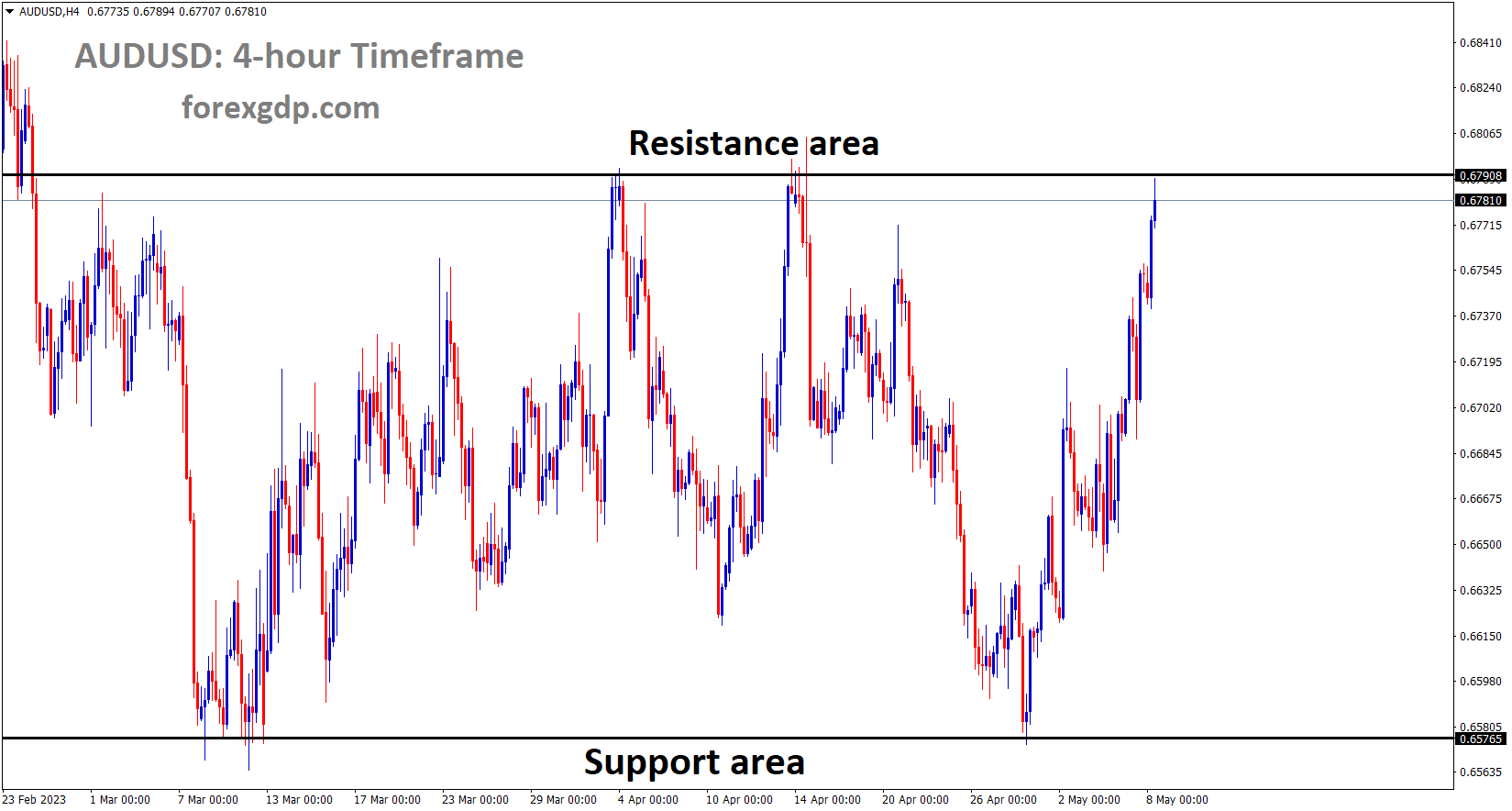

AUDUSD Analysis

AUDUSD is moving in the Box pattern and the market has reached the resistance area of the pattern.

