XAUUSD Resilient While US Targets Bullion Imports with Fresh Tariffs

Gold has been making headlines lately, not just for its steady value but for the political and economic moves surrounding it. The recent announcement by the United States to impose tariffs on imported gold bars has stirred discussions in global markets. While futures reached record highs, spot prices have remained relatively stable, showing that investor sentiment is influenced by more than just immediate headlines. Let’s break down what’s happening, why it matters, and what could be on the horizon.

A Fresh Twist in the Gold Market

The global gold market thrives on stability, but every so often, a policy decision shakes things up. The latest twist came when the US government decided to place tariffs on one-kilogram gold bars. This move, confirmed through a letter from US Customs & Border Protection, has widened the gap between spot prices and futures.

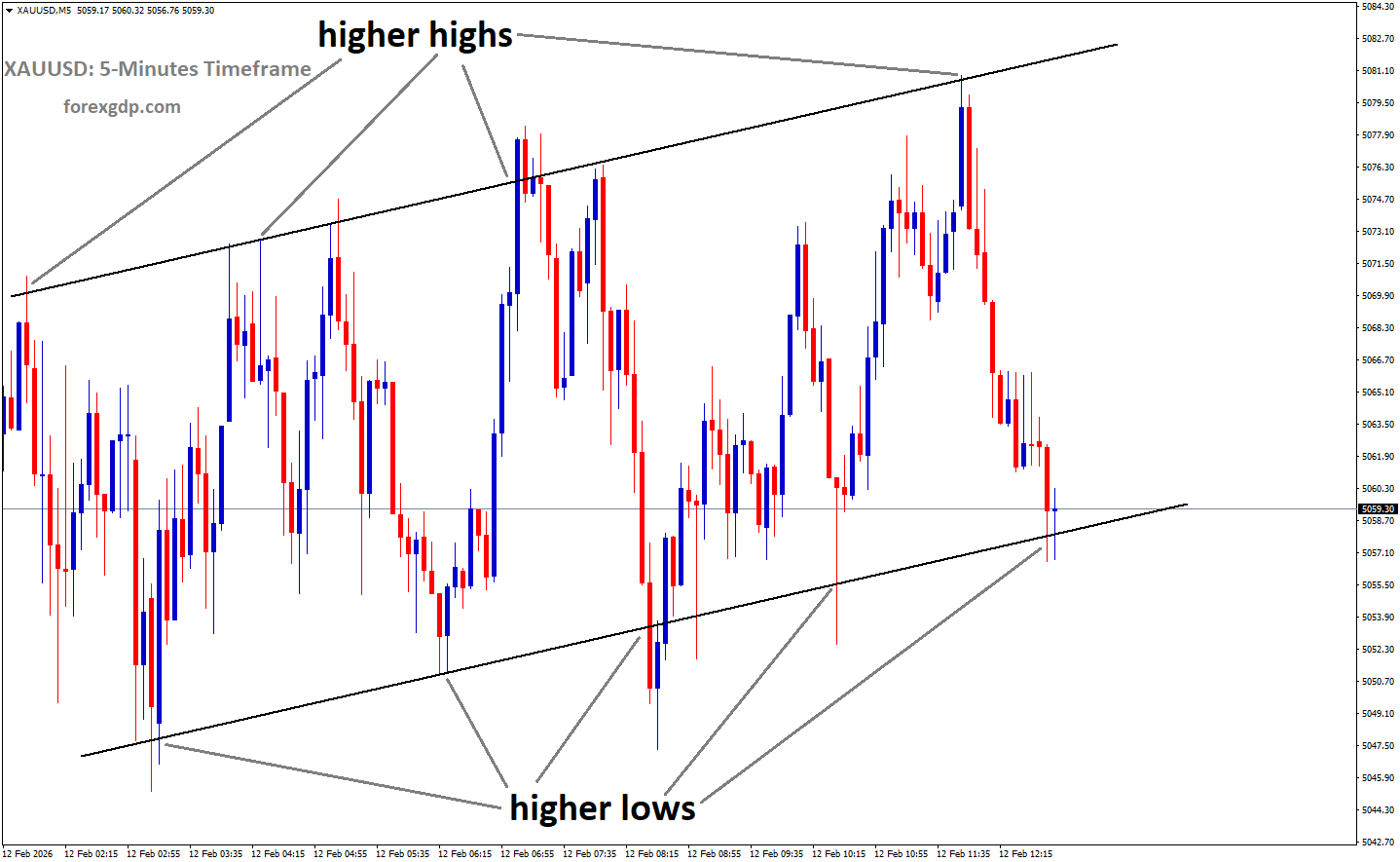

XAUUSD is moving in a box pattern, and the market has rebounded from the support area of the pattern

The interesting part? While futures prices jumped significantly, spot prices barely moved. This suggests that while traders are reacting strongly to the policy in future markets, immediate demand and supply in the physical market have not shifted dramatically yet. The difference between these two price movements has sparked curiosity among investors and analysts, as it may point to deeper shifts in trading strategies and supply chains.

The Swiss Reaction: Concerns Over Trade Flow

Switzerland, a key player in the global gold trade, quickly voiced concerns about the new tariffs. The Swiss Gold Association stated that the added costs make exporting gold bars to the US far less viable. Given Switzerland’s historical role in refining and distributing gold worldwide, any disruption to this flow can have ripple effects on the global precious metals market.

Impact on International Gold Movement

Tariffs don’t just affect price; they can alter the entire logistics of gold distribution. By increasing costs for Swiss gold exporters, these tariffs could force a shift in trade routes, leading to changes in where and how the US sources its bullion. Over time, this could influence refining centers, shipping channels, and even the role of gold in certain investment portfolios.

