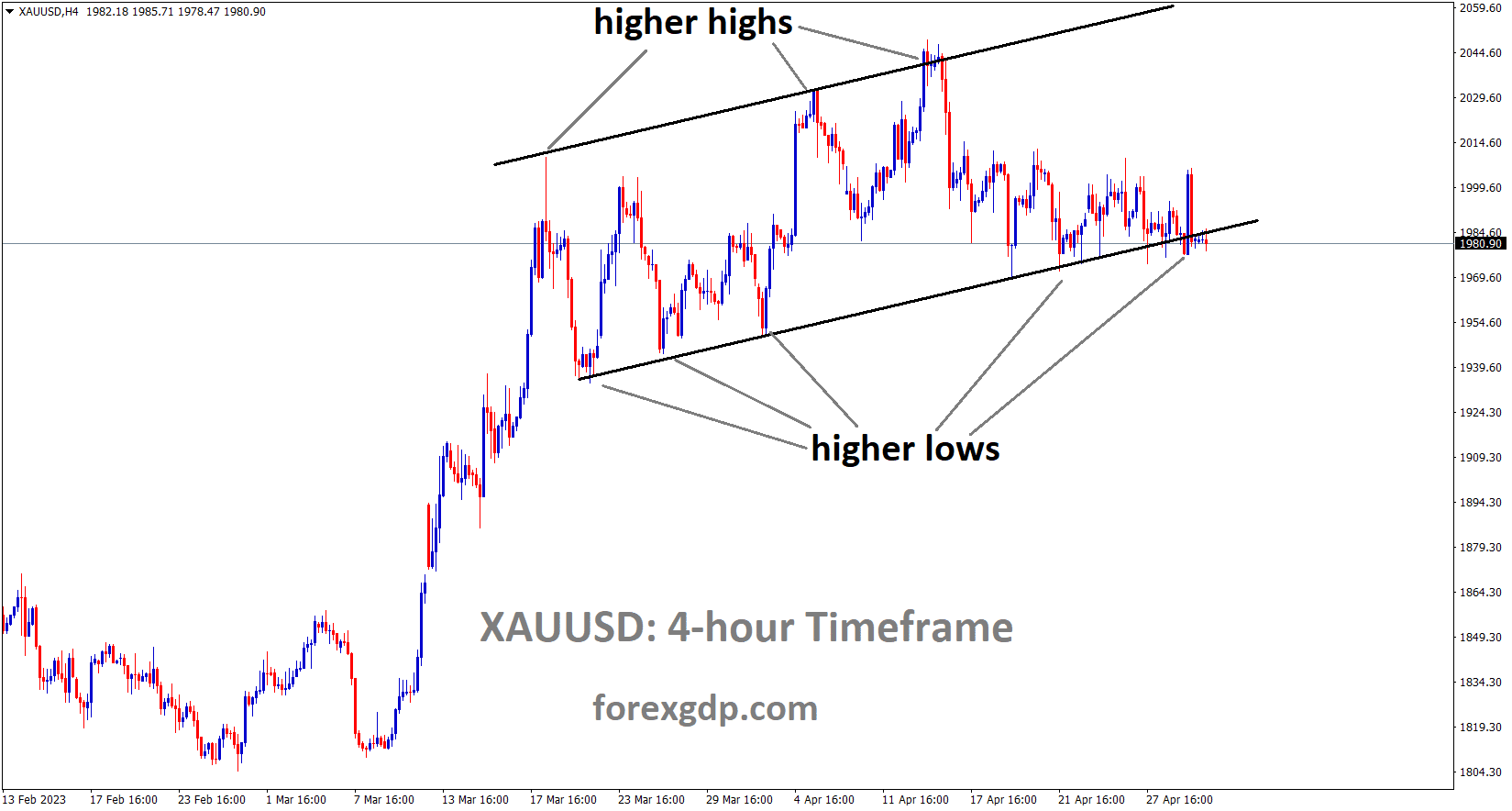

GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel.

