood remains cautious, and the Yen continues to benefit from its safe-haven appeal amid global economic turbulence.

GBPJPY Finds Stability While Weak Yen Fails to Lift the Struggling Pound

The GBP/JPY currency pair found some balance after a few rough trading sessions, managing to recover slightly from its lowest point in nearly two months. Even though the Japanese Yen lost ground following disappointing employment data from Japan, the British Pound couldn’t make the most of it due to weak business activity figures coming out of the UK. Let’s break down what’s happening between these two major currencies and what it could mean for traders watching the pair.

GBPJPY is moving in a box pattern, and the market has reached the resistance area of the pattern

Understanding What’s Driving the GBP/JPY Pair

The GBP/JPY pair is known for its volatility, often reacting strongly to shifts in economic data, market sentiment, and central bank policies. Recently, both the Pound and the Yen have been influenced by contrasting domestic developments, creating a tug-of-war effect on the pair.

Japan’s Economic Data Adds Pressure on the Yen

Japan’s latest unemployment figures came as an unpleasant surprise. The unemployment rate climbed to 2.6%, which was higher than what analysts had expected. This rise signaled that Japan’s job market might be slowing down a bit, putting pressure on the Yen. Usually, when unemployment rises, it suggests weaker domestic demand and can lower confidence in the country’s currency.

The Yen’s weakness wasn’t just about jobs, though. Investors have been watching Japan’s overall economic growth, inflation trends, and the Bank of Japan’s stance on monetary policy. The central bank has been hesitant to move away from its ultra-loose policy, even when other global central banks have been tightening. This has made the Yen less attractive for investors seeking better returns elsewhere.

The British Pound Faces Its Own Challenges

While the Yen weakened, the Pound didn’t have a great day either. Data from the UK’s Purchasing Managers Index (PMI) showed that both the services and manufacturing sectors were slowing down. The Composite PMI dropped to 50.1 — barely above the line that separates growth from contraction. This figure suggests that business activity in the UK is losing steam, which could make it harder for the economy to expand in the coming months.

For the services sector, which plays a huge role in the UK’s economy, the slowdown was especially concerning. A weaker PMI means that companies are seeing fewer new orders, slower customer demand, and possibly lower confidence about future business conditions.

These numbers raised questions about how strong the UK economy really is right now and whether the Bank of England will continue raising interest rates. Higher rates usually strengthen a currency, but if growth slows too much, the central bank might need to ease up — something that can drag the Pound lower.

Market Sentiment and the Broader Picture

Beyond just the economic data, the GBP/JPY pair is being influenced by broader global themes — including investor sentiment, interest rate differences, and risk appetite.

Investors Turn Cautious Amid Economic Uncertainty

With inflation, growth, and employment data sending mixed signals globally, traders are becoming more cautious. The GBP/JPY pair often reflects this mood because it’s considered a “risk barometer.” When investors feel confident, they tend to buy higher-yielding currencies like the Pound and sell the Yen, which is seen as a safe haven. But when uncertainty rises, the opposite often happens — the Yen strengthens as traders look for safety.

Recently, though, that pattern has been less predictable. The Yen hasn’t gained as much as it usually would during risk-off periods because of Japan’s stubbornly low interest rates. On the other hand, the Pound’s performance has been restrained by weak domestic data. The result? GBP/JPY has been caught in a range, moving sideways rather than strongly trending in one direction.

Interest Rate Differentials Still in Play

Interest rates remain one of the biggest factors shaping this pair. The Bank of England has kept rates relatively high to fight inflation, while the Bank of Japan continues to maintain its near-zero policy. This wide gap supports the Pound against the Yen because investors can earn higher returns holding Pound-based assets.

However, as the UK’s growth outlook dims, traders are starting to question how long that advantage can last. If the Bank of England hints at slowing its rate hikes, or even cutting rates later on, the Pound could lose some of its edge over the Yen.

Why Traders Are Watching This Pair Closely

GBP/JPY is one of the most watched cross-currency pairs because it often delivers sharp and fast moves. It reflects not just the health of the UK and Japanese economies, but also global risk sentiment.

What Makes GBP/JPY So Volatile?

The pair tends to move more than many others because it lacks the stabilizing influence of the US Dollar. That means shifts in either currency’s fundamentals — or global risk appetite — can cause quick reactions. For traders, this volatility can mean big opportunities but also higher risks.

When both economies show weakness, the market becomes even more unpredictable. Investors then focus more on global market cues such as stock performance, commodity prices, and central bank commentary.

What’s Next for GBP/JPY?

