GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel.

The US Dollar lost ground against G10 currencies and non-yielding assets like Gold after the FED raised interest rates to 5.00-5.25% yesterday. This is the final rate hike of the year, and economists expect rate pauses or rate cuts.

Following today’s North American close, gold prices began to climb while the price of crude oil plummeted. The actions follow yesterday’s Federal Open Market Committee target rate increase of 25 basis points to 5-5.25%. On Wednesday, the US Dollar finished the day down against every G-10 currency, possibly supporting the price of gold. The rise in volatility in gold, oil, and other commodities may be reflected in the fact that the commodity-linked currencies of the AUD, CAD, and NZD have had a rough start to Thursday. Today, the COMEX front contract for gold reached US$2,085.4 per ounce. Since the historic high of US$ 2089.2 in August 2020, that is the highest level. Although it exceeded the US$ 2,078.8 high set in March 2022, a Triple Top is now in effect unless a new high is set. A Double Top extends into a Triple Top. The price of COMEX gold futures priced in NYMEX WTI barrels of crude oil is at its highest level since February 2021.

Both gold and oil fell back to close levels from Wednesday after the Thursday opening bustle as markets adjusted to the Fed rate move. With cuts factored in as early as the third quarter, interest rate markets seem to be calling the Fed’s bluff. The pivot in some of the language looks to have received a lot of focus from the market. Before listing the considerations that will be taken into account for making decisions, the statement from the March meeting stated, “The Committee believes that some more policy firming may be needed. This sentence was altered in the May meeting statement to read, “In assessing the extent to which additional policy firming may be required. This appears to be what caused the market to stop expecting hikes and start anticipating impending cutbacks. Fed Chair Jerome Powell underlined that this isn’t always the case during the news conference following the game. He repeatedly stated that moving forward, each choice would depend on evidence and be evaluated on an ongoing basis at each meeting. Despite this, Treasury rates continued to decline, with the 2-year bond touching 3.81%, a significant decline from the peak of 4.29% last month. With the 10-year rate hovering around 1.15%, down from the peak of 1.38% reached on Monday, real yields are still stagnant. The market-priced inflation rate determined from Treasury inflation-protected securities with the same tenor less the nominal yield results in the real yield. Unsurprisingly, given the frantic price movement, gold volatility increased slightly. Similar to how the VIX index gauges S&P 500 volatility, the GVZ index gauges the volatility of gold.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel.

If an inflation target of 2% is met, the IMF predicted that Japan’s ultra-loose monetary policy will soon shift to one that is tightening. If the Bank of Japan raises interest rates, a lot of investors will switch their portfolio assets to JPY bonds.

In 2028, the Chinese economy will develop by 4% less because productivity and investment will increase more slowly.

The International Monetary Fund issued a “uncertainty” alert on Thursday on the future of Japan’s monetary policy, stating that a potential departure from ultra-low interest rates might have a significant effect on international financial markets. The risks to Asia’s economic outlook were also highlighted by Krishna Srinivasan, director of the IMF’s Asia and Pacific Department, including weaker exports to advanced economies, slowing productivity in China, and a fragmentation of global trade. We anticipate a downturn in productivity and investment in the Chinese economy over the medium term, which would bring growth below 4% by 2028, he said. Additionally, Srinivasan warned during a briefing at the Asian Development Bank’s annual meeting in Incheon that there is a danger that the world economy will split into trading blocs, which could be especially devastating for Asia because of its reliance on exports. Japan continues to be an outlier with inflation remaining mild, despite the fact that this could change, while most Asian central banks must continue tightening monetary policy.

In Japan, there is uncertainty about the course of monetary policy due to rising inflation, according to Srinivasan. Japanese investors, who have sizable positions in foreign debt instruments, could be affected by changes in Japan’s monetary policy that result in future increases in government bond yields, according to Srinivasan. These investors’ portfolio rebalancing might lead to an increase in global yields, which would result in portfolio outflows for some nations, the author continued. Market rumours are widespread that the Bank of Japan may change its bond yield control policy in the upcoming months as a result of inflation exceeding its 2% target. The BOJ kept interest rates extremely low on Friday, but also revealed a strategy to evaluate previous monetary policy decisions, laying the framework for new governor Kazuo Ueda to gradually wind down the enormous stimulus programme his predecessor had implemented.

