GOLD Analysis

XAUUSD is moving in a Ascending channel and the market has rebounded from the higher low area of the channel.

The early-day Tuesday corrective bounce around $2,000 is difficult for gold price to hold onto as XAUUSD bears the weight of the US Dollar’s decline into the European session. Even though recent China statistics have been good, the market’s mixed mood, combined with the cautious attitude in front of major United States events and data, is likely to push gold buyers. Despite the recent difficulty of the XAUUSD bulls, the price of gold is able to rebuff the bearish bias that had been dominating for the previous two days despite a decline in US Treasury bond yields and the US Dollar. The 10-year and two-year Treasury bond rates, however, reverse a three-day upswing with modest falls of about 3.60% and 4.18%, respectively, by the time of press, bringing the US Dollar Index down to 102.00. The positive US figures combine hawkish Federal Reserve bets to place a floor under the USD, which challenges gold purchasers despite the recent decline of the US Dollar and Treasury bond yields.

The New York Empire State Manufacturing Index increased to 10.8 on Monday, breaking a four-month downward trend and reaching its highest level since July of last year. Additionally, the housing market index for the US National Association of Home Builders increased for the fourth consecutive month in April to 45 from the anticipated and previous reading of 44. Thomas Barkin, president of the Richmond Fed, stated on Monday that he wanted to see more evidence of inflation returning to goal in response to the statistics. The decision-maker also mentioned that he is comforted with what he is observing in the banking industry. It’s important to note that the XAUUSD pulled down from a multi-day high on Friday as a result of US consumer-focused data. As the policymakers remain divided on the specifics before the June deadline, the current cautious atmosphere ahead of the US debt ceiling plan, due for publication on Wednesday, challenges the US Dollar bulls while also attracting the Gold purchasers. According to Reuters, House Majority Leader Stephen Joseph Scalise, who represents Louisiana’s 1st congressional district, said earlier in the day that the Grand Old Party’s debt ceiling solution would be unveiled tomorrow.

President Christine Lagarde stated over the weekend that she is extremely confident that the US will prevent the nation from going into debt default. The XAUUSD bulls are also aided by positive economic news from China, one of the biggest importers of gold. However, China’s Q1 GDP increased 2.2% QoQ as opposed to the projected 2.2% and the 0.0% previous. In addition, March’s retail sales growth above expectations by 10.9% YoY, jumping from 3.5% in February to 3.5% in March, while industrial production growth slowed to 3.9% from 2.4% in January, falling short of expectations. After observing Gold’s initial response to China’s first quarter GDP, XAU/USD traders should wait for the US Housing Starts and Building Permits for March in order to accurately forecast the metal’s intraday movements. However, the discussions over the US debt ceiling and Federal Reserve will receive the majority of attention because recent hawkish views about the US central bank caused the US Dollar to strengthen and put pressure on the price of gold.

USDJPY Analysis

USDJPY is moving in a Ascending channel and the market has reached the higher high area of the channel.

Bulls in the USDJPY are having trouble maintaining control over a three-day winning streak early on Tuesday. The Yen pair eases from an intraday high and its highest point since March 15 to 134.50 at the latest while maintaining the same trend. The Yen pair appears to be affected by the most recent discussions regarding the Bank of Japan’s loose money policy as policymakers attempt to defend the existing course of action in the face of opposition from bond purchases and fiscal actions. In spite of this, Kazuo Ueda, the new governor of the Bank of Japan, claimed that the purpose of the BoJ’s bond purchases is not to pay down the nation’s debt. Prior to BoJ’s Ueda, recently appointed BoJ Deputy Governor Shinichi Uchida made an effort to defend the current monetary policy by asserting that fiscal restraints won’t make it more difficult to implement it. The USDJPY price is also affected by the market’s trepidation ahead of important US PMI and Japanese inflation data as well as by conflicting information from China. S&P 500 Futures, which reflect the sentiment, are still undecided even though Wall Street closed with modest gains and Japan’s Nikkei 225 is up 0.67% intraday to 28,705 at the latest.