Going forward, traders will likely pay close attention to upcoming economic releases from both the UK and Japan. For the Pound, the focus will be on inflation data, wage growth, and any hints from the Bank of England about its next move. For the Yen, attention will center on inflation figures, wage negotiations, and whether the Bank of Japan is ready to signal a shift away from its ultra-loose stance.

If Japan’s economic data continues to disappoint, the Yen could stay under pressure. But if the UK’s economy keeps slowing down, the Pound might also struggle to gain ground — keeping GBP/JPY trapped in a balancing act.

Final Summary

The GBP/JPY pair’s recent behavior tells a clear story — both currencies are under pressure from their respective economies, and neither has a decisive upper hand. The Yen’s weakness stems from rising unemployment and a persistently dovish central bank, while the Pound is weighed down by sluggish business activity and uncertainty about the UK’s economic outlook.

At the same time, the broader market environment remains uncertain. Global investors are cautious, trying to balance between seeking returns and avoiding unnecessary risks. That’s why GBP/JPY continues to see choppy movement rather than a clear trend.

In the near term, much will depend on how economic data evolves. If Japan’s job market continues to weaken and the Bank of Japan maintains its loose policy, the Yen could stay soft. Meanwhile, if UK data keeps signaling slower growth, the Pound might also find it hard to gain consistent strength.

For traders, the key lies in staying alert to global sentiment and economic signals from both countries. The story of GBP/JPY isn’t just about two currencies — it’s about how the world’s financial mood swings between risk and caution. And right now, that balance is what keeps this pair so fascinating to watch.

EURJPY Rises as Investors Turn Away from Yen Over Japan’s Political and Economic Concerns

The currency market has been showing interesting movements lately, especially in the EUR/JPY pair. After falling to its lowest level in weeks, the Euro made a modest comeback against the Japanese Yen. But this recovery isn’t just about numbers on a chart — it’s about the political and economic stories shaping both sides of this currency equation. Let’s take a deep dive into what’s happening behind the scenes and why traders and investors are keeping such a close eye on this pair.

EURJPY is moving in an uptrend channel, and the market has reached the higher low area of the channel

Political Uncertainty in Japan and Its Impact on the Yen

When it comes to the Japanese Yen, stability has always been one of its strongest traits. But right now, politics seems to be shaking that foundation. Japan’s ruling Liberal Democratic Party (LDP) is set to hold its leadership election soon, and the outcome will essentially determine the country’s next prime minister.

This leadership race has created a cloud of uncertainty over Japan’s near-term policy direction. Investors generally dislike uncertainty, and whenever political events create doubt about future decisions, markets tend to react cautiously. That’s exactly what’s happening with the Yen.

Why Politics Matter for Currency Traders

Political transitions can have a real impact on currency markets. When traders suspect that a change in leadership might alter economic or monetary policy, they often adjust their positions. In Japan’s case, this election could influence how the government approaches spending, economic reform, and cooperation with the Bank of Japan (BoJ).

The Yen, already struggling against most major currencies, weakened further as investors preferred to move funds into safer or more stable assets until the political picture becomes clearer.

Economic Weakness Adds More Pressure on the Yen

Adding to Japan’s challenges is a slight cooling in its economic indicators. The unemployment rate recently climbed higher than expected, suggesting that the labor market might be slowing down. A weaker job market typically affects consumer spending and business confidence, which in turn can drag on economic growth.

This change in unemployment may seem small on paper, but in a country like Japan — where even minor shifts are closely watched — it can influence how investors view the overall strength of the economy. The uptick in joblessness raised questions about whether Japan can sustain the moderate recovery it has been trying to build.

The Role of the Bank of Japan

Amid all this, the Bank of Japan continues to walk a very fine line. Governor Kazuo Ueda recently made some cautious comments about the bank’s stance on interest rates. He mentioned that the BoJ is prepared to raise rates if inflation and growth conditions justify it, but he also pointed to global uncertainties that could delay such decisions.

These uncertainties include slower global trade, shifting wage patterns, and economic softness in major partners like the United States and China. The BoJ’s message was clear — Japan’s economy isn’t weak enough to demand immediate stimulus, but it isn’t strong enough to fully remove support either. This delicate balance leaves the Yen vulnerable to swings driven by investor sentiment.

The Euro’s Modest Rebound: Supported but Struggling

While the Yen faces pressure, the Euro isn’t exactly having an easy ride either. The Eurozone has been dealing with its own set of economic challenges, which have limited how far the common currency can climb.

Recent data from Europe showed only mild improvement in business activity. The latest composite and services indices stayed just above the neutral 50 mark, indicating modest growth but no strong momentum. This tells us that businesses in the Eurozone are growing, but not by much.

