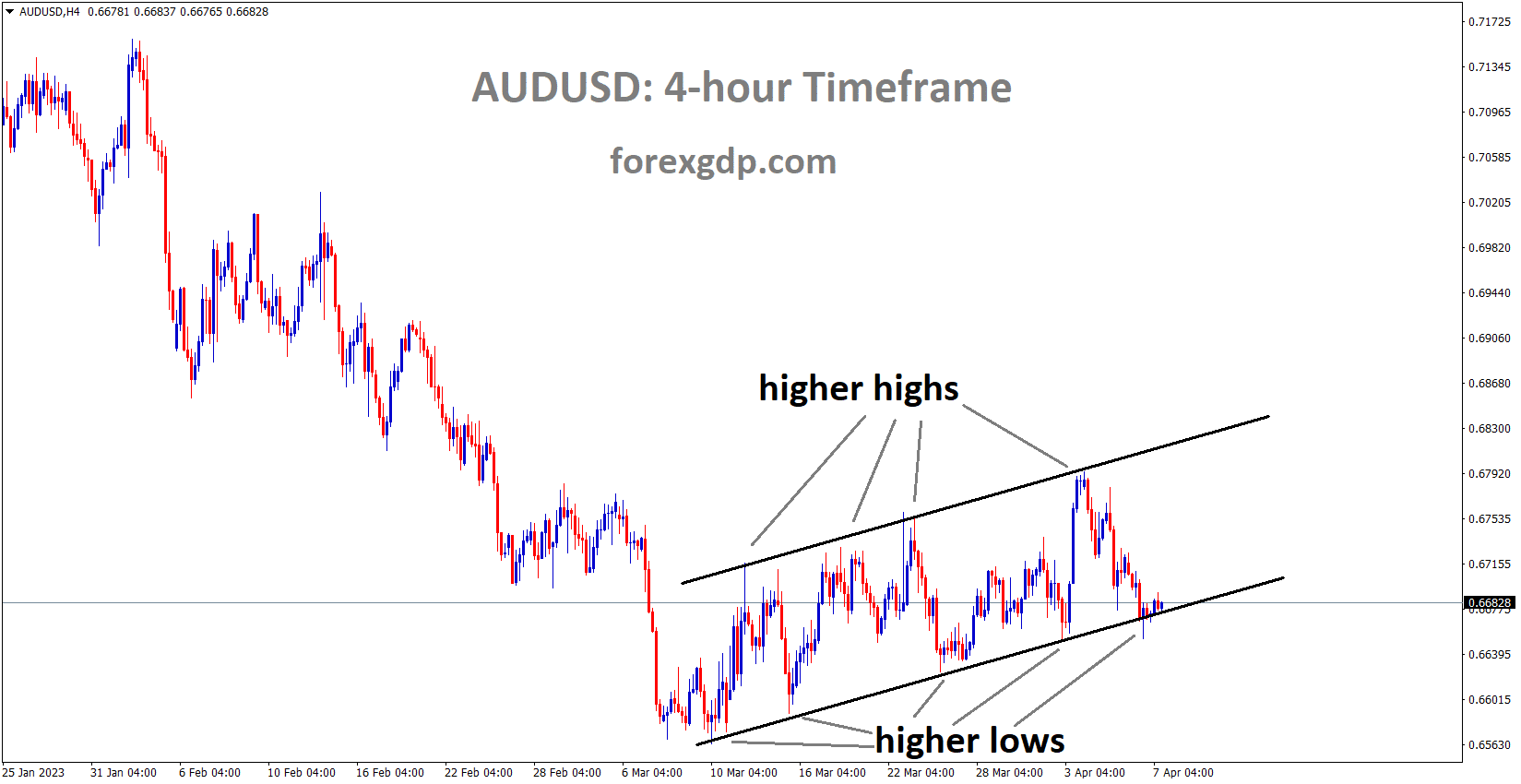

AUDUSD Analysis

AUDUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

The Chinese Commerce Ministry stated that Australia must only treat all businesses equally in response to Australia’s ban on the TIKTOK app on government-owned devices. This demonstrates a resounding confidence in Australian businesses and the public. To establish a successful business and economic partnership with China, Australia must bear this in mind.