The Federal Reserve’s Role in the Bigger Picture

While tariffs dominated the headlines, the Federal Reserve has also been a big factor in shaping gold sentiment. Recent US economic data — from weaker job numbers to slower service sector growth — has led traders to believe that the Fed is leaning toward a rate cut in September. In fact, many market watchers are pricing in a high probability of a 25-basis-point cut.

Why Interest Rates Matter for Gold

Gold doesn’t yield interest, so when rates are high, it can become less attractive compared to interest-bearing assets. A potential rate cut makes gold more appealing, as the opportunity cost of holding it decreases. This is why even without major movements in spot prices, the broader outlook for gold has a bullish undertone.

Key US Data to Watch

The coming weeks will be important for gold watchers, as several pieces of economic data could shape the Fed’s next move — and in turn, gold’s trajectory. Among the most closely watched reports will be:

-

Consumer Price Index (CPI) – A critical measure of inflation that could either support or weaken the case for a rate cut.

-

Producer Price Index (PPI) – Offers insights into wholesale price changes, another inflation gauge.

-

Retail Sales Data – A measure of consumer spending strength, which reflects economic health.

-

Jobless Claims – Provides clues on labor market stability.

-

Consumer Sentiment Index – Reveals how optimistic or cautious households are about the economy.

With multiple Federal Reserve officials also scheduled to speak, traders will be parsing every word for hints about policy direction.

Labor Market Weakness Adds Pressure

Recent US labor market figures showed a modest increase in unemployment benefit claims, hinting at potential cracks in what has been a resilient employment picture. Continuing claims have risen to their highest level since late 2021, suggesting some people are finding it harder to get back into the workforce.

For the Fed, this presents a balancing act. On one hand, rising unemployment supports the case for lowering rates to stimulate economic activity. On the other, inflationary pressures — such as higher costs in the service sector — might make them more cautious about cutting too soon.

Gold’s Steadiness in Uncertain Times

Despite all these developments, gold’s spot price has remained relatively stable. This stability tells us that while there are short-term reactions in the futures market, the physical market remains anchored by broader forces such as long-term investor demand, global economic uncertainty, and central bank policies.

XAUUSD is moving in an ascending triangle pattern

Why Investors Still Flock to Gold

-

Safe-Haven Appeal – In times of political or economic uncertainty, gold remains a go-to asset.

-

Hedge Against Inflation – Even modest inflation fears can drive interest in gold.

-

Portfolio Diversification – Investors use gold to balance risk in their holdings.

Global Trade Tensions Could Keep Gold in Focus

The tariff move is just the latest reminder that gold prices can be influenced as much by geopolitical decisions as by traditional market factors. If other countries respond to the US move with their own trade measures, or if tensions rise in other sectors, gold could see renewed demand.

For now, investors are taking a wait-and-see approach. They’re closely watching both the Fed’s next move and the global response to these tariffs. Any signs of prolonged trade friction or slowing US economic growth could push gold back into the spotlight for even more investors.

Final Summary

The gold market is navigating a unique mix of influences right now. On one side, US tariffs on imported gold bars are reshaping trade dynamics and sparking concern from major exporters like Switzerland. On the other, US economic signals are pointing toward a possible interest rate cut, which could make gold more attractive in the months ahead.

While futures markets have reacted strongly to the tariff news, spot prices have held steady, reflecting a balance between immediate physical demand and speculative trading. In the coming weeks, the release of key US economic data and further Fed commentary will likely set the tone for gold’s next major move.

In short, gold is once again proving its reputation as a resilient, long-term store of value — even as politics, economics, and global trade keep throwing it into the headlines.

EURUSD Nears Top of the Week with Dollar Under Pressure from Fed Speculation

The EUR/USD pair has been making small moves recently, but the bigger picture tells an interesting story. Even though the euro has been holding close to recent highs, it hasn’t been able to push much further. Several global and domestic factors are shaping its direction, from political developments to changes in economic sentiment.

This week, the market’s attention has shifted away from technical price patterns and toward broader events that could influence the euro’s future path. Let’s break down what’s been going on and what could be next.