Weak Inflation and Production Concerns

Another piece of data that weighed on the Euro was the decline in producer prices. Falling producer prices often signal that businesses are facing weaker demand or are unable to pass higher costs on to consumers. This situation puts pressure on profit margins and can hint at broader economic weakness ahead.

For currency traders, this means less confidence in the Euro’s growth prospects. When the economic data remains underwhelming, investors are hesitant to buy more Euros even when other currencies — like the Yen — are showing signs of weakness.

Balancing Acts Across the Globe

Europe’s economic recovery is also being challenged by global headwinds such as higher borrowing costs and sluggish export demand. Central banks in the region have been cautious, trying to control inflation without stifling growth. This has resulted in a slower pace of policy tightening compared to earlier years, keeping the Euro’s gains fairly limited.

How Global Factors Are Shaping the EUR/JPY Pair

The current rebound in EUR/JPY is less about one currency’s strength and more about the other’s weakness. Investors are essentially weighing which side looks more stable at the moment. With Japan’s political uncertainty and economic slowdown, the Yen has lost some of its traditional safe-haven appeal.

At the same time, while the Eurozone is facing its own set of issues, it still appears relatively steadier than Japan from a market perspective. This perception has helped the Euro make a modest comeback, even if the gains aren’t dramatic.

Investor Sentiment and Market Behavior

When both currencies are under pressure, market sentiment becomes the deciding factor. Traders tend to move toward whichever economy seems to offer more predictability in the short term. In this case, the Eurozone — despite its challenges — looks slightly more predictable than Japan right now.

However, this balance could shift quickly depending on political outcomes in Japan or any major shifts in European data. If Japan’s new leadership brings clarity and confidence, or if the BoJ signals a stronger stance on inflation, the Yen could regain ground. Conversely, if Eurozone numbers continue to weaken, the Euro might lose its current edge.

What to Watch Moving Forward

For anyone tracking this currency pair, the next few weeks could be especially interesting. Political developments in Japan will be a major driver, as investors watch how the LDP leadership election unfolds. The chosen leader’s approach to economic reform and cooperation with the central bank will set the tone for how the Yen performs in the near term.

Meanwhile, traders will also be paying attention to new economic data from Europe. Any signs of a slowdown or stronger recovery will likely influence how the Euro behaves. Inflation trends, job figures, and business sentiment surveys will all play a role in determining market direction.

If the Eurozone manages to hold steady while Japan continues to face uncertainty, the EUR/JPY pair may continue to find support. But if Japan stabilizes politically and economically, the Yen could quickly regain strength, leading to another shift in this dynamic relationship.

Final Summary

The story behind EUR/JPY right now is about two economies facing different kinds of uncertainty. Japan is grappling with political transitions and a cooling labor market, both of which are putting pressure on its currency. On the other hand, the Eurozone is managing to hold its ground, but not without its own struggles — particularly sluggish business growth and weak inflation data.

In simple terms, the Euro’s rebound isn’t necessarily a sign of strong performance; it’s more a reflection of the Yen’s vulnerability. As global investors seek stability, their choices between these two currencies depend on which side seems less risky in the short term.

Over the coming weeks, political outcomes in Japan and fresh economic reports from Europe will likely determine the next direction for this pair. For now, the Euro enjoys a temporary lift, while the Yen waits for clarity — a reminder that in the world of currencies, uncertainty often plays the biggest role of all.

USDCAD Extends Gains While Investors Watch for US Data Clues

The USD/CAD pair has been showing remarkable strength in recent days, maintaining its position near a four-month high. This movement highlights growing pressure on the Canadian Dollar, which has been struggling amid expectations of another interest rate cut by the Bank of Canada (BoC). On the other hand, the US Dollar is facing its own challenges, influenced by domestic issues like government uncertainty and a cooling job market. Together, these dynamics are shaping the current tone of the USD/CAD currency pair.

USDCAD is moving in an uptrend channel, and the market has reached the higher low area of the channel

The Canadian Dollar Faces Growing Weakness

The Canadian Dollar, often referred to as the Loonie, has been under steady pressure for weeks. Traders and investors seem increasingly convinced that the Bank of Canada will announce another rate cut later this month. This belief stems from signs of slowing economic activity and a weaker job market in Canada.

Why the Market Expects a Rate Cut

The BoC already took a significant step in September by reducing its key borrowing rate by 25 basis points. This move was part of a broader monetary easing approach aimed at supporting an economy that has shown signs of fatigue. Unemployment numbers have edged higher, and wage growth has not been strong enough to create inflationary pressure. That gives policymakers more room to cut rates without worrying about runaway inflation.

