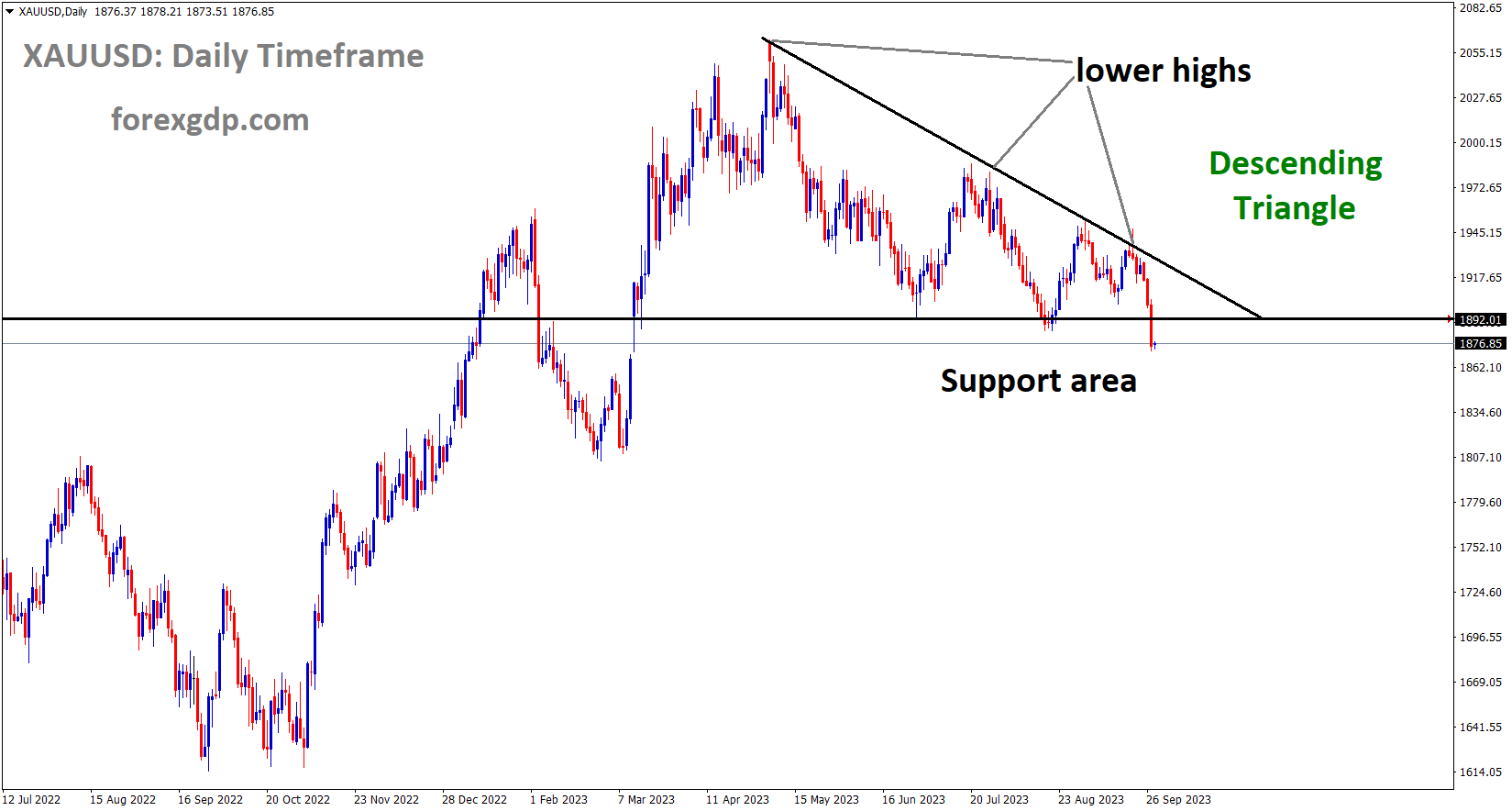

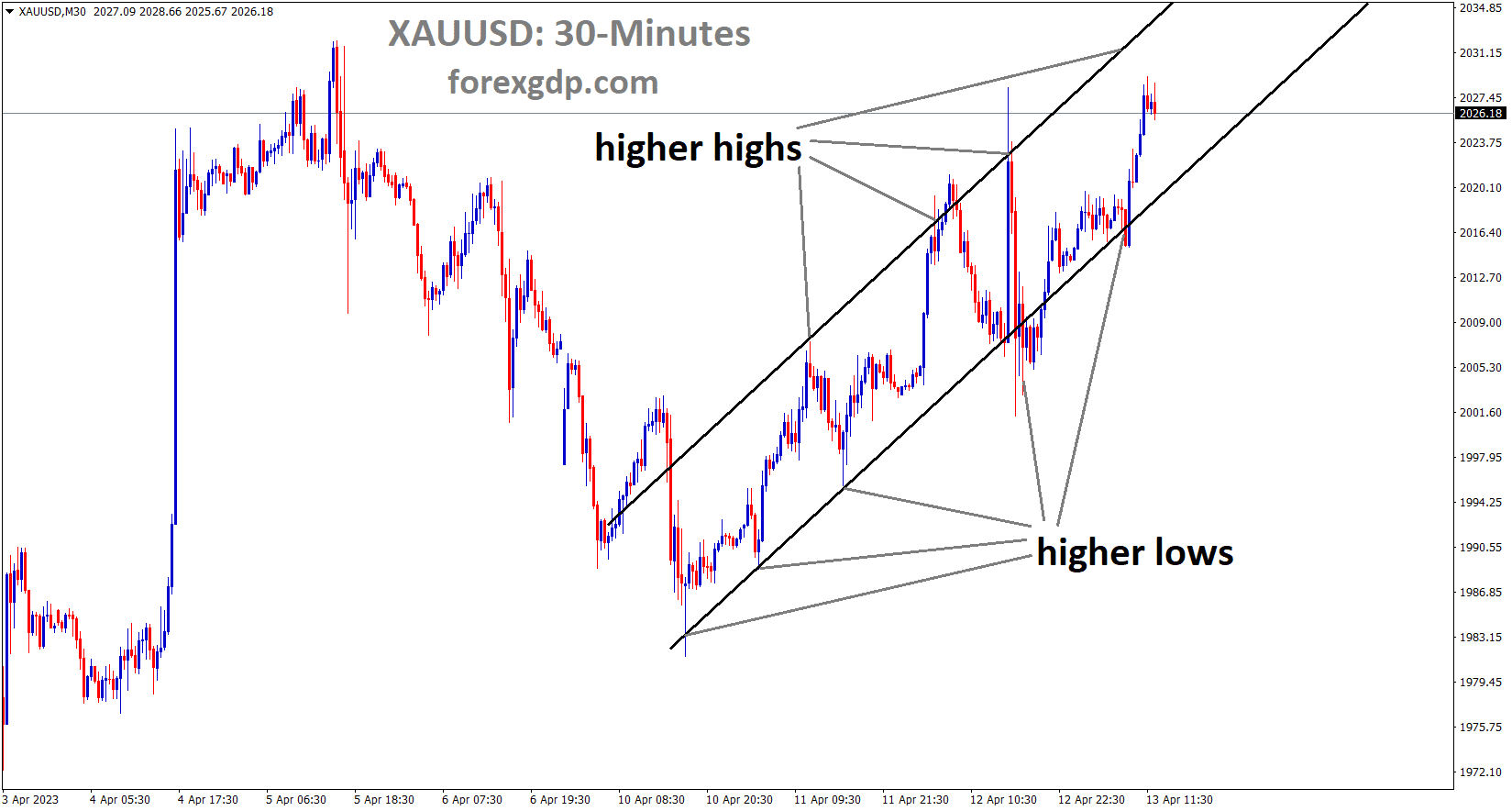

GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher high area of the channel.

The previous day, after the US CPI came in at a level that was lower than anticipated, gold prices peaked at around 2031$. US CPI came in at 5%, compared to the 5.1% consensus and 6.00% in the prior month. After the data was released yesterday and the FED meeting minutes showed a less aggressive stance on raising rates in May, the US dollar hurried to sell.