The US ISM manufacturing PMI data was 47.1, compared to estimates of 46.8 and the prior reading of 46.3. The US good services sector has decreased for the last six consecutive months, and the employee and prices paid components increased from 46.9 and 49.2 to 50.2 and 53.2, respectively. The US labour market and pay prices are rising, according to ISM data, thus the FED will raise interest rates this month earlier than anticipated.

Non-yielding assets, such as gold, fell sharply when the US data was released yesterday.

Due to the Labour Day vacation in the region, most European markets were closed on Monday, which resulted in a session with low volume for gold prices. When gold first regained the psychological level of $2,000, it rapidly sank after being unable to maintain gains and returned below it when U.S. macroeconomic data exceeded expectations. To put things in perspective, the ISM manufacturing PMI improved in April, mildly rebounding to 47.1 vs. the projected 46.8. The employment and prices paid components of the survey increased to 50.2 and 53.2 respectively, up from 46.9 and 49.2 previously, supporting the U.S. dollar and Treasury yields across the curve even as the sector producing products shrank for the sixth consecutive month. The findings of the ISM survey point to the near-term persistence of tight labour markets and an upward tendency in wage pressures. The increase in prices paid is particularly worrisome since it can portend an impending rise in inflation. In light of the current situation, the Fed might be discouraged from quickly abandoning its tightening programme. This indicates that additional interest rate increases beyond the one anticipated for May shouldn’t be entirely ruled out just yet.

SILVER Analysis

XAGUSD Silver price is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Traders should pay particular attention to the Fed’s policymakers’ choices and projections this week, when the May meeting comes to a close. As part of its efforts to restore price stability, the central bank is anticipated to raise borrowing costs by a quarter point to 5.00–5.25%, which would raise the benchmark rate to its highest level in 17 years. The 25 bp raise has already been discounted, so advice should be the main concern. The rise in rates, which would harm precious metals and prevent them from continuing their recent advance, could occur if the Fed does not give a clear indication that it is about to put the breaks on. On the other hand, if the Fed signals that it is pressing the “pause button,” gold may recover swiftly. Keeping the XAUUSD technical analysis in mind, resistance seems to be close to the $2,000 mark. Bulls may be able to boost prices towards the 2023 highs quickly if they are successful in doing so. On continued strength, focus will turn to the record high, $2,080. Initial support on the downside is at $1,975. The 50-day simple moving average can serve as the next floor if this region is breached.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel.

Western nations including the EU and US are reportedly experiencing liquidity issues and interest rate worries, according to Japan’s minister of economics Shigeyuki Goto. However, there are currently no liquidity issues or interest rate risks in the Japanese economy.

By using YCC and negative interest rates, we are able to keep a balance between interest rates and inflation rates. As our debt continues to grow, we are balancing our budget through March 2026.

Liquidity and interest rate risks were the root of the banking sector issues in the US and Europe, but for the time being, they won’t have an impact on Japan’s economy or financial system, according to Shigeyuki Goto, Japan’s economy minister, in an interview with Reuters on Tuesday morning. Goto responded, “I expect the central bank to steer policy flexibly and appropriately,” according to Reuters, when asked if the Bank of Japan’s efforts to eventually normalise its easing policy may be delayed by the US banking troubles. Risks related to interest rates and liquidity were present in what occurred to the West. Liquidity risks will require a forceful response from policymakers and financial institutions.

I don’t anticipate significant issues in the American financial system. Risk considerations include lower revisions to global economic predictions and changes in the financial markets should be taken into consideration as Western nations continue to tighten their monetary policies. The BOJ should focus on monetary policy operations as the country’s central bank, but I don’t see how the present financial scenario will affect Japan’s economy and financial industry as a whole. I anticipate the BOJ to use flexible monetary policy guidance, which calls on the central bank to make appropriate decisions while taking the economy and financial markets into consideration. Given the shaky situation of the Japanese economy, it would be challenging to use sales tax revenue as a financing source to pay for higher childcare expenses. The government would continue to work towards its goal of balancing the nation’s primary budget by the fiscal year’s end in March 2026, excluding fresh bond sales and debt servicing costs, a target he described as not easy.

USDCAD Analysis

USDCAD has broken the ascending channel in downside.