According to Srinivasan, China’s quick rebound following the lifting of restrictions brought on by the pandemic will probably boost exports to some Asian nations, notably South Korea. While South Korea’s overall inflation is slowing due to lower energy costs, the core rate of inflation, which excludes the cost of food and energy, has not yet decreased significantly, according to him. Accordingly, he said, the Bank of Korea (BOK) must avoid a premature monetary easing while minimising the risk of tightening policy excessively. Considering all of these factors, the BoK rightly postponed rate increases at its meetings in February and April while keeping the door open for additional increases in response to new data.

USDCHF Analysis

USDCHF has broken the Descending channel in upside.

Sergio Ermotti, chief executive officer of UBS, stated that UBS will buy assets from Credit Suisse by the end of May or the beginning of June. This is the positive effect of the Swiss Franc’s decline against other currencies. Under intense political and public pressure, Credit Suisse and UBS agreed to merge in March.

The merger between UBS and Credit Suisse is expected to be completed by the end of May or the beginning of June, according to UBS Chief Executive Sergio Ermotti on Wednesday. At the Finanz ’23 conference in Zurich, Ermotti was giving a speech. In a transaction quickly brokered by Swiss authorities, UBS agreed to acquire its struggling rival Credit Suisse for 3 billion Swiss francs ($3.37 billion) and stated it would assume up to 5 billion ($5.61 billion) in losses. Switzerland’s largest bank is reportedly working on spinning off the Swiss division of Credit Suisse amid mounting public and political pressure.

USD Index Analysis

USD Index has broken the rising wedge pattern in downside.

Following yesterday’s 25 bps rate hike by the FED, the US dollar fell. Based on US economy data, the FED made comments about potential rate increases or hikes that might be postponed.

After falling into the New York close following yesterday’s Federal Open Market Committee target rate increase to 5-5.25%, the US dollar is still under pressure today. The idea that the Fed has stopped raising interest rates looked to be the root of the weakening, as the interest rate market is currently pricing in a rate cut for the third quarter. Despite assurances from Fed Chair Jerome Powell that future meetings will be data-dependent and necessitate ongoing evaluation, this is the case. The statement from the March meeting began, “The Committee anticipates that some additional policy firming may be appropriate,” before listing the considerations that will be made. This sentence was changed to, In considering the extent to which additional policy firming may be required, in the statement from the May meeting. The market appears to be preparing for a recession and consequent loosening of monetary policy. If the downturn proceeds in that manner but inflation stays much above the Fed’s 2% target, the US economy may face difficulties in the future.

Treasury yields fell following the FOMC meeting, which contributed to the US dollar’s decline. The presumed safest currencies, the Swiss franc and the yen, suffered the worst losses. The USDCHF hit a 15-month low around 0.8800, while the DXY index is still hovering around 2-year lows. After both currencies received positive economic data, the Australian and New Zealand dollars have strengthened. March saw an increase in NZ building permits of 7% month over month. The second-highest reading on record for Australia’s expanding trade surplus, for the month of March, was AUD 15.27 billion. Though futures indicate a steady start to today, Wall Street ended its cash session lower. APAC equities indices are uneven, with Japan still closed and Chinese markets opening for the first time this week. Crude oil was slammed lower at the start of the Asian session, but gold soared higher at the same time. Since then, both markets have returned to levels close to their opening levels. WTI crude hit a 17-month low at US$ 63.34 barrel, more than 7% below the New York close that had occurred just moments earlier. With a price of 2,085.4 per ounce, the front month COMEX gold futures contract’s high came close to breaking all previous records.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the pattern.

Today’s ECB monetary policy meeting is set, and it is anticipated that a 25 bps rate increase will be made to combat inflation readings that are above the 2% target level.

Three consecutive rate increases of 50 basis points established the current rate of 3.50%; if it were raised today, it would become 3.75%.

Strong inflation and a tight labour market are prevalent in the Euro region, which the ECB must control without harming banks or the general population by raising interest rates.