On the other hand, recent positive US statistics increase market bets on the 0.25% Fed rate increase in May and decrease the likelihood that the US central bank will reduce rates at some point in late 2023. The recent rise in US Treasury bond yields before the most recent decline may be related to the same. The US 10-year and 2-year Treasury bond rates, however, conclude a three-day upswing with little declines of roughly 3.60% and 4.18% as of the time of publication. Not only did hawkish Fed bets and USDJPY buyers previously benefit from the data and yields, but also from Fed conversations. Nevertheless, the NY Empire State Manufacturing Index increased to 10.8 in April, breaking a four-month slump and reaching its highest level since July of last year. In addition, the housing market index for the US National Association of Home Builders increased for the fourth consecutive month in April, rising to 45 compared to the preceding and projected reading of 44. Thomas Barkin, president of the Richmond Fed, stated on Monday that he wanted to see more evidence of inflation returning to goal in response to the statistics. The decision-maker also mentioned that he is comforted with what he is observing in the banking industry. Moving forward, as the economic calendar becomes active, USDJPY traders may experience additional volatility. However, the key to following for precise directions is to watch Fed bets and rates.

USDCHF Analysis

USDCHF is moving in a Descending channel and the market has reached the lower high area of the channel.

USDCHF struggles to maintain its two-day recovery from a multi-month low as it fluctuates between 0.8990 and 0.8990-85 in the early hours of Tuesday. In doing so, the Swiss Franc pair reflects the market’s lack of movement in a cautious atmosphere prior to the major data from China, which is significant due in large part to the most recent recession talks. The stronger US Treasury bond yields and the hawkish Fed bets are the key reasons why USDCHF investors are still optimistic despite the US Dollar’s recent recovery. However, as positive US data and hawkish Fed talks joined the rising odds of another Fed rate hike in May and a decline in the market’s bets anticipating a rate cut in later 2023, the US Dollar Index extended Friday’s recovery from a one-year low. The US 10-year and two-year debt coupons printed a three-day increase to 3.60% and 4.20%, respectively. The same may be true for the US Treasury bond yields.

The NY Empire State Manufacturing Index increased to 10.8 for April, breaking a four-month slump and reaching its highest level since July of last year. In addition, the housing market index for the US National Association of Home Builders increased for the fourth consecutive month in April, rising to 45 compared to the preceding and projected reading of 44. Thomas Barkin, president of the Richmond Fed, on the other hand, stated on Monday that he wants to see more proof of inflation returning to the target level. The decision-maker also mentioned that he is comforted with what he is observing in the banking industry. In the midst of these manoeuvres, Wall Street posted a positive closing price but was unable to challenge the US Dollar bulls amid expectations for a further recovery and optimism that the US will be able to resolve the debt ceiling conflict before its June deadline. Moving forward, it will be crucial to keep an eye on the US Housing Starts and Building Permits for March in order to predict intraday directions. More crucially, speculation about China’s accelerated economic recovery will be put to the test as the Dragon Nation prepares to release its first quarter Gross Domestic Product figures. These figures will be widely watched to gauge market mood, which in turn influences the values of the USDCHF pair.