China’s Commerce Ministry urged Australia to treat all businesses equitably when asked about Australia’s ban on Tiktok on government computers. Encourage Australia to foster an environment that is conducive to the growth of China-Australian trade and economic cooperation. The restriction hurts the interests of Australian enterprises and the general public while also undermining confidence in Australia’s business environment among the international community.

GOLD Analysis

XAUUSD Gold price is moving in the descending channel and the market has rebounded from the lower low area of the channel.

The BRICS meeting’s act of “de-Dollarization” makes the US Dollar weaker than Gold. Russia and China talk about using the Chinese Yuan instead of the US Dollar for trade. Here, the US dollar loses value for businesses that trade.

US Congressman said that the Gold Restoration Act should be brought back to keep the value of the US dollar stable in relation to gold.

After its steepest drop in two weeks on Thursday, gold is holding steady at $2,007 in the early hours of Good Friday. The XAUUSD is restrained by both the lack of liquidity caused by the holidays and the cautious mindset preceding the premier United States employment statistics for March. It’s worth mentioning that recent worries of a recession have weighed on the Gold price, even as the US Dollar battles to recover, mostly due to the dismal data coming out of the US. As consecutive bad U.S. statistics and negative U.S. Treasury bond yields stoked fears of a recession in the world’s largest economy, gold price ended a three-day advance and posted the worst daily fall in nearly two weeks.

US Initial Jobless Claims decreased to 228K for the week ending March 31 from 200K forecasted and an upwardly revised 246K the week before, according to the most recent data on employment in the United States. The Challenger Job Cuts for that month increased to 89.703K from 77.77K the month before. Prior to this, in February, US JOLTS Job Openings fell to a 19-month low, and in March, ADP Employment Change statistics of 145K also disappointed markets. The gloom was compounded by a decrease in the March US ISM Services PMI to 51.2 from 54.5 in February and 55.1 in March. Separately, Reuters recently raised recession concerns by pointing to the latest drop in the favourite bond market index, which is led by Federal Reserve Chairman Jerome Powell. The news reported that the most dependable bond market indication of an upcoming economic contraction was the near-term forward spread, which was calculated by subtracting the forward rate on 18-month Treasury bills from the current yield on 3-month Treasury bills. Wall Street is picking itself up and moving on while US 10-year and 2-year Treasury bond rates remain under pressure despite recent stability around 3.30 percent and 3.83 percent, respectively.

Traders in Gold, worried about a possible economic downturn, will need to carefully analyse the upcoming US job data. Gold buyers have been challenged by worries about the economy and inflation, but XAUUSD prices also appear to be vulnerable to rising geopolitical tensions between the United States, China, Russia, and North Korea. The deterioration of relations between the world’s two largest economies is hinted at by China’s criticism of US-Taiwan ties and hatred of White House competition. The fact that China is one of the world’s largest Gold importers, along with the expected haven demand for the US Dollar, should put downward pressure on the price of gold. The war between the Ukraine and Russia, Moscow’s fight with the West, and North Korea’s threat to use nuclear powers all roil the geopolitical background and stimulate the Gold buyers, in addition to the tensions between the United States and China.

Recent market action against the US Dollar’s role as the world’s reserve currency, in contrast to the aforementioned factors, appears to be keeping the Gold price in the bulls’ sights despite a weakening greenback. The recent rise in favour for the Chinese Yuan in Russia and the agreement between China and Brazil to bypass the US Dollar as an intermediary currency are two major developments that threaten the dollar’s hegemonic position. Speculation that certain US Congressmen have proposed a Gold Standard Restoration Act to preserve the US Dollar lends credence to the metal’s prospects. In the same vein as before 1971, the law proposes re-pegging the dollar to a predetermined quantity of Gold’s weight. In light of current recession fears and diminishing hawkish Fed predictions, the future price of gold depends on the March employment data from the United States.