As its lengthy battle against persistent inflation continues, the European Central Bank will raise interest rates for the seventh meeting in a row on Thursday. Only the size of the move is still up for debate. In an effort to halt the uncontrollable rise in prices, the central bank of the 20-nation euro zone has already increased rates by a record-breaking 350 basis points since July. However, achieving the 2% target for inflation will take years, so policymakers will have no choice but to tighten the economy’s financial conditions once more this month and moving forward. The most likely result after three straight 50 basis point increases is a move of 25 basis points, while a larger rise is still possible given that this is almost certainly not the conclusion of a record tightening cycle. A consensus among policymakers on the signals to provide regarding upcoming rises might be the deciding factor. The Governing Council’s comfortable majority of conservative hawks is leaning towards a larger rise. Even though some counterparts, most notably the U.S. Federal Reserve, are close to reaching their own interest rate peaks, they have indicated they could live with a lower advance as long as the ECB indicates that May is not the end of its hikes.

How large of a majority Christine Lagarde wants to support the decision will be another problem. Given the right direction, many hawks could accept a smaller move, but if the hike is larger, their dovish colleagues are likely to voice loud opposition, resulting in the ECB once again speaking with many voices, which has been viewed as a weakness for years. An agreement to stop reinvesting maturing debt purchased through the ECB’s 3.2 trillion euro Asset Purchase Programme starting in July might be included in the compromise. This modest move would further reduce the bank’s excessive balance sheet, even if the impact on inflation would be minimal. Markets expect a change of 25 basis points with a 75% to 80% probability, and the vast majority of experts surveyed by Reuters also predicted the lower increase. After that, rates are predicted to peak at about 3.75% in September. The U.S. Federal Reserve raised interest rates by 25 basis points on Wednesday and hinted that it would halt further hikes, supporting a potential ECB downshift. Even while the dovish arguments appear to be multiplying, economic fundamentals offer plenty of material for both sides of the debate.

The euro zone economy barely expanded last quarter, and lending data revealed the greatest decline in credit demand in over ten years, supporting the argument for a lesser move. This suggests that previous rate hikes are beginning to affect the economy. If pushed too far, this credit decline could turn into a full-blown credit crunch, which would drag down growth, which is now barely positive. The ECB’s deposit rate, which is currently at 3%, is already limiting economic activity, and underlying inflation has also stopped increasing, at least temporarily. Moving to 25 bps would provide the ECB more flexibility to address both upside and downside threats to growth and inflation, according to Davide Oneglia of TS Lombard. Therefore, a 25 bps increase is not always “dovish.” For the time being, we continue to advocate for a 3.75% ECB terminal rate.