After the US Dollar declined following the release of the US CPI data and the minutes of the Federal Open Market Committee meeting, the gold price fell just shy of a one-year high overnight. In summary, US CPI came in at 5.0% year-on-year to the end of March as opposed to the expected 5.1% and previous 6.0%. As a result, Treasury rates declined across the yield curve, with the 2-year bond losing the most ground, ending the day about 6 basis points lower and trading below 4.0%. In March, it had been trading above 5.0%. The minutes of the Fed meeting revealed that the bank has significantly softened its previously blatantly hawkish position. Even if the tilt favours less assertive tightening, it has generally been interpreted as remaining hawkish, albeit to a lesser extent. A slight recession is predicted by internal bank researchers towards the end of 2023.

The minutes also showed that although the March meeting unanimously approved a 25 bp increase, several board members had proposed both a halt and a 50 bp increase in the target rate. The next meeting will take place in early May, and the interest rate markets anticipate a 25 bp increase. All of this worked to devalue the US dollar as the New York close approached. Presidents of the Richmond branch Thomas Barkin and the San Francisco Federal Reserve Bank sang from the same hymnal overnight. Rhetoric from both politicians suggests that the current tight monetary policy will continue. The biggest mover so far today has been the Australian dollar, which received a boost from the country’s unemployment rate continuing close to 50-year lows. It was 3.5% in March, which was less than the previous projections of 3.6% and 3.5%. Australia created 53.0k jobs in the month, which was far more than the 20k forecast and the 64.6k added the month before. With a surplus of USD 88.19 billion rather than the USD 40.00 billion expected, Chinese trade figures surprised to the upside. Despite this, APAC equities indices have generally weakened a little bit since Wall Street recorded minor losses. Today, silver reached a new 12-month high of USD 25.66 per troy ounce. The top of USD 2,032 per ounce set last week is another target for gold. Overnight, crude oil reached a 5-month high and has remained there since. While the Brent contract is just over US$ 87 barrel, the WTI futures contract is close to US$ 83 bbl.

USDCAD Analysis

USDCAD is moving in the Descending channel and the market has reached the lower low area of the channel.

The monetary policy of the Bank of Canada was left unaltered at a cash rate of 4.5% at the meeting the previous day. The meeting’s conclusion is that the labour market has tightened and inflation is decreasing. The Bank of Canada will be able to raise rates if employment and inflation start to falter. The 2023 CAD GDP was predicted by the Bank of Canada to increase from 1.0% to 1.4%.

Crude oil Analysis

Crude oil Price is moving in the Descending channel and the market has reached the lower high area of the channel.

The final decision of the Bank of Canada’s April monetary policy meeting was to keep the overnight interest rate at 4.50% for a second straight meeting. This choice was roughly in line with what was anticipated. Following the announcement, USDCAD briefly recovered but still fell by about 0.08% for the day. The statement stated that the bank is prepared to raise borrowing costs once more if necessary to restore price stability, in line with last month’s recommendations. This suggests that the tightening cycle is probably still ongoing despite this halt. The labour market is still tight, growth is holding up better than anticipated, and inflationary pressures are continuing to ease, but policymakers acknowledged that given underlying price dynamics, bringing inflation back to the target of 2.0% may prove more difficult.

Macroeconomic predictions show that the central bank increased its predicted 2023 GDP estimate from 1.0% to 1.4%. Meanwhile, the inflation forecast showed no change, indicating that consumer prices are usually evolving in line with existing forecasts. The table below provides a summary of the modified projections. The overall mood suggests that the BoC would be extra cautious and wait and see, but if the inflationary environment worsens or new evidence supports it, it might accelerate its tightening effort in the future. This bias should help the Canadian dollar in the near term.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has reached the lower low area of the channel.

The lower house of the Swiss parliament has voted against the proposed UBS acquisition of Credit Suisse. The main letdown of the Banking Crisis remedy is this. However, the outcome of the UBS and Credit Suisse Deal will be decided in the second round of voting.