The market expects the headline Nonfarm Payrolls number to drop to 240k from 311k, and the unemployment rate to remain unchanged at 3.6%. Gold market participants already have a lot invested in the result, but the divergent forecasts for Average Hourly Earnings just add intrigue. In the event that the US jobs report comes out worse than expected, Gold could rise much more.

SILVER Analysis

XAGUSD Silver price is moving in an ascending channel and the market has reached the higher high area of the channel.

US FED Bond markets declined due to apprehensions that FED Chairman Powell will cut interest rates at his upcoming meeting. Treasury Yields and the Bond Market’s broader spread indicate recession concerns in the United States due to the bond market’s precipitous decline. From the current range of 4.75 to 5.00%, the FED will reduce the cash rate by 70 basis points.

As Asian markets celebrate the Good Friday holiday, Reuters released negative indications from the Federal Reserve’s study, adding to the ongoing recession buzz. By falling to new lows, the bond market’s favoured recession indicator has bolstered the case for those who believe the Federal Reserve will soon need to slash rates to boost economic activity. According to Reuters, the most dependable bond market warning of an upcoming economic contraction is the near-term forward spread, which compares the future rate on Treasury bills 18 months from now with the current yield on a three-month Treasury bill.

Since November, that spread has been falling, and by Thursday of this week, it had fallen to roughly minus 170 basis points, a fresh all-time low. Investors in the money market, however, were betting on a rate cut by the Federal Reserve of around 70 basis points by December, from the current range of 4.75 to 5 percent. Powell’s curve continues to fall to new century lows, according to a note published by Citi rates analysts William O’Donnell and Edward Acton on Thursday. According to Refinitiv statistics, this was the most inversed curve seen since at least 2007.