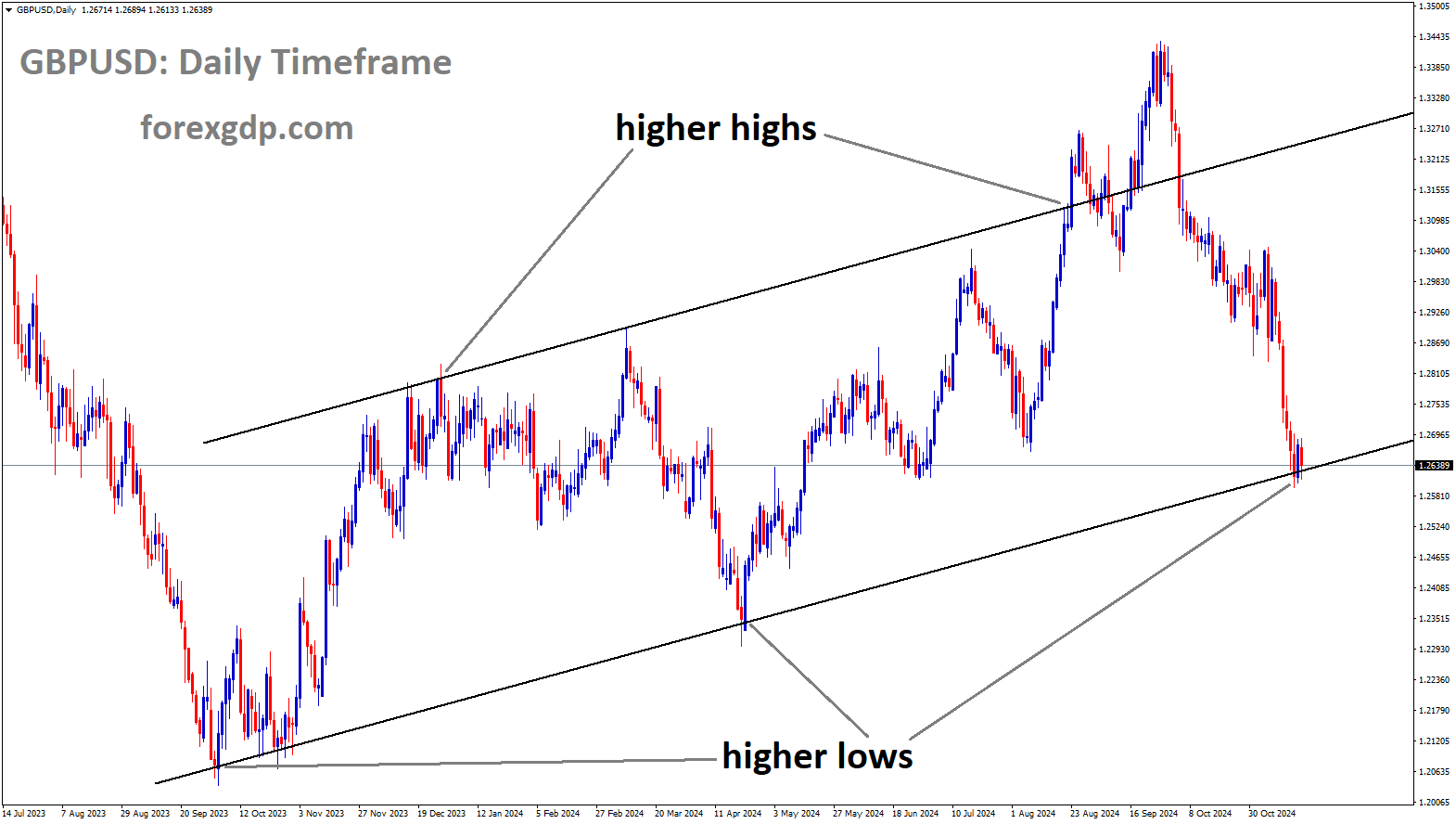

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has reached the higher high area of the channel.

The Bank of England is expected to increase interest rates at its meeting on May 11 in order to keep inflation below double digits, according to economists. Although the UK’s job market is stronger, consumer spending is higher, fuel prices have decreased as a result of OPEC+’s production cuts, UK inflation is still only in the double digits.

Despite the fact that inflation is still hovering around double digits and investors are preparing for a cycle of rate hikes to linger into the summer, UK economists only expect the Bank of England to raise rates by one more quarter point.According to a Bloomberg survey of analysts, the majority believe the key rate will raise to 4.5% on May 11 before remaining unchanged and pausing the most aggressive sequence of hikes in forty years. Despite a wealth of evidence demonstrating that both the economy and inflation are shockingly healthy, this is the case. The outcomes are significantly different from market expectations, which tilt towards rates peaking at 5% by September. After the US Federal Reserve’s decision this evening and the European Central Bank’s decision on Thursday, that wager may change. One further increase is anticipated from both of those central banks. The data in recent weeks, particularly those related to inflation and wages, have changed our initial assessment that this would be the pause point, according to Elizabeth Martins, senior economist at HSBC. Although the language and tone may not change much in May, the picture might be very different by June.

In the UK, the money markets have changed rapidly. Investors are betting that the bank rate will continue to rise until it is above 4.90% by September despite having completely priced in a quarter point interest-rate increase this month. Even up to Tuesday, before market concerns about US regional banks erupted, traders were betting on terminal rates exceeding 5%. Less hawkish economists are present. A third of the 30 analysts in the UK predict two more increases to 4.75%, while almost 60% predict rates will peak at 4.5%. Only two, including Goldman Sachs, anticipate rates to reach 5%. On the nine-member Monetary Policy Committee of the BOE, the majority anticipated a 7-2 split between those voting for another hike and the doves calling for a pause. Some predict that after being alarmed by recent data, the more hawkish rate-setters, particularly Catherine Mann, may support a larger hike. They also unanimously anticipate that the BOE will raise its predictions for both inflation and GDP for this year and the following year.

