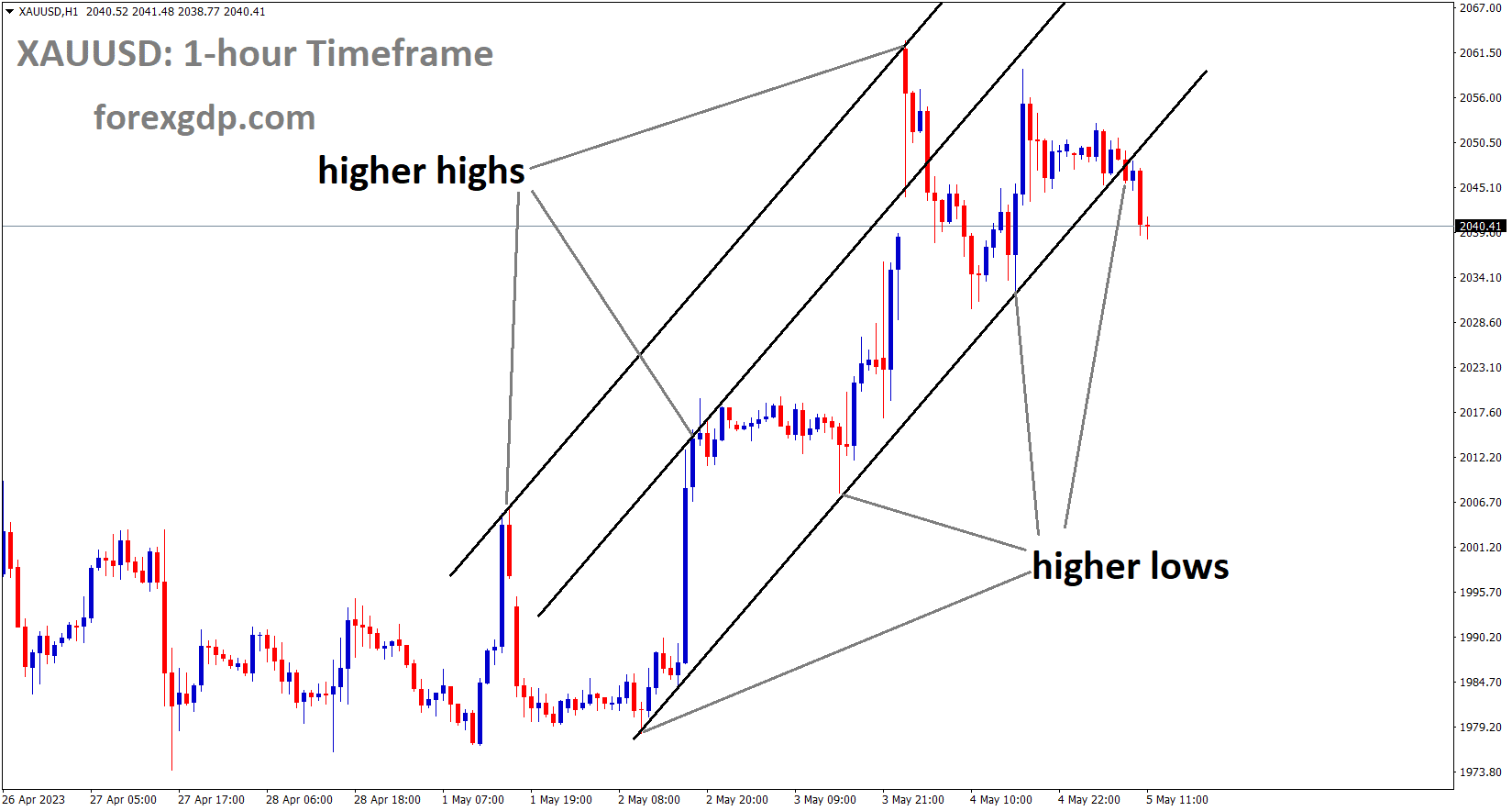

GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel.