A symbolic vote against giving state guarantees for UBS Group AG’s acquisition of Credit Suisse Group AG was cast in Switzerland’s lower house, demonstrating the strong public opposition to the transaction. The lower house rejected an upper house compromise, which resulted in the collapse of the measure and put a halt to parliamentary activities. Regardless of the result, the appointed committee of MPs had already approved the takeover, thus parliament cannot halt it. The denial nevertheless casts a shadow over the already challenging process of merging two major banks, especially given the impending threat of significant job layoffs in Switzerland in a year with upcoming elections. Though no agreement has been reached, MPs have called for a number of changes following the historic $3.3 billion deal, including increased authority for the financial regulator Finma. Michael Hermann, a political scientist and the director of the Zurich-based research organisation Sotomo, claimed that the majority of the parliament wanted to make a message. This demonstrates how politically charged the subject is in Switzerland. The populist right and left joined together to secure enough votes to prevent the law from passing. It would have given the go-ahead to risking as much as $120 billion in state funds. Together with the Greens and some Social Democrats, the Swiss People’s Party (SVP), which makes up the largest group, lobbied against it. According to Pirmin Schwander, a member of the SVP’s lower house, the party has insisted since 2008 that there is no bank that cannot go bankrupt. According to him, bankers’ “narcissistic company culture” is only fueled by the governmental guarantees.

Finance Minister Karin Keller-Sutter and the delegation of senior legislators who approved the backstop on behalf of the parliament before the takeover was disclosed in March lost the vote with 103 votes against, 71 votes in support, and eight abstentions. Although the argument is not likely to have any immediate consequences for UBS, it may signal a future appetite for stronger regulations. Questions have already been raised about UBS’s potential for local dominance and the combined company’s scale, which is double that of the Swiss economy. The bank would examine all options for Credit Suisse’s Swiss division, according to the vice chairman of UBS last week. Earlier this month, the Swiss government ordered UBS to make sure that its pay arrangements encourage employees to refrain from accessing the state guarantee. Politicians and business executives had expressed concern that the combined institution would have too much market power and eliminate competition. According to analysts at JPMorgan Chase & Co., despite the challenges of integrating Credit Suisse, UBS has the potential to grow into a “powerhouse” in the banking industry after the merger. Additionally, there was little public enthusiasm for the purchase. The Bern parliament appeared to be close to reaching an agreement in the afternoon as some Social Democrats seemed to be shifting their positions. A tighter approach to banks is “a major development,” according to Social Democrat lawmaker Roger Nordmann. A compromise featured greater equity requirements and limited incentives.

The discussion is now heated. There won’t be any further attempts to reconcile the differences between the government and the parliament, according to Hermann of Sotomo. “Now that democracy has been undermined, everyone can feel vindicated once more. The far right and populists will gain more support as a result of this systemic discontent.Seven ministers from the four biggest parties in Switzerland make form the executive instead of a coalition or a majority. They frequently work across party lines to reach pragmatist concessions and typically reach decisions by consensus. Regardless of how their parties have voted or how they personally voted in private, ministers do not openly criticise decisions made by the administration. Due to this configuration, parliament provides parties with the best opportunity to influence voters, which explains why there are often harsh statements made there, despite their infrequently biting nature.

USD Index Analysis

USD Index is moving in the Descending channel and the market has reached the lower low area of the channel.

The US FED meeting minutes said that the rate increase in May was the final rate increase of 25 basis points and that rate reduction may have occurred in the second part of the cycle. Members of the central banks believe that a modest recession could occur at the end of the year as a result of the strain of the US bank financial crisis.After US FED Minutes and US CPI data fell short of expectations, the US dollar fell.

Federal Reserve policymakers unanimously opted to raise the benchmark interest rate by 25 basis points to 4.75%-5.00% as part of the continuous tightening effort to drive inflation back to the 2.0% objective during the meeting on March 21-22, and the minutes of that meeting were made public today. Several Fed officials remarked that inflation continues biassed upward, with scant evidence pointing to prolonged deflation for core services, excluding housing, in recent data, according to the transcript of the proceedings. Many participants reduced their predictions for the FOMC’s terminal rate in response to the instability in the U.S. banking sector that sent investors into a frenzy a few weeks ago, despite worries about the inflation profile. The general consensus was that the strains on the financial system that surfaced last month could result in tighter lending requirements in the months to come, allowing for weaker pricing pressures in the medium run.

