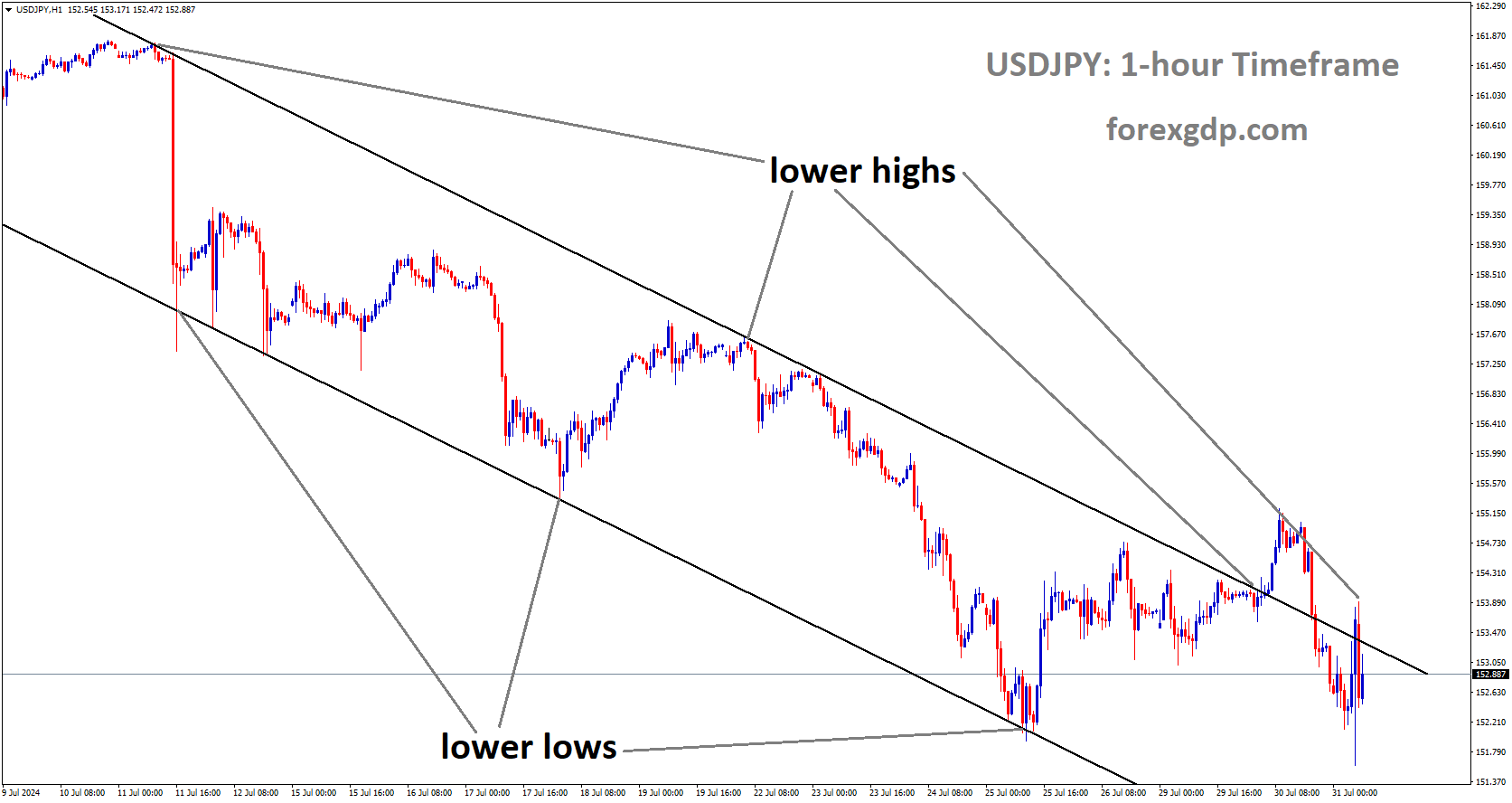

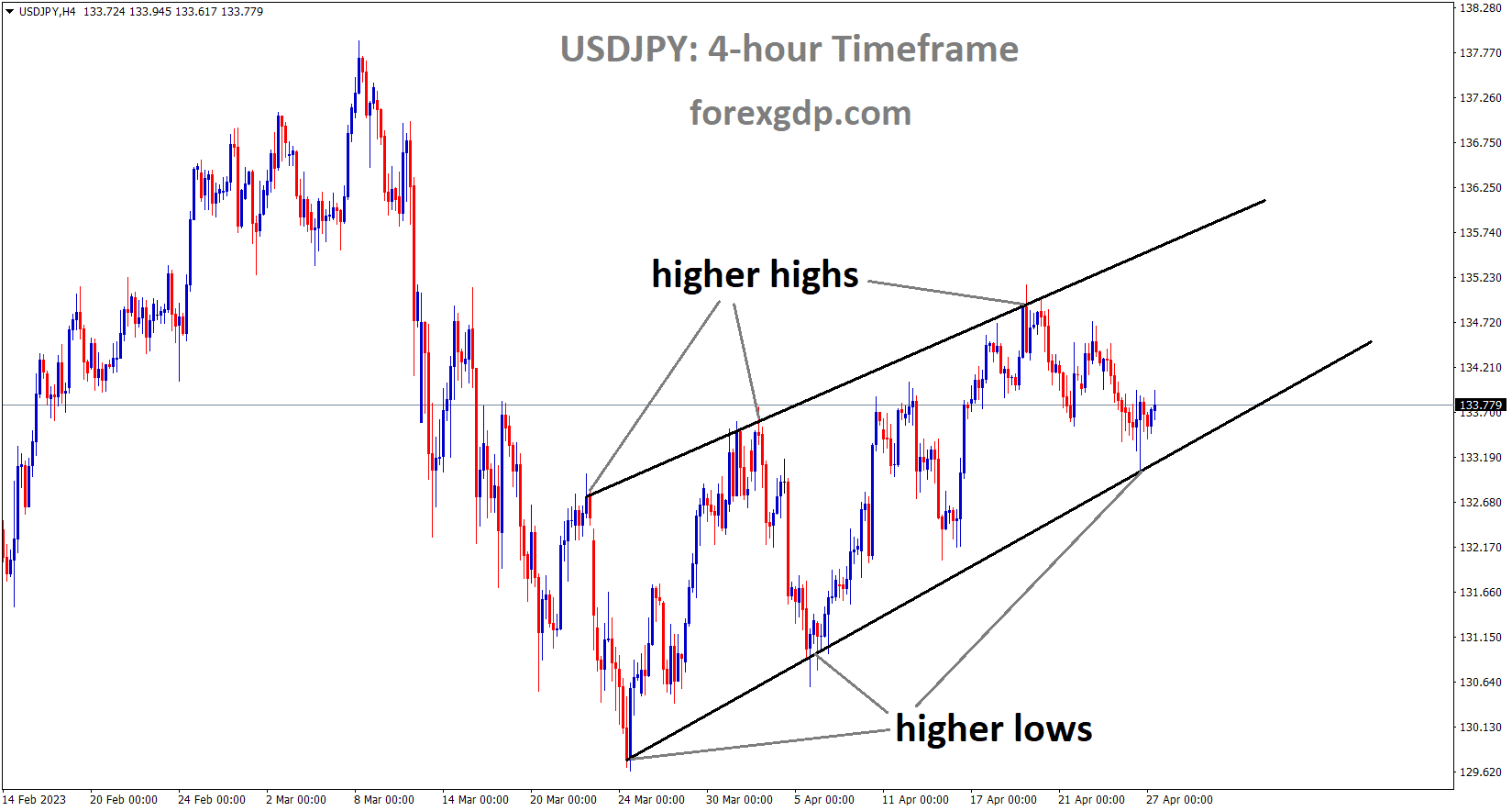

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Ex-Deputy Governor Wakatabe of the Bank of Japan stated that yield curve control will not be used in this meeting, contrary to his expectations. Tomorrow’s Bank of Japan Monetary Policy Meeting is more important; it is the first meeting for BoJ Governor Ueda, and no changes are expected. However, the YCC remains normal; no changes are expected in YCC.