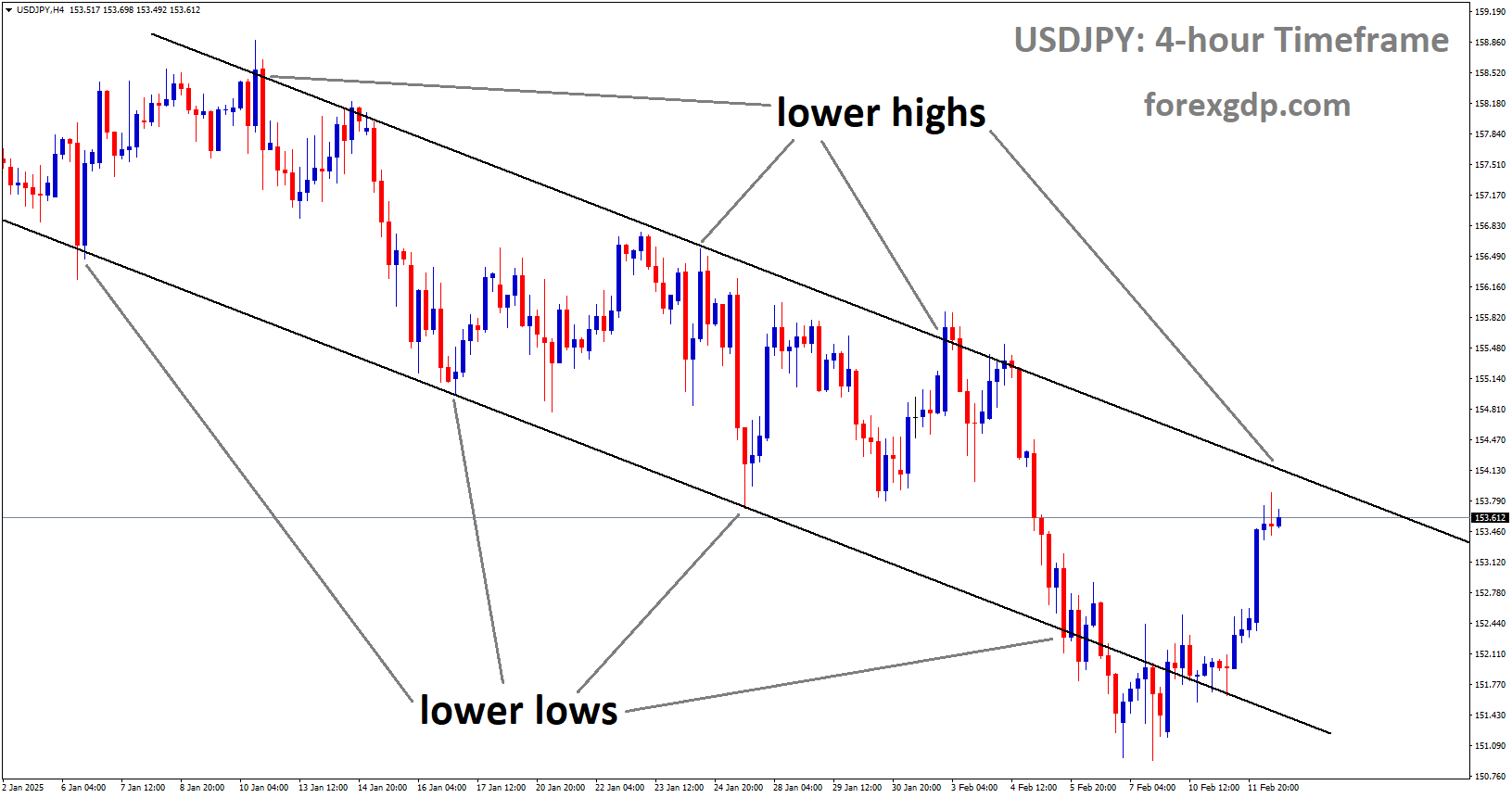

USDJPY Analysis

USDJPY is moving in the Descending channel and the market has reached the lower high area of the channel.

In his farewell interview, retiring Bank of Japan governor Haruhiko Kuroda indicated that the central bank was being patient with ultra-easy monetary policy and wage growth in order to ensure the economy’s long-term viability. Once wage growth accelerates, the inflation target will be met. The Japanese labour market is becoming increasingly competitive, yet wage growth has been slow. We can keep YCC going until we get our inflation target, and we can finally start raising interest rates once wage growth stabilises.

On Friday, at his retirement news conference, Haruhiko Kuroda, the outgoing governor of the Bank of Japan, noted that a growing trend of rising inflation being reflected in wages is being observed in Japan. Japan has made consistent progress towards the BoJ pricing target, which has been achieved in a sustainable manner. The tightening labour market in Japan is setting the stage for salary increases. With any luck, the norm that wages and prices won’t rise will be disproved, and the inflation target will be met in concert with wage increases. Inflation should reach the Bank of Japan’s price target next year if salaries continue to rise, as expected. The financial system can be kept stable even after a transition away from ultra-easy policy.

As the public’s expectation that inflation and wage growth would not occur begins to shift, the time for achieving the inflation target steadily and sustainably is drawing near. The government and the Bank of Japan’s joint statement was reasonable in terms of preventing deflation, but neither organisation will speculate on what may happen next. The claim that YCC cannot continue indefinitely whereas QQE can is false. To sustain economic expansion and wage increases, it is crucial to maintain monetary easing. It’s not accurate that policymakers deliberately tried to shock the market.

USDCAD Analysis

USDCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

The 34.7 increase in jobs in Canada well above the 12k prediction and the 21.8k previous reading. Unemployment has remained unchanged at 5% since the previous report. Although the Canadian dollar is holding its own versus most major counterparts, the Bank of Canada will likely delay any further rate hikes at next meetings due to the country’s tight labour market.

