Weekly Forecast Video on Forex, BTCUSD, XAUUSD

Stay ahead in the markets with our detailed analysis of gold and forex trade setups for this upcoming week, Oct 27 to Oct 31.

XAUUSD lifts as US CPI slowdown heightens expectations of upcoming rate cuts

The gold market ended the week on a positive note, bouncing back from earlier losses and closing slightly higher after fresh U.S. inflation data supported expectations of an upcoming interest rate cut by the Federal Reserve. The report on September’s Consumer Price Index (CPI) suggested that inflation remains stable enough to keep the central bank on course for a more dovish policy move later this month.

A Calm Inflation Report Boosts Gold’s Appeal

Gold has always been a safe haven for investors, especially when inflation data sparks uncertainty about the future of monetary policy. The latest CPI report showed that prices continued to rise but at a manageable pace — just enough to assure traders that the Fed will not hesitate to cut rates in its next meeting.

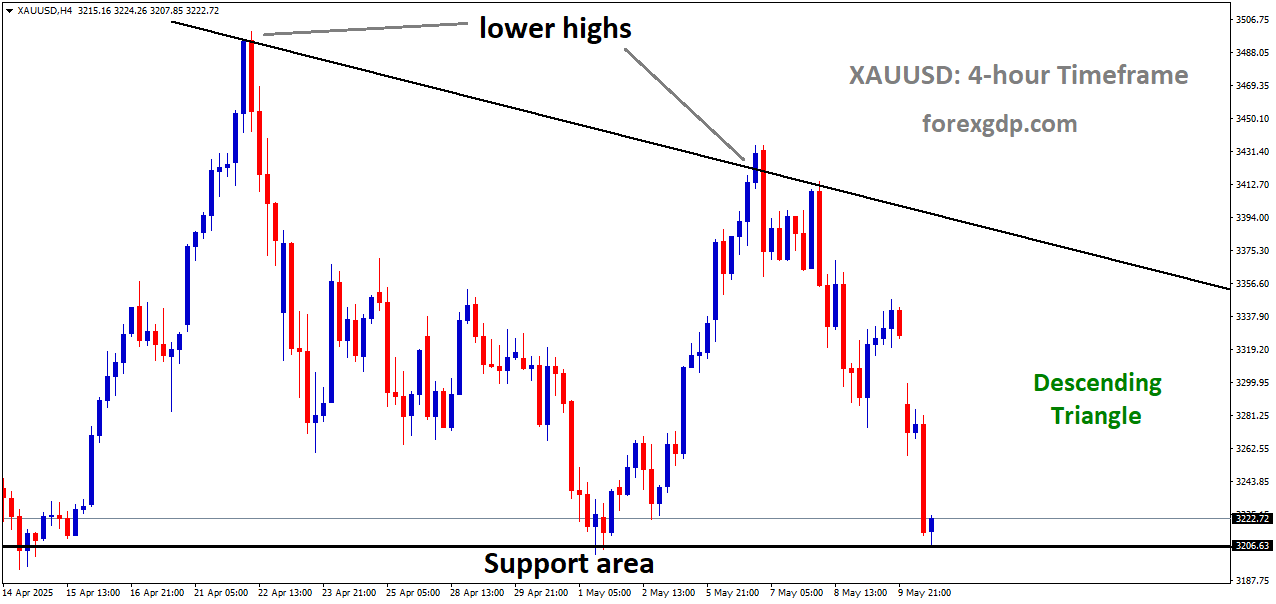

XAUUSD is moving in a symmetrical Triangle pattern

This softer inflation reading helped gold recover from its morning dip, as many investors shifted their attention toward assets that perform well in lower interest rate environments. Lower rates generally weaken the U.S. dollar and reduce bond yields, making gold — which doesn’t yield interest — more attractive in comparison.

In simpler terms, when borrowing costs drop, the opportunity cost of holding gold decreases. That’s why investors are often quick to buy when signs of rate cuts appear on the horizon.

Market Sentiment: A Mix of Optimism and Uncertainty

While the inflation report gave gold a short-term lift, broader market sentiment remained divided. Traders are almost certain that the Federal Reserve will reduce rates in its late-October meeting, with most projections showing a very high probability of that move. However, not all economic data painted a rosy picture.

Business Activity Improves Slightly

According to recent figures from S&P Global, U.S. business activity in October picked up modestly. This suggests that while growth remains steady, it’s not strong enough to change the Fed’s easing stance. Many companies reported an increase in new orders and a slight improvement in manufacturing and services output, signaling that the economy is holding up despite high borrowing costs in previous months.

Consumer Sentiment Weakens

On the other hand, the University of Michigan’s consumer sentiment index showed a noticeable drop compared to preliminary readings earlier in the month. Americans are becoming more cautious about spending as they face continued cost pressures. Inflation expectations for the next year slipped slightly, while long-term expectations ticked up — showing that consumers aren’t fully confident that price growth is under control yet.

This combination of cautious optimism from businesses and growing anxiety among consumers reflects an economy in transition. For gold investors, it reinforces the idea that uncertainty remains high — and that’s usually good news for the yellow metal.

