The CIPLA company acquiring Ivia Beaute cosmetics company for distribution and selling health care products in India and World wide. Cost of Acquisition is Rs.130 cr for Cipla and will take over fully by May month 2024.

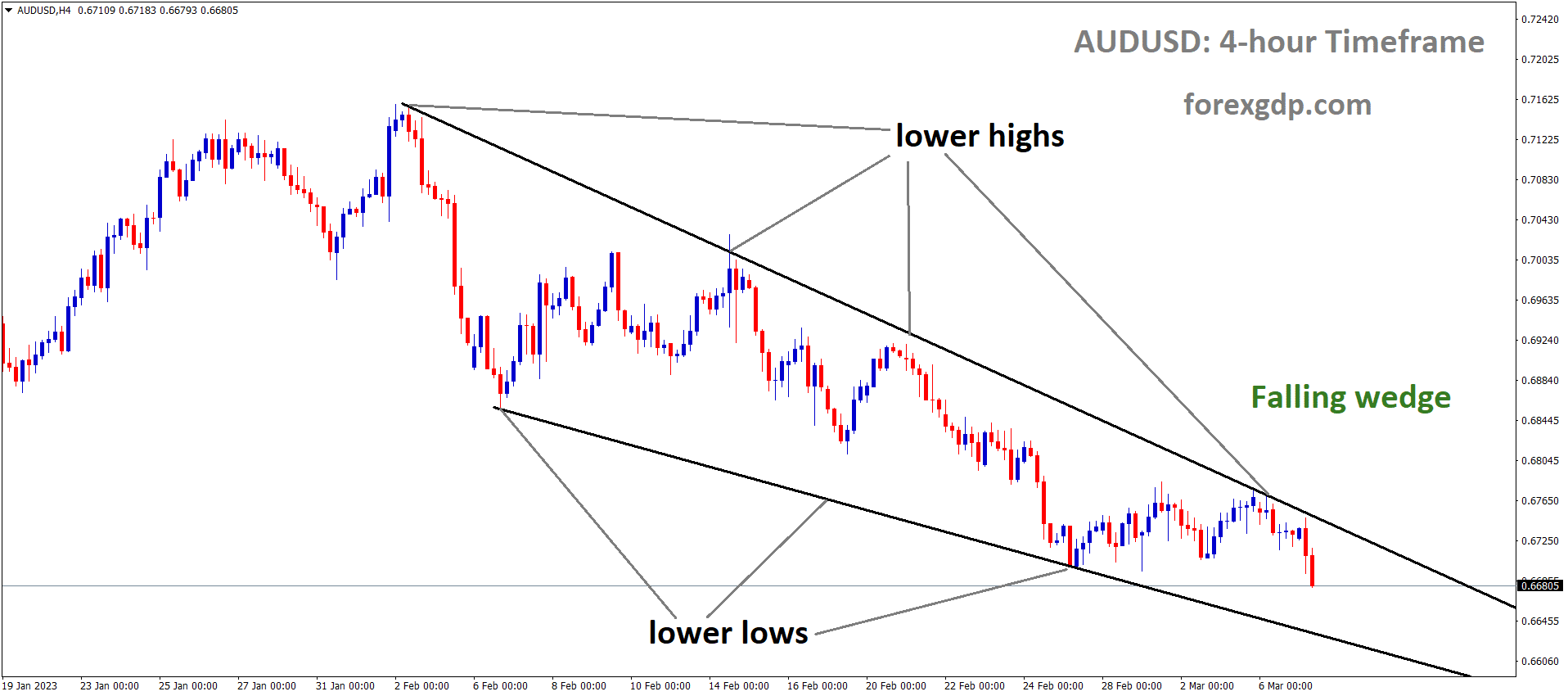

CIPLA Market Price is moving in Ascending channel and market has reached higher low area of the channel

On April 16, the share price of Cipla remained stable in early trading following the announcement of the company’s plan to acquire a business undertaking from Ivia Beaute Private Limited.

Cipla Health Limited India, a wholly owned subsidiary of Cipla, entered into a business transfer agreement (BTA) to acquire the distribution and marketing business undertaking of cosmetics and personal care products from Ivia Beaute Private Limited India. The agreement involved a slump sale arrangement on a going concern basis.

The acquisition encompasses Ivia’s brands, including Astaberry, Ikin, and Bhimsaini, on a global scale.

The transaction is anticipated to be finalized within 60 days from the signing of the BTA, subject to the successful completion or waiver of the conditions precedent and closing conditions outlined in the agreement.

This strategic move is expected to bolster Cipla Health Limited’s (CHL) consumer healthcare and wellness portfolio. The addition of Ivia’s brands is seen as complementary to CHL’s existing offerings in the skincare segment, enriching the portfolio with trusted and effective solutions for consumers.

The acquisition cost amounts to Rs 130 crore upon closing, with an additional Rs 110 crore contingent upon the achievement of specified financial milestones over the next three years, as stipulated in the BTA.

Furthermore, a meeting of the board of directors of Cipla is scheduled for May 10, 2024, to review and approve the standalone and consolidated audited financial results for the quarter and fiscal year ended March 31, 2024. The board will also consider recommending any final dividend for the fiscal year ended March 31, 2024, if applicable.