The Australian government likes to add A$ 14.1 billion to the budget to help people and businesses with the rising cost of living. While households and businesses can operate well without being affected by inflation, this does not lessen the inflation rate.

An additional 5% cigarette tax and higher taxes on oil and gas companies are responsible for this expenditure. As soon as the inflation rate drops, Australia’s deficit will decrease.

The federal budget for Australia’s center-left Labour administration will contain A$14.6 billion ($9.84 billion) over four years for cost of living assistance for families and companies, which it promises won’t fuel inflation. The report also emphasises the Reserve Bank of Australia’s Friday warning that, in light of weak productivity growth, rising energy prices, and an increase in rents, inflation risks were on the rise. Treasurer Jim Chalmers stated that the cost-of-living relief that doesn’t increase inflation will be the main focus of the budget while providing suggestions for the federal budget to be announced on Tuesday. The legislator also mentions that many are strapped for cash. This Budget has been carefully calibrated and created to relieve rather than increase pressure on the cost of living.

After the Reserve Bank of Australia last week shocked markets with a rate rise, bucking trader expectations for an extended pause, Chalmers has consistently stressed his budget would be limited on expenditure so as to not add to inflationary pressures while still providing some relief. The most recent relief measures follow the government’s announcement of an additional 5% cigarette tax and an additional A$2.4 billion in tax on oil and gas companies, together with A$11.3 billion put aside for pay increases for aged care workers over a four-year period. The budget is anticipated to demonstrate that Australia’s deficit has significantly decreased as a result of tax windfalls from the export of commodities, but the future will be sombre as fiscal troubles loom.

GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

After the US NFP statistics showed strong numbers on Friday, gold prices fell sharply from highs. In contrast to non-yielding assets like gold, yielding assets like US Treasury bonds benefit more from FED rate increases. US CPI numbers due out this week that were lower than anticipated compared to the prior reading are bullish in the short term for gold.

After taking into account the market-moving potential of the resurgent regional bank instability and the prospect for weaker fundamental data in the US, the bullish label that comes with this weekly forecast was decided upon. A negative pressure on economic activity and prices is asserted by cumulative tightening, which includes multiple increases in the Fed funds rate, quantitative tightening, and tighter credit conditions (caused by financial instability). Although headline inflation has decreased well, when the April CPI data is issued the following week, core inflation must also do the same. The continuation of expected rate reduction in the market for H2 is positive for the non-interest bearing metal. Despite a somewhat protracted process, markets realised that a resolution to the First Republic Bank situation was inevitable last weekend, and in the early hours of Monday morning, a deal was reached with JP Morgan being viewed as the best option to take on depositors. However, a day later, the US regional banking index fell as the share prices of PacWest Bancorp and Western Alliance resumed their separate declines.

Markets experienced a new wave of widespread concern, and investors rushed to buy gold. A day after the gold volatility index made a dramatic swing higher, the price of the precious metal set a new record high of about $2081.80 for an ounce. Due to its dual benefits as a safe haven and as a beneficiary of the currently priced-in environment of reduced interest rates, gold has emerged as an appealing option.Historically, the 10-year US Treasury yield, which declined at the start of the week, has shown a strong negative association to gold. Treasuries often follow the same path if markets predict a lower Fed funds rate, therefore lowering yields are expected to benefit gold prices going forward. Everything hinges on core inflation and the Fed’s ability to halt the spiralling bank failures that are currently taking place.Up until the massive and abrupt decline that followed Thursday’s record all-time high, gold seemed to be a runaway market. Given the size of the bullish surge, the pullback is expected; nevertheless, as of Friday, following the NFP surprise, the move has already recovered about two thirds of the initial advance.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

According to the Bank of Japan meeting minutes from today, an ultra-easy monetary policy can help achieve the country’s 2% inflation target this year. In the long run, inflation will decline while wages can rise. In the minutes of the Bank of Japan meeting, members made a variety of ideas, but the conclusion was that an easy monetary policy should continue until the world’s economic difficulties are resolved.