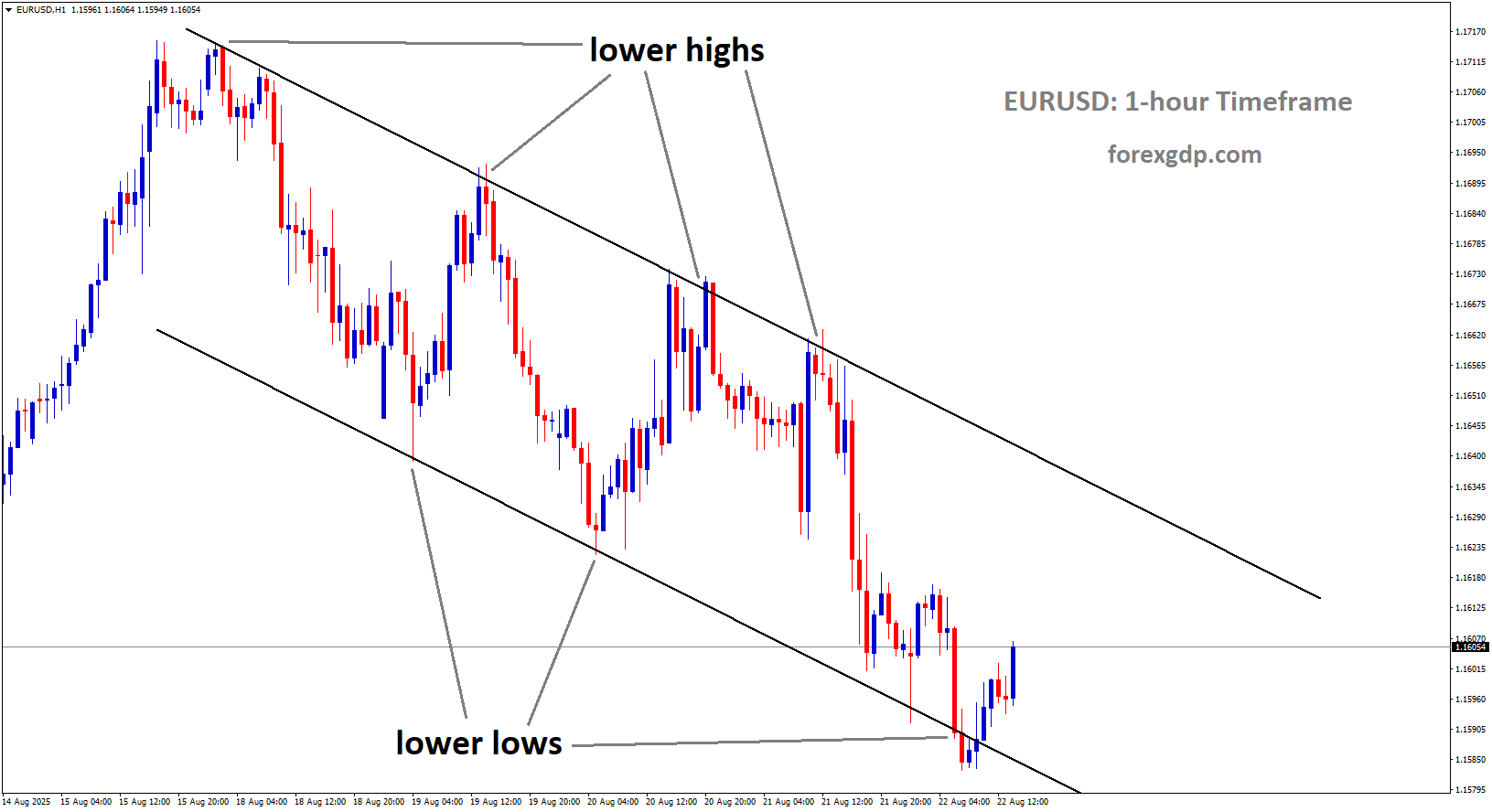

EURUSD is moving in an Ascending channel, and the market has rebounded from the higher low area of the channel

Geopolitical Shifts: Could Peace Talks Change Everything?

One of the biggest stories influencing the market this week is the possibility of a Trump–Putin meeting. Reports suggest that the two could meet next week to discuss a ceasefire in Eastern Europe, particularly addressing the ongoing conflict in Ukraine.

Such a development would have significant implications. A potential halt in hostilities could improve market sentiment, reduce uncertainty, and boost investor confidence in the region. While nothing is confirmed yet, even the possibility of progress has already had an impact on currency movements.

The euro initially responded positively to the news, reflecting optimism that tensions might ease. However, this upward push didn’t last long, as other factors quickly came into play.

The Dollar’s Strength and the Fed’s Influence

The US Dollar has been staging a quiet comeback, which has capped the euro’s ability to climb higher. This strength isn’t just about the dollar itself—it’s also tied to speculation over who will take over as the next Federal Reserve Chair.

Rumors suggest that Fed Governor Christopher Waller could be a leading candidate to replace Jerome Powell. Markets tend to react strongly to leadership changes at the Fed, especially when they could signal a shift in interest rate policy.

At the same time, comments from Fed officials are adding to the mix. St. Louis Fed President Alberto Musalem recently adopted a more neutral tone, highlighting risks to both inflation and employment. This balanced approach has left investors wondering whether the Fed might be preparing to adjust its strategy.

Economic Data and Market Sentiment

While geopolitics has been in the spotlight, recent US economic data is also playing a major role in shaping currency movements.

Weakening Labor Market Signals

Thursday’s jobless claims report showed an increase in new unemployment filings, while continuing claims hit their highest level since late 2021. These figures point to a potential softening in the labor market.

Some economists are warning that this could be part of a larger stagflationary trend—a mix of slow growth and high inflation. If this view gains traction, it could push the Fed toward easing monetary policy sooner than expected.

Upcoming Economic Events

Looking ahead, traders will be keeping a close eye on:

-

US Retail Sales data

-

Initial Jobless Claims

-

Speeches from Fed officials

These releases could provide fresh clues about the direction of the US economy and the Fed’s next moves.

The European Side of the Story

While much of the euro’s recent movement has been influenced by the US, there’s also plenty happening within the Eurozone.

Next week’s European economic calendar is expected to include:

-

Inflation figures for Italy and Germany

-

ZEW Economic Sentiment surveys for Germany and the EU

-

EU GDP growth data for Q2 2025

These reports will be important for assessing the health of the euro area’s economy and could influence whether the European Central Bank (ECB) maintains its current policy stance or shifts toward easing.

Currently, market expectations suggest that the ECB is likely to keep interest rates unchanged in September, with only a small chance of a rate cut. This cautious approach contrasts with speculation that the Fed might move toward rate reductions sooner.

What Traders Are Watching Right Now

The euro’s rally in recent days has stalled mainly due to the US dollar’s renewed strength and ongoing uncertainty about the Fed’s policy direction. Traders are weighing the possibility of a major geopolitical breakthrough against the reality of slowing economic growth and rising inflation pressures in the US.

EURUSD is moving in an Ascending channel, and the market has reached the higher high area of the channel

On the European side, the focus will be on whether inflation continues to ease and whether business sentiment improves. Any surprises—positive or negative—in the upcoming data could trigger stronger moves in EUR/USD.

Final Summary

The EUR/USD pair is caught between optimism and caution right now. Hopes of a breakthrough in Eastern Europe and signs of a softer US labor market have given the euro some support. However, the US dollar’s resilience, Fed leadership speculation, and mixed economic signals have kept the currency from breaking out higher.