Masazumi Wakatabe, a former deputy governor at the Bank of Japan, has expressed surprise at the possibility of a change in Yield Curve Control by the BoJ this coming Friday. Officials from the Bank of Japan have expressed reluctance to make changes to or eliminate their yield control stimulus during the policy meeting this week, which wraps up tomorrow. Instead, BOJ policymakers believe it is necessary to maintain its yield cap on government bonds for the time being in order to bolster the economy. During his first meeting as governor, Kazuo Ueda is expected to maintain status quo during the two-day event. The press conference will be the main event, as it will reveal how much of a change he plans to implement.

GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

In anticipation of this week’s US GDP and US Core PCE index reports, gold prices are consolidating. The US dollar is consolidating ahead of next week’s US Federal Open Market Committee meeting, where a 25-basis-point rate cut is expected, and gold purchasers are unsure if demand for the US dollar would be robust then.

So far today, the precious metal’s price has fluctuated a modest amount, going up and down by less than US$ 0.2 between $1,999 and $2,000. The dollar has been rather stable so far today, indicating calm in the markets ahead of the release of US GDP and Core PCE statistics later on. After dropping early in the week, Treasury rates have levelled off. Ten-year government bonds continue to trade below 3.50%. Despite last week’s record high of 1.36%, real rates have remained stagnant at around 1.20% for the same portion of the yield curve. Thursday has started slowly for G-10 currencies, although the New Zealand dollar has managed to recover ground over 0.6140.

The company’s second-quarter sales prediction was raised to USD 32 billion after the North American market closed on Tuesday, up from the previous forecast of USD 29.48 billion. The stock market is expected to open on Wall Street with slight gains, according to futures. Even APAC stock markets have been rather calm so far today. Deutsche Bank said that its first-quarter results fell short of expectations. Revenue for the period was recorded at € 2.36 billion, down below the expected € 2.53 billion.

USDCAD Analysis

USDCAD is moving in an Ascending channel and the market has reached the higher low area of the channel.

Due to declining inflation and a robust labour market, the Bank of Canada may be able to keep interest rates at 4.50% until 2024, as indicated by the minutes of a recent meeting. The Bank of Canada was the first central bank to put a hold on its rate-hike plan as the economy showed signs of picking up steam.

Crude Oil Analysis

Crude Oil price is moving in the Descending channel and the market has fallen from the lower high area of the channel.

The Minutes from the Bank of Canada’s April monetary policy meeting were released on Wednesday, and analysts from TD Securities shared their comments on the document. The April Summary of Deliberations from the Bank of Canada expanded on its hawkish tone by explaining the case for a rate hike and noting that the economy was performing better than projected in January. Given both GDP and inflation expectations remained constant, the case for maintaining the status quo amounted to a call for further data suggesting that current policy is too restrictive. However, the Bank warned of some potential positive outcomes and resisted market expectations for interest rate decreases in 2023.

Although we anticipate the Bank to maintain its current policy of a 4.50% interest rate through 2024, the minutes released today should remind us that risks remain tilted towards additional rate increases in the near future.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Today, the Swiss National Bank reported a profit of 26.9 billion Swiss francs, a rise in the value of gold and an increase in foreign currency investments for the first quarter.

Bank made a profit of 24,2 billion francs in foreign currencies and 4.3 billion from gold holdings in the first quarter.

The 27th of April, in the City of Zurich As the value of its gold and foreign currency investments rose in the first quarter of the year, the Swiss National Bank reported a profit of 26.9 billion Swiss francs on Thursday.

A rise in the value of the bank’s gold reserves resulted in a profit of 4.3 billion Swiss francs, and the bank’s foreign currency positions yielded a profit of 24 billion francs.

USD Index Analysis

USD Index is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Next month’s FOMC meeting is anticipated to increase the cash rate by 25 basis points to 5.25 percent, and another rate hike is conceivable in June. In the first half of 2023, the cash rate could reach 5.50 percent. The second half of 2023 will see a rate pause in order to control inflation.

Australia and New Zealand Banking Group’s analysts provide their forecasts for the monetary policy decision to be published by the US Federal Reserve on the following Wednesday. We anticipate a 25bp rate hike from the FOMC at their upcoming meeting. The effective Fed Funds rate would then be 5.10%, which is in line with the median dot plot value. In the long run, we anticipate one more rate hike of 25 basis points, reaching 5.50%. However, in the grand scheme of things, the tightening cycle may be winding down. Future rate decisions are likely to be made on a meeting-by-meeting basis.