According to the Bank of Japan’s March monthly Monetary Policy Meeting minutes, several members stated that they must be watchful to avoid the possibility that inflation may increase more quickly than anticipated. Members concurred that the economy of Japan was surrounded by a significant degree of uncertainty. If global commodity prices rise more than anticipated, a number of participants indicated, cost-push price pressure may endure longer than anticipated. Several participants stated that there were promising signals that the BoJ price target will be reached. A few members stated that while considering the cost and balance of effects of the stimulus, it was necessary to retain the current level of stimulation. One participant asserted that the BoJ should place more emphasis on the danger of a premature policy shift than the risk of a late policy change.

One participant stated that because a change in monetary policy would have an impact on so many different companies and markets, it was important to debate the issue carefully. One participant stated that BoJ must act to enhance market performance, especially that of the corporate bond and swap markets, if necessary. One participant raised the possibility that high levels of salary and price growth might be permitted as long as they are stable and constructive.

Several participants argued against the validity of such theory, arguing that historically, inflation tends to fluctuate in erratic ways when it is too high. Several members felt it was appropriate to discuss changing the BoJ’s policy recommendations related to the COVID-19 outbreak.

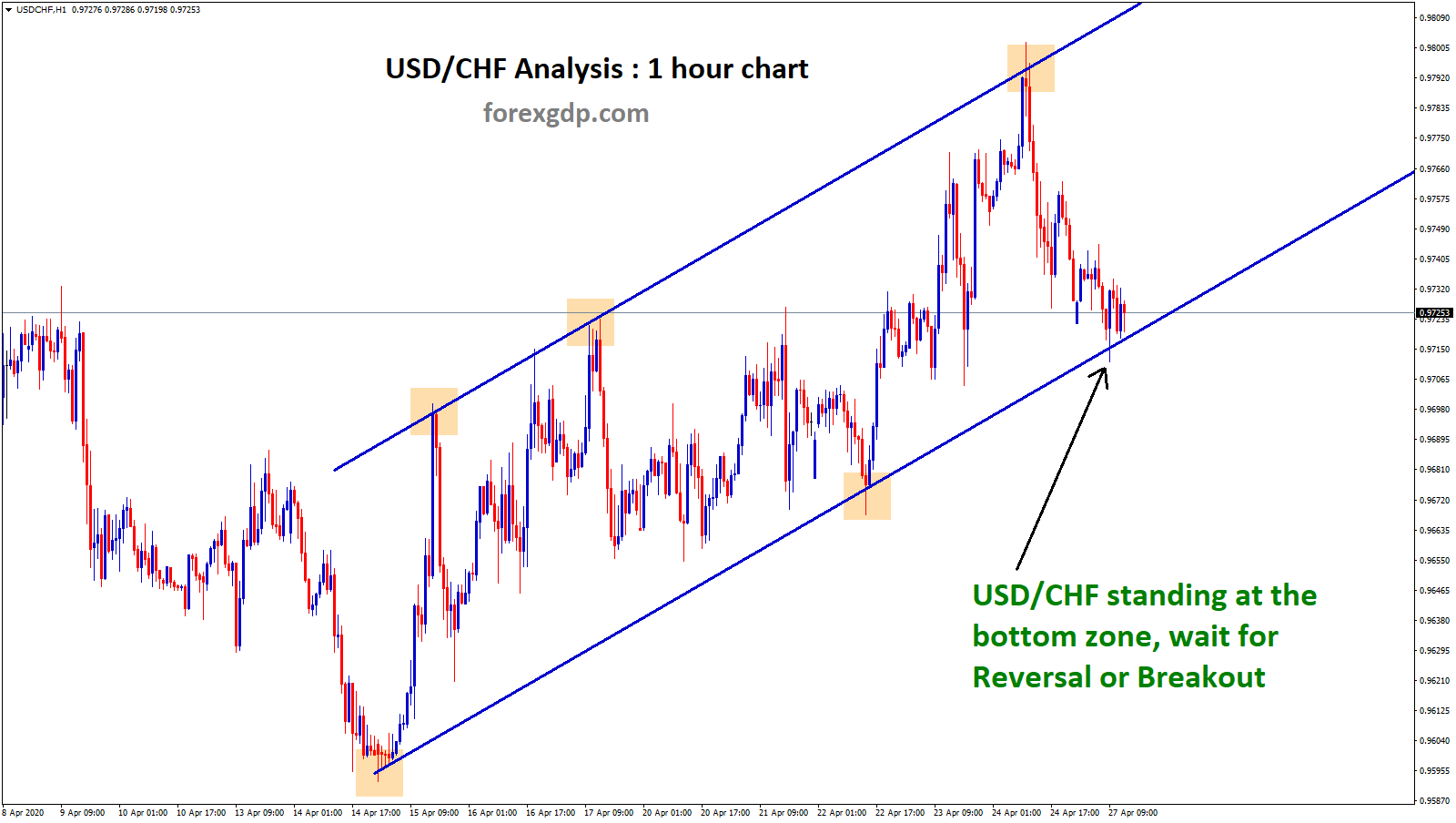

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Swiss inflation was 2.6% as opposed to the projected 2.85% and the previous estimate of 2.9%. For SNB policymakers, this information is now advantageous. However, on Friday, the Market fell sharply against Counter pairings. In the month of June, SNB may increase rates once more.

In the Asian session, the USDCHF pair is moving back and forth close to the round-level support of 0.8900. Investors are waiting for the Wednesday release of the Consumer Price Index (CPI) data for the United States, which has caused the Swiss franc asset to move sideways. After a Friday that was extremely positive, S&P500 futures are showing marginal losses in the Asian session, signalling a small amount of caution in the otherwise upbeat market atmosphere. After a less confident fall, the US Dollar Index (DXY) has retreated and is now seeking to drop farther