Essentially, when a central bank lowers interest rates, it makes borrowing cheaper, encouraging businesses and consumers to spend more. However, this also tends to weaken the local currency, as investors move their capital toward regions offering higher returns. That’s precisely what’s happening with the Canadian Dollar right now.

Impact on the USD/CAD Pair

As a result of the BoC’s dovish outlook, the USD/CAD pair has gained upward momentum, showing clear strength even as the US Dollar remains somewhat restrained. The imbalance between a cautious BoC and a Federal Reserve still debating its next move has tilted investor sentiment in favor of the USD against the CAD.

US Dollar Under Pressure Despite Market Advantage

While the Canadian Dollar’s weakness is driving USD/CAD higher, the US Dollar itself isn’t particularly strong. The Greenback is facing a range of domestic challenges that have prevented it from fully capitalizing on the situation.

Government Concerns and Job Market Worries

A major factor limiting the US Dollar’s rise is the ongoing uncertainty surrounding the US government’s fiscal stability. With discussions of potential funding shortfalls and temporary shutdowns, investor confidence in the USD has been somewhat shaky. Such political risks often discourage traders from holding large positions in the US Dollar.

At the same time, the US labor market has been cooling. Job creation has slowed, and wage growth has started to flatten out. This shift suggests that the post-pandemic hiring boom is losing steam. For policymakers at the Federal Reserve, weaker job numbers raise the question of whether it’s time to consider interest rate cuts to support growth.

The Federal Reserve’s Dilemma

According to the CME FedWatch tool, investors are increasingly betting on rate cuts by the Federal Reserve before the end of the year. Market expectations for a 50-basis-point reduction have risen sharply over the past week. This shift in sentiment has contributed to a softening of the US Dollar, as lower rates would reduce returns for those holding USD-denominated assets.

Essentially, both the US and Canada are moving toward looser monetary policies — but since the BoC appears to be more aggressive in that direction, the USD/CAD pair continues to trend upward.

Market Focus Shifts to Economic Data

As traders prepare for upcoming events, economic data releases from the US remain in sharp focus. One of the key reports investors are watching is the US ISM Services PMI, a measure of business activity in the service sector. This data gives important clues about how the economy is performing outside of manufacturing.

Why It Matters

A strong reading in the ISM Services PMI can signal that the economy remains resilient, reducing the chances of a near-term Fed rate cut. Conversely, a weaker reading could reinforce the belief that the central bank will need to act soon to prevent an economic slowdown. Traders use this kind of data to adjust their expectations and trading positions — which in turn affects how the USD moves against other major currencies like the CAD.

In essence, the direction of the USD/CAD pair in the coming weeks will likely depend not only on central bank policy decisions but also on how upcoming US economic reports shape market expectations.

Canada’s Economic Struggles Add to Loonie Pressure

Beyond monetary policy, there are broader economic concerns in Canada that are weighing on the Loonie. The Canadian job market has softened, and wage growth has remained modest. Additionally, exports — a major contributor to Canada’s economy — have faced headwinds from global demand fluctuations.

Investor Sentiment

Foreign investors, who play a major role in determining the strength of a currency, have been cautious about increasing their exposure to Canadian assets. With uncertainty surrounding future rate cuts and slower economic data, many are choosing to wait for clearer signs of recovery. This cautious tone is another factor preventing the CAD from rebounding, even when the US Dollar weakens temporarily.

What Traders Are Watching Next

The upcoming Bank of Canada policy meeting is now the key event everyone is waiting for. Traders expect another interest rate cut, but the tone of the central bank’s statement will be equally important. If policymakers hint that further cuts are possible, it could push the CAD even lower. On the other hand, any sign that the BoC might pause its easing cycle could help the Loonie stabilize.

For the US Dollar, the focus remains on the Federal Reserve’s response to recent economic trends. Should inflation continue to cool and unemployment rise further, the Fed may feel increasing pressure to act, which could weaken the USD. However, if upcoming economic data proves stronger than expected, it might keep the Dollar from falling too far.

Final Summary

The USD/CAD pair is currently reflecting two different economic realities. On one side, Canada is facing a weakening economy and the likelihood of further rate cuts from the Bank of Canada. On the other side, the US is dealing with its own challenges — including political uncertainty and a slowing job market — but is still perceived as relatively stable.

This combination has created a scenario where the US Dollar maintains the upper hand against the Canadian Dollar, even without showing strong independent momentum. Moving forward, traders and investors will be closely monitoring central bank statements, economic data releases, and broader market sentiment to gauge the next big move.