Over the next week, traders will be closely following both US and European economic releases, as well as any developments in geopolitical talks. The combination of political events, central bank policy signals, and economic data will likely decide whether the euro can extend its recent gains—or if it will retreat.

If peace talks progress and European data surprises on the upside, the euro could find new momentum. On the other hand, if the US dollar continues to strengthen and economic uncertainty lingers, the currency may face more challenges ahead.

GBPUSD Flat as BoE Draws Line on Cuts While Fed Chair Chatter Fuels Dollar Strength

The GBP/USD currency pair is holding steady as traders digest fresh developments from both the Bank of England (BoE) and the U.S. Federal Reserve. While the pound has managed to maintain its gains despite recent interest rate adjustments, overall market sentiment is still being influenced by a mix of political rumors, central bank leadership changes, and shifting economic expectations.

Bank of England’s Cautious Rate Cut and Market Reaction

The Bank of England recently reduced interest rates by 25 basis points in a narrow 5–4 vote. This move, while technically easing policy, was interpreted by markets as a cautious, possibly one-off adjustment for the year. The closeness of the vote highlights just how divided policymakers are about the future path of rates.

GBPUSD is moving in a descending channel, and the market has reached the lower high area of the channel

For traders, the key takeaway is that the BoE is signaling caution rather than an aggressive shift. Current market pricing suggests an 87% probability that rates will remain unchanged at the upcoming September meeting. This shows that investors believe the central bank is content to pause further cuts until more data comes in.

Why the Market Sees Limited Cuts Ahead

A major reason behind this outlook is the BoE’s own language. Some officials have voiced concern about inflation pressures in the medium term, suggesting they do not want to ease too quickly and risk undoing recent progress in bringing price growth down. In fact, BoE Chief Economist Huw Pill—who opposed the cut—emphasized that while disinflation is ongoing, there are still risks of inflation rising again over the next two to three years.

U.S. Federal Reserve Dynamics and Leadership Speculation

Across the Atlantic, the U.S. dollar has seen a modest recovery, partly due to a swirl of political and central bank developments. One of the most talked-about rumors is that Fed Governor Christopher Waller is the preferred choice of the Trump administration to succeed Jerome Powell when his term ends in May 2026. This kind of speculation can influence market expectations about the Fed’s future policy stance, especially if traders believe Waller might adopt a different approach to interest rates.

In the meantime, the Fed is experiencing changes in its own leadership. Dr. Stephen Miren has been nominated to replace Fed Governor Adriana Kugler, who has stepped down. While these personnel changes may not immediately affect interest rate policy, they can subtly shape the Fed’s internal debates in the months and years ahead.

Fed’s View on Inflation and Jobs

St. Louis Fed President Alberto Musalem, who will be a voting member of the Federal Open Market Committee (FOMC) in 2026, recently shared his views on the economy. He noted that economic activity remains steady and that companies are generally not resorting to layoffs to cut costs. However, he admitted that inflation is still missing the Fed’s target, which remains the central challenge. According to him, the risks are more tilted toward potential weakness in the job market rather than overheating.

Key Economic Events to Watch Next Week

The week ahead promises to be busy for both UK and U.S. economic calendars, with several important releases that could influence GBP/USD direction.

In the UK

-

Retail Sales – A key measure of consumer spending, which could give insights into whether UK households are tightening their belts or spending more freely.

-

Employment Data – Labor market conditions are crucial for the BoE’s policy outlook, as strong employment often supports higher wages and, in turn, inflation.

-

GDP Figures – This will provide a broad snapshot of how the economy performed recently, offering clues about whether growth momentum is picking up or slowing down.

In the U.S.

-

Consumer Price Index (CPI) – The most closely watched inflation measure, CPI can shift expectations about future Fed rate moves.

-

Retail Sales – Like in the UK, U.S. consumer spending trends are a major driver of economic growth.

-

Producer Price Index (PPI) – Offers an early look at inflation pressures in the supply chain.

-

University of Michigan Consumer Sentiment – A gauge of household confidence that can indicate whether consumers are feeling optimistic or cautious.

What This Means for Traders and Investors

With both central banks facing policy crossroads, traders are likely to see choppier conditions in GBP/USD in the near term. The pound’s resilience despite a rate cut suggests markets had already anticipated the move, and the lack of an aggressive easing signal has supported the currency. Meanwhile, in the U.S., the dollar’s slight recovery reflects both improved sentiment toward the economy and the ongoing speculation about future Fed leadership.

GBPUSD is moving in an uptrend channel

The coming week’s data will be crucial. Any surprises—especially in inflation or job numbers—could quickly shift expectations for both the BoE and the Fed. For now, the market seems content to wait for clearer signals, which is why GBP/USD has remained steady.

Final Summary

The GBP/USD exchange rate is treading water as traders weigh a cautious BoE rate cut, steady economic signals from the Fed, and political rumors about future central bank leadership. While the pound has held firm due to expectations that no further cuts are likely this year, the U.S. dollar is finding some support from leadership speculation and stable economic indicators. With a busy calendar of economic data ahead in both countries, the next few days could bring more decisive moves. For now, the market mood is one of patience, waiting for the next big signal before making bold moves.

USDCHF Struggles While US Tariffs Hit Switzerland’s Precious Metal Trade

The currency market has been buzzing recently, with the USD/CHF pair showing limited movement while traders keep a close eye on new trade developments. The Swiss Franc has been under pressure, largely due to a fresh round of US tariffs that directly target Switzerland’s gold exports. This move could have lasting consequences for the Swiss economy, the global gold market, and trade relations between the US and Switzerland. Let’s break down what’s happening, why it matters, and what could come next.

USDCHF is rebounding from the retest area of the broken ascending triangle pattern

A Calm Market with Big Underlying Tensions

Over the past week, USD/CHF has been moving within a narrow range, showing little sign of breaking out strongly in either direction. On the surface, it might look like a calm market, but beneath that stability lies a story of economic tension and cautious investor sentiment.