Global Events Fuel Interest in Safe-Haven Assets

Beyond U.S. economic data, global politics also played a role in driving gold’s performance. Reports emerged that U.S. President Donald Trump and Chinese President Xi Jinping are set to meet soon to discuss trade and economic cooperation, a move closely watched by markets as the deadline for new tariffs approaches.

At the same time, geopolitical tensions flared as the U.S. government announced fresh sanctions against Russian oil companies, intensifying concerns about energy supply disruptions and potential economic consequences. Historically, events like these push investors toward assets perceived as stable — and gold is often at the top of that list.

Geopolitical Tensions Strengthen Gold Demand

Whenever there’s uncertainty about global trade, military conflict, or diplomatic relations, gold tends to benefit. Investors see it as a hedge against both market volatility and political risk. In this case, the combination of trade uncertainty and new sanctions created an environment where gold’s safe-haven status once again shone through.

The Bigger Picture: Why Gold Remains Strong in 2025

Gold’s upward movement this year hasn’t been just a short-term reaction to individual data points. Several deeper trends are supporting its strength:

1. Central Bank Buying

Many central banks around the world continue to add gold to their reserves. This steady demand helps support prices even when investor sentiment fluctuates. Central banks see gold as a way to diversify reserves and protect against currency instability — especially in uncertain economic times.

2. Inflation and Rate Cut Expectations

Although inflation has moderated, it’s still above long-term targets in many major economies. That keeps gold relevant as a hedge against price pressures. Additionally, markets are betting that interest rates will trend lower over the next year, which typically provides sustained support for gold prices.

3. Investor Demand

Institutional and retail investors alike are returning to gold as part of a broader risk management strategy. With stock markets showing mixed signals and cryptocurrencies remaining volatile, gold provides a sense of stability. It’s not about chasing quick profits — it’s about balance and safety.

Analysts Eye Longer-Term Growth

Financial analysts are increasingly bullish about gold’s long-term potential. Major financial institutions have projected that if central bank demand remains consistent and investors continue to seek protection against market volatility, gold prices could climb significantly in the coming years.

Forecasts suggest that ongoing demand from both official and private sectors may drive average gold prices higher by 2026. While projections vary, the general consensus is that gold’s upward momentum isn’t over yet.

This outlook aligns with historical patterns: gold often performs best during times of economic transition, when interest rates are shifting, and global politics add layers of uncertainty.

Why Gold Still Matters for Everyday Investors

You don’t have to be a professional trader to understand gold’s importance. Whether you’re building a portfolio or simply looking for a stable store of value, gold continues to hold its place as a timeless asset.

Diversification and Protection

Including gold in your investment mix helps reduce overall risk. It often moves differently from stocks or currencies, offering protection when other assets decline.

XAUUSD is moving in an uptrend channel, and the market has fallen from the higher high area of the channel

Confidence During Volatile Times

In today’s unpredictable global environment, having part of your savings in gold can provide emotional and financial confidence. It’s one of the few assets that has held value for centuries, through wars, recessions, and economic booms alike.

Final Summary

Gold’s latest rise reflects a broader narrative of economic caution and global tension. While inflation remains stable and business activity shows signs of life, weakening consumer sentiment and geopolitical uncertainty are keeping demand for gold strong.

With rate cuts on the horizon and global risks persisting, gold continues to shine as a preferred safe-haven asset. For investors, it’s not just about chasing short-term gains — it’s about maintaining balance and security in a changing world.

As we move forward, all eyes will remain on how the Federal Reserve’s decisions and global political developments shape the next chapter of gold’s journey. For now, the message is clear: gold remains a symbol of stability in uncertain times — and that’s something investors aren’t ready to give up anytime soon.

EURUSD Steady as Soft U.S. Data Strengthens Market’s Rate Cut Expectations

The EUR/USD currency pair has managed to remain fairly steady this week, even though it’s on track to close slightly lower. While the movement may seem minor, the bigger story lies behind the scenes — a mix of U.S. inflation data, expectations of a Federal Reserve rate cut, stronger-than-expected Eurozone business activity, and concerns over France’s financial outlook. Let’s dive into what’s really shaping this currency pair and what these shifts might mean going forward.

U.S. Inflation Miss Sparks Talk of a Rate Cut

When the latest U.S. Consumer Price Index (CPI) report came out, it fell just short of expectations. This might not sound dramatic, but it had a ripple effect across global markets. Inflation remains below the Federal Reserve’s 2% target, and that’s fueling speculation that another rate cut could be around the corner.

At this point, traders are largely betting that the Fed will reduce rates by the next meeting. The logic is simple: weaker inflation means less pressure to keep rates high. While inflation isn’t dropping sharply, it’s stable enough for policymakers to consider easing conditions to support growth.

Meanwhile, business activity in the U.S. continues to surprise. According to recent data, both the manufacturing and services sectors expanded at a faster pace in October — a sign that the economy still has some strength left. However, even with this resilience, consumer confidence isn’t keeping up. The University of Michigan’s report showed Americans are becoming slightly more cautious, suggesting that households may still be feeling the pinch of higher prices, even if inflation isn’t soaring.