In short, while the Loonie struggles under the weight of economic softness and policy uncertainty, the USD/CAD pair remains positioned for potential gains, with its direction likely determined by how both nations’ central banks balance the fight between growth and inflation in the weeks ahead.

USDCHF Loses Steam Near 0.8000 but Manages to Stay Above Key Support

The US Dollar continues to face headwinds, failing once again to find firm ground against the Swiss Franc. While global markets maintain a modest appetite for risk, the Dollar remains under pressure. Meanwhile, Switzerland’s soft inflation data is limiting any meaningful recovery for the Swiss Franc. Together, these factors have left both currencies trading cautiously, with investors searching for direction amid economic uncertainty.

USDCHF is moving in a downtrend channel, and the market has fallen from the lower high area of the channel

A Tiring Battle for the US Dollar

For most of the week, the US Dollar has been moving within a narrow range, reflecting uncertainty in the global market. Despite brief moments of strength, the Dollar struggled to maintain momentum, particularly after hitting a key psychological barrier. This suggests that traders remain cautious, avoiding large positions until they see clearer signs from the US economy and the Federal Reserve.

On Thursday, the Dollar showed some resilience after comments from Lorie Logan, President of the Dallas Federal Reserve. She cautioned against cutting interest rates too quickly, suggesting that the central bank should maintain a careful approach. Her statement dampened hopes for a rate cut in the near future, offering temporary support for the currency. However, this was short-lived, as weak economic data soon shifted the mood once again.

Weak Job Growth Keeps Pressure on the Dollar

The biggest challenge for the US Dollar lately has been disappointing employment data. Investors have grown increasingly worried that the labor market is losing steam, raising questions about whether the Federal Reserve can continue to keep rates high.

The latest employment figures showed that job creation has slowed down considerably. Data from ADP Employment Change revealed a decline in private sector hiring, falling well below expectations. August’s figures were also revised downward, further emphasizing the weakness in the job market. This slowdown has left many wondering if the US economy is beginning to feel the strain of tight monetary policy.

Adding to the concern, reports on Challenger Job Cuts showed a mixed picture. While the number of layoffs slightly declined, hiring activity hit its lowest level since 2009 — a time when the global economy was recovering from the financial crisis. Such numbers paint a worrying picture, suggesting that businesses are reluctant to expand their workforce amid ongoing economic uncertainty.

This fragile job market places the Federal Reserve in a difficult position. On one hand, inflation remains above target, requiring continued caution. On the other, a weakening labor market could force policymakers to step in with support sooner than planned. Until there’s clarity on which path the Fed will take, the Dollar is likely to stay stuck in a state of indecision.

Swiss Economy Stays Cool with Low Inflation

While the Dollar faces its own struggles, the Swiss Franc is also dealing with its share of challenges. Switzerland’s recent inflation report confirmed that consumer prices remain subdued. Data showed that inflation rose only slightly on a yearly basis, with a monthly reading indicating another contraction. This persistent weakness has reinforced the idea that the Swiss economy is cooling.

Low inflation may sound like good news for consumers, but it presents a problem for policymakers. The Swiss National Bank (SNB) has been cautious about its next moves, balancing between keeping prices stable and avoiding a deeper slowdown. With inflation failing to pick up, some analysts believe the SNB may eventually need to ease monetary policy again — possibly through rate cuts. However, such a move could weaken the Franc further, limiting its potential to appreciate against the Dollar.

The combination of weak inflation and subdued global demand has also affected Switzerland’s export-driven sectors. Companies that rely heavily on foreign sales are finding it harder to maintain growth, especially as global trade conditions remain uncertain. This keeps the Franc from making any strong gains, even when the Dollar is under pressure.

Investor Sentiment: A Tug of War Between Risk and Safety

The broader market environment is also playing a role in the ongoing currency tug-of-war. Right now, investors appear cautiously optimistic, with a moderate appetite for risk. This means they are more willing to invest in riskier assets such as stocks and emerging-market currencies, while stepping back from safe-haven assets like the US Dollar and Swiss Franc.

However, the situation remains fragile. Any sudden shift in global sentiment — such as renewed geopolitical tensions or a surprise economic report — could quickly send investors back into safer assets. This constant balancing act has kept both the Dollar and Franc trapped in tight trading ranges, with neither able to dominate for long.

Global Factors Shaping the Next Move

Beyond domestic data, both the Dollar and Franc are heavily influenced by global developments. Rising oil prices, ongoing trade disputes, and slowing growth in major economies are just a few of the factors creating volatility in the foreign exchange market.