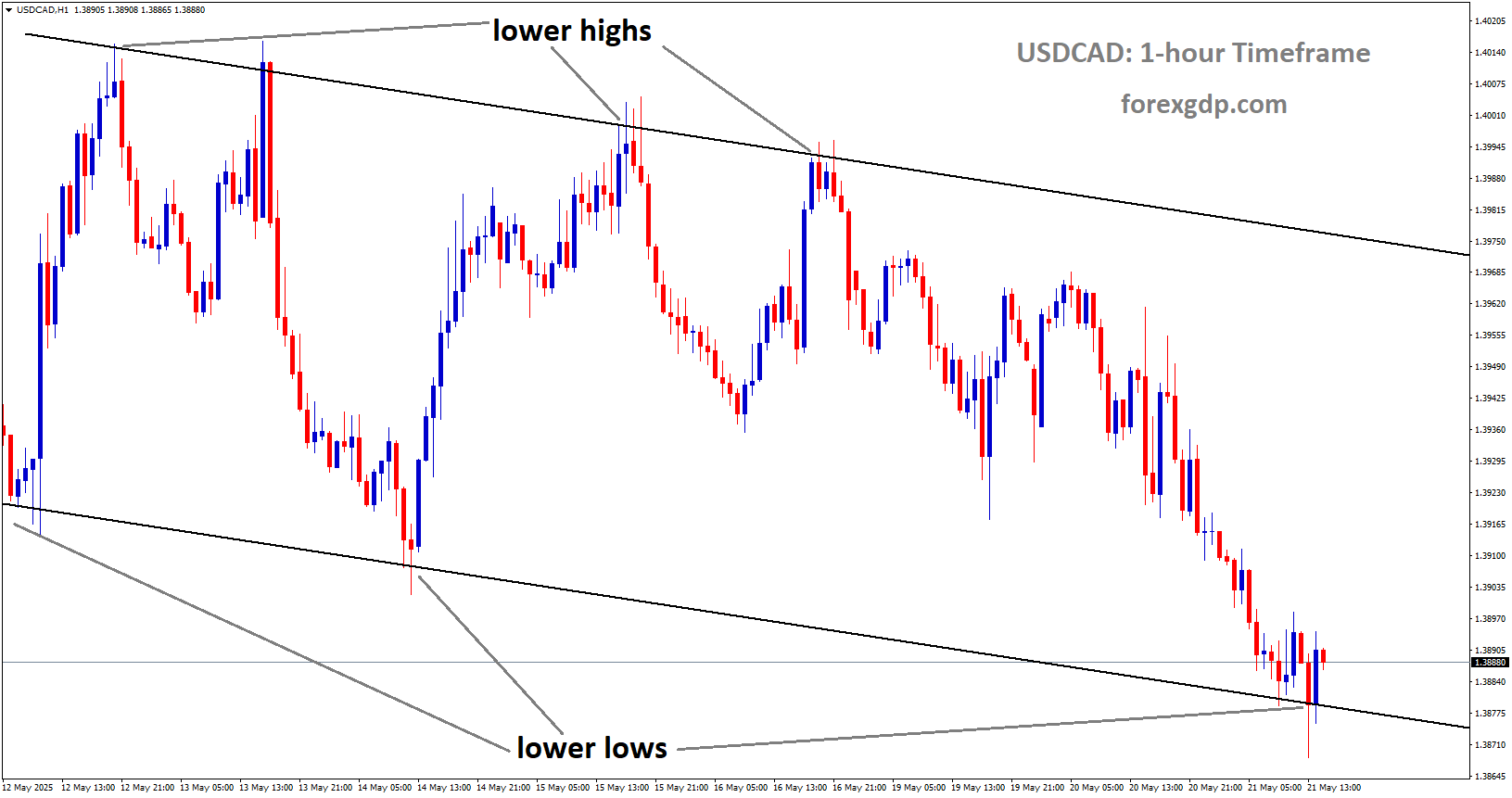

USDCAD Analysis

USDCAD is moving in a Descending channel and the market has reached the lower high area of the channel.

After a modest fall to close to 1.3380 in the Tokyo session, the USDCAD pair has gauged an intermediate cushion. Support is required for a strong recovery in order to prevent further loss for the loonie asset. The US Dollar Index has also found a cushion near 102.00, providing support to the Loonie asset. Following a bullish settlement on Monday, S&P500 futures have experienced marginal losses in the Tokyo session, signalling a small amount of caution amid the market’s general optimism. As banking stocks release their quarterly results and any effects of the financial turbulence on their asset quality, investors should ready themselves for extreme volatility in US equities. Investors appear to be in favour of the USD Index as the Federal Reserve is anticipated to raise rates even more in order to control persistent inflation. While the US labour market fundamentals and headline inflation have undoubtedly improved, core inflation remains persistent and calls for additional constraints on interest rate policy.

The Canadian inflation figures will probably cause the Canadian Dollar to sway. According to forecasts, the headline inflation rate would slow from the previous report of 5.2% to 4.3%. The monthly headline figure is expected to increase by 0.6% as opposed to the previously announced 0.4% growth. If oil and food costs are excluded, the core CPI, which was previously reported at 4.7%, would decline to 4.2%. This might enable Tiff Macklem, governor of the Bank of Canada, to maintain the current course of action. Attempts at a rebound in oil prices have been made after they fell to $81.00 following the announcement of positive statistics on China’s Gross Domestic Product. It is important to remember that Canada is the top oil exporter to the US, and a rise in oil prices will help the Canadian Dollar.

EURUSD Analysis

EURUSD is moving an Ascending channel and the market has rebounded from the higher low area of the channel.

