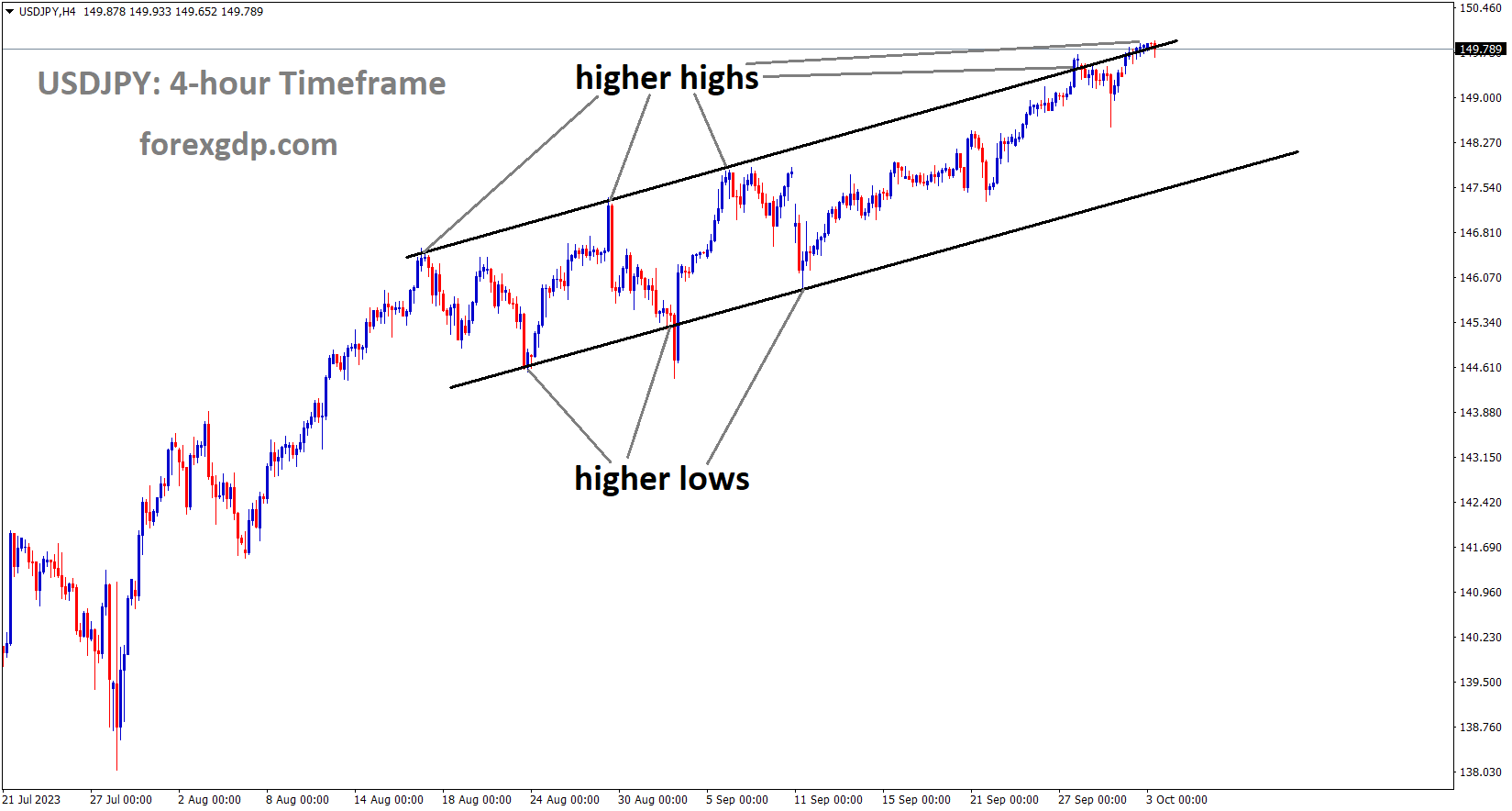

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher high area of the channel

Today, the minutes of the BoJ Meeting were discussed in order to remove negative rates from the table. Only after inflation and wage prices have reached their targets are changes in monetary policy discussed. Importing prices put pressure on the Bank of Japan to change the table’s negative rates.