According to our GDP forecasts, the lingering effects of last year’s rate hikes will become more noticeable in the second quarter. We anticipate moderate increase in consumption and the labour market. However, it may take some time for core services inflation ex-shelter to decline. The Federal Open Market Committee will consider the health of the banking system as a whole. Inflation must be contained if banks are to retain their purchasing power. To further rein in inflation in the second half of 2023, we anticipate that the Fed will leave interest rates unchanged.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Today’s release of the Australian Export and Import Price Index reveals that the Export price index rose to 1.6% QoQ in Q1 2023, up from -0.90% in Q1 2022 and below the 1.9% forecast. Import price index decreased to -4.2%, compared to 3.6% anticipated and 1.8% previously.

Mild bidding persists around 0.6610, defensive in recent sessions, as buyers struggle to extend the previous bounce from the 1.5-month low ahead of Thursday’s European session amid cautious sentiment. As traders wait for the US first-quarter GDP, which is predicted to slip to 2.0% on an annualised basis from 2.6% previously, the Aussie-U.S. dollar pair reflects this uncertainty. After lower Aussie Consumer Price Index disclosures the day before, the Australian Bureau of Statistics issued the Q1 Export and Import Price Index statistics earlier in the day, but they failed to dispel the dovish bias surrounding the Reserve Bank of Australia’s policy stance. However, the Import Price Index fell by -4.2%, while the Export Price Index grew to 1.6% QoQ in Q1 2023 from -0.9%, easing below the 1.9% projections. Meanwhile, market sentiment is still unstable due to varying opinions on the US default, banking sector health, and first quarter GDP.

The United States House of Representatives approved a bill to extend the debt ceiling late on Wednesday. With such a large gap between Republican and Democratic demands, though, politicians are certain to continue bickering. As a result, the Aussie pair is unchanged due to cautious optimism on the US debt ceiling discussions. New data on US tax receipts gives Goldman Sachs hope that the US Treasury may delay the prospect of a default on federal payments until late July, which supports prices. Nasdaq, meanwhile, held its ground thanks to positive earnings reports from Microsoft and Alphabet Inc., the parent company of Google. Concerns about the First Republic Bank continue to grow in the wake of a 20% drop in share price on Wednesday and a 50% drop the day before.

Concerns of an escalation in the conflict between the United States and China were rekindled after US Commerce Secretary Gina Raimondo’s statements. According to Reuters, US Commerce Secretary Raimondo warned that Chinese cloud computing firms like Huawei Cloud and Alibaba Cloud could threaten US security. An official’s promise to look into a request to put them on an export control list was also reported. Wall Street ended on a mixed note, and US Treasury bond rates haven’t moved much in either way since then. Despite this, S&P 500 Futures are trading up slightly at approximately 4,080 as of this writing. Traders in the AUD/USD pair will need to keep an eye on the US GDP data for the first quarter to determine a path forward in the face of recession fears. Then, this coming Friday, information on the Fed’s favourite inflation indicator, the Core PCE Price Index, may provide some entertainment for traders in advance of next week’s Federal Open Market Committee meeting.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

Chris Hipkins, the prime minister of New Zealand, stated that there is no new tax for every citizen to compensate for Cyclone funds; the government will take care of Cyclone funds and there is no need to increase taxes on the public.

New Zealand’s Activity outlook deteriorates from -8.5% to -7.6%, and business confidence falls from 43.4 to -43.8.

As Thursday’s European session begins, the NZD/USD exchange rate has risen to 0.6140, continuing its ascent from a six-week low that ended a two-day decline. By doing so, the Kiwi pair supports the general weakening of the US Dollar in the face of conflicting domestic factors. The Australia and New Zealand Banking Group released their monthly Activity Outlook and Business Confidence data for New Zealand earlier in the day. The former rose to -7.6% from -8.5% and -8.9% before, while the latter fell dramatically to -43.8 from -43.4 forecasts and earlier readings. Contrarily, New Zealand Prime Minister Chris Hipkins was quoted as saying by Stuff New Zealand, There will be no new tax everyone would have had to pay, like a cyclone levy, to fund the recovery.