lower below the immediate support level of 101.17. Despite a strong comeback on Friday following a positive US employment data, the USD Index gave up gains after realising that the news was tainted. The disclosed figure for payroll additions for March was reduced downward from 263K to 165K, indicating that new additions were just 2% more than the earlier figure. From a consensus estimate of 3.5%, the unemployment rate decreased to 3.4%.

Investors are now focusing on the Wednesday publication of US inflation data after the riddle surrounding the US Nonfarm Payrolls. The monthly headline Consumer Price Index (CPI), according to the preliminary report, increased by 0.4% in April as compared to a 0.1% pace seen in March. The core CPI increased by 0.3%, which was less than the 0.4% increase seen in March. Annual CPI for the Swiss currency dropped to 2.6% from the consensus estimate of 2.85 and the previous release of 2.9%. While the street was expecting a 0.5% increase, monthly inflation remained unchanged. Policymakers at the Swiss National Bank (SNB) may feel relieved as a result of this.

USD Index Analysis

USD Index is moving in the Box pattern and the market has reached the horizontal support area of the pattern.

After Friday’s Non-Farm Payrolls report came in stronger than anticipated (253k printed versus 185K projected), the US dollar is slightly up from lows. The predicted 3.5% unemployment rate was reduced to 3.4%, and average hourly earnings increased by 4.4% year over year.

However, due to the bank liquidity shortage and the bank crisis that occurred in 2023, the FED is predicted to implement rate cuts of 75 basis points by the year’s end.

The Federal Reserve rate decision caused the US dollar to carefully end the week down. Rates were increased by 25 basis points by the central bank, which also hinted at a break in the cycle of tightening. Chair Jerome Powell attempted to emphasise during his news conference that the committee’s outlook did not currently support rate reduction. Markets had approximately a 50% chance of a rate cut by July after the Fed. Then came Friday’s release of the non-farm payrolls. The economy created 253k new employment in April. Once more, this result was substantially greater than the predicted 185k. Unexpectedly, the unemployment rate dropped to 3.4% while the average hourly wage increased by 4.4% year over year. Despite this positive print, July rate-cut forecasts have only been modestly reduced by overnight index swaps. This possibility is now just approximately 40.5% likely.