The unemployment rate remained unchanged from February at 5% in March as an additional 34.7k jobs were added. Initial projections placed the unemployment rate at 5.1%, which is consistent with the softening US employment figures released this week. Early this week, both the manufacturing and services PMI employment subcomponents and the US ADP employment report showed improvement.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel.

Because Credit Suisse mishandled bank deposits and went bankrupt, the Swiss government cut bonuses for the company’s top credit workers. Credit Suisse was sold to UBS for 3 billion Francs. Now, workers’ bonuses have been cut by 50–60 million Francs. This is mostly to help the Swiss government pay off its debts after Credit Suisse went bankrupt.

This change follows a mad dash by Swiss officials in the middle of March to complete the sale of Credit Suisse to UBS for 3 billion Swiss francs. As the ailing bank moves towards a forced merger with rival UBS, the Swiss government has reportedly imposed bonus cuts for top executives at Credit Suisse, with over 1,000 managers losing tens of millions of dollars collectively.

The seven-member Federal Council, which governs Switzerland’s executive branch, revealed on Wednesday that it had authorised the Finance Department to scrap or decrease by half or a quarter such incentives due last year among the top three echelons of management. That’ll cost you somewhere between 50 and 60 million Swiss francs in bonus money.After Credit Suisse saw massive withdrawals of deposits and a precipitous drop in its share price, Swiss officials rushed in mid-March to piece together a 3 billion Swiss franc sale to UBS. The government announced it would temporarily halt incentive payments to Credit Suisse staff two days after the deal was announced.

Top Credit Suisse executives will also have reduced or eliminated bonuses this year. UBS officials anticipate completing the acquisition within the next few months. Credit Suisse had been having problems for a long time before to the rescue, and was one of 30 banks around the world that were regarded systemically significant due to concerns that its failure would lead to a global financial crisis similar to the one that was caused by the failure of two U.S. banks. The Swiss executive branch explained that not all bank workers were affected by the bonus changes by saying that Credit Suisse’s 49,000 employees’ total deferred variable compensation, such as share awards, has fallen to 635 million francs, or about one-fourth of their total worth when initially awarded. In other words, due to the decline in Credit Suisse’s share price, all workers have already suffered a loss of over 2 billion francs. This news comes after executives of the 167-year-old lender, Credit Suisse, were criticised by shareholders the day before. At UBS’s annual shareholder meeting on Wednesday, the company’s chairman reaffirmed his firm’s belief in the transaction while highlighting its significant risks.

USD Index Analysis

US Dollar index is moving in the Descending channel and the market has reached the lower high area of the channel.

Eleven prominent banks have predicted that US nonfarm payrolls will come in at 240k, down from 311k the month before; the unemployment rate will be 3.6%; and average hourly wages will have fallen to 4.3% YoY, down from 4.6% in February. As interest rates rise, it becomes more difficult for firms to make ends meet, and 11 banks have predicted a range of 150K-250K in today’s Non-Farm Payrolls statistics. If the unemployment rate rises this time, the FED will likely raise interest rates again at their monthly meeting in May, triggering another more layoff announcements.

In anticipation of this, economists and researchers from 11 major banks have made the following predictions about the upcoming employment data. After a 311k gain in February, economists predict a 240k increase in nonfarm payrolls in March. The unemployment rate is expected to remain unchanged at 3.6%, while average hourly earnings are predicted to fall to 4.3% year-over-year from 4.6% in February. We forecast payroll growth in March to be slightly lower than in January and February, at 240K. The first two months’ data was likely inflated by the season’s extraordinary warmth, while March’s middle was a bit too chilly. If our projection holds, the rate of job creation will continue to outpace the rate of population growth, which is anticipated to add no more than 100,000 new workers every month. As a result, job availability would continue to be scarce, and the unemployment rate would likely be steady at its current all-time low of 3.6%.

It will take some time for the rising number of job layoff announcements and the expected tightening of lending conditions as a result of financial strains to be reflected in payroll data, but in the meanwhile, we remain anxious about the prognosis for jobs. Payroll growth in March of more than 200k is expected to increase hopes for a rate hike of 25 basis points. We anticipate an NFP increase of 250,000 in April and believe that job growth was robust in March.