The BoJ minutes, which included a discussion about exiting negative interest rates, were released in the early hours of this morning. One board member expressed concerns about the major policy change from a risk management standpoint, stating that the Bank of Japan may have enough data on hand to make a decision on negative rates in the first quarter of next year. The prospect of exiting negative interest rates pushed 10-year Japanese government bond yields higher, necessitating unplanned bond purchases from the bank. Bond yields have previously served as a release valve for a period of above-target inflation and rising wages, two key determinants of the historic policy shift. The 10-year yield is now permitted to rise steadily above 0.5%, with an upside limit thought to be around 1%.

At the start of this week, the counter-trend move from the end of last week has already been clawed back. The US dollar has continued to rise as a result of rising US yields, and the pair is now testing a level that could force Tokyo’s hand. For weeks, Japanese officials have been warning markets about potentially harmful speculative FX moves. However, we have not seen the same level of volatility as in 2022, when Japan intervened in the forex market to defend the yen’s value. Nonetheless, higher import costs are being passed on to consumers, contributing to overall price pressures.

Gold Analysis

XAUUSD Gold price has broken the Descending triangle pattern in downside.

Following the last-minute resolution of the US government shutdown issue and the passage of the funding bill, gold prices have decreased. The American economy is doing well, and US FED members are in favour of potential rate increases this year.

The gold price has been trending lower over the last two weeks or so, following the Federal Reserve’s announcement that sticky inflation was likely to attract at least one more rate hike in 2023. Furthermore, several Fed officials backed the case for keeping rates low for longer in order to achieve the 2% inflation target. In addition, the incoming resilient macro data from the United States (US) supports the Fed’s prospects for further policy tightening. This, in turn, keeps US Treasury bond yields elevated, pushing the US Dollar (USD) to its highest level since November 2022 and driving flows away from the non-yielding yellow metal.

The selling pressure continues unabated on Tuesday, dragging the gold price to its lowest level since March 9 during the Asian session. However, a sea of red in global equity markets helps the safe-haven precious metal find some support near the $1,815 level and recover a large portion of its intraday losses despite extremely oversold conditions on the daily chart. Any further recovery, however, appears elusive in light of hawkish Fed expectations and a strong USD. Furthermore, the lack of any meaningful buying suggests that the Gold’s path of least resistance is to the downside, and any subsequent move up is likely to attract new sellers.

Silver Analysis

XAGUSD Silver price is moving in an Ascending channel and the market has reached the higher low area of the channel.

The United States has warned China that Advanced AI Chips and Semiconductors exports to China will be restricted beginning in October. This restriction is primarily intended to compensate for China’s military weakness and to support Russia in the Ukraine war by supplying weapons in secret.

According to Reuters, the Biden administration has warned China that additional export restrictions on AI chips and chipmaking tools to China are set to take effect early this month. This would be an update around the one-year anniversary of the measures’ initial unveiling on October 7, 2022. The restrictions announced in October aimed to prevent US technology from being used to strengthen the Chinese military by restricting China’s access to advanced AI chips and imports of the most advanced chipmaking tools from the US.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has reached the higher high area of the channel

Swiss CPI inflation was 1.7% in September, down from 1.6% the previous month and lower than the 1.8% expected. The Swiss Franc fell against the US Dollar as a result of negative data.

During the early European session on Tuesday, the USD/CHF pair gains traction above 0.9200. The pair’s rise is aided by stronger US data and weaker-than-expected Swiss inflation data. The latest data from the Swiss Federal Statistical Office revealed on Tuesday that the country’s Consumer Price Index (CPI) for September came in at 1.7% YoY, down from 1.6% the previous month and below the 1.8% expected. On a monthly basis, inflation fell to 0.1%% from 0.2% the previous month, falling short of the market consensus of 0%. As a result of the negative data, the Swiss Franc (CHF) loses ground against the US Dollar. In terms of the US dollar, business conditions in the US manufacturing sector continued to deteriorate in September.