For the US, uncertainty about the Federal Reserve’s next policy steps continues to drive speculation. Investors are paying close attention to every piece of economic data, from inflation figures to job reports, in hopes of predicting the Fed’s next move. Meanwhile, Switzerland’s economy remains closely tied to European performance, especially as its largest trading partners face their own economic challenges.

The result is a complex landscape where both currencies are responding more to global mood swings than domestic fundamentals. Until the economic picture becomes clearer, traders are likely to see more of the same — cautious movement and range-bound trading.

What Could Happen Next?

Looking ahead, much depends on how the US and Swiss economies evolve in the coming months. If US employment data continues to weaken, it may push the Fed toward a more dovish stance, potentially lowering interest rates sooner than expected. This could lead to further Dollar weakness in the medium term.

On the other hand, if inflation in Switzerland remains soft, the Swiss National Bank may also have to reconsider its policy approach. While cutting rates could help boost growth, it may also put downward pressure on the Franc. This means the USD/CHF pair might continue to fluctuate without a clear long-term direction, as both sides face conflicting forces.

Traders and investors should also keep an eye on broader market sentiment. Any signs of increased risk aversion could strengthen both the Dollar and the Franc temporarily, given their reputation as safe-haven currencies. However, in periods of optimism, both may find it harder to attract demand.

Final Summary

In simple terms, the US Dollar and Swiss Franc are both navigating uncertain waters. The Dollar is weighed down by a slowing labor market and unclear signals from the Federal Reserve, while the Franc faces the challenge of persistently weak inflation. Both currencies are being tugged back and forth by global sentiment, leaving them trapped in narrow ranges for now.

The coming weeks will be crucial. Fresh economic data from the US and Switzerland could set the tone for where these currencies head next. For now, traders can expect continued caution, as markets wait for clearer direction from policymakers and the global economy.

USD Index Falters as Rate Cut Speculation and Shutdown Fears Hit the Dollar

The US Dollar Index (DXY) seems to be losing its shine lately. After gaining some strength earlier in the week, the greenback is now struggling to hold its ground. A mix of weaker labor data, ongoing political tensions, and uncertainty about government policies has caused investors to rethink their positions. Let’s take a closer look at what’s really going on behind this dip in the dollar’s strength and what it could mean in the coming weeks.

USD Index market price is moving in a downtrend channel, and the market has fallen from the lower high area of the channel

Weaker Labor Market Adds Pressure on the Dollar

When we talk about the US economy, one of the biggest indicators investors watch closely is the labor market. Recently, new data suggested that job growth is slowing down. Fewer jobs were added compared to earlier expectations, and that has raised concerns that the economy might be losing some momentum.

A weaker labor market often pushes the Federal Reserve to consider cutting interest rates. Lower rates make borrowing cheaper, which can help boost spending and investment — but they also tend to make the dollar less attractive to investors. That’s exactly what’s happening now.

Market analysts are already pricing in a strong possibility of upcoming rate cuts by the Federal Reserve. The latest figures show almost full market confidence that a rate cut could happen as early as October, with another one potentially following in December. The expectation of lower interest rates is a major reason behind the current downward pressure on the dollar.

Political Stalemate: The Government Shutdown Drama

As if the weaker labor data weren’t enough, the political scene in Washington has added another layer of uncertainty. The US government is facing a partial shutdown, which has already started affecting several sectors. This isn’t the first time this has happened, but the timing couldn’t be worse.

The ongoing shutdown has led to delays in the release of important economic data, including reports that help investors understand how the economy is performing. The delay in data such as the Nonfarm Payrolls (NFP) report means the markets are left guessing about the true health of the labor market.

What makes things more complicated is that the standoff in Congress doesn’t appear close to ending. Senate Democrats and Republicans are locked in a battle over short-term funding bills, and with neither side willing to budge, the situation may drag into next week or longer. The uncertainty surrounding the government’s ability to function smoothly creates a sense of instability — and that’s never good news for a currency.

When investors sense political instability, they often move their money into safer assets like gold, the Japanese yen, or government bonds. That shift in capital reduces demand for the US dollar, leading to further weakness.

Economic Policies and Rebate Proposals: Another Twist

While the markets are already juggling concerns about rate cuts and political gridlock, a new policy idea from the White House has added yet another talking point. President Donald Trump recently mentioned that his administration is considering sending rebate checks to taxpayers — potentially ranging between $1,000 and $2,000.

The proposed rebates would be funded through revenue collected from tariffs. According to the administration, these tariffs could generate hundreds of billions of dollars, which could be redirected to support consumers. Trump even claimed that tariff revenues could reach as high as $1 trillion per year, while Treasury Secretary Scott Bessent gave a more conservative estimate of over $500 billion.