Although the rate of payroll growth has slowed, we anticipate it to be around 190,000, which is still extremely solid considering the shrinking labour pool. A similar increase is anticipated from the household survey, which would maintain the current unemployment rate of 3.6% providing the participation rate remains stable at 62.5%. We anticipate a slowing in NFP growth. If realized, March’s projected absolute rise of 215K would be the weakest since December 2021. Monthly gains in excess of 150-175K are considered robust since they have the potential to significantly reduce the unemployment rate over time. Work opportunities are few and few between as the unemployment rate is at 3.6%. In March, wage growth is forecast to remain steady at 0.3% mum from February. Wage growth would slow as a result of this. Although the average hourly wage is not the most accurate indicator of wage inflation, it is extensively monitored because the data is released monthly and ahead of other data. Pay cuts could be the result of management giving in to employee requests. Employers’ readiness to increase salaries to retain and attract workers decreases if they believe labour needs have been met and anticipate a round of layoffs in the next few quarters. We anticipate a +250K increase in nonfarm payrolls with flat growth in both the unemployment rate and wages per hour. The March payroll survey reference period saw a steady 220K pace of hiring and continued low jobless claims. We still anticipate a final 25 bps rate hike is ahead, assuming there is no proliferation of banking sector issues, even though our forecast of 0.3% growth in average hourly earnings does not preclude reaching ontarget inflation and a 220K pace of hiring is roughly double what Powell has suggested is consistent with sustainable ontarget inflation. We anticipate a further cooling in the pace of hiring ahead, combined with a downturn in cyclical sectors, which will likely leave the Fed on pause following the May FOMC meeting. This is because private measures of job postings are falling and previously announced layoffs are still coming to actuality. Although payrolls are slightly below expectations, this is unlikely to have a significant impact on bond yields due to declining worries about the banking sector.

This year, the Good Friday payroll report will be issued in the US. A robust gain of approximately 240K is likely on tap, bringing the total for all of Q1 to beyond 1 million net new employment, making a mockery of recession rhetoric, at least at the beginning of the year. There are some downside risks due to increasing evidence of job losses in rate-sensitive sectors, but overall, we anticipate a slowing of monthly payroll growth in March to a still healthy pace of 250K jobs added. The risks of a higher or smaller rise compared to February’s average hourly earnings growth of 0.3% MoM are about even. On the one hand, underlying wage growth is likely running at least 4-6% yearly, as tightness in the US labour market should continue to put upward pressure on wages. However, the average hourly wage has likely been under downward pressure due to shifts in the sector composition of payroll employment over the past few months, and this trend may continue into March. We anticipate a drop in the unemployment rate to 3.5% in March after it unexpectedly rose to 3.6% in February. This assumes that the household survey used to calculate the unemployment rate and the labour force participation rate will show no change following recent increases in both.

In March, we anticipate a slowing in job growth to around 240K. The tight labour market is likely to be reflected in a drop in the unemployment rate to 3.5% and a gain of 0.3% in average hourly wages in March. Payrolls are predicted to have increased by 270k in March, which is a deceleration from the stronger prints seen in January and February but still indicates above-trend employment growth. It is predicted that the unemployment rate would remain at 3.6%. Last but not least, monthly pay growth should register at a solid 0.3%.

EURUSD Analysis

EURUSD is moving in an Ascending triangle pattern and the market has reached the resistance area of the pattern.

The May monetary policy meeting will be based on inflation rates, manufacturing and job figures, ECB Chief Economist Philip Lane stated at the Cyprus meeting. These interest rates are the primary means by which inflation can be reduced, and the predictions made in these words do not reflect the outcome of the May Month meeting. According to IMF MD Kristalina Georgiva, global growth will only reach 3% in 2023, down from 3.4% in 2022.