The US ISM Manufacturing PMI was 49.0 in September, up from 47.6 the previous month and above the market consensus of 47.7. In addition, the Prices Paid Index fell from 48.4 to 43.8. The Employment Index increased from 48.4 to 51.2 points. Finally, the New Orders Index climbed from 46.8 to 49.2 points. Loretta Mester, President of the Federal Reserve Bank of Cleveland, stated earlier on Tuesday that the Fed will most likely need to raise interest rates again this year, and that the Fed’s monetary policy path will be determined by how the economy performs. Furthermore, Fed Governor Michelle Bowman stated on Monday that it is likely that the policy rate will need to be raised further and maintained at restrictive levels for an extended period of time. However, the higher-for-longer rate narrative in the United States strengthens the Greenback and acts as a tailwind for the USDCHF pair. Traders are looking forward to the August US JOLTS Job Openings, which are due on Tuesday. Later this week, the focus will shift to US employment data, including the US ADP report on Thursday and the US Nonfarm Payrolls, Average Hourly Earnings, and Unemployment Rate on Friday. Traders will use these figures to identify trading opportunities in the USD/CHF pair.

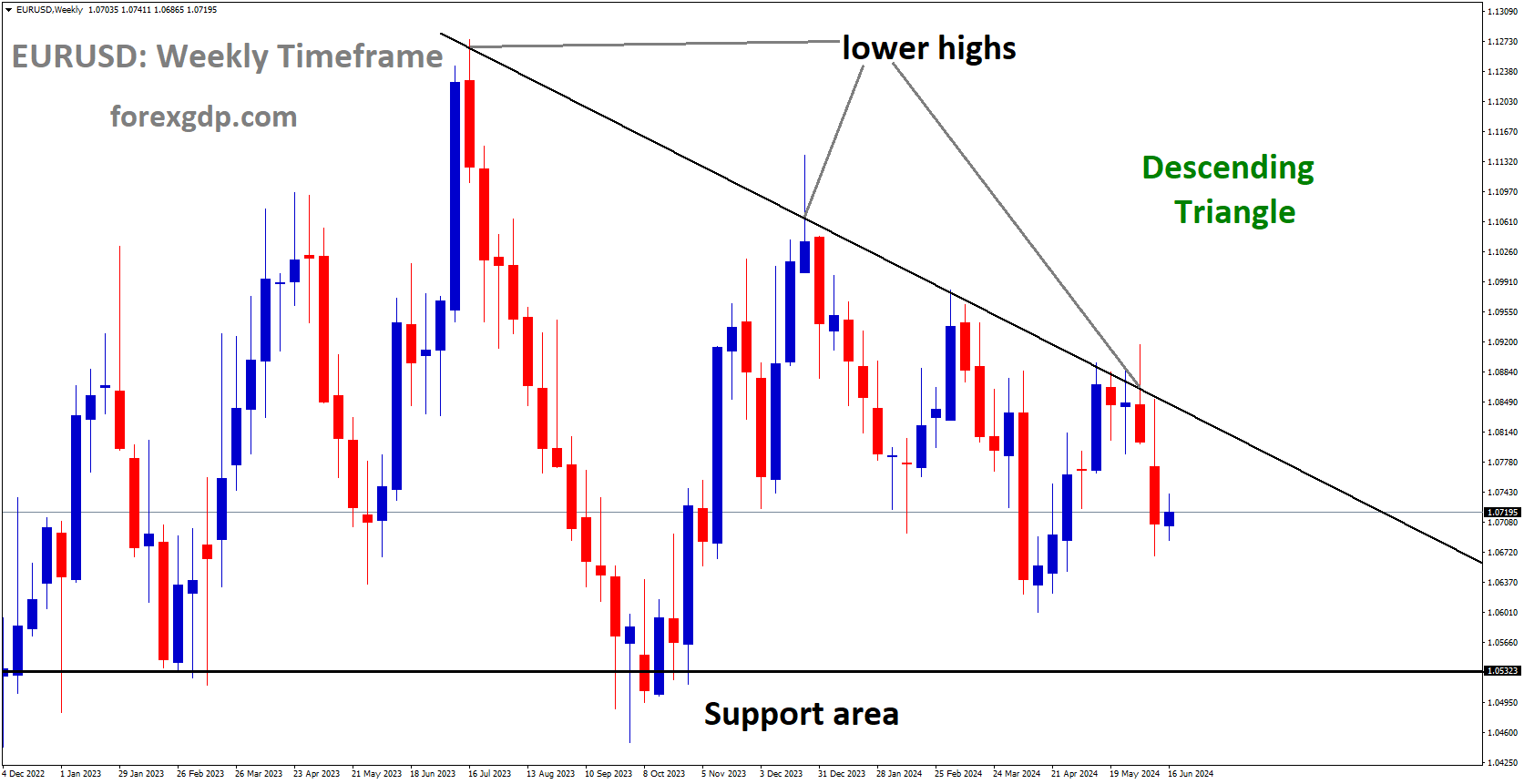

EURUSD Analysis

EURUSD is moving in the Box pattern and the market has reached the support area of the pattern

Loretta Mester, president of the Federal Reserve Bank of Cleveland, stated that there will be one more rate hike this year to combat inflation and slow wage growth. The economy is holding up well, and job growth is slowing but not at a rapid pace.