On the surface, the idea of rebate checks sounds like a quick way to boost household income and spending. If people have more cash, they tend to spend more, which could help stimulate the economy. However, there’s also skepticism about whether this approach can deliver long-term benefits. Some economists argue that such rebates provide only temporary relief and don’t address the underlying issues slowing the economy — such as lower productivity, weak job growth, or trade-related uncertainties.

Additionally, using tariff revenue to fund rebates is a double-edged sword. While tariffs bring in money, they can also raise costs for businesses and consumers, ultimately offsetting the benefits of the rebates. This mix of optimism and uncertainty has made investors cautious, leading to volatile movements in the currency market.

Market Sentiment: Investors Watching Every Move

At this stage, investor sentiment is fragile. The combination of weak labor data, political tension, and experimental economic policies has created a cloud of uncertainty over the market.

Many traders are choosing to wait for more clarity before making big moves. They’re keeping an eye on upcoming reports like the ISM Services PMI and the final S&P Global Services PMI, which provide insight into how well the service sector — the backbone of the US economy — is holding up.

If these reports show further signs of weakness, it could strengthen the case for more rate cuts by the Federal Reserve. On the other hand, if the data shows resilience, it might give the dollar a chance to bounce back temporarily. Still, the overall outlook remains cautious, as confidence in sustained economic growth seems to be fading.

What It Means for the Average Investor

For everyday investors, all these developments might sound like distant political and financial talk, but they can have real-world impacts. A weaker dollar can make imported goods more expensive, which could eventually raise prices for consumers. However, it can also benefit exporters, as US goods become cheaper for foreign buyers, potentially boosting manufacturing and trade.

For people with investments tied to the US market, this environment could bring more volatility. Stock prices might swing more sharply depending on how investors react to the changing economic landscape. Keeping an eye on central bank announcements, political developments, and key data releases can help investors make more informed decisions during such uncertain times.

Final Summary

The US Dollar Index is currently under pressure, and it’s not hard to see why. Weak labor market numbers have increased expectations of upcoming rate cuts, reducing the appeal of the greenback. At the same time, the ongoing government shutdown has created additional uncertainty, shaking investor confidence.

Adding to the mix, the Trump administration’s proposal to issue rebate checks funded by tariff revenues has sparked debates about its effectiveness. While it could offer short-term relief, the long-term impact on the economy remains unclear.

In the weeks ahead, much will depend on how quickly the government resolves its shutdown, how the Federal Reserve responds to economic data, and whether consumer confidence remains steady. Until then, the dollar is likely to remain under pressure as investors continue to navigate an unpredictable economic and political environment.

BTCUSD Gains Strength as U.S. Market Activity Lifts Bitcoin’s Uptrend

Bitcoin is once again grabbing everyone’s attention. After a brief period of consolidation, the world’s most popular cryptocurrency has bounced back with remarkable strength. Its upward momentum has been largely driven by strong buying activity in the United States, growing institutional demand, and renewed investor confidence. Let’s dive into what’s behind this powerful comeback and why many believe Bitcoin’s next major breakout could be closer than expected.

BTCUSD is moving in an uptrend channel, and the market has reached a higher low area of the channel

A Wave of Optimism Sweeps the Market

Bitcoin’s impressive recovery has sparked a new wave of enthusiasm across the crypto space. Over the past few weeks, interest from both individual and institutional investors has surged. This fresh burst of activity signals that confidence in digital assets is returning, especially after months of uncertain market movements.

What’s fueling this renewed optimism? For starters, U.S. investors are stepping up in a big way. Trading activity on major exchanges shows that American buyers are willing to pay slightly more for Bitcoin compared to other markets. This suggests growing local demand — a trend often linked to major bull runs in the past. When U.S. traders get active, global markets tend to follow their lead.

Another major factor driving enthusiasm is the steady inflow into Bitcoin exchange-traded funds (ETFs). These investment products have been attracting significant capital from institutions seeking exposure to Bitcoin without directly holding it. Throughout the week, ETFs recorded billions in new inflows, showing that professional investors are once again betting big on crypto. This consistent investment interest signals strong long-term belief in Bitcoin’s potential.

Institutional Investors Step Back Into the Game

For months, institutional participation in Bitcoin had been relatively subdued. But now, the tide is clearly turning. The renewed interest in Bitcoin ETFs reflects a notable shift in investor sentiment — from hesitation to confidence. Institutions are not just watching from the sidelines anymore; they’re actively participating in the rally.

These large players bring deep liquidity and credibility to the crypto market. Their involvement often acts as a stabilizing force, making the market more attractive to everyday investors. The consistent inflow into ETFs also shows that Bitcoin is gaining recognition as a legitimate asset class rather than just a speculative investment.