Bulls on the euro take a break with the EURUSD trading around 1.0920 ahead of Friday’s crucial U.S. employment data. This includes Europe’s biggest markets, which are closed on Good Friday, adding further pressure to the Euro pair. Despite recent recession worries, it’s important recalling that the European Central Bank has a more hawkish tilt than the Federal Reserve, which is helping the EURUSD to register its third straight weekly gain. By contrast to their US counterparts, European Central Bank hawks are unmoved by the most recent data from Germany and the Eurozone. Industrial Production in Germany increased 0.6% YoY in February, beating both market expectations and previous readings of -2.7%. Monthly results also above forecasts by 0.1%, coming in at 2.0% compared to 3.7% the month before. Germany’s factory orders for February showed an increase of 4.8% month-over-month despite a decrease of 0.3% from the prior month and 0.5% from market expectations.

Overall, the S&P Global Composite PMI for the Eurozone fell to 53.7 in March from 54.1 initial readings, with the Services PMI falling to 55.0 from 55.6 projections. For the week ending March 31 in the United States, Initial Jobless Claims decreased to 228K from the previously reported and revised 246K. The Challenger Job Cuts for that month increased to 89.703K from 77.77K the month before. Prior to this, in February, US JOLTS Job Openings fell to a 19-month low, and in March, ADP Employment Change statistics of 145K also disappointed markets. The gloom was compounded by a decrease in the March US ISM Services PMI to 51.2 from 54.5 in February and 55.1 in March. In a lecture given at a university in Cyprus, European Central Bank Chief Economist Philip Lane hinted that the May decision would depend on three factors: inflation outlook, underlying dynamic, and the rate at which these interest rate increases are stifling the economy and bringing down inflation. The policymaker added that these factors explain why they haven’t preannounced or indicated what will be discussed at the next meeting.

However, James Bullard, president of the Federal Reserve Bank of St. Louis, predicted on Thursday that inflation will be persistent in the months ahead. The euro is holding its ground against the dollar in the lead-up to crucial data due to the ECB policymaker’s somewhat hawkish tone. Recession fears were referenced by the Federal Reserve’s preferred gauge of economic health, which helped keep EURUSD prices stable. According to Reuters, the most reliable bond market signal of an imminent economic contraction has been found to be the ‘near-term forward spread, which compares the forward rate on Treasury bills 18 months from now with the current yield on a three-month Treasury bill.

In a similar vein, International Monetary Fund Managing Director Kristalina Georgieva said in prepared remarks on Thursday that she anticipates global economic growth of less than 3% in 2023, down from 3.4% in 2022. Even if the EURUSD’s reaction to data is expected to be muted by the Good Friday holiday, today US jobs report for March becomes crucial given the recently negative US employment hints and the hopes of no rate hikes from the Federal Reserve. The market expects the headline Nonfarm Payrolls number to drop to 240k from 311k, and the unemployment rate to remain unchanged at 3.6%. The result will be considerably more intriguing due to the divergent forecasts for AVERAGE HOURLY EARNINGS.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Chief UK Economist Andrew Goodwin predicted at the last meeting that the Bank of England would raise interest rates by 25 basis points at the next gathering. European trade would be hampered by the Brexit deal, and goods entering the UK will be subject to inspection. As a result of this agreement, European suppliers would suffer and food prices will rise.

In the early hours of Good Friday morning in London, the GBPUSD oscillates between 1.2155 and 1.260, recording its first day advances in three days. In doing so, the Cable pair applauds the Bank of England’s hawkish expectations while simultaneously presenting the cautious atmosphere in advance of the important US Nonfarm Payrolls. In light of ongoing inflation pressure, Oxford Economics’ Chief UK Economist Andrew Goodwin recommends that the BoE raise interest rates by another 0.25%.