Reuters reports that Federal Reserve Bank of Cleveland President Loretta Mester will discuss her economic outlook on Monday. The state of the economy dictates the course of monetary policy. It is likely that the Fed will have to raise rates once more this year. The economy is “on the right track” as supply and demand continue to balance.

Though robust, the job market is slowing down and improving in balance. Despite “too high” inflation, there are encouraging signs that price pressures are being reduced. For inflation to return to 2%, the Fed will need to maintain high interest rates. The economy has expanded faster than anticipated. The risks associated with inflation were positive. The tightening of credit conditions is consistent with monetary policy. There are indications that the pressure on wages is lessening.

EURCHF Analysis

EURCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel

According to ECB Chief Economist Philip Lane, achieving the 2% inflation target will take time; however, by hiking interest rates, the goal can be reached in two years. There will be pressure from service inflation on all industries, and wage prices will rise for at least two years.

Philip Lane, Chief Economist at the European Central Bank , offered some insights on the bloc’s inflation outlook. The transition from 4% to 2% inflation will not happen as quickly. Today, inflation in services plays a significant role. Food inflation remains a significant problem. We do not think the low petrol prices we currently have will last. Services and the energy sector are closely related. More work needs to be done because we have not yet reached the inflation target. Domestic inflation demonstrates that wage pressure is still present. We still have two years remaining of relatively high wage increases.