The Eurozone Finds Its Footing — But Faces Political Headwinds

Across the Atlantic, things are looking a bit more optimistic — at least on the surface. The latest Purchasing Managers’ Index (PMI) reports for the Eurozone came in above expectations. This means business activity is picking up again after months of sluggish performance. Both manufacturing and services are showing signs of life, hinting that demand is beginning to rebound.

EURUSD is rebounding from the retest area of the broken downtrend channel

But it’s not all sunshine for Europe. Moody’s recently issued a warning about France’s financial and political stability, cutting its outlook from “stable” to “negative.” The reason? Rising debt levels and ongoing political uncertainty could make it harder for France to tackle its fiscal challenges. That kind of news doesn’t just affect France — it can also weigh on broader confidence in the Eurozone economy and, by extension, the euro itself.

Still, the euro has shown resilience. Despite this cautionary note from Moody’s, the currency has managed to hold firm. The market seems to believe that as long as economic indicators like the PMIs stay positive, the euro can weather temporary setbacks.

The Dollar’s Balancing Act: Strength vs. Expectations

The U.S. dollar has been walking a fine line lately. On one hand, economic data remains relatively strong, giving it a reason to stay supported. On the other hand, expectations of rate cuts are limiting how high it can climb. Investors are torn between solid business figures and the anticipation of looser monetary policy.

The Dollar Index, which tracks the greenback against a basket of other major currencies, edged only slightly higher this week. This reflects the broader tug-of-war — strong data from manufacturing and services helps the dollar, but weaker inflation data and rate cut expectations keep it from breaking out significantly.

Meanwhile, a recent development added another twist: reports that the U.S. government may revisit trade issues with China. Such headlines can create uncertainty, and that’s never good for market stability. The dollar tends to benefit from safe-haven demand in times of global tension, but it can also face selling pressure if investors think trade disputes could hurt U.S. growth.

Europe’s Recovery vs. America’s Slowdown — A Subtle Shift in Balance

For much of the past year, the U.S. economy has outperformed the Eurozone, helping keep the dollar strong. But the latest numbers suggest that balance might be starting to shift. The Eurozone’s recovery signs — combined with softer U.S. inflation — are slowly closing the gap. This doesn’t necessarily mean the euro will soar, but it could mark the beginning of a more level playing field between the two economies.

Interestingly, this trend might also reduce volatility in the EUR/USD pair. When both economies are performing in a similar range, sharp movements tend to fade. Instead, traders focus more on long-term trends like central bank policy, fiscal outlooks, and consumer confidence. That could explain why, despite all the headlines, the EUR/USD has stayed relatively calm this week.

What Traders Are Watching Next

All eyes are now on the Federal Reserve’s upcoming decision. Markets are already pricing in a rate cut, but investors will be looking closely at any hints about future moves. If the Fed signals more easing ahead, it could weaken the dollar further and give the euro a lift.

On the European side, the focus will be on how governments handle fiscal challenges — particularly in France and Italy — and whether economic momentum continues through the next quarter. Stronger consumer spending and sustained growth in services could help keep the euro on steady ground.

Traders are also paying attention to the broader political landscape. Ongoing tensions in global trade, energy prices, and domestic politics all play a role in shaping currency flows. Stability tends to support the euro, while uncertainty often benefits the dollar — so whichever region manages to maintain confidence will likely see its currency hold the upper hand.

Final Summary

In short, the EUR/USD market is currently being pulled in opposite directions by contrasting forces. The U.S. economy remains strong but faces softer inflation and growing expectations of rate cuts. The Eurozone, meanwhile, is showing early signs of recovery, even as concerns rise over political and fiscal stability in countries like France.

For now, the pair’s stability suggests that investors are waiting for a clearer signal — whether from the Fed’s next move or Europe’s economic momentum. Until then, the euro and dollar may continue this careful dance, each supported by strength in some areas and challenged by uncertainty in others.

In the weeks ahead, the story will likely revolve around one key question: which economy blinks first? If the U.S. moves toward looser policy while Europe continues improving, the euro could regain more ground. But if Europe’s recovery stalls or fresh risks emerge, the dollar may once again take the lead. Either way, the balance between these two global giants remains as fascinating — and delicate — as ever.

GBPUSD steadies after wild swings as UK growth and US inflation shape market mood

The GBP/USD pair has been moving in a relatively calm manner after a series of big economic updates from both the United Kingdom and the United States. While the market has seen its fair share of ups and downs lately, the pair’s current stability reflects a broader balance between the UK’s economic resilience and the US’s shifting monetary outlook. Let’s break down what’s really happening and what’s keeping this pair steady.

UK Economy Shows Strength Despite Global Headwinds

The UK has delivered some surprisingly positive economic data, suggesting that its recovery remains on track. This optimism primarily stems from two important reports — retail sales and the Purchasing Managers’ Index (PMI).

Retail Sales Exceed Expectations

UK retail sales saw a noticeable rebound in September, growing far beyond analysts’ forecasts. This growth was mainly fueled by strong consumer spending and a surge in online purchases, especially in luxury segments like jewelry. This bounce-back signals that UK consumers, despite facing inflationary pressures earlier in the year, are still confident enough to spend.