The US Dollar may now be in a positive position going forward as a result. Members John Williams, Christopher Waller, James Bullard, and others will speak on the Fed. The US Dollar could be in for a treat if officials maintain their downplaying of expectations for near-term easing. Additionally, the upcoming US inflation report will be closely watched by the markets. CPI is anticipated to remain constant on Wednesday at 5.0% y/y, the same as in March. The core print is assessed to be somewhat ebbing, from 5.6% to 5.5%. More evidence of price pressures that are more persistent might support the dollar’s gain, particularly if risk aversion hits Wall Street and increases demand for safe-haven assets.

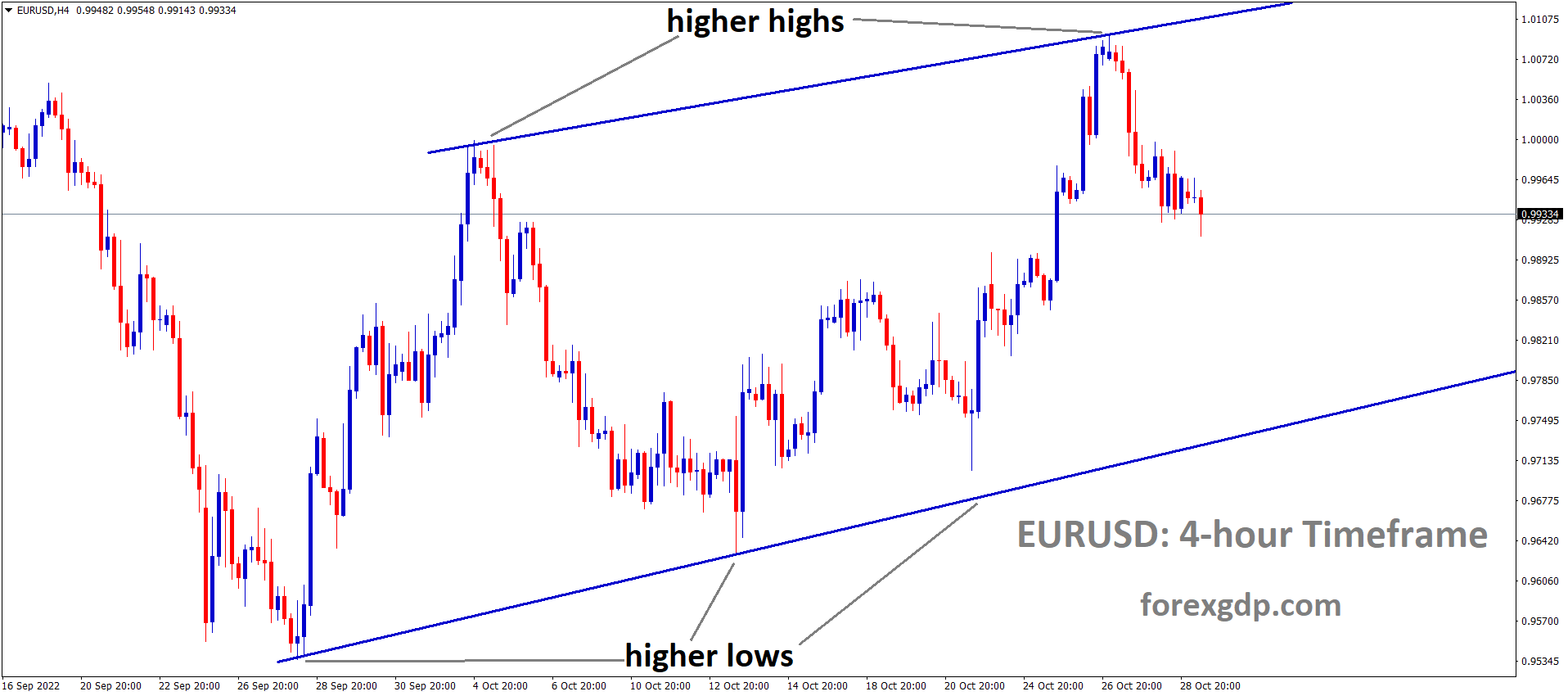

EURUSD Analysis

EURUSD has broken the descending channel in upside.