The central bank staff’s economic forecast called for a “mild recession” to begin later in the year, indicating that the outlook is deteriorating amid rising credit crunch threats. This evaluation could be a definite sign that the aggressive rising cycle that started in 2022 has ended or is about to, probably following the policy meeting next month. As soon as the minutes were made public, the U.S. dollar, as represented by the DXY index, continued to decline, falling as high as 0.65% to 101.50 for the day under pressure from falling bond rates, with futures markets pricing in a slight dovish turn in the Fed’s monetary policy trajectory. The path of least resistance for the U.S. dollar in the near term, with a Fed pause just around the corner, is probably lower, particularly if sentiment manages to stabilise. However, the greenback may be well-positioned to compel strength against riskier rivals due to its safe-haven characteristics if the mood deteriorates once more and volatility soars higher.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has reached the higher high area of the channel.

According to a Reuters story, ECB policymakers are converging on a 25 bps rate increase for May. The possibility of 50bps in May was mentioned by one group of policymakers, while no changes to the policy settings were indicated by another group. Because the current cash rate in the Eurozone is 3.00%, the rate increase is limiting growth.

Reuters reported on Thursday that officials at the European Central Bank are in agreement on raising interest rates by 25 basis points (bps) in May, citing five sources who had direct knowledge of the conversation. Even so, there is still some disagreement, with one tiny group arguing for a 50 bps increase in May and another small group supporting no change.

The ECB’s March economic predictions are seen as mainly maintaining their baseline. The peak in rates is now within sight, and it is safer to travel this “last mile” in more measured steps. Another justification for gradualism was that the ECB’s deposit rate, which is currently at 3%, is too low and limits growth.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has reached the higher high area of the channel.

The UK GDP data for the month of February came in flat with forecasts. But the Services sector is not doing better, printing 0.10% instead of the 0.70% estimate from January. The areas where the services industry struggled the most were education, government, and defence.

Meeting of the IMF held in US The UK’s finance minister, Jeremy Hunt, stated that the UK elections, which would change the UK economy’s direction, will take place in the spring of 2024. The US-UK trade agreement won’t be resolved anytime soon and could even be delayed, and the UK economy will grow faster than the IMF’s 2023 projection.

As a result of strikes in several different service-related industries, the UK economy stagnated in February. The most recent monthly GDP figures from the Office for National Statistics revealed no increase in February, with the services sector declining by 0.1% after growing by a revised higher 0.7% in January. The ONS states that “education, public administration, and defence made the largest contributions to the decline in services output in February 2023: compulsory social security, and industrial action took place in both of these industries in February 2023.” Today’s UK data and a slightly weaker US dollar are helping the GBPUSD pair. The US headline inflation dropped for the ninth consecutive month to 5%, below estimates of 5.2%, which caused the greenback to decline yesterday. According to yesterday’s FOMC minutes, the US economy may experience a minor recession as inflation gradually declines. The recent banking crisis may cause a slight recession later this year because of more stringent bank lending requirements, claims the research. This will slow down the economy, but it will also have an impact on inflation.

AUDUSD Analysis

AUDUSD is moving in an Ascending channel and the market has reached the higher high area of the channel.

The unemployment rate came in at 3.5%, a 50-year low, and was predicted to be 3.6%, which gave the Australian dollar a boost. 53.0K jobs were created, compared to the 20K expected and the 64.6K printed before. For February, Australia’s trade surplus reached a record high of AUD 13.87 billion. Based on the three-month AUD CPI statistics released next week, the RBA prefers to pause the rate the following month.