GBPUSD is moving in a downtrend channel, and the market has rebounded from the lower low area of the channel

Such momentum could mean that the overall economic output for the third quarter will turn out stronger than the Bank of England (BoE) initially expected. In simpler terms, people are buying more, businesses are performing better, and the economy is moving forward faster than previously thought.

PMI Data Points to an Expanding Economy

Adding to the good news, the S&P Global flash PMI data revealed that the UK’s business activity continues to grow. The Composite PMI rose to 51.1, a level that suggests expansion rather than contraction. Both the services and manufacturing sectors showed improvement, with the latter reaching its best level in a year.

The manufacturing sector’s recovery is especially significant because it has been one of the weakest parts of the economy in recent years. Now, with factories seeing more demand and production levels rising, the economic outlook looks much healthier.

Why the Pound Isn’t Gaining Much Ground Yet

Even with all this positive news, the Pound Sterling (GBP) has not made major moves upward. You might wonder — if the economy is doing well, why isn’t the pound rallying strongly? The answer lies in monetary policy expectations.

Market Still Expects BoE Rate Cuts

Investors are already looking ahead and predicting that the Bank of England might lower interest rates in the coming months. Despite the current economic strength, markets are pricing in a total of around 50 basis points in rate cuts over the next year.

This means traders believe the BoE will eventually have to ease monetary conditions to support growth and prevent the economy from slowing too much later on. The likelihood of any immediate rate cut, however, remains small — analysts suggest that a policy shift at the next meeting in November is unlikely.

The cautious tone from policymakers also adds to the pound’s limited momentum. In essence, while the UK economy looks good for now, the anticipation of future rate cuts keeps investors hesitant about pushing the pound higher.

US Economic Data and the Federal Reserve’s Next Move

Across the Atlantic, the US economy is also facing major turning points. The Federal Reserve (Fed) is now walking a fine line between keeping inflation under control and preventing a slowdown in growth.

Softer Inflation Supports Rate Cut Expectations

Recent data showed that US inflation has continued to ease. The Consumer Price Index (CPI) numbers came in lower than expected, indicating that price pressures are cooling down. Both the overall and core inflation readings suggest that the Fed’s earlier rate hikes are working effectively.

This development has increased expectations that the Fed could begin cutting rates sooner rather than later. Many traders are now betting on a possible move toward monetary easing in the coming months, as lower inflation gives the Fed more flexibility.

US Business Activity Still Resilient

Interestingly, even as inflation slows, US business activity remains strong. The S&P Global PMI readings indicated solid expansion across both manufacturing and services sectors. This resilience shows that businesses are still operating at a healthy pace, even with tighter financial conditions.

However, this same strength could make the Fed’s job more complicated. A strong economy usually argues against rate cuts, but cooling inflation supports them. The balance between these forces is why the US dollar has remained steady — neither too weak nor too strong.

The Ongoing Tug of War Between the Pound and the Dollar

The GBP/USD pair is caught in a unique position where both currencies are supported by opposing but equally strong narratives. On one hand, the UK’s economy is outperforming expectations, while on the other, the US’s softer inflation data keeps rate cut hopes alive.

The result? A kind of stalemate — neither currency can fully dominate the other right now. Traders are waiting for more clarity from central banks, especially the BoE and Fed, before making any big moves.

Short-Term Outlook

In the near term, volatility could remain moderate unless a major policy announcement changes the game. For instance, if the Bank of England hints at delaying rate cuts or the Federal Reserve signals a deeper shift toward easing, the market might react more decisively.

For now, however, the pair is likely to continue moving in a range as investors digest the mixed economic signals from both sides.

Final Summary

To sum it up, the GBP/USD pair’s stability reflects the balance between two powerful economic stories. The UK’s economy is showing real signs of recovery — with stronger retail activity and improving business confidence — while the US is navigating through softer inflation and steady business momentum.

Even though the pound has not surged, its underlying fundamentals look healthy. Meanwhile, the dollar’s direction depends largely on how the Federal Reserve handles the evolving inflation picture.

In essence, both economies are doing well, but investors are treading carefully. With interest rate decisions from the BoE and Fed on the horizon, the next few months could finally reveal which side takes the lead in this ongoing currency tug of war.