Yesterday, gold prices surged as speculation of a rate decrease by the Federal Reserve in the month of July reached 50%. Inflation will be tempered in the coming days as a result of the FED pausing rate hikes due to the ongoing bankruptcy filings.

Over the past 24 hours, gold prices have inched cautiously higher, despite a volatile intraday trading session. On Wednesday, following the Federal Reserve’s monetary policy statement, XAU/USD momentarily reached its highest level in almost a year. However, costs have decreased recently. Gold failed to achieve its target gain of nearly 2%, instead gaining 0.35 percent. Following a 25 basis point increase in interest rates, the central bank has signalled that it may pause its tightening cycle. But Chair Jerome Powell did his best to dampen rate cut expectations for 2018. However, nobody paid any attention to his press conference. The markets finished the day strongly in favour of a rate drop in the foreseeable future. The likelihood of a rate drop in July has been priced into overnight index swaps at around 50% as of Thursday.

SILVER Analysis

XAGUSD Silver Price is moving in the Box pattern and the market has reached the resistance area of the pattern.

Problems at regional banks in the United States continued to be a source of economic unpredictability. PacWest Bancorp indicated it was contemplating a sale after getting hammered by shareholders following the acquisition of First Republic by JP Morgan and the release of Fed monetary policy. Over 93% of the stock’s value has been wiped out since its all-time high in late 2021. The near-term outlook for US inflation remains negative. The breakeven rate over two years has dropped to under 2%, the lowest level since January 2021, as shown in the chart below. The 5-year rate is moving in the same general direction, albeit not as swiftly. The weakening of the US Dollar and Treasury yields is contributing to a rise in the price of gold on the expectation of looser US monetary policy.

USDCAD Analysis

USDCAD has broken the Box pattern in downside.

In March, the Canadian Balance of Trade was C$ 0.97 billion, higher than the C$ 0.2 billion projected and the prior C$ -0.49 billion, according to a report released Tuesday. The Canadian Dollar rose versus other currency pairs as a result of this news. The Canadian dollar is receiving less support due to falling oil prices.

After a sharp decline that coincided with falling crude oil prices, the Canadian dollar has been recovering recently. Forecasts of future demand have been lowered due to worries about a global economic slowdown, and the ongoing banking problems has hampered the growth of commodity-linked currencies. The Canadian dollar strengthened against the US dollar as the country’s balance of trade report came in better than expected, while the United States’ statistics came in slightly lower than expected and their initial unemployment claims print came in higher than expected. Despite the USD trading higher on the day, the CAD has been stronger against the greenback today on the back of crude oil and the aforementioned balance of trade data. As a result of yesterday’s dovish FOMC announcement, investors are pricing out any further rate hikes until at least 2023, which has contributed to a slightly weaker dollar forecast.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel.

Inflation data for Switzerland came in at 2.6% YoY in April, down from 2.9% in March; this marks the 14th time inflation has met or exceeded the SNB’s target range of 0% – 2%. To bring inflation down to the desired 2%, the SNB raised interest rates repeatedly. In June of 2022, the SNB is widely likely to raise rates again.

Data released on Friday indicated that Swiss annual inflation decreased more than anticipated in April despite declining fuel prices, nevertheless above the central bank’s target range while still exceeding the goal. The 14. consecutive month in a row that price hikes have exceeded the Swiss National Bank’s goal range between 0% and 2% was last month, when consumer prices climbed by 2.6% year over year, down from 2.9% in March. According to Reuters’ poll of analysts, annual inflation would fall to 2.8% on average. The Federal Statistics Office reported that prices remained stable month over month as declining heating oil costs were offset by rising expenditures for air travel, package vacations, apparel, and footwear. Annual core inflation, which excludes volatile goods like food and fuel, was 2.2%, remaining constant from March.