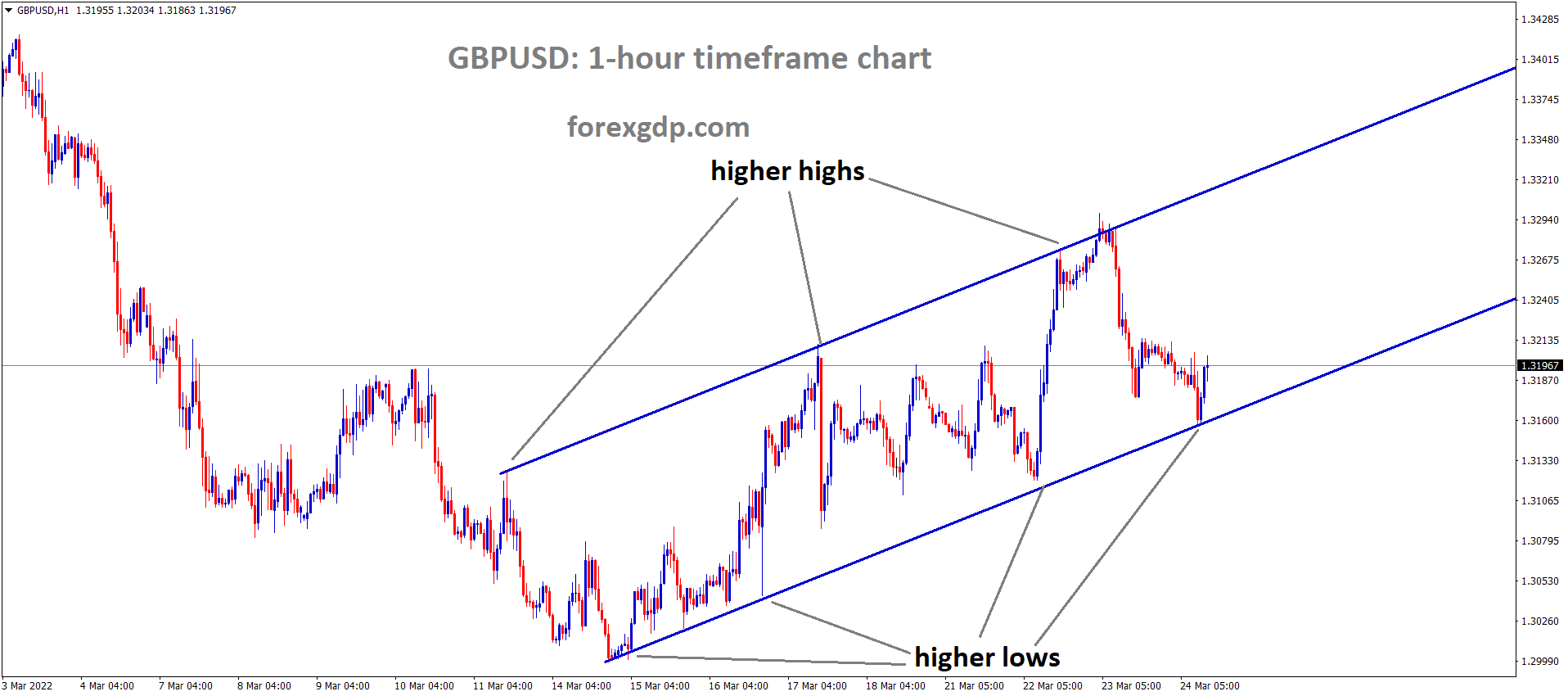

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lowered low area of the channel

The Bank of England stopped raising interest rates in September of last year, which caused the GBP to fall against counter pairs. With the GDP projection for July through September down by 0.10% to 0.40%, more disappointment for the GBP is anticipated.

The GBPUSD pair is seen oscillating in a narrow trading band below 1.2100, consolidating recent losses to the lowest level since March 16, which was reached during the Asian session on Tuesday. Bearish traders are hesitant to place new bets because the daily chart is extremely oversold, even though the fundamental backdrop suggests that the path of least resistance for spot prices is to the downside. The British Pound GBP has continued to underperform in the aftermath of the Bank of England’s BoE surprise decision to pause its rat-hiking cycle in September. The Bank of England did not raise interest rates for the first time since December 2021. In addition, the UK central bank reduced its forecast for economic growth in the July-September period to 0.1% from 0.4% previously, and gave no indication of its intention to raise rates further. This, combined with the underlying strong bullish sentiment surrounding the US Dollar USD, works against the GBPUSD pair. The USD Index DXY, which measures the value of the US dollar against a basket of currencies, rises to its highest level since November 2022, buoyed by growing confidence that the Federal Reserve Fed will maintain its hawkish stance. Indeed, the markets have priced in at least one more rate hike by the end of the year. In addition, Cleveland Fed President Loretta Meste stated that the US central bank will need to keep interest rates restrictive in order to return inflation to the 2% target. As a result, US Treasury bond yields have reached a new multi-decade high, supporting the USD.

Aside from the Fed’s higher-for-longer narrative, a generally weaker risk tone is seen as another factor benefiting the Greenback’s relative safe-haven status and weighing on the GBPUSD pair. The market’s initial reaction to the mixed Chinese PMIs and the passage of a US stopgap funding bill over the weekend was short-lived due to concerns about economic headwinds caused by rapidly rising borrowing costs. This continues to drive investors to traditional safe-haven assets and favours USD bulls, validating the major’s near-term negative outlook. Moving forward, there is no relevant market-moving economic data from the UK due for release, leaving the GBPUSD pair at the mercy of USD price dynamics. Traders will take cues from the US JOLTS Job Openings data later in the early North American session. This, along with US bond yields and broader risk sentiment, will influence and provide some impetus to the USD price dynamics. However, the focus will remain on the US NFP report, which is due on Friday.

CADHF Analysis

CADCHF has broken the Ascending channel in downside

The Canadian economy slowed following a 0.20% drop in GDP. Manufacturing activity fell for the first time in two years in June. The Bank of Canada prefers to keep interest rates unchanged until the end of the year. As the US dollar rises, Canadian Dollar weakness persists in the market.