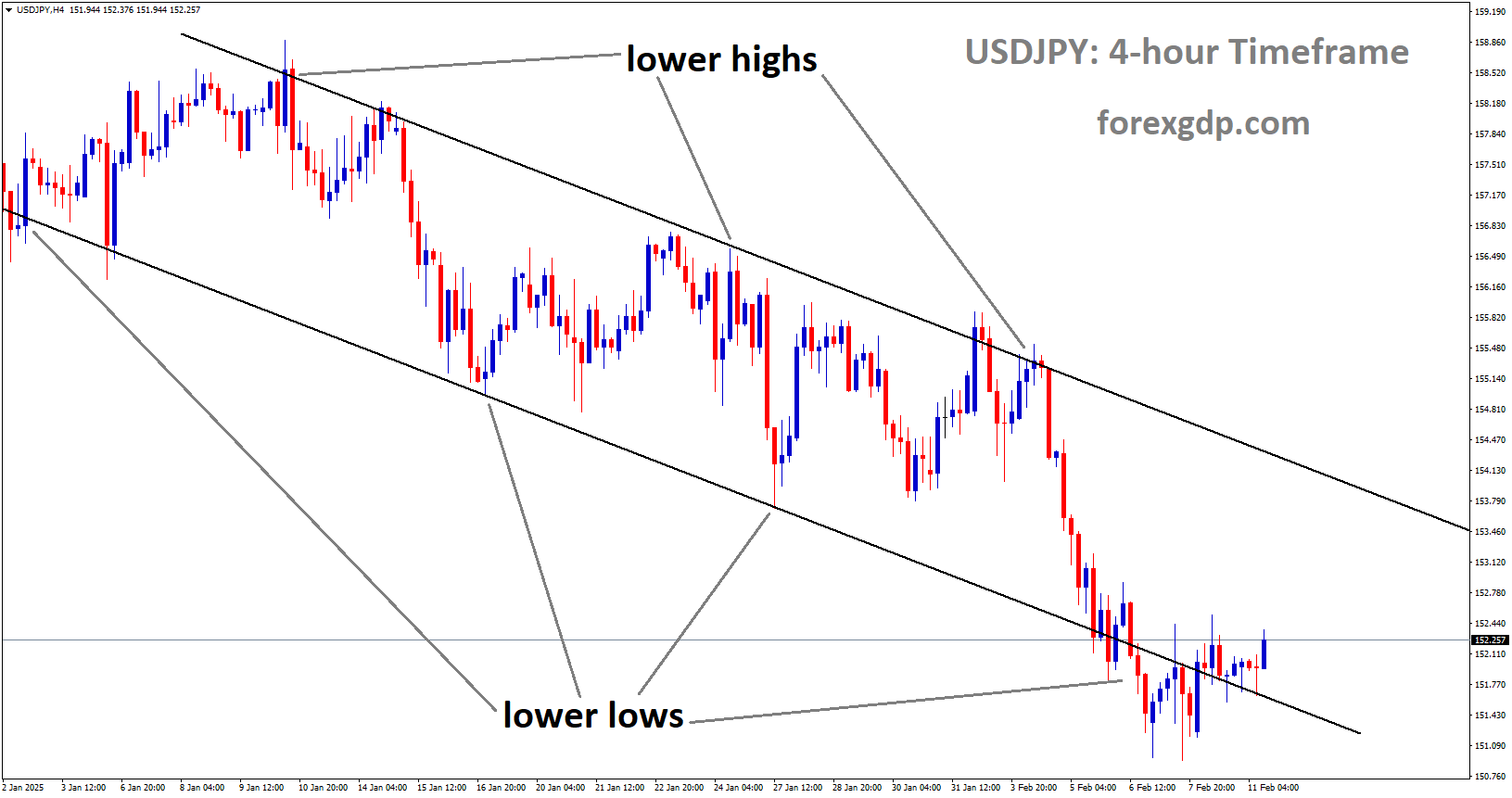

USDJPY Pushes Upward as Strong American Growth Momentum Balances Slower Inflation

The U.S. Dollar continues its remarkable rise against the Japanese Yen, marking six consecutive days of gains. This rally is powered by strong U.S. business activity data, growing optimism around the American economy, and a cautiously optimistic stance from the Federal Reserve. The story unfolding in the USD/JPY pair reflects a broader economic picture — one where U.S. growth momentum is challenging Japan’s continued monetary easing stance.

The Dollar’s Winning Momentum: What’s Driving It?

Over the past week, the U.S. Dollar has been on a roll, strengthened by encouraging economic data and renewed investor confidence. The latest data from the S&P Global Composite PMI showed a solid uptick, signaling strong expansion in both the manufacturing and services sectors. The index climbed to 54.8, the highest level in three months, pointing toward a resilient private-sector performance.

USDJPY is moving in an uptrend channel, and the market has reached the higher low area of the channel

This rise suggests that businesses in the U.S. are seeing higher demand, particularly within the services sector, which remains the backbone of the economy. The Services PMI surged to 55.2, while Manufacturing PMI ticked up slightly to 52.2, indicating that growth is not limited to a single sector. Robust domestic consumption, rising new orders, and steady hiring trends have all played a role in supporting these gains.

What stands out here is the balance between strong business activity and easing inflation pressures. While production and demand remain healthy, prices are not climbing at an alarming pace — a combination that gives the Federal Reserve room to maneuver on its policy path.

Why Softer Inflation Still Supports the Dollar

The U.S. Consumer Price Index (CPI) data released earlier revealed that inflation rose less than expected. Prices increased at a slower monthly pace, reinforcing the idea that inflation is gradually cooling after a period of stubborn highs. For traders and investors, this means the Federal Reserve is likely to continue with its measured and gradual rate-cut strategy rather than aggressively tightening or easing.

This measured approach is seen as supportive for the Dollar. Here’s why — when inflation cools but the economy continues to grow, investors tend to favor the Dollar as it signals economic stability without the risk of runaway inflation or deep cuts that could weaken the currency.