Canada’s GDP for February came in at 0.10%, falling short of the projection of 0.20% and worse than the 0.605 reported for January. Because of Canada’s robust labour market and low inflation, the Bank of Canada has decided to postpone rate increases.

There won’t be any rate reduction until 2024, according to Tiff Macklem, governor of the Bank of Canada.

Statistics Canada reported that the gross domestic product (GDP) of Canada came in at a pitiful 0.1% in February, falling short of the 0.2% estimate and worse than the upwardly revised 0.6% in January. According to the early estimate for March, which is -0.1%, the good start in January swiftly fizzled. The expected growth rate is a reasonable 2.5% on an annualised basis. The economy is experiencing the effects of the Bank of Canada’s rate tightening, as evidenced by the economy’s sluggish growth and the benchmark cash rate, which is now at 4.5%, the highest level since 2007. The BoC may continue raising rates until the slowdown in GDP results in lower core inflation, which decreased from 4.9% to 4.5% in March but remains above than the 2% target. Governor Macklem hinted that there wouldn’t be any rate reductions until 2024 at the April rate meeting, which saw the BoC stall on rates.

The employment market, which has been unexpectedly strong despite the Canadian economy’s obvious slowdown, is expected to follow suit. Despite the BoC’s aggressive tightening, the unemployment rate has stayed around 5%. The BoC is hoping that the labour market will deteriorate and assist drive inflation levels lower because employment levels are several months behind growth. Manufacturing PMIs from both sides of the border start off the week. All across the world, including in Canada and the US, the industrial sector is still having difficulties. The PMI for Canada is predicted to increase in April from 48.6 to 50.5, indicating stagnation. Five consecutive months have seen a fall in manufacturing in the US, with readings below the 50.0 mark. After 46.3 in March, the estimate for April is currently 46.6.

USD Index Analysis

USD index is moving in the Descending channel and the market has reached the lower high area of the channel.

This week’s US Dollar movement is largely determined by the FOMC meeting and non-farm payrolls data. The economy added 236,000 jobs in March, according to figures, but the impact of the banking crisis last month was minimal. The data for this month will paint a vivid picture of the crisis that took place and the lack of liquidity in US banks.

The DXY index, which tracks the performance of the U.S. dollar, declined slightly this past week, falling about 0.10% to 101.68, hurt by a rebound in equity markets and strong performance by tech stocks on Wall Street after strong earnings from major companies like Microsoft and Meta Platforms. High-impact events that could strengthen the U.S. dollar’s bearish bias will occur next week, therefore it is crucial to attentively monitor the U.S. economic calendar to make better trading decisions. However, the Fed’s decision on monetary policy on Wednesday and the nonfarm payrolls survey on Friday are two events that merit close attention. Let’s start with the U.S. central bank. As part of their continuous attempts to bring inflation back to the 2.0% objective, authorities there are anticipated to increase interest rates by 25 basis points to 5.00%-5.25%. Given that this choice has already been discounted, the market will focus mostly on the forecast horizon guidance.

Traders should keep an eye out for comments on the outlook as the FOMC signalled last month that its tightening campaign was coming to an end after upheaval in the U.S. banking industry heightened risks to the economy and elevated the chance of a recession. The U.S. dollar is anticipated to decline if the Fed officially presses the pause button as markets try to anticipate the next actions, which in this scenario would be rate reduction. Monetary policy divergence is anticipated to work against the dollar because other important central banks, like the ECB, are still likely to raise borrowing prices a couple more times this year. The U.S. jobs data will be the main topic of discussion on Wall Street on Friday. The U.S. banking sector crisis may have overestimated March’s data, which showed the economy adding 236,000 jobs, but the April report should make up for this error by more accurately representing those developments.

For the reasons stated above, NFP’s figures may disappoint, falling short of expectations of a 178,000-job gain. Soft statistics might lead to a dovish recalibration of the Fed’s policy stance, which would be bad for the U.S. currency. On the other hand, a terrible report might be good for the dollar in the near run because it would scream “recession” and cause investors to become more risk averse. Due to its safe-haven characteristics, the U.S. dollar typically benefits during times of market turmoil.

EURGBP Analysis

EURGBP is moving in an Ascending channel and the market has reached the higher low area of the channel.