Right now, there’s a “risk-on” mood in global markets, supported by strong performances in equities. Typically, when stocks are doing well, investors feel less inclined to seek the safety of the Swiss Franc. However, the calmness in the USD/CHF pair is not just about global stock market optimism—it’s also about traders waiting to see how the US tariff decision plays out.

The US Targets Swiss Gold Bars

In a surprising move, the United States has imposed import tariffs on two specific forms of Swiss gold bars—1-kilogram and 100-ounce cast bars. These are not just any gold bars; they are standard bullion forms refined in Switzerland, a country widely regarded as one of the world’s leading precious metal hubs.

Switzerland’s gold industry is massive. Every year, the country exports billions of dollars’ worth of gold to the US. By targeting these specific bars, the US has effectively disrupted a major flow of trade in the global bullion market.

The change came after a ruling from US Customs & Border Protection (CBP) on July 31, which reclassified these gold bars under a new tariff code. This move was unexpected, and the global bullion market reacted sharply, with gold futures jumping to record highs immediately after the announcement.

Why This Tariff Matters So Much

Impact on Switzerland’s Gold Industry

The Swiss Association of Manufacturers and Traders in Precious Metals (ASFCMP) has openly expressed concern about the US decision. Industry leaders say this tariff could cause serious disruptions in the gold supply chain. Switzerland’s refiners were caught off guard, especially since these gold bars had previously been exempt from such import duties.

This isn’t just about higher costs. It’s about potentially reshaping trade flows that have been stable for decades. For a country that plays such a key role in the world’s gold market, this could mean rethinking production strategies, finding new buyers, or negotiating trade adjustments with the US.

Strain on US-Swiss Trade Relations

The relationship between Switzerland and the US has generally been stable when it comes to trade. But this move has introduced friction. Swiss officials have been quick to engage in talks with their American counterparts to try and resolve the issue.

The State Secretariat for Economic Affairs (SECO) confirmed that discussions are ongoing at a technical level. However, political efforts have so far not yielded a breakthrough. In fact, Swiss President Karin Keller-Sutter recently left Washington without securing any progress on reducing the tariffs, signaling that the situation might take time to resolve.

Global Market Reactions and the Bigger Picture

The gold market is sensitive to policy changes, and this tariff is no exception. When a major trading route is affected—especially one involving Switzerland—global supply chains feel the pressure. This can influence pricing, investor behavior, and even currency movements.

For the US, this is part of a broader trade approach that has, in recent years, included tariffs on a range of imports. For Switzerland, it’s a test of its ability to navigate changing global trade policies while protecting one of its most valuable export sectors.

What Could Happen Next for USD/CHF

Even though the Swiss Franc has been under some pressure, its downside might be limited in the near term. One reason is the growing expectation that the US Federal Reserve could cut interest rates as early as September. If that happens, it could cap the strength of the US Dollar, giving the Swiss Franc some breathing room.

Investors will also be paying close attention to upcoming US economic data, including inflation numbers, retail sales figures, and consumer sentiment surveys. These reports will influence market expectations for the Fed’s next move and, in turn, could impact the USD/CHF pair.

The Road Ahead: Trade Talks and Market Watch

For now, both traders and policymakers will be watching two key developments:

-

How trade negotiations between Switzerland and the US unfold

-

Whether the Federal Reserve changes interest rates in the coming months

USDCHF is moving in a box pattern, and the market has reached the support area of the pattern

Any progress in tariff discussions could quickly shift sentiment around the Swiss Franc, while changes in US monetary policy could either strengthen or weaken the Dollar’s position against it.

Final Summary

The current USD/CHF stability hides an undercurrent of trade tension sparked by the US decision to impose tariffs on Swiss gold bars. This move has rattled Switzerland’s gold industry, strained trade relations, and raised concerns over the stability of the global bullion market. While the immediate currency impact has been modest, the long-term effects could be significant if trade talks stall and global market conditions shift.

As things stand, the Swiss Franc may find some support if the US Dollar softens due to potential Fed rate cuts. But until there’s clarity on tariffs, traders and businesses will remain cautious. This situation is a reminder that in global markets, even a highly specific policy change—like targeting certain gold bars—can ripple across industries, borders, and currencies.

USDCAD Gains Momentum After Canada’s Labor Market Stumbles

The Canadian Dollar (CAD) lost ground against the US Dollar (USD) after Canada’s latest jobs report showed a sharp drop in employment. Fresh numbers from Statistics Canada revealed that the economy shed 40,800 jobs in July, a stark contrast to expectations of a modest gain. While the unemployment rate held steady at 6.9%, the disappointing data has raised fresh concerns about the strength of Canada’s economy and the possibility of a more cautious stance from the Bank of Canada (BoC) in the months ahead.

USDCAD is rebounding from the retest area of the broken descending triangle pattern

Job Losses Signal Economic Slowdown

The July employment report was a setback for those hoping the Canadian economy would maintain momentum. After adding over 83,000 jobs in the previous month, the loss of nearly 41,000 positions came as a surprise. Even more telling was the drop in the participation rate, which slipped from 65.4% to 65.2%. This decline suggests that fewer Canadians are actively looking for work, a sign that the labor market may be losing steam.

While the unemployment rate did not increase, staying just below forecasts, the drop in participation masks some of the underlying weakness. Employers seem to be pulling back on hiring, and combined with a softer labor force, it paints a picture of an economy struggling to maintain growth.

Wage Growth Offers a Mixed Signal

One notable aspect of the report was the rise in average hourly wages, which climbed 3.5% year-over-year in July, up from 3.2% in June. On the surface, this might seem like good news for workers, as it indicates they are earning more. However, the wage growth comes against the backdrop of slower job creation, which complicates the outlook.