NIFTY: Sensex, Nifty Decline for Third Day; Bond Yields, Israel-Iran Tensions Impact Sentiment

The NIFTY and Sensex fall down for the third straight day on yesterday due to Geopolitical tensions between Iran and Israel. US Government Bond Yields are surged after the fears sustained in the market. Israel military officer said Iran will get retailiation on Israel Attack on Sunday.

Nifty 50 Index Market Price is moving in Ascending channel and market has reached higher low area of the channel

The decline in both the Sensex and the Nifty persisted for the third consecutive day as investors evaluated the repercussions of escalating tensions in West Asia. Additionally, the surge in US treasury bond yields, reaching a five-month high, further dampened investor sentiment.

Analysts cautioned investors to exercise prudence and monitor the unfolding developments closely.

The Sensex recorded a decline of 334.28 points, or 0.46 percent, settling at 73,065.50, while the Nifty experienced a drop of 86.50 points, or 0.39 percent, closing at 22,186.00. Despite this, the market breadth favored gainers, with approximately 1,811 shares advancing, 851 declining, and 107 remaining unchanged.

The escalating bond yields diminish the likelihood of rate cuts by the US Federal Reserve this year, as highlighted by VK Vijayakumar, Chief Investment Strategist at Geojit Financial Services. Elevated bond yields are typically unfavorable for riskier assets like equities and could accelerate selling by Foreign Institutional Investors (FIIs) in emerging markets such as India.

The recent statement by the Israeli military chief, indicating a forthcoming response to Iran’s attack on Israel, has heightened the probability of heightened tensions in the already volatile region. The uncertainty surrounding the timing and nature of Israel’s response is anticipated to keep the markets under pressure in the near term, according to Vijayakumar.

Vaishali Parekh, Senior Vice-President of Technical Research at Prabhudas Lilladher, identified the 22,000 level as a strong support zone for the Nifty amidst a weakening positive bias due to Middle-East tensions. She suggested that the support level for the day is projected at 22,100, with resistance forecasted at 22,400.

Despite the challenging market conditions, the broader markets outperformed benchmarks in the initial hours of trading, with the BSE Midcap and BSE Smallcap indices surging up to 0.7 percent on April 16. Furthermore, the fear gauge, India VIX, marginally eased to 12.46.

In sectoral performance, the Nifty IT and Nifty Realty indices were the worst performers, while the Nifty Auto and Nifty Metal indices saw marginal gains, rising up to 0.4 percent on April 16 morning.

Given the rising geopolitical tensions, strengthening dollar, and higher bond yields, the domestic currency opened at a record low against the US dollar on April 16. The rupee began trading at 83.51 against the dollar, down by 6 paise from the previous close of 83.45.

From an investment standpoint, Vijayakumar recommended accumulating quality large-cap stocks for the long term, particularly in sectors such as banking, IT, autos, capital goods, oil & gas, and cement, as further corrections may render valuations of large-caps more reasonable.

Bharati Hexacom: Jefferies: Bharti Hexacom Stock Target Price Doubles in a Year for IPO Investors

The Bharati Hexacom driving 16% CAGR revenue in this year, compounded CAGR will be 21% for FY 24-27, then it reduced the capitial expenditure in few years, then the CAGR will be 41% in the next five years as per Jefferies forecasted this company. The Bharati Hexacom focussing on structural wireless users in India. So Future of Wireless is the gain for this company.

BHARATI HEXACOM Market Price is moving in Ascending trend line and market has rebounded from the higher low area of the pattern

Jefferies, a brokerage firm known for its optimistic outlook, has expressed bullish sentiments towards Bharti Hexacom, a subsidiary of the Bharti Airtel group. Citing robust growth prospects and favorable margin expansion, Jefferies has initiated coverage on the stock with a “buy” rating and set an ambitious price target of Rs 1,080. This target stands out as the most aggressive among market analysts, projecting a nearly 34 percent upside potential for the stock.

According to Jefferies’ target price, investors who participated in the Bharti Hexacom IPO could potentially double their investment within a year, considering the issue price of Rs 570.

Jefferies views Bharti Hexacom as an attractive investment opportunity within the Indian telecom sector. The company offers investors exposure to segments of Bharti Airtel’s business that demonstrate accelerated growth, higher returns on capital employed (RoCE), and improved free cash flow (FCF) conversion rates.

The brokerage forecasts a robust 16 percent compound annual growth rate (CAGR) in revenue and a 21 percent CAGR in earnings before interest, taxes, depreciation, and amortization (EBITDA) from fiscal year 2024 to fiscal year 2027. This anticipated growth trajectory, combined with a reduction in capital expenditure, is expected to drive a significant 40 percent CAGR in free cash flow.

Furthermore, Jefferies anticipates that Bharti Hexacom’s strong cash generation will facilitate substantial debt reduction of Rs 5,500 crore, equivalent to 14 percent of its market capitalization. This reduction is projected to contribute to lowering the net debt to EBITDA ratio to 0.4 times by fiscal year 2027, potentially paving the way for increased dividend payouts.

In addition to Jefferies, another brokerage firm, JM Financial, had previously initiated coverage on Bharti Hexacom prior to its market debut. JM Financial also assigned a “buy” rating to the stock and set a price target of Rs 790. JM Financial views Bharti Hexacom as a midcap company positioned to benefit from the structural growth story of wireless average revenue per user (ARPU) in the Indian telecom sector.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!