Petroleum product costs decreased 12.1% year over year, which reflects the base effect of significant price hikes following Russia’s invasion of Ukraine in February 2022. Even though it is significantly lower than in many other nations, many of which have experienced double-digit price growth, Swiss headline inflation has continued to be above the central bank’s target range since February 2022. As a result, the SNB increased interest rates at four straight policy sessions, pushing its benchmark up to 1.5% in March. Many analysts anticipated the central bank to raise rates by at least one more time when it meets next on June 22 in light of the data released on Friday and recent statements by policymakers that suggested they were not yet finished.

USD Index Analysis

USD index is moving in the Box pattern and the market has reached the support area of the pattern.

It is predicted that the increase in US non-farm payrolls for the month of April will be 176,000, down from the 236,000 seen in March. Since 2020, this reading has been decreasing. Unemployment is forecast to remain constant at 3.5 percent today after FED rate hikes dampened slack in the labour market.

The Bureau of Labour Statistics will publish the latest Nonfarm Payrolls numbers. The NFP report is anticipated to show employment growth of 179,000 in April, down from March’s 236,000 gain.

With dovish Federal Reserve bets dominating the financial markets, the US dollar has had a hard time finding buyers this week. The next significant movement in the USD is likely to be set off by the April jobs report due to its possible impact on the Fed’s policy stance. The Federal Reserve lifted its policy rate by 25 basis points as expected, to a range of 5-5.25%; however, the statement’s note that some more policy firming may be justified was removed. In his post-meeting press conference, FOMC Chairman Jerome Powell discussed the state of the labour market, noting that there were some encouraging signs that supply and demand were returning to a more sustainable level. There are no assurances, but it is possible that the labour market cooling can persist without significant increases in the unemployment rate.

The United States monthly jobs report data for April is the most anticipated event on Friday’s economic agenda. The consensus forecast for April’s Nonfarm Payrolls is for a gain of 179K positions, down from March’s unexpectedly high 236K gain. It is predicted that the unemployment rate would stay at 3.5% in November of this year. Average hourly earnings, which are expected to remain unchanged at 4.2% annually, and labour force participation rates will also be closely watched by investors.

According to Wells Fargo analysts, payroll growth will slow even further at the start of the second quarter. So far this year, the labour market has bowed rather than broken. The employment report for April is not likely to change that. The 236K increase in nonfarm payrolls last month was the lowest reading since December 2020. Employment increased by 577K, which is positive, while the unemployment rate dropped back down to 3.5% in the separate home survey. The number of people actively seeking work has increased for the fourth consecutive month.

EURUSD Analysis

EURUSD is moving in the Box pattern and the market has reached the horizontal resistance area of the pattern.

The Euro gained ground yesterday as the European Central Bank boosted interest rates by 25 basis points in a monetary policy meeting. A statement from the ECB indicated that further rate hikes will be necessary to achieve the inflation objective of 2% in the Eurozone. Credit conditions tightened as a result of the impact on GDP growth from rate hikes in the first quarter.

The bar for an impending break higher in the euro against some of its rivals may have just been lifted by the European Central Bank. The ECB delivered the largely anticipated rate increase, which raised expectations that the central bank is getting close to pausing its tightening programme. The European Central Bank increased the main deposit rate by 25 basis points to 3.25% following a string of previous rate increases, as anticipated by the market. The central bank kept its hawkish approach, claiming that the current level of interest rates was insufficient to restrain inflation to the ECB’s 2% target. The allusion to potential policy choices suggests that there will be more than one rate increase this cycle.

According to the ECB, the reason for the downshift was likely due to the weak Q1 GDP growth, tepid inflation, and tightening credit conditions, which indicate that the effects of the rate hikes are beginning to firmly filter down to the economy. The terminal rate is subject to downside risks because of the central bank’s sensitivity to the robust transmission mechanism. Because of this, money markets have reduced their prior forecast of the ECB terminal rate from 3.75% to 3.65%, which has weighed on the EUR.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

The last S&P Global/CIPS Services PMI for the UK went up from 52.9 to 55.9. This information shows that businesses put the cost of higher wages on the customer side. This will put more stress on households. On May 11, the Bank of England will have to raise interest rates to lower the costs of inflation for the public. The Bank of England has raised rates 12 times since 2021.