For the Bank of Canada, this is a delicate balancing act. On one hand, higher wages can support consumer spending and help offset slower hiring. On the other, they can also keep inflation pressures alive, making it harder for the central bank to ease monetary policy too aggressively.

Bank of Canada’s Policy Challenges

The BoC recently held its key interest rate steady at 2.75% in July, marking its third consecutive pause. This decision followed several earlier rate cuts in the year, aimed at supporting growth in the face of global uncertainties. But the latest jobs report, combined with ongoing concerns about trade tensions and inflation, could push policymakers to take an even more cautious approach.

Governor Tiff Macklem has previously highlighted the unpredictable nature of US trade policy as a key risk to Canada’s economic stability. With tariffs and trade negotiations still in flux, the central bank has little room for error. Market analysts are now leaning toward the possibility of a rate cut by the end of the year, with many seeing the odds as high as 80%.

External Factors Adding Pressure on the Loonie

Aside from domestic economic data, the Canadian Dollar is also feeling the impact of broader market forces. A modest rebound in the US Dollar, coupled with weaker oil prices, has put additional pressure on the Loonie. Since Canada is a major oil exporter, falling crude prices often translate into reduced demand for the Canadian currency.

Meanwhile, the US Dollar Index has been holding firm, reflecting investor confidence in the US economy relative to other major economies. With few major US data releases this week, traders are already looking ahead to next week’s US Consumer Price Index (CPI) report, which could influence the Federal Reserve’s next move on interest rates. Any signs of persistent US inflation could further strengthen the Dollar and weigh on CAD.

Looking Ahead: What to Watch Next

For traders and investors, the next big event on the calendar will be the release of US inflation data. This report could shift expectations for the Federal Reserve’s policy path, which in turn could have ripple effects on the USD/CAD exchange rate. If US inflation comes in higher than expected, it might delay Fed rate cuts, keeping the Dollar stronger for longer.

USDCAD is moving in a box pattern, and the market has fallen from the resistance area of the pattern

On the Canadian side, markets will be closely watching upcoming economic indicators such as retail sales and GDP growth figures. Any signs of further weakness could bolster the case for the BoC to ease policy sooner rather than later. At the same time, energy prices will remain a critical factor, as any rebound in crude oil could offer some support to the Canadian Dollar.

Final Summary

The Canadian Dollar’s recent weakness stems from a combination of disappointing domestic job data, cautious central bank policy, and external market pressures. July’s employment losses highlight the challenges facing Canada’s economy, even as wage growth suggests some resilience. For now, traders will keep their eyes on both US and Canadian economic releases, knowing that central bank decisions in the coming months could shape the trajectory of the CAD well into year-end.

AUDUSD Gains Momentum with Fed Rate Talk, Traders Await RBA Move

The Australian Dollar has been making a steady climb against the US Dollar, with recent moves driven by shifting interest rate expectations and a softer outlook for the US economy. Investors are closely watching both the Reserve Bank of Australia (RBA) and the US Federal Reserve as their upcoming policy decisions could shape the currency’s next big move.

A Weaker US Dollar Gives AUD a Boost

Over the past few days, the US Dollar has struggled to maintain its strength. Softer labor market data and signs of slowing economic growth in the United States have fueled speculation that the Federal Reserve may begin cutting interest rates as soon as September.

AUDUSD is moving in an Ascending channel, and the market has rebounded from the higher low area of the channel

When the US economy shows signs of cooling, investors often reassess the value of holding US Dollar positions. Lower interest rates make the currency less attractive to global investors, and this can open the door for other currencies – like the Australian Dollar – to gain ground. That’s exactly what we’ve seen recently, as AUD/USD has risen steadily and looks set to end the week with solid gains.

RBA’s August Decision: A Key Moment for AUD

The spotlight is now on the Reserve Bank of Australia’s upcoming policy meeting. Markets are widely expecting the RBA to cut interest rates by 25 basis points in August. If that happens, Australia’s cash rate will drop to 3.60%, a move aimed at supporting growth amid easing inflation and a slightly softer job market.

Why Markets Expect More Cuts

Australia’s inflation, as measured by the trimmed mean CPI, has eased to 2.7%, signaling that price pressures are cooling. Meanwhile, the unemployment rate has edged up to 4.3%, suggesting the labor market is losing some of its previous tightness. These conditions give the RBA more room to lower borrowing costs without risking a surge in inflation.

Major Australian banks – including ANZ, CBA, NAB, and Westpac – are on the same page. They forecast the cash rate could fall further by the end of the year, with most expecting it to reach around 3.35%. Some analysts even believe cuts could continue into 2026 if global economic challenges persist.

Global Risks Could Influence RBA’s Tone

While a rate cut in August is almost certain, traders are paying close attention to how the RBA communicates its future plans. Central banks tend to guide markets by signaling whether more policy easing is on the way or if they are ready to pause.

RBA Governor Michele Bullock has already pointed to external risks, including ongoing trade tensions between the United States and China. Australia, being a trade-reliant economy, is sensitive to changes in global demand and commodity flows. Any renewed tariffs or trade restrictions could disrupt exports, impact business confidence, and add uncertainty to the economic outlook.

US-China Trade Talks: A Wild Card for Markets

Beyond central bank decisions, international trade developments are another factor influencing AUD/USD. The United States and China are in talks to extend their current tariff truce, which is set to expire in mid-August. Early reports suggest progress is being made, with both sides showing cautious optimism.

If an agreement is reached, it could boost global trade sentiment and support risk-sensitive currencies like the Australian Dollar. However, if negotiations fall apart, markets could quickly shift to risk-off mode, strengthening the US Dollar and putting pressure on AUD/USD.