Between its meetings in May and June, the attitude of the BOE policymakers, led by Governor Andrew Bailey, could change significantly. The BOE will have seen two more months’ worth of inflation statistics by the next meeting on June 22, with a significant decline anticipated in April’s reading as the spike in energy prices last year is removed from the annual figures. Rate increases after next week’s meeting will be “highly data dependent,” according to UBS analyst Anna Titareva. The signals for the future rate path would be the main topic at the next meeting, she said. Our present baseline predicts no additional rises after May because inflation and wage expectations lead to a gradual relaxation and because there is significant uncertainty over the effects of the tightening that has already been delivered. The experts anticipate that after the first year, when the BOE sold about £10 billion worth of bonds every three months, the economy will continue to grow at the same rate due to quantitative tightening. The balance sheet of the BOE was expected to finish shrinking around £400 billion or £500 billion, down from its height of £895 billion after the epidemic, as predicted by just over half of respondents.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

The Australian trade surplus for the month of March reached a peak of A$ 15.27 billion, above estimates of A$12.65 billion and A$13.87 billion for the corresponding months. Coal and iron ore were the two main exports, increasing to 20% and 7% respectively. Australian dollars are stronger versus other currency pairings as a result of overall export growth of 4% and import growth of 2%.

According to figures released on Thursday, Australia’s trade surplus increased to a nine-month high in March, largely due to a resurgence in commodity exports as demand resumed after a two-month slump. According to figures from the Australian Bureau of Statistics, the nation’s trade balance in March totaled A$15.27 billion (at an exchange rate of A$1 = $0.6671). The amount was greater than both February’s reading of A$13.87B and estimates for a surplus of A$12.65B. The trade balance for Australia was likewise at its greatest point since it reached a record high of A$17.13 billion in June 2022. The country’s exports increased by 4% in March compared to the previous month, with a surge in shipments of metal and mineral ore providing the biggest boost to the total. The major exports of the nation, coal and iron ore, increased by about 20% each, while LNG shipments increased by 7%.

Due to weaker demand in its two largest markets, China and Japan, the nation’s commodity exports had decreased for two consecutive months. However, slightly improving economic conditions in China are probably what contributed to the rise in commodity demand over the past month. However, despite the fact that China’s post-COVID economic recovery now appears to be fizzling out, commodity exports were still lagging behind levels seen in January. The nation, which is Australia’s top trading partner, surprisingly saw a decline in manufacturing activity in April, according to data released on Thursday.

Additionally contributing to the overall trade surplus in March were increased exports of agricultural products from Australia, specifically meat and cereal. However, Australian imports increased by 2% following a significant decrease in the previous month. The main factors influencing the reading were increasing purchases of capital goods including machinery and industrial equipment as well as rising debits from international trips. Despite obstacles to local economic growth from higher inflation and rising interest rates, the improved trade balance demonstrates the resilience of Australia’s export-driven economy. Strong exports may also offer the Reserve Bank of Australia more space to raise interest rates in the future as it fights against inflation that is out of control.

NZDUSD Analysis

NZDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

After the RBNZ rate hike, there is no liquidity pressure on the banks, according to the Bank of New Zealand, which reported a half-year net profit of $805 million, an increase of 13.5%. When repaid at higher interest rates than before, public home loans were impacted by the RBNZ rate increase. However, the $15 million in savings for bank customers due to BNZ’s reduced fees for international payments.

According to the bank, this was caused by increasing revenue, which was “somewhat offset by higher operating expenses and higher credit impairment charges… BNZ has solid liquidity, is steady, and is well-capitalized. The company’s chief executive, Dan Huggins, acknowledged that many of its clients were having difficulty keeping up with the rising cost of living. We are familiar with our customers and are aware of the pressure that rising living expenses are placing on many New Zealand households, especially those with mortgages. Although we are confident that our home loan customers can manage the current environment of higher interest rates, for some it will be difficult. As the Reserve Bank keeps raising the official cash rate in an effort to lower inflation, home loan rates have increased. It sits at 6.7%. The four major banks, BNZ, ASB, ANZ, and Westpac, each reported eye-popping after-tax earnings of $6 billion in the previous fiscal year. All are owned by Australians.

All major parties, with the exception of Labour, and Consumer NZ, have supported requests for a Commerce Commission investigation into bank profits and competition. High profits and little innovation, according to Consumer NZ Chief Executive Jon Duffy, show that consumers have few options, and the top four banks now in operation are in a really secure position where they can continue to increase their profits. Huggins claimed that the bank has eliminated or lowered several fees over the previous six months, saving consumers $15 million annually. On BNZ’s well-known TotalMoney account, this includes eliminating international transaction fees and monthly account fees.