Markets are already pricing in another potential rate cut during the late October Federal Reserve meeting, followed by the possibility of one more before the end of the year. This expectation has created a sense of balance: investors see monetary easing ahead but not at a pace that undermines the Dollar’s strength.

At the same time, business surveys and consumer spending data show the U.S. economy remains resilient. Even though the University of Michigan Consumer Sentiment Index dipped slightly, the overall outlook for spending remains firm. Consumers are cautious, but not retreating — a sign that inflation fatigue might be easing among households.

Japan’s Yen Struggles Despite Rising Domestic Inflation

On the other side of the Pacific, the Japanese Yen remains under heavy pressure. Despite a small pickup in Japan’s inflation numbers, the currency continues to lose ground against the Dollar.

Japan’s consumer prices rose in September, both in headline and core terms, showing a moderate increase from the previous month. While that would typically support the Yen, the Bank of Japan’s (BoJ) ultra-loose monetary policy continues to limit its upside potential. The BoJ’s reluctance to move away from negative interest rates, combined with the U.S.’s relatively higher yields, has widened the interest rate gap between the two economies — a key factor driving Yen weakness.

Adding to this, there is growing speculation that Prime Minister Sanae Takaichi may soon introduce a large-scale fiscal stimulus to support households and small businesses. While such a package could help Japan’s domestic economy, it may also lead to higher government borrowing. Finance Minister Katayama hinted that additional government bonds might be necessary to finance these measures — a statement that reinforced concerns about Japan’s rising debt burden.

In short, Japan faces a delicate balancing act: stimulate the economy without triggering more currency depreciation or long-term financial strain.

A Broader Perspective: Global Sentiment and Market Behavior

The USD/JPY trend also reflects a wider global narrative. Investors are currently navigating between optimism about U.S. growth and concerns about slowing activity in Europe and Asia. With the U.S. economy continuing to outperform most major peers, the Dollar’s position as a safe and stable investment has been reinforced.

Another element supporting the Dollar is capital flow dynamics. Investors seeking yield are drawn toward U.S. assets, which offer higher returns compared to those in Japan. The result is a steady demand for the Dollar and continued selling pressure on the Yen.

Meanwhile, Japanese policymakers are walking a fine line. While they have occasionally hinted at possible market intervention to curb excessive Yen weakness, the overall market consensus remains that fundamental economic factors — rather than short-term interventions — are steering the USD/JPY direction.

USDJPY is moving in a descending triangle pattern, and the market has reached the lower high area of the pattern

The broader sentiment can be summed up as follows: the U.S. economy’s relative strength continues to drive currency markets, and unless Japan makes a significant policy shift, the Yen is likely to remain on the defensive.

What to Expect Moving Forward

Looking ahead, the next few weeks could be pivotal for the USD/JPY trend. The Federal Reserve’s meeting at the end of October will be closely watched, as investors look for clues about how confident policymakers are in the U.S. economy’s ability to handle moderate rate cuts.

If the Fed maintains its steady tone — emphasizing patience and confidence in growth — the Dollar may continue to attract global capital. Conversely, any sign of deeper rate cuts or cautious economic commentary could slow the Dollar’s upward run.

In Japan, attention will shift to how the government’s stimulus discussions evolve and whether the BoJ provides any policy adjustments. Although inflation is slowly rising, it remains far below the sustained levels that would justify tightening monetary policy. That means the Yen’s recovery, if any, is likely to be gradual rather than sudden.

For now, the overall sentiment remains clear: as long as the U.S. economy outpaces Japan’s and interest rate differentials stay wide, USD/JPY will likely remain elevated.

Final Summary

The steady rise of the U.S. Dollar against the Japanese Yen tells a story of two very different economies. The United States is showing resilient growth and softening inflation, a mix that supports cautious optimism and attracts global investment. In contrast, Japan’s continued ultra-loose monetary stance and looming fiscal stimulus have kept the Yen on the weaker side, even amid modest inflation gains.

As investors await the next major policy updates from both Washington and Tokyo, the balance between economic strength, inflation trends, and central bank actions will continue to define the USD/JPY path. For now, the Dollar remains firmly in the driver’s seat — backed by confidence in the U.S. economy and steady expectations for the months ahead.

USDCHF Keeps Its Ground as Investors Focus on Upcoming U.S. CPI Update

The USD/CHF pair is showing little movement as investors around the world keep a close eye on the upcoming U.S. inflation report. This data, which reveals how quickly prices are rising in the American economy, could have a major influence on how both the U.S. Dollar and the Swiss Franc behave in the coming days.

Let’s dive deep into what’s happening in the market, why this data is so important, and how global developments might shape the next move for the USD/CHF pair.

What’s Going On with USD/CHF Right Now

The USD/CHF pair has been trading within a narrow range, reflecting a sense of caution among traders. This kind of movement usually happens when investors are waiting for a big piece of economic news before making any major decisions.

Right now, the spotlight is on the United States as markets await the latest Consumer Price Index (CPI) report. This report measures the average change in prices paid by consumers for goods and services — basically, it’s one of the best indicators of inflation.