The Week Ahead: High-Impact Data and Events

The next week could be one of the most eventful for AUD/USD traders in months. Several key releases and decisions are lined up:

For Australia:

-

RBA Interest Rate Decision – Likely to cut rates, but the focus will be on the RBA’s statement for hints about future moves.

-

Labor Market Data – Employment and unemployment numbers will provide fresh insight into the health of the job market.

-

Wage Price Index (Q2) – A key gauge of wage growth, which could influence the RBA’s inflation outlook.

For the United States:

-

Consumer Price Index (CPI) – A closely watched measure of inflation that could confirm or challenge expectations of a September Fed rate cut.

-

Producer Price Index (PPI) – Another inflation measure, often viewed as a leading indicator for consumer prices.

-

Retail Sales Data – Will show whether US consumers are still spending despite higher borrowing costs.

-

Michigan Consumer Sentiment Index (Preliminary) – A snapshot of household confidence that can affect economic forecasts.

AUDUSD is rebounding from the major support area

With both countries set to release important economic data, volatility in AUD/USD is likely to increase. Traders will be watching every headline, especially anything related to central bank policy or trade talks.

Final Summary

The Australian Dollar has been on a winning streak against the US Dollar, fueled by a combination of a weaker Greenback and growing expectations of interest rate cuts in both Australia and the United States. The RBA’s upcoming decision is front and center, with markets almost fully pricing in a rate cut, and many analysts expecting more by year-end.

At the same time, the Fed’s September decision is hanging in the balance, with US economic data and inflation reports likely to be decisive. Adding to the mix are US-China trade negotiations, which could either support risk appetite or trigger market uncertainty.

For traders and investors, the coming days offer plenty of opportunities – but also heightened risks. With major data releases and central bank meetings on the horizon, AUD/USD could see sharp swings in either direction, making it a pair to watch very closely in the week ahead.

EURGBP Gains Footing After BoE Rate Move Highlights Policy Split with ECB

The EUR/GBP currency pair has recently shown a bounce after slipping to its lowest point in a week. This rebound has caught the attention of traders, not only because of the price movement but also because of the broader backdrop of changing monetary policies in the UK and the Eurozone. The situation highlights how economic decisions, central bank strategies, and political uncertainties can shape currency market trends.

EURGBP is moving in a descending channel, and the market has reached the lower low area of the channel

A Quick Look at What Happened This Week

The week began with the EUR/GBP pair facing downward pressure, but it found some stability by Friday. The rebound came after a volatile period that followed the Bank of England’s latest interest rate decision.

On Thursday, the Bank of England (BoE) decided to lower its benchmark interest rate by 25 basis points to 4.00%. While the move was widely expected, the decision was far from unanimous. The 5–4 voting split among policymakers revealed that the bank is divided on how quickly to ease monetary conditions.

Interestingly, despite the cut, the BoE’s tone wasn’t overly dovish. Many analysts described the decision as a “hawkish rate cut” because of the cautious language that accompanied it. This suggests the central bank isn’t rushing into an aggressive easing cycle, given the uncertainty around inflation trends and economic growth.

Why the BoE Is Being So Cautious

The Dissenting View from the BoE

Chief Economist Huw Pill, who voted against the rate cut, has been vocal about his concerns. He warned that the recent pace of interest rate reductions might not be sustainable. His argument is that inflation risks could rise again, especially if the labor market and wage growth remain resilient. In his view, cutting rates too quickly could undo the progress made in controlling inflation.

Pill also pointed out that while inflation is slowly easing and the labor market is showing signs of cooling, there are still risks coming from external shocks. These include higher import prices and potential disruptions to global supply chains. Such shocks, if prolonged, could spill over into domestic inflation, making it more persistent and harder to control.

A Narrow Window for More Cuts

Pill emphasized that the UK economy is still operating under restrictive monetary conditions. The central bank believes that interest rates are now within the 2% to 4% “neutral range” where they neither stimulate nor slow the economy significantly. However, the scope for further cuts might be limited if inflationary pressures pick up again.

Governor Andrew Bailey also struck a note of caution, stating there is now “genuine uncertainty” about the future direction of interest rates. This uncertainty underscores the BoE’s focus on taking a data-driven approach to future policy changes rather than committing to a fixed path.

The ECB Takes a Different Approach

While the BoE is cautiously trimming rates, the European Central Bank (ECB) has taken a different stance. At its most recent policy meeting, the ECB decided to keep its key interest rates unchanged. This decision reflects its belief that inflation in the euro area is moving closer to the 2% target and that no immediate action is necessary.

Why the ECB Is Standing Still

ECB policymakers remain mindful of economic headwinds facing the Eurozone. Factors like trade tensions, uncertainty in global markets, and potential US tariffs on European goods all pose risks to growth. For now, the ECB prefers to wait and see how the economy responds before adjusting rates again.

The ECB has also been clear about its approach: it will make decisions “meeting-by-meeting” and remain highly dependent on incoming data. This flexibility allows it to adapt quickly if conditions change. Some economists believe that the ECB might already be at the end of its easing cycle, while others think there could still be room for future cuts if the economy weakens further.

What This Means for EUR/GBP Going Forward

The diverging strategies between the BoE and ECB are a major factor shaping the EUR/GBP outlook.

-

If the BoE continues to cut rates cautiously while the ECB stays on hold, the pound may face periods of weakness against the euro.

-

If UK inflation pressures re-emerge and the BoE slows or pauses its rate cuts, the pound could find stronger support.

-

If the Eurozone economy shows resilience and the ECB delays easing further, the euro might maintain an upper hand in the medium term.

EURGBP is moving in a descending triangle pattern, and the market has reached the lower high area of the pattern

For traders and investors, this means paying close attention not only to inflation data and economic growth figures from both regions but also to the tone of statements from central bank officials.