GBPCAD Analysis

GBPCAD is moving in an Ascending channel and the market has reached the higher low area of the channel.

The overall poverty rate in Canada increased to 7.4% in 2021 from 6.4% in 2020 and decreased from 14.5% in 2015. The Canadian government organises investments for social programmes and income supplements so that Canadians can spend their lives in a cycle that is healthy. Because of the challenging job market, one reason that poverty has declined is because the Bank of Canada has stopped raising interest rates.

The Canadian government took exceptional steps at the onset of the COVID-19 epidemic to assist Canadians and guarantee a strong economic recovery. By March 2023, there were 865,000 more employed Canadians than there were prior to the pandemic. But rising inflation rates are making it hard for many Canadians to make ends meet, and rising costs for necessities are adding unnecessary stress. The Canadian government is still giving Canadians much-needed respite despite global inflation and rising prices. The results of the 2021 Canadian Income Survey, which Statistics Canada released today, revealed that the rise in median market income more than compensated the loss seen in 2020 and raised it 3.5% above its level in 2019. The findings also revealed that, when the temporary emergency pandemic payments were discontinued in 2020, Canada’s general poverty rate was 7.4% in 2021. This rate is lower than the pre-pandemic rate for 2019 (10.3%) and is almost half of the baseline rate for Canada’s legally mandated poverty reduction targets, 2015 (14.5%).

2.3 million fewer Canadians, including 653,000 less children, 11,000 fewer seniors, and 556,000 fewer people with disabilities, were living in poverty in 2021 compared to 2015. The Government is still dedicated to achieving its target of a 50% decrease in poverty from 2015 levels by 2030. The rising cost of living and its effect on household and personal finances are major concerns for many Canadians. To combat poverty, alleviate food insecurity, and improve wellbeing, the Canadian government is continuing to invest heavily in targeted social programmes and income supplements. Examples include the expansion of the Canada Workers Benefit, the creation of a national system for early learning and child care, the new Canada Dental Benefit, and the proposed one-time grocery rebate announced in Budget 2023.

Crude Oil Analysis

Crude Oil price is moving in the Descending channel and the market has reached the lower low area of the channel.

Following yesterday’s FED rate hike of 25 basis points and concerns about a US economic recession, oil prices plunged. Already, OPEC+nations are slowing the growth of oil demand by reducing oil production by 1 million Bpd. Oil usage decreased as a result of global banks’ increases in interest rates.

Crude oil prices fell sharply on Wednesday, extending losses from the previous session and reaching their lowest point since March 24. This decline was attributed to escalating macroeconomic headwinds, particularly the potential for a possible medium-term U.S. recession. WTI futures were down around 5% to trade at $68.05 per barrel in early afternoon trading in New York, totaling a loss of more than 11% since the beginning of the month, making it abundantly evident that bears are once again in charge of the wheel. Many traders predict that the North American economy will suffer a painful downturn later this year as a result of rising borrowing costs, with the Federal Reserve’s funds rates at their highest level since 2007. This is despite the fact that the U.S. outlook is still in flux. Although it is impossible to accurately predict the future, a recessionary environment should, at the very least, sharply reduce fuel demand, increasing downside risks for energy commodities that are sensitive to growth. This is because the United States is the world’s largest consumer of petroleum.

The continuous turmoil in the US banking industry, which started in March, is changing the landscape in yet another unexpected way. Investors worry that the crisis’s aftereffects may considerably tighten credit conditions in the upcoming months, severely dampening economic growth. This might accelerate oil’s downward trend, especially in light of the fact that recent OPEC+ production cuts and Chinese demand haven’t had any significant long-term effects on the energy markets. Technically speaking, oil prices have recently broken through two significant support levels, the first of which is roughly at $71.50 and the second of which is roughly at $70.00. These bearish breakdowns, which have accelerated the selloff, could pave the way for a quick retest of the $66.25 area. The 2023 lows would come into focus in the event of more decline. Initial resistance for a bullish reversal is seen at the symbolic $70.00 level. By successfully navigating beyond this obstacle, the market might draw in more buyers, which would create the ideal circumstances for a return to $71.75.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/