Although inflation in the eurozone is considerably lower than it was the previous month, investors are watching for potentially significant rate increases from this week’s ECB monetary policy meeting. Unemployment claims are down, and pay prices are up in the Europe region as companies haggle with job searchers. The euro is rising ahead of this week’s ECB meeting on Thursday.

In the Asian session, the EURGBP pair is fluctuating within a constrained range below 0.8890. The cross is anticipated to retake the round-level resistance of 0.8800 going forward as investors wait for the European Central Bank to declare a significant interest rate hike this week. The Eurozone’s consumer spending is becoming more resilient as job searchers now have more negotiating power with hiring companies due to the labour shortage. In order to curb persistent inflation, ECB President Christine Lagarde announced a massive interest rate hike. However, data on inflation in the Eurozone will be closely watched first. The Eurozone’s Harmonised Index of Consumer Prices (HICP) data on Tuesday are crucial because the ECB will carefully evaluate them before setting an interest rate.

The preliminary headline Harmonised Index of Consumer Prices is expected to remain constant at 6.9% and 0.9% on a quarterly and monthly basis, respectively, according to the consensus. The monthly core HICP is also expected to drop from its previous release of 1.3% to 1.1%, while the annual core HICP is expected to remain stable at 5.9%. As the Bank of England (BoE) gets ready to raise interest rates for the 12th consecutive time, inflation expectations in the United Kingdom have decreased significantly, which is good news for the Pound Sterling. As reported by Reuters, Citi said its monthly survey by market research firm YouGov revealed popular estimates for inflation in the next 12 months declined to 5.2% in April from 5.4% in March and forecasts for the next five to 10 years decreased to 3.6% from 3.7%.

AUDUSD Analysis

AUDUSD is moving in the Box pattern and the market has rebounded from the horizontal support area of the pattern.

Following a pause last month, the RBA increased the rate by 25bps today. The economy is experiencing increased inflation rates; the predicted annual inflation rate is 6.6%, but the March 2023 data indicates 6.9%. The tighter employment market and rising salaries, according to the RBA, will cause interest rates to rise at this meeting. There is a 50/50 likelihood that a 25 bps rate hike will occur in the second half of 2023, according to experts. After hearing about the rate hike, the Australian dollar increased.

After a pause in monetary policy last month, the RBA tightened it this month, sending the Australian Dollar soaring above 67 cents. The cash rate increased by 25 basis points to 3.85%. The bank stated that some more tightening of monetary policy may be necessary to guarantee that inflation returns to goal in a fair amount of time, but that decision would be made based on how the economy and inflation develop. They emphasised the labour shortage and the first uptick in pay. This week will see the release of Australian retail sales and trade data, with building approvals data coming out the following week. The chart below shows the Citibank Economic Surprise Index, which points to a potential beat for the next AUD fundamental data. Interest rate markets anticipated a 50/50 possibility of a 25 basis point boost later this year prior to the meeting. The market is readjusting and taking in the statement’s tonality now that it has arrived. The AUDUSD response was more abrupt. With headline CPI of 7.0%, slightly exceeding predictions of 6.9% year-over-year to the end of March and it was against 7.8% earlier, it appears that last week’s inflation data fanned some concerns.

GBPAUD Analysis

GBPAUD is moving in an Ascending channel and the market has reached the higher low area of the channel.

Instead of estimates of 6.7% and 6.9% for the same period, the RBA’s preferred metric of trimmed-mean CPI was 6.6% year-over-year. Since the second quarter of 2021, the headline CPI figure has exceeded the RBA’s mandated 2–3% inflation target, while the trimmed mean has done so since the first quarter of 2022.It wasn’t until May 2022 that the RBA began hiking the cash rate. This instance may have revealed the inadequacies of the trimmed mean measure. The middle 70% of the headline CPI basket is the focus of this adjusted inflation gauge. The 15% of the basket that climbed the most and least is therefore eliminated. Because of this symmetrical technique, if one side of the basket experiences significantly more drastic price changes, the elimination of the other side of the basket may not always fairly make up for it. The value of evaluating the underlying price changes using a core method, such as the trimmed mean, may not be as valuable as it has historically been when inflation pressures are shifting noticeably up or down. The RBA appears to be back in the inflation-fighting game based on today’s decision. Later this week, the Federal Reserve and the European Central Bank will meet, and the Bank of England will meet the following week. Interest rate markets have already factored in all three central banks’ 25 basis point increase.