Final Summary

The recent rebound in EUR/GBP isn’t just about short-term market sentiment—it reflects a broader story about two major central banks navigating uncertain economic waters in different ways. The Bank of England has started a cautious rate-cutting cycle, but divisions among policymakers and concerns about inflation are likely to keep future moves measured. In contrast, the European Central Bank is opting for a wait-and-see strategy, holding rates steady as it monitors inflation and economic performance across the Eurozone.

This divergence is creating a dynamic backdrop for the EUR/GBP pair, where shifts in policy tone, economic data, and global developments could quickly alter the balance. For now, both the pound and the euro are being shaped by a mix of caution, uncertainty, and the constant challenge of balancing growth with price stability.

BTCUSD Eyes Bigger Gains After Trump Backs Crypto in U.S. Retirement Funds

Bitcoin had an exciting week, closing strongly and catching the attention of both investors and policymakers. Momentum picked up after the announcement of new U.S. government measures that could make cryptocurrency more accessible to everyday retirement savers. At the same time, global developments in Asia, particularly from Japan and China, added even more fuel to the growing optimism around digital assets.

This combination of policy shifts, institutional interest, and international demand signals that the crypto market is entering a new chapter—one where Bitcoin is becoming increasingly recognized as a serious asset class.

BTCUSD is moving in a descending channel, and the market has reached the lower high area of the channel

Trump’s Executive Order Shakes Things Up

One of the biggest headlines came from Washington. U.S. President Donald Trump signed an executive order allowing cryptocurrency, private equity, and real estate to be included in 401(k) retirement plans. This means that, for the first time, Americans could potentially diversify their retirement portfolios with digital assets alongside traditional investments like stocks and bonds.

Why This Matters

For years, crypto advocates have argued that retirement accounts should be able to include digital currencies, offering savers more choice and potentially higher returns. This move could open the doors for millions of Americans to gain exposure to Bitcoin without having to directly buy and store it themselves.

While some critics have raised concerns about the risks of including volatile assets in retirement funds, supporters see this as a groundbreaking step toward mainstream adoption. The order also covers other non-traditional investments such as precious metals and private loans, signaling a broader push toward diversification in retirement savings.

Global Demand for Stablecoins is Rising

Another major storyline is coming from Asia, where demand for stablecoins is increasing—especially in China. According to reports, China is preparing to launch its first stablecoins as part of a larger plan to promote the international use of the Renminbi (CNY) and reduce reliance on the U.S. Dollar in global trade.

Hong Kong as a Crypto Gateway

Hong Kong has become the testing ground for these developments. While mainland China has strict bans on cryptocurrency trading, Hong Kong’s new regulatory framework for stablecoins is giving global companies a chance to experiment with digital currency adoption in the region.

Interestingly, this move comes shortly after Trump introduced the first U.S. regulatory framework for stablecoins, known as the GENIUS Act. With both the U.S. and China making regulatory moves around stablecoins, the global competition for digital currency influence is heating up. Stablecoins often act as an entry point into the crypto market, meaning increased demand could indirectly boost Bitcoin adoption.

Rate Cuts Could Boost Risk Assets

Even though Bitcoin’s price didn’t see major swings earlier in the week, there’s growing belief that the U.S. Federal Reserve will cut interest rates in September. Analysts expect at least two rate cuts before the end of the year. Lower interest rates generally make riskier assets—like Bitcoin—more attractive to investors searching for higher returns.

This macroeconomic backdrop could play an important role in driving more capital into crypto markets, especially if investors anticipate a weaker U.S. Dollar and a friendlier financial environment for alternative assets.

Trade Tensions Add to Market Uncertainty

Trade policies are also influencing market sentiment. Trump announced fresh tariffs on Indian imports as a response to the country’s oil purchases from Russia, raising total tariffs to 50%. He also revealed that new tariffs on semiconductors and pharmaceuticals would be implemented soon.

These kinds of trade tensions often push investors toward assets perceived as hedges against global uncertainty—such as gold and, increasingly, Bitcoin.

SBI Holdings Pushes for a Crypto ETF

Japan’s SBI Holdings made headlines by filing for a dual-asset cryptocurrency Exchange Traded Fund (ETF) that would include Bitcoin (BTC) and Ripple’s XRP. If approved, this ETF would give investors in Japan a regulated way to gain exposure to two major cryptocurrencies without directly purchasing them.

Potential Long-Term Impact

ETFs can significantly boost mainstream adoption by simplifying the investment process. For Bitcoin, this could mean a steady inflow of institutional and retail money, potentially supporting long-term growth. The fact that this ETF would also include XRP suggests that SBI Holdings is betting on diversification within the crypto market.

Regulatory Clarity on Staking

Adding to the positive news flow, the U.S. Securities and Exchange Commission (SEC) clarified that liquid staking activities in crypto do not count as securities offerings. This is a significant step toward clearer digital asset regulation, which many in the industry believe is necessary for continued growth.

BTCUSD is moving in an uptrend channel, and the market has reached a higher high area of the channel

SEC Chair Paul Atkins emphasized the agency’s commitment to offering more straightforward guidance on how federal securities laws apply to cryptocurrency. This could reduce legal uncertainty for crypto businesses and encourage more institutional participation.

Final Summary

This week showcased how policy changes, international developments, and regulatory clarity can combine to create a strong narrative for Bitcoin and the broader crypto market. From Trump’s groundbreaking move to allow cryptocurrencies in retirement accounts, to China’s stablecoin ambitions, to Japan’s push for a dual-asset ETF, the signs of growing acceptance are clear.

While challenges remain—from potential market volatility to ongoing trade disputes—the overall trend is one of increasing integration of digital assets into the global financial system. Whether you’re a casual observer or a dedicated investor, the past week has made one thing clear: cryptocurrency is no longer on the sidelines—it’s steadily moving into the mainstream.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!