In the early European session, the GBPUSD pair broke through the psychologically significant round number of 1.2600. The Cable has re-established a fresh 11-month high at 1.2614, and further gains are possible as the US Dollar Index is anticipated to show additional decline in the face of several headwinds. In Asia, S&P500 futures have soared as investors become more optimistic in response to the Federal Reserve’s dovish stance on interest rates. Consistently for the past three trading days, US shares have closed in the red region on revived worries of a US financial crisis, potential worries about the US debt ceiling, and uncertainty over the Federal Reserve’s plan for bringing down stubborn inflation.

As a delay in the US debt ceiling rise could impact the long-term outlook of the United States economy, the USD Index has sharply corrected to near 101.15 and is expected to show some further downside to near the crucial support of 101.00. However, after a precipitous drop, US yields have begun to rise again. Ten-year bond yields in the United States have risen back above the 3.38% mark. Millions of Americans could lose their jobs and the GDP would be stifled if the White House delays raising the debt ceiling, which is a major concern for investors. The dollar will suffer greatly as a result of this. The US dollar would suffer even if the debt ceiling increase was approved on schedule, since credit rating agencies would likely downgrade their long-term outlook for the US economy as a result. The value of the dollar, Treasury yields, and stock markets would all be significantly affected by raising the debt ceiling, while demand for Gold as a safe haven would rise.

USD Index rebound would depend on the availability of US labour market statistics, as Fed head Jerome Powell has already indicated that any future policy action will be data-driven. Preliminary data from the US Bureau of Labour Statistics shows that the economy added 179K jobs in April, which is less than the 236K jobs added in March. At 3.5%, the unemployment rate is anticipated to remain stable. Aside from them, the data on average hourly earnings will be the most important factor. The median hourly wage may stay put at $9.00 per month and $4,20.00 per year. The final reading for the United Kingdom’s S&P Global/CIPS Services PMI increased to 55.9 from March’s 52.9. Reuters found that pay increases were easily passed on to consumers by UK companies. More pressure will be put on households, and the Bank of England will be torn between easing these pressures and reducing persistent inflation. Thursday, May 11, marks the date that investors will be waiting for the Bank of England to announce its interest rate decision. To stem double-digit inflation, Bank of England Governor Andrew Bailey is widely anticipated to implement an additional rate hike of 25 basis points. If the Bank of England were to increase interest rates in 2021, it would be the 12th increase in a row.

GBPJPY Analysis

GBPJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

It was widely anticipated by economists that the Bank of Japan would soon recover from its ultra-easy monetary policy. However, the Bank of Japan has consistently maintained its easy monetary policy despite rising concerns about inflation. The Japanese Yen this week is mostly being influenced by data from the European Central Bank, the Federal Reserve, and the United States.

In the Asian session, the EURJPY pair is having trouble pushing past the immediate barrier of 148.00. Investors are waiting for the publication of data on Eurozone Retail Sales, which is putting pressure on the cross. After the European Central Bank ended the suspense and raised interest rates by 25 basis points to 3.25% on Thursday, the euro suffered greatly. The ECB’s 50-bps rate-hike cycle came to an end, and it switched to a lower rate increase since the Eurozone economy was demonstrably responding to the monetary policy. Because businesses are struggling to deal with the burden of higher borrowing costs and a gloomy economic outlook, the ECB chose to raise interest rates only slightly in the face of a weak Eurozone growth rate and declining credit disbursement from Eurozone commercial banks.

The struggle against persistent inflation is far from done, as ECB President Christine Lagarde stated ‘loud and clear’ in the monetary policy statement, signalling the imminence of more than one additional rate hike. Future Eurozone retail sales will be closely monitored. According to projections, monthly retail sales have remained unchanged after declining by 0.8% in March. The yearly retail demand is predicted to fall by 3.1% instead of the previous 3.0%. Investors anticipate that the Japanese Yen will experience a wider recovery if the Bank of Japan abandons its ultra-loose monetary policy. However, the BoJ is being forced to maintain an expansionary policy stance due to Japan’s declining consumer inflation expectations.