The growing expectations that the Bank of Canada (BoC) will stop raising interest rates are weighing down the value of the Canadian dollar (1CAD). According to a Statistics Canada report released on Friday, the manufacturing sector saw its largest decline in over two years in July, which caused the country’s economic growth to stall.

This follows a 0.2% GDP decline in June, which stoked expectations that the BoC would maintain interest rate stability in spite of persistently high inflation. This compounds with a further decline in the price of crude oil, undermining the “Loonie” linked to commodities.

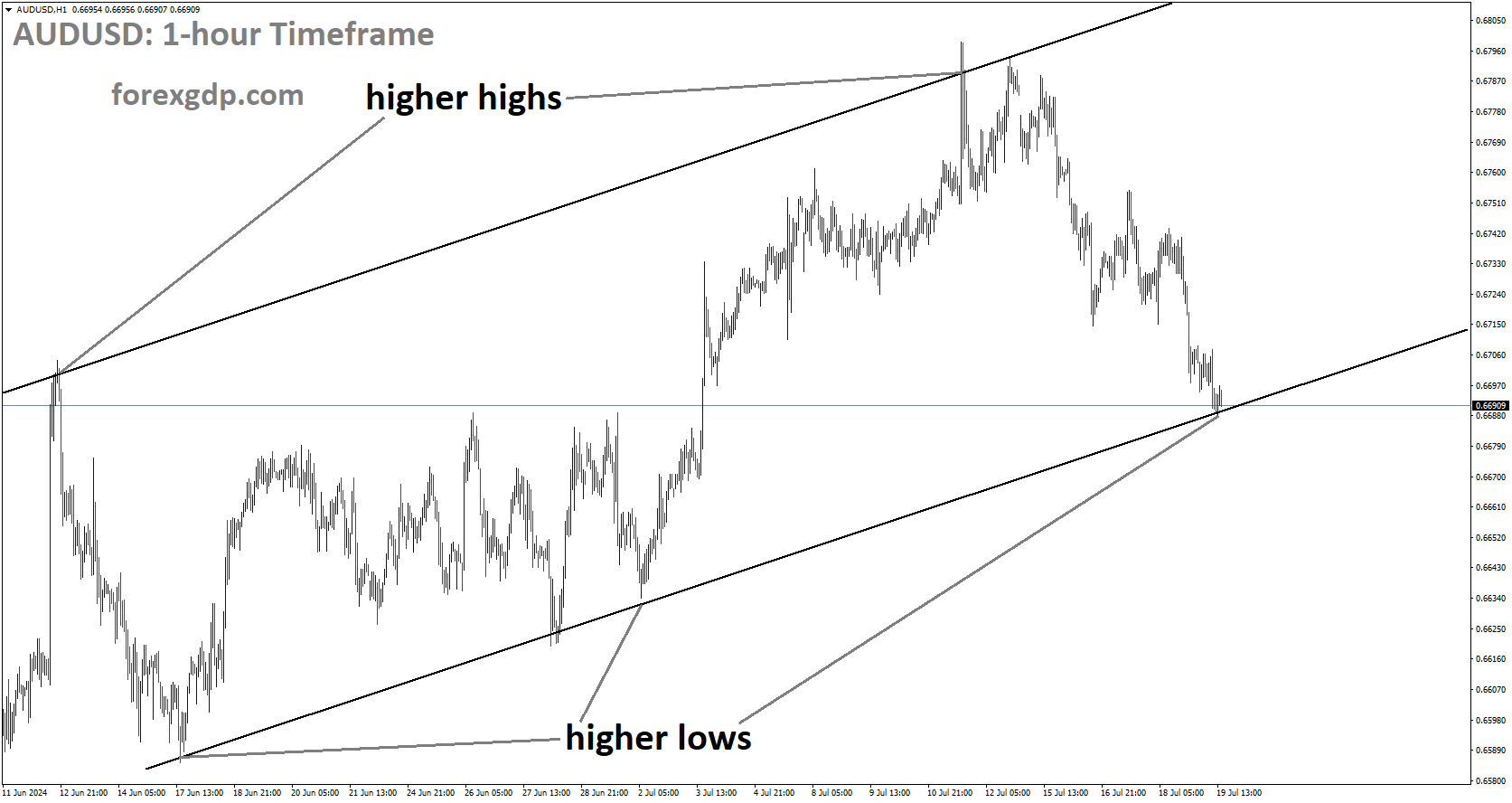

AUDUSD Analysis

AUDUSD has broken the Box pattern in downside

Because of growing inflation and a robust labour market, the RBA has maintained interest rates at 4.10% for the fourth consecutive month. While the RBA projected a 2-3% inflation target in 2025, the August inflation reading increased by 5.2%. We anticipate one more rate increase by year’s end or early in 2024.

Following the Reserve Bank of Australia’s (RBA) decision to maintain benchmark interest rates unchanged in line with market expectations, the Australian dollar held onto its early losses. The RBA maintained the benchmark rate at 4.1% for the fourth consecutive month, but acknowledged that given the persistently high rate of inflation and the robust labour market, additional monetary policy tightening might be necessary. The central bank upheld its central projection that, by late 2025, inflation would have returned to the target range of 2-3%. In August, Australia’s CPI increased to 5.2% year over year, well above the central bank’s target range of 2-3%. The RBA’s inflation forecast is at risk from the recent sharp increase in oil prices, which also maintains the possibility of one more rate hike this cycle. The markets are factoring in one more rate increase from the RBA early in 2019 and then generally stable rates starting in 2024.

Concurrently, there are some indications that China’s manufacturing sector may be bottoming out; in September, factory activity increased for the first time in six months. This comes after a flurry of other indicators in August that suggested the second-largest economy in the world’s economic growth may be bottoming out, including retail sales and an easing of deflationary pressures. For Australia, any improvement in China’s growth prospects could be encouraging. In addition, the US Congress made a last-minute agreement to save the AUD by averting a partial government shutdown. But even with US yields rising due to a view that US rates should remain higher for longer, overall risk appetite has stayed in check. On Monday, Federal Reserve Governor Michelle Bowman reaffirmed the position, stating that should new data indicate that inflation is either too slowly increasing or has stalled, she would still be willing to support raising the policy rate at a later meeting.