AUDCHF Analysis

AUDCHF has broken the Descending channel in upside.

Prior to the UBS merger, Saudi Bank owned around 9.88% of the shares of Credit Suisse. At the moment, this holding equates to 0.5% of UBS shares. On Monday, Saudi Bank said that its first-quarter results exceeded expectations. The fall of Credit Suisse had no impact on their bank investments.

Once the Swiss lenders’ merger is complete, Saudi National Bank, the largest shareholder of Credit Suisse Group AG, will own roughly a 0.5% stake in UBS Group AG. Before UBS agreed to purchase its rival in a historic, government-brokered deal, the Riyadh-based bank, which is 37% owned by the kingdom’s sovereign wealth fund, held about 9.88% of Credit Suisse. Saudi National Bank stated that its 1.4 billion franc ($1.6 billion) stake in Credit Suisse had decreased by almost 20% by the end of 2022 and then by an additional 70% during the first three months of this year in its first-quarter earnings report, which topped estimates. It stated that the investment’s carrying value at the end of March was 1.3 billion riyals ($346.6 million). However, there was “no income statement impact” because the bank had irrevocably chosen to present subsequent changes in the fair value of the Credit Suisse investment through other comprehensive income, as permitted by the accounting standards, the Saudi lender said.

After Credit Suisse’s rival was brought dangerously close to bankruptcy by client withdrawals and a sharp drop in share price, capping years of scandals and losses, UBS and Credit Suisse reached an agreement to merge in March. Ammar Al Khudairy, the former chairman of the Saudi National Bank, resigned a few days after his remarks to Bloomberg TV contributed to the decline in stocks and bonds, which prompted the Swiss government to intervene and organise the acquisition. Credit Suisse “had no effect on Saudi SNB’s earnings, yet equity fell 3.1 billion riyals as comprehensive incomes were hit, trimming the lender’s CET1 ratio by about 45 bps, we calculate,” according to Edmond Christou, senior industry analyst at Bloomberg Intelligence.

AUDNZD Analysis

AUDNZD has broken the Descending channel in upside.

This week, New Zealand’s Q1 employment data will be released; the unemployment rate is predicted to increase from 3.4% to 3.5%. Normal employment change is anticipated to be 0.20 percent, while the quarterly employment change is anticipated to remain at 1.1%. The RBNZ will be pausing the interest rate in upcoming sessions due to fewer job gains and greater unemployment rates in New Zealand.

After failing to maintain a surge over 1.0760 in the Asian session, the AUDNZD pair has declined to within a few cents of 1.0740. Prior to the Reserve Bank of Australia’s interest rate decision, the cross is anticipated to continue in operation. Governor of the RBA Philip Lowe is predicted to maintain his impartial approach on policy. Inflation in Australia has been steadily falling over the last three months. Since peaking at 8.4% in December, the monthly Australian Consumer Price Index has already slowed, reaching 6.3% in March. Additionally, RBA policymakers are confident that a significant slowdown in the Australian economy is anticipated as a result of higher interest rates. This might put future Australian inflation under additional stress. In addition, the Australian Retail Sales report on Wednesday will be closely followed. It is anticipated that monthly retail sales will stay constant at 0.2%.

Investors are eagerly expecting the publication of the Employment statistics , planned for release on Wednesday, on the New Zealand front. Estimates predict that the employment change will remain constant at 0.2%. While the unemployment rate is projected to increase from its previous release of 3.4% to 3.5%. At 1.1%, the quarterly Employment Cost Index is expected to remain constant. The Reserve Bank of New Zealand (RBNZ) would be able to consider pausing the process of tightening policy if fewer jobs were added and the unemployment rate increased. Investors should be aware that RBNZ Governor Adrian Orr unexpectedly increased the Official Cash Rate (OCR) in April by 50 basis points to 5.25% in order to fortify the bank’s resistance to escalating inflation.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/