While managing to leave behind two consecutive daily pullbacks despite rising selling pressure surrounding the dollar, EURUSD manages to post respectable gains far north of the 1.0900 barrier. Expectations of more tightening by the ECB in May are still very much in play for the time being. While for the time being markets were leaning towards a rate increase of 25 basis points, some ECB policy makers have hinted that a greater rate increase may be possible in the future. Later in the domestic calendar, the consistently important Economic Sentiment index for Germany and the euro bloc, as well as trade balance data for the euro area, will take centre stage. Later in the NA session, attention will turn to housing statistics and M. Bowman’s address from the FOMC across the Atlantic. After a brief retreat to the area of the 1.0900 zone, EURUSD is able to resume its upward movement. When it comes to the banks’ intentions on the probable next adjustments in interest rates, price action surrounding the single currency should continue to closely track dollar dynamics as well as the emerging Fed-ECB split. Although this stance looks in contrast to some sluggishness in the region’s economic realities, aggressive ECB-speak continues to support more rate hikes.

GBPUSD Analysis

GBPUSD is moving an Ascending channel and the market has reached the higher low area of the channel.

Tuesday’s robust buying stops the GBPUSD pair’s two-day corrective slide from its highest point since June 2022, which was at the 1.2545 level reached last week. Throughout the first part of the European session, the pair maintains its significant intraday gains in the 1.2435–1.2440 range, and for the time being, it appears to have ended a two-day losing streak to a one-week low hit on Monday. The UK Office for National Statistics announced stronger-than-expected wage growth figures, which will keep pressure on the Bank of England to hike interest rates further. This results in a general strengthening of the British Pound. In reality, according to the UK Office for National Statistics, average earnings increased by 5.9% during the three months ending in February, while labour costs increased by 6.6%, both of which were higher than expected. A broader extent of the scorching pay growth numbers obscure a rise in the unemployment rate and an unanticipated increase in the number of people claiming unemployment-related benefits.

In addition, a generally upbeat risk tone weakens the safe-haven US Dollar and gives the GBPUSD pair a further lift. However, despite rumours that the Federal Reserve would keep rising interest rates, the USD’s downside appears cushioned. In actuality, the market’s current pricing suggests that the odds of another 25 bps lift-off at the May FOMC monetary policy meeting are higher. This, in turn, keeps US Treasury bond yields high, which, at least temporarily, boosts possibilities for the appearance of some dip-buying around the USD and restrains any additional intraday appreciation for the GBPUSD pair. The US housing industry statistics, including Building Permits and Housing Starts, are currently anticipated by market participants as a potential source of momentum later in the early North American session. This will affect the USD price dynamics and present traders with short-term possibilities around the GBP/USD pair, along with US bond yields and the general risk mood. The newest consumer inflation numbers from the UK will, however, continue to be the centre of attention because they will be released on Wednesday and will have a significant impact on the demand for the sterling pound.

AUDUSD Analysis

AUDUSD is moving an Ascending channel and the market has rebounded from the higher low area of the channel.

Following the day’s two-way, aimless price movement, the AUDUSD pair attracts new bids and keeps up its bid tone throughout Tuesday’s early European session. The pair is currently trading in the range of 0.6735 to 0.6740, up over 0.60% on the day, and is supported by a number of variables. In spite of some US Dollar selling, the Australian Dollar is supported by the hawkish tone of the Reserve Bank of Australia’s meeting minutes from April and the positive macroeconomic data from China. In fact, the RBA meeting minutes revealed that board members discussed the argument for a further 25 bps rate increase in April due to the persistently high inflation rate and the extremely tight employment market. In the meantime, according to data made public on Tuesday, the Chinese economy expanded by 4.5% between January and March, significantly above forecasts and the 2.9% growth seen in the prior quarter. Additionally, Industrial Production increased in March by 3.9%, up from 2.4% in February, while Retail Sales increased by 10.6% last month, which was higher than anticipated. Furthermore, Fixed Asset Investment increased 5.1% in March compared to 5.5% in February, which lowered concerns about a deeper global economic crisis and increased optimism about the post-COVID recovery in the world’s second-largest economy. This continues to underpin an overall upbeat mood on the equities markets, which draws new selling on the safe-haven US Dollar and helps the risk-averse Australian dollar.