After jobs data showed a continuously tight labour market, which could keep inflation higher for longer, the Australian Dollar increased once more. Compared to the 3.6% predicted and the 3.5% before, the jobless rate remained low at 3.5% in March. Australia created 53.0k jobs in the month, which was far more than the 20k forecast and the 64.6k added the month before. It is an even more compelling data point when you consider the underlying change in the employment statistics. Full-time employment soared to 72.2k while part-time work declined by -19.2k. With the interest rate market anticipating no move, this raises the question of what the RBA will do at its meeting next month. Next week’s release of the more precise quarterly Australian CPI will garner notice. The central bank may experience problems if pricing pressures pick up again. The US CPI came in slightly below expectations, which helped the AUDUSD gain ground overnight on a weaker dollar. To the end of March, it was 5.0% instead of the projected 5.1% and the preceding 6.0%. The Federal Open Market Committee meeting minutes from that same session showed that the bank had relaxed from a hawkish, aggressive stance from its previous conclave.

The coastline of Western Australia is anticipated to be crossed by cyclone Isla elsewhere late Thursday or early Friday. Its route will be constantly monitored, even though it is currently not anticipated to have any long-term effects on the substantial iron ore holdings in the Pilbara region. This week, the deputy foreign minister of China is in Australia and has met with a number of federal government representatives and corporate executives. Both sides have continued to express a desire to develop a commercial partnership that is more fruitful. Since China placed an embargo on a number of Australian exports in 2021, several businesses have reexamined the risk of relying on a single sizable client. Most people have largely shifted in favour of creating export markets through a variety of strategies. As a result, Australia’s trade surplus continued to grow at a record clip in February, according to the most recent data, reaching a sizzling AUD 13.87 billion. The second-largest economy in the world is still a crucial market, but in the short term, improved relations between the two countries may boost sentiment rather than lead to a stronger bottom for the Australian dollar. Given the US Dollar’s challenges and the strong fundamentals in the home market, the AUD/USD pair may attempt to test the potential resistance zone in the range of 0.6785 and 0.6800.

NZDUSD Analysis

NZDUSD has broken the Descending channel in Upside.

Chinese trade surplus was $88.19 billion versus $39.2 billion. nevertheless less than the preceding release, which was $ 116.8 billion. In contrast to the 5.0% expectation, China’s imports decreased by 1.4%, and its exports increased by 14.8%. As a result of China exhibiting less contraction in import orders, this data shows a lift for the New Zealand dollar.

In the Asian session, the NZDUSD pair is exhibiting back-and-forth movements in a constrained range of 0.6210-0.6220. The Kiwi asset has moved in the opposite direction as the US Dollar Index has begun to stabilise after a sharp sell-off. Positive foreign trade data from China from March also failed to give the New Zealand Dollar a boost. China’s Trade Balance statistics came in at $88.19 billion, which is much more than the average estimate of $39.2 billion but less than the previous announcement of $116.8 billion. Annual imports have decreased by 1.4%, although the market had anticipated a 5% decrease. However, exports notably increased by 14.8% as opposed to the anticipated 7.0% decline. It is important to remember that New Zealand is one of China’s top trading partners, and the New Zealand Dollar would benefit from a slower-than-anticipated decline in Chinese imports.

EURJPY Analysis

EURJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Shunichi Suzuki, the finance minister of Japan, stated that during Group of Seven meetings, we are urging China to implement supply chain policy directives. At the G7 summit in Washington, Finance Minister Suzuki and Bank of Governor Ueda participated.

The G7’s supply chain policy recommendations are not necessarily targeted at China, according to Japan’s Finance Minister (FinMin) Shunichi Suzuki, who made the remarks early on Thursday. As they talk at the G7 summit in Washington, Suzuki of Japan joins Governor Kazuo Ueda of the Bank of Japan. The high-level policy recommendations made public today don’t specifically mention any one nation.

If a country’s supply chain is regarded to be very concentrated, that may not be the best development for economic security. Which nations qualify for supply chain assistance will be determined on a case-by-case basis by the G7. For economic security, supply chain concentrations in particular nations are undesirable. Japan, France, and India will present a framework for coordinating the restructuring of Sri Lanka’s debt. The world’s financial system is now stable, and things are currently stable. Japan has promised to boost sdr reallocation from 20% to 40% of the 2021 allotment.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/