The shift in attitude can also be linked to macroeconomic developments. The delay of key U.S. government reports, like the jobs data, has pushed investors toward alternative assets such as Bitcoin. When uncertainty looms over traditional markets, digital assets often become an appealing hedge — and this time is no different.

Investor Confidence Reaches New Heights

Another clear sign of rising confidence is the surge in trading activity. Open interest — a measure of the total number of active futures and derivatives contracts — recently hit a record level. This increase indicates that traders are not only buying Bitcoin but also placing strategic bets on its future price direction.

This surge in open interest shows that more traders are taking calculated risks, reflecting a growing appetite for volatility. After a recent reset during options expiry, the market is now seeing more deliberate positioning. Instead of random speculative plays, many investors are making informed decisions based on broader market trends and economic indicators.

It’s important to note that such market behavior often precedes large price movements. High open interest typically means strong participation from both bullish and bearish traders, setting the stage for potential breakouts. Whether the next big move will push Bitcoin beyond its previous highs remains to be seen, but the enthusiasm is clearly building.

Global Demand and U.S. Influence

While Bitcoin’s appeal has always been global, the latest rally shows just how influential U.S. investors can be. The price differences across exchanges highlight how American demand is outpacing other regions. When U.S. buyers pay a premium, it usually reflects strong belief in Bitcoin’s long-term value and potential.

This trend has been reinforced by growing institutional adoption. Financial firms, hedge funds, and asset managers are increasingly integrating Bitcoin into their portfolios. The introduction of regulated investment products like ETFs has made it easier for these organizations to gain exposure without dealing with the complexities of digital wallets or private keys.

As more financial institutions enter the space, mainstream adoption continues to grow. Bitcoin is no longer seen as a fringe asset reserved for tech enthusiasts — it’s becoming a serious contender in the global investment landscape.

Comparing Bitcoin’s Growth with Other Assets

Despite the impressive momentum, Bitcoin’s performance this year still trails behind traditional precious metals like gold and silver. While Bitcoin has recorded solid growth, gold and silver have outperformed it in year-to-date returns. This comparison, however, doesn’t tell the full story.

BTCUSD is moving in a box pattern, and the market has reached the resistance area of the pattern

Gold and silver are centuries-old stores of value, while Bitcoin is a digital newcomer that thrives on innovation, decentralization, and scarcity. The fact that Bitcoin can compete with these long-established assets is itself a powerful statement about its growing importance. As more investors understand the advantages of blockchain-based assets — including transparency, portability, and independence from traditional banking systems — Bitcoin’s appeal is likely to expand even further.

Why the Market Is Watching Bitcoin Closely

There’s a sense of anticipation building across the crypto community. The combination of strong institutional inflows, renewed retail interest, and record-level trading activity has created the perfect environment for a potential breakout. Many traders believe that if momentum continues, Bitcoin could soon test new highs.

Another interesting aspect is how Bitcoin’s reputation has evolved. It’s no longer viewed solely as a speculative asset but as a reliable hedge against inflation and economic uncertainty. This shift in perception is key to its long-term growth story. More people now see Bitcoin as “digital gold” — a secure, decentralized alternative to traditional financial systems.

At the same time, the market’s maturity has improved significantly. Regulatory clarity in several regions and the rise of compliant investment products have made it easier for everyday investors to participate safely. This broader accessibility ensures that Bitcoin’s next growth phase could attract an even wider audience than before.

The Road Ahead for Bitcoin

Looking ahead, Bitcoin’s path appears promising but not without challenges. The crypto market has always been known for its volatility, and short-term corrections are part of the journey. However, the underlying fundamentals — strong demand, institutional adoption, and increasing market maturity — paint a positive long-term picture.

As more traditional investors explore Bitcoin and more companies integrate blockchain technology, the potential for expansion remains massive. Whether it’s through ETFs, corporate investments, or payment integrations, Bitcoin’s role in the financial ecosystem continues to grow.

Final Summary

Bitcoin’s recent surge is a reminder that the cryptocurrency market is alive and thriving. Strong U.S. demand, institutional inflows, and rising investor confidence have all played key roles in driving its comeback. While it may still trail behind gold and silver in short-term gains, Bitcoin’s potential for long-term growth remains unmatched.

The current momentum shows that Bitcoin isn’t just a passing trend — it’s a movement reshaping the future of finance. As global interest rises and adoption deepens, Bitcoin’s next milestone might not be far away. Whether you’re a seasoned trader or just getting started, one thing is clear: Bitcoin’s story is far from over, and its best chapters may still be ahead.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!