However, rumours that the Federal Reserve would keep rising interest rates may restrict the dollar’s potential decline and act as a temporary headwind for the AUDUSD pair. In fact, the markets currently predict a higher likelihood of a subsequent 25 bps lift-off at the May FOMC policy meeting. In order to avoid placing new bullish bets around the major and positioning for any more intraday appreciating rise, some prudence is advised before continuing to support the elevated US Treasury bond yields and possibilities for the appearance of some dip-buying. The US housing industry statistics, including Building Permits and Housing Starts, are currently anticipated by market participants as a potential source of momentum later in the early North American session. This will affect the USD price dynamics and present traders with short-term possibilities around the AUDUSD pair, along with US bond rates and the general risk mood.

NZDUSD Analysis

NZDUSD is moving in a Ascending channel and the market has rebounded from the higher low area of the channel.

Bulls are still sceptical despite positive China data from early Friday, and the NZDUSD oscillates around 0.6180, lately falling from an intraday high. The hawkish Fed bets and cautious atmosphere ahead of Zealand Q1 Consumer Price Index may be the cause. Compared to the 2.2% predicted and the 0.0% before, China’s Q1 GDP increased by 2.2% QoQ. In addition, March’s retail sales growth above expectations by 10.9% YoY, jumping from 3.5% in February to 3.5% in March, while industrial production growth slowed to 3.9% from 2.4% in January, falling short of expectations. On the other hand, recently stronger US data reduce the probability of a rate decrease from the US central bank sometime in late 2023 and increase the market’s expectations on the 0.25% Fed rate hike in May. In addition to the data, the hawkish Fed bets and the US Dollar were also favoured by Fed talks and positive rates, which drag down the NZDUSD prices.

It should be mentioned that the Reserve Bank of New Zealand shocked the markets by raising interest rates by 0.50% at its most recent monetary policy meeting. This heightens the significance of this week’s NZ CPI, which is predicted to increase to 2.0% QoQ from 1.4% previously. However, mixed fears over the US-China dispute over Taiwan and scepticism regarding the impending recession have also recently prompted NZDUSD purchasers. S&P 500 Futures continue to move in circles, reflecting the sentiment, while Australia’s ASX 200 reports a 0.30% intraday loss as of press time. Moving forward, it will be crucial to keep an eye on the US Housing Starts and Building Permits for March in order to predict intraday directions. On Thursday, New Zealand’s quarterly CPI is scheduled for release, while on Friday, the US PMIs for April are scheduled to be released.

AUDJPY Analysis

AUDJPY is moving an Ascending channel and the market has reached higher high area of the channel.

The Minutes of the Reserve Bank of Australia’s April policy meeting are the subject of some afterthoughts from analysts at Australia and New Zealand Banking Group. Information for on in the April Board meeting minutes of the RBA is The length of that debate in the Minutes suggests that the Board gave the request for a rate increase serious thought. Members agreed that there was a stronger case to halt at this meeting and reevaluate the necessity for further tightening at subsequent sessions, even though they acknowledged the validity of both sets of arguments.

It’s important to note that month rather than months is used to describe the duration of any such halt. In particular, it says Members noted that they would receive additional monthly readings on the labour market, household expenditure, and business conditions during the course of the following month, as well as more data on developments in the global economy and financial markets. They would also receive another quarterly reading on inflation. At the meeting that followed, the staff was also expected to deliver a comprehensive set of updated forecasts. The aforementioned leads us to believe that the decision to pause was a relatively tight call because both an increase in interest rates and a halt might be justified.It also implies that the Board will be able to be swayed in either direction based on the remaining evidence and the new set of estimates they will get at the May meeting.

CADJPY Analysis

CADJPY is moving an Ascending channel and the market has fallen from the higher high area of the channel.

According to the newly appointed Governor of the Bank of Japan , Kazuo Ueda, there is no imminent need to revisit the 2013 joint statement with the government. Ueda continued by saying that the government’s labour reform has boosted the economy. Prices and wage growth are both showing signs of improvement. will reach the desired inflation rate, however it can take some time. exchanging ideas with the government whenever feasible and looking for relevant policy. It is crucial for economic expansion to result in rising worker pay

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/