AUDUSD Analysis

AUDUSD is moving in an Ascending channel and the market has reached the higher high area of the channel.

According to the RBA’s monetary policy statement, interest rates could rise to 3% by the middle of 2025, up from the current 3.75%. The skyrocketing cost of energy has had a ripple effect on the price of petrol.

Inflation is expected to reach 4.5 percent in 2023, 3.2 percent in 2024, and 3 percent by the middle of 2025. Forecasts for GDP are 1.2% in 2023, 1.7% in 2024, and 2.1% by the middle of 2025.

The following is the RBA Monetary Policy Statement from the Reserve Bank of Australia. The forecasts assume a peak rate of 3.75%, with rates falling to 3% by mid-25. It’s possible that more stringent monetary policy is needed. The rising cost of fuel will have a major impact on inflation next year. We remain dedicated to bringing inflation back down to acceptable levels. The board’s goal is to preserve as many job increases as feasible. A price-wage spiral is more likely the longer inflation is persistently higher than the goal rate.

Although goods inflation has been low so far this year, energy price increases are expected to remain elevated. The Consumer Price Index is expected to rise 4.5% in 2023, 3.2% in 2024, and 3.0% by the middle of 2025. Trimmed mean inflation is expected to reach 4.0% by 2023’s end, 3.1% by 2024’s, and 2.9% by 2025’s midpoint. It seems likely that China will achieve its growth target of 5% for the year. GDP growth predictions for 2023 are 1.2%, 1.7%, and 2.1% by mid-2025.

NZDUSD Analysis

NZDUSD is moving in an Ascending channel and the market has reached the higher high area of the channel.

The weakening of the US dollar helped the New Zealand dollar after the FED said that the rate hike was enough to slow inflation in the US. This month’s RBNZ meeting is likely to be 50bps, which is good for the New Zealand Dollar. The New Zealand Dollar went up against the US Dollar because the US NFP numbers were due and people expected them to be lower than the month before.

As Friday’s European session begins, the NZDUSD is at its strongest level in a month, up around 0.5 percent near 0.6310. By doing so, the Kiwi pair is celebrating widespread weakness in the US Dollar before the release of US Nonfarm Payrolls data. The recent difference between the Fed’s and the Reserve Bank of New Zealand’s biases may provide support to the positive case. After raising benchmark interest rates to record highs not seen since 2007, the Federal Reserve has hinted that it may suspend the rate hike trajectory. This adds to the Fed chairman’s cautionary comments that the existing monetary policy is already rather restrictive.

After that, the NZDUSD rally gets a boost from Thursday’s mixed US data and rising market bets for a Fed rate hike in September 2023. However, initial estimates for the first quarter of 2023 for US Nonfarm Productivity and Unit Labour Cost were contradictory. Unit Labour Cost increased by 6.3% from 5.5% predicted and 3.0% previously, while Nonfarm Productivity fell to -2.7% in Q1 from 1.6% in Q4 and -1.8% in market estimates. U.S. goods and services trade surplus also rose to $-64.2B from $-70.6B and the $-63.3B expected by the market. In addition, the number of people filing for unemployment benefits rose to 242K in the week ending April 28, which is more than the 240K forecast and the 229K seen in prior reports. In addition, there is rising evidence in Fed Fund Futures that a rate cut will occur in late 2023.

However, despite RBNZ Governor Adrian Orr earlier in the week citing the negative impacts of higher rates on farms, the RBNZ has already pleased the NZDUSD hawks with a 0.50% rate hike. When asked about the causes of this unusual performance, ANZ speculated that “strong local data and widespread markets expectations that the Fed is done this cycle” were possible contributors. Now, before the crucial US employment data for April, NZDUSD bull may see lacklustre moves. Forecasts indicate negative prints of the headline US Nonfarm Payrolls, projected 179K versus 236K prior, while early signals for the data are robust, therefore the odds favouring the pair’s retreat are high.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/