USDCHF is moving in a box pattern, and the market has rebounded from the support area of the pattern

Analysts expect both headline and core inflation (which excludes food and energy) to rise by about 3.1% annually, showing that price pressures are still present in the U.S. economy. While this is not as high as the peaks seen in previous years, it still sits above the Federal Reserve’s 2% target — meaning inflation remains an ongoing challenge.

On a monthly basis, economists predict a small but steady rise in prices, suggesting that the economy isn’t cooling off too quickly. However, many traders believe this data won’t drastically change the Federal Reserve’s approach for now.

The Fed’s Dilemma: Inflation vs. Employment

Even though inflation remains above the desired level, recent comments from Federal Reserve officials show a shift in focus. Policymakers have started to express more concern about the weakening job market rather than inflation itself.

The Fed’s dual mandate is to maintain price stability and achieve maximum employment. When inflation is high, the Fed raises interest rates to cool spending and borrowing. But if jobs start disappearing or hiring slows down, aggressive rate hikes can do more harm than good.

That’s the balancing act the Fed is currently trying to manage — keeping inflation under control without triggering an economic slowdown.

Because of this, even a slightly higher CPI number might not cause an immediate policy change. Instead, the Fed may continue to monitor how the labor market performs in the coming months before deciding on its next move.

Global Spotlight: U.S.–China Trade Talks

Aside from inflation data, another key event drawing attention is the trade discussion between U.S. Treasury Secretary Scott Bessent and China’s Vice Premier He Lifeng, taking place in Malaysia.

These talks are important because the U.S. and China are two of the world’s largest economies, and any progress or tension between them can ripple across global markets. The main topics expected to be discussed include tariffs, trade barriers, and fair competition practices.

If the talks result in positive developments, investor confidence could rise, potentially boosting global risk appetite. On the other hand, if discussions stall or tensions increase, safe-haven currencies like the Swiss Franc could gain ground as traders look for stability.

This means that the USD/CHF pair could see subtle shifts depending on the outcome of these negotiations, even if the inflation data doesn’t cause major moves.

What’s Happening in Switzerland

On the Swiss side, the Swiss National Bank (SNB) has been fairly calm and steady in its approach. The minutes from its recent policy meeting suggest that officials see no need to make big adjustments to their monetary stance right now.

According to SNB policymakers, inflation in Switzerland is unlikely to stay “persistently negative,” meaning they don’t expect a long period of deflation (falling prices). This is a good sign for the economy, as steady prices often reflect healthy demand and stability.

The SNB also believes that the impact of U.S. tariffs and global trade shifts on the Swiss economy will be limited. Switzerland’s economy is strong, built on stable exports, a robust financial sector, and a currency that tends to attract investors during uncertain times.

That said, the Swiss Franc remains one of the most reliable safe-haven currencies in the world. When global uncertainty rises — whether from geopolitical issues or economic fears — traders often move their money into the Franc for protection.

Market Sentiment: A Period of Waiting and Watching

At the moment, both the U.S. Dollar and the Swiss Franc are being driven more by global sentiment than by technical market patterns. Traders are cautious, waiting for the CPI report and other key global updates before taking big positions.

When uncertainty dominates, the market often enters a “wait-and-see” mode, where prices move within a tight range. This is exactly what’s happening with USD/CHF right now.

If inflation turns out to be higher than expected, it might strengthen the U.S. Dollar slightly as investors anticipate the Fed could stay cautious about cutting rates. However, if inflation is weaker or the job market continues to show signs of strain, the Dollar could come under pressure, giving the Swiss Franc a small advantage.

Why This Matters for Investors and Traders

For traders, periods like these can be tricky. When major data is due, volatility can increase sharply right after the release. That’s why many experienced investors prefer to stay cautious until the data is out and the market reaction becomes clear.

In a broader sense, the upcoming inflation numbers will also help shape expectations for interest rates, economic growth, and currency performance over the next few months.

The Swiss economy’s stability and the SNB’s cautious stance continue to make the Franc an appealing choice during uncertain times. Meanwhile, the U.S. economy’s resilience will depend on how inflation and employment evolve together — a delicate balance that will determine the Dollar’s strength moving forward.

Final Summary

The USD/CHF pair is currently in a holding pattern as traders wait for the U.S. inflation data and monitor ongoing global developments. While expectations point toward a moderate rise in inflation, the overall market reaction may remain muted as the Federal Reserve focuses more on employment concerns than on inflation alone.

At the same time, Switzerland’s steady monetary policy and calm economic outlook provide a solid foundation for the Swiss Franc. Ongoing trade talks between the U.S. and China could also influence investor sentiment, but for now, markets seem more interested in clarity than risk-taking.

In short, the next few days could set the tone for how both currencies perform in the weeks ahead. Whether you’re a trader or a long-term investor, it’s a time to stay informed, watch the data carefully, and wait for the right moment before making your move.

USDCAD Gains Support as US Inflation Eases and Markets Eye Fed Rate Cuts

The latest inflation numbers from the United States have once again drawn attention from global investors. With inflation showing signs of cooling off, market expectations for a Federal Reserve rate cut have grown stronger. The US Dollar has reacted modestly, slipping lower, while the Canadian Dollar remains comparatively quiet. The USD/CAD pair, however, continues to trade strongly above the 1.4000 level, suggesting the broader sentiment still favors the greenback despite a softer inflation reading.