But even while the BoE’s Monthly Decision Maker Panel poll suggests that the Consumer Price Index may be softening, from 5.9% predicted in February to 5.8% for the one-year forward measure, the UK’s house price index indicated that price pressure was still present. However, according to BBC News, concerns that the new Brexit deal may discourage imports from the European Union appear to be putting pressure on the GBPUSD exchange rates. According to new plans for post-Brexit border inspections on commodities entering the UK, many EU suppliers would be discouraged and food costs will rise, according to a Cold Chain Federation quoted in the press. In other places, negative US data hurt the US dollar and fuel concerns that the Federal Reserve won’t raise interest rates in May.

The same US numbers, however, cause recession problems and provide the dollar a bottom. As a result, the US Dollar Index maintains modest advances near 102.000.Speaking of US data, first claims for unemployment insurance increased to 228K for the week ended March 31 from the previously reported 246K, which was higher than projected at 200K. It’s important to note that the number of Challenger Job Cuts increased to 89.703K from 77.77K the month before. Prior to this, the US JOLTS Job Openings fell to a 19-month low in February, and the 145K statistics from the ADP Employment Change for March also let markets down. Additionally, the March US ISM Services PMI, which fell to 51.2 from 55.1 in February and 54.5 in anticipation, increased pessimism. Despite these maneuvers, market sentiment is still negative and the yields appear to be pausing their recent decline, which puts the GBPUSD purchasers in a difficult position. For new calls, the US jobs report is ultimately what matters.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

Despite the RBNZ’s rate hike this week, which boosted the New Zealand dollar, U.S. jobless claims printed at 228 thousand yesterday, favouring the US dollar over the Kiwi. New Zealand’s economy has been hit harder by inflation and has responded more slowly to the recent recession, thus a rate increase is desperately needed.

During the quiet Asian session on Good Friday, the NZDUSD continues to hover around 0.6245-40. The New Zealand traders are taking a break after the biggest one-day decline in the quotation in a month the day before. In addition to the lack of liquidity caused by the holidays, the cautious mood in advance of the March US jobs data is also limiting the quote’s immediate movements. The latest drop in the quotation may be related to scepticism in the market about the state of the world’s largest economy, the United States, and the subsequent spread of worries about a global economic crisis. But it’s important to remember that the US Dollar isn’t jumping for joy over the risk-off atmosphere because hawkish Fed forecasts are fading. However, despite the improvement in US Initial Jobless Claims to 228K for the week ending March 31, concerns of a recession increased. An increase from the previous month’s 77.77K Challenger Job Cuts to this month’s 89.703K is noteworthy. The US data has been gloomy from the get-go, notably in terms of employment and activity, which has only served to fuel fears of a downturn. The previous month saw a 19-month low in US JOLTS Job Openings, and March’s ADP Employment Change statistics of 145K also underwhelmed investors. U.S. services PMI for March decreased to 51.2 from 54.5 and 55.1, adding to the gloomy outlook. The Federal Reserve’s favoured gauge of economic health has also pointed to the recession, adding to the pressure on the NZD/USD.

The most dependable bond market indication of an upcoming economic downturn, according to Federal Reserve research, is the near-term forward spread, which compares the forward rate on Treasury bills 18 months from now with the current yield on a three-month Treasury bill. The Reserve Bank of New Zealand has surprised financial markets by increasing the benchmark interest rate by 0.50%, against the general tendency of central banks to pause rate hikes. Traders became more sceptical about the NZDUSD pair’s prior run-up and flooded the pair with further strength subsequently in response to the aforementioned unfavourable factors. The US 10-year and 2-year Treasury bond rates remain under pressure, hovering at 3.30 percent and 3.83 percent, respectively, while the Wall Street benchmarks nurse their wounds. However, despite the lack of trading activity, S&P 500 Futures are down slightly. After a period of inactivity owing to the holidays, today’s US jobs report could spark dramatic swings in the market, especially in light of the recent recessionary difficulties and dismal US data. However, the market anticipates that the headline Nonfarm Payrolls will be 240K, down from 311K, with the Unemployment Rate remaining unchanged at 3.6%.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/