The market has been supported by cautious optimism on the back of mixed US data and buoyant technology company profits, as well as the passing of a law that allows US policymakers to negotiate the extension of the debt ceiling. While March’s increase in US Durable Goods Orders was welcome news, it wasn’t enough to offset the damage done by the misleading information on consumer confidence. Alternatively, the NZDUSD purchasers are pushed by concerns over a US recession, banking sector turmoil, and Sino-American friction. A drop in the price of First Republic Bank unsettles investors while recent conflicting US data and the likelihood of the Fed’s higher for longer rates keep economic slowdown fears on the table. The tension between the United States and China has been reignited by statements made by US Commerce Secretary Gina Raimondo. U.S. Commerce Secretary Raimondo was quoted by Reuters as saying, Chinese cloud computing companies like Huawei Cloud and Alibaba Cloud could pose a threat to US security. The policymaker reportedly also promised to investigate the proposal to place them on the export restriction list.

US Treasury bond rates continue to trend lower, reflecting the current climate, while S&P 500 Futures show slight gains near 4,080 at press time, following Wall Street’s mixed close. As hawkish fears about the Reserve Bank of New Zealand subside, the US first quarter GDP, which is predicted to slow to 2.0% on an annualised basis from 2.6% previous, becomes critical for the NZDUSD traders to watch.

EURCHF Analysis

EURCHF has broken the Descending channel in Upside.

ECB rate hike expectations for May month are 50 basis points higher than FED rate hike expectations for May month, which are 25 basis points. The euro has great financial stability in banks and plenty of liquidity to deal with any bank defaults. This week, German CPI and employment data are expected.

Following Wednesday’s pullback from 1.1095 in the early hours of Thursday morning Europe time, EUR/USD maintains a strong position around the mid-1.1000s as buyers start a run-up seeking the highest levels since March 2022. This is good news for the Euro since it coincides with a general decline in the value of the US dollar and hawkish ECB concerns in the run-up to first-quarter GDP, which is forecast to slow to 2.0% annually from 2.6% previously. Rates of interest are expected to rise by 0.50% during the European Central Bank’s monetary policy meeting in May, according to interest rate futures. Despite conflicting US data, the EURUSD run-up is supported by the very certain 25 basis points of Fed rate hike and calls of the policy shift afterward, which keep the bloc’s central bank more lucrative than its US counterpart. New data shows that March increases in durable goods orders in the United States weren’t enough to offset the damage done by the leak of questionable data on consumer confidence. Notably, the PMIs for Europe and Germany were both more robust than their US counterparts, indicating greater economic optimism in the old continent.

The US House of Representatives has recently enacted a bill allowing the government to negotiate an increase in the debt ceiling, which is discussed in greater detail on a different page. With such a large gap between Republican and Democratic demands, though, politicians are certain to continue bickering. This helps maintain the Euro’s strength amid cautious optimism on the US debt ceiling talks. In addition, the most recent US tax reception data give Goldman Sachs reason to believe that the US Treasury Department may delay the possibility of a federal payments failure until late July. This boosts the Euro against the dollar. Positive results from Microsoft and Alphabet Inc., the parent company of Google, helped keep the Nasdaq higher. The First Republic Bank’s growing worries weigh on morale and push EUR/USD bulls, however, as their share price fell another 20% on Wednesday after falling 50% the day before. Intraday EUR/USD traders should pay close attention to the annualised rate of growth in US gross domestic product for the first quarter. The headlines surrounding the efforts to raise the US debt ceiling and the financial sector news will also be significant.

GBPJPY Analysis

GBPJPY is moving in an Ascending channel and the market has reached the higher high area of the channel.

According to a British industry survey, monthly retail sales grew in April of this year. The monthly retail sales balance increased to +5 in April, up from +1 in March. However, the May month forecast is lower than the current month.

london An industry poll released on Wednesday showed that British retail sales went up a little bit in April, but most store chains don’t expect this to last. The monthly retail sales balance for the Confederation of British Industry went from +1 in March to +5 in April. This is the highest number for this year. But expectations for May were a little bit gloomy. From March 27 to April 13, 72 stores were asked to fill out the poll.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/