NZDUSD Analysis

NZDUSD is moving in the Box pattern and the market has reached the support area of the pattern

In relation to counter pairs, NZD pairs are slowing down ahead of the RBNZ interest rate decision. The previous month’s 63% decline in business confidence was followed by a 52% decline in the NZ report.

A higher US Treasury yield contributes to the strengthening of the greenback. The United States avoided a partial government shutdown, which caused the yield on the 10-year US Treasury to rise above its highest level since 2007. As of this writing, the spot price is 4.68%. The positive sentiment surrounding the US dollar is also being strengthened by the market’s caution regarding the US Federal Reserve’s (Fed) interest rate trajectory. In addition, the mixed US data that was made public on Monday supported the US dollar. The US ISM Manufacturing PMI increased to 49.0 in September from 47.6 in August, surpassing the 47.7 market estimate.Manufacturing Prices Paid dropped from 48.4 to 43.8, a significant decline. The Employment Index increased to 51.2 from 48.4. Governor of the Federal Reserve , Michelle Bowman, stated on Monday that she believed it was appropriate to raise the policy rate again and keep it at a restrictive level for a longer period of time. On the other hand, Fed Vice Chair for Supervision Michael Barr emphasised a prudent monetary policy stance. The significance of taking the trajectory of interest rates into account. And is nevertheless confident that the Fed can control inflation without seriously impairing the labour market.

is scheduled to make its interest rate announcement")

With the release of the ADP report on Wednesday and the Nonfarm Payrolls on Friday, traders are anticipating the release of US employment data. The Reserve Bank of New Zealand (RBNZ) is scheduled to make its interest rate announcement on Wednesday. The market expects the RBNZ to keep interest rates where they are, at 5.50%. Trader attention will be focused on the accompanying statement, though, in case there are any hints of a future rate hike that might contain the downside risk for the Kiwi pair. The third-quarter business outlook was released by the New Zealand Institute of Economic Research. Data from NZIER Business Confidence showed a 52% decline, an improvement over the previous 63% decline.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/