Understanding the Recent Inflation Data

The US Bureau of Labor Statistics recently released the Consumer Price Index (CPI) report for September, which showed inflation rising at a slightly slower pace than expected. Consumer prices went up by 0.3% on a monthly basis, compared to the market forecast of 0.4%. On a yearly basis, inflation rose to 3%, just under the expected 3.1%.

USDCAD is moving in an uptrend channel, and the market has fallen from the higher high area of the channel

This small difference might not seem like much, but it tells an important story — inflation is cooling gradually, not collapsing. For policymakers and investors, this is a positive sign. It means the economy is easing off inflationary pressures without an abrupt slowdown in demand or growth.

Core Inflation: A Key Indicator for the Fed

When economists and the Federal Reserve talk about inflation, they often focus on core inflation — a measure that excludes volatile items like food and energy. Core inflation in September eased to 0.2% on a monthly basis and held steady at 3% annually. Both numbers came in below market projections, which supports the idea that inflationary pressures are becoming more contained.

This easing in core inflation gives the Federal Reserve more room to adjust its monetary policy. With the economy showing resilience but price growth slowing, the Fed might feel more comfortable considering rate cuts to support long-term stability and growth.

Market Reaction: Dollar Weakens, But USD/CAD Holds Firm

Following the inflation report, the US Dollar Index (DXY) dipped modestly by around 0.12%, reflecting a mild weakening as traders adjusted their expectations for interest rates. A softer inflation number typically increases the likelihood of rate cuts since it suggests that price pressures are under control.

Despite the slight dip in the US Dollar, the USD/CAD pair remained strong, holding above the important 1.4000 level. The resilience in this pair highlights the interplay between the two currencies. While the US Dollar faced minor selling pressure, the Canadian Dollar did not show enough strength to take full advantage.

Why the Canadian Dollar Stayed Weak

The Canadian Dollar, often influenced by global commodity trends and oil prices, has remained subdued. Even though oil is one of Canada’s main exports, fluctuations in global energy prices have added uncertainty to its performance. This has limited the strength of the CAD, allowing the USD/CAD pair to stay elevated.

In essence, the combination of a slightly weaker US Dollar and a still-soft Canadian Dollar has created a balance that keeps USD/CAD relatively firm.

Looking Ahead: What Traders Are Watching Next

The next big focus for the markets is the Federal Reserve’s upcoming meetings and statements. The current data supports expectations that the Fed will begin easing its policy soon, possibly at the December meeting. Some investors believe the central bank might even signal a more aggressive path of rate reductions if inflation continues to trend lower in the coming months.

For now, markets have already priced in a rate cut in the near term. This anticipation has shaped currency movements and bond yields, with traders positioning themselves for a softer US Dollar over time.

The Role of Oil Prices in USD/CAD’s Future

Oil remains a major driver for the Canadian Dollar. If global oil demand increases or supply issues push prices higher, it could strengthen the CAD and potentially pull USD/CAD lower. However, if oil prices stay uncertain or decline, the Canadian Dollar could remain under pressure, keeping USD/CAD supported above key levels.

Fed Guidance: The Ultimate Market Mover

Even though inflation has softened, the Fed will likely be cautious. Policymakers are expected to analyze future inflation readings, employment trends, and overall economic performance before making any moves. Investors will closely monitor speeches and reports from Federal Reserve officials for hints about the direction of monetary policy.

This communication will play a big role in shaping market sentiment. A more dovish tone — meaning the Fed is inclined toward cutting rates — would likely weaken the US Dollar further. On the other hand, if the Fed signals that it’s still concerned about inflation, the Dollar could regain strength.

Investor Sentiment: Balancing Optimism and Caution

Markets are entering a phase of optimism mixed with caution. The moderation in inflation is good news, but it’s not yet enough to guarantee a full shift toward looser monetary policy. Traders and investors are aware that the Federal Reserve will act carefully to avoid reigniting inflation while still supporting economic growth.

Meanwhile, for the USD/CAD pair, the short-term direction will depend on two main factors — Fed policy signals and energy market developments. Any major shift in either of these could quickly change the current market balance.

Final Summary

The latest US inflation report has confirmed what many investors were hoping for: price pressures are gradually easing without harming economic momentum. The numbers came in slightly below expectations, reinforcing confidence that the Federal Reserve may begin cutting interest rates soon.

The US Dollar reacted mildly to the data, slipping just a bit, while the Canadian Dollar stayed relatively weak. This kept the USD/CAD pair strong above 1.4000, reflecting a steady demand for the US Dollar in the current environment.

As markets look ahead, all eyes are on the Federal Reserve and its next steps. The direction of oil prices will also play a major role in determining how the USD/CAD pair behaves. For now, investors can expect a period of careful observation, as the market adjusts to a world where inflation is slowing and monetary policy could soon turn more supportive.

In the coming weeks, both currencies are likely to react to every new piece of data and every comment from central bank officials — making this an exciting and closely watched period for traders and investors alike.