Klass Knot, president of the Dutch central bank and a member of the ECB Governing Council, claimed that ECB rate increases are bringing down inflation rates, which is good for the Eurozone economy. Francois Villeroy, the CEO of France Bank, added that additional modest rate increases are welcome in a statement released on Friday. In advance of the German CPI, the euro is strengthening versus other currency pairs, and the ECB Governing Council has indicated that additional rate hikes may be feasible.

Bulls in the EUR/USD currency pair maintain control around 1.1040 as it renews its intraday high and rises 0.15% on the day before Monday’s European session. The hawkish remarks from a European Central Bank official and the US Dollar’s general weakness amid mixed sentiment may be responsible for the Euro pair’s recent gains. Klaas Knot, president of the Dutch Central Bank and a member of the ECB board, stated over the weekend that although ECB interest rate increases are beginning to have an impact, more will be required to keep inflation under control. Francois Villeroy de Galhau, president of the Bank of France and a member of the ECB Governing Council, said on Friday that there will likely be a number of additional increases.It should be noted that the US Dollar Index, which has fallen 0.13% to 101.15 as of press time, represents one more attempt to breach a three-week-old ascending support line. Even though the positive headline figures allowed James Bullard, president of the St. Louis Federal Reserve, to retain his bullish view, the downward revision of the US Nonfarm Payrolls (NFP) could be the cause of the dollar’s most recent depreciation.

Ahead of Tuesday’s meeting between US President Joe Biden, Republican House Speaker Kevin McCarthy, Republican Senate Minority Leader Mitch McConnell, and top congressional Democrats at the White House to discuss the debt ceiling issue, there are also hopes that US policymakers will be able to address looming default fears. It’s important to note that according to Reuters, US Treasury Secretary Janet Yellen on Sunday issued a stern warning that failure by Congress to act on the debt ceiling may result in a constitutional crisis that also calls into question the creditworthiness of the federal government.

Other factors, such as the recent positive performance of US IT companies and the conflicting opinions surrounding the US banking industry, have weighed on the US Dollar while depressing Treasury bond yields. However, following a great run-up on Friday, the S&P 500 Futures print slight losses near 4,147, while the US 10-year Treasury note yields fell 1.5 basis points to 3.43%, under pressure for the third straight week. Looking ahead, movements in the EURUSD will be influenced by US and German inflation statistics as well as possible European Union sanctions on China due to its alleged involvement in the Russia-Ukraine war.

EURCAD Analysis

EURCAD is moving in an Ascending channel and the market has reached the higher low area of the channel.

The Friday Canadian Job Reports were better than anticipated, which helped the CAD gain ground against other currencies. Employment increased to 41.4K, up from 34.7K previously and 20K predicted. The unemployment rate was 5.0% as opposed to the predicted 5.1%.

It is widely anticipated that the Bank of Canada would raise rates at its upcoming meeting due to strong job growth.

During early Monday morning in Europe, USDCAD remains under pressure at its lowest levels in three weeks, close to 1.3380. Despite this, the Loonie pair fell the most in four months the day before despite a positive Canada jobs data and a dismal US Nonfarm Payrolls report. The increase in the price of oil, Canada’s principal export, strengthened the quote’s bearish performance. The April jobs data for Canada was positive, with Net Change in Employment increasing by 41.4K versus the 20K forecast and 34.7K in the prior month. Additionally, the unemployment rate remains at 5.0% despite market expectations for it to increase to 5.1%, while average hourly wages and the participation rate stayed constant at 5.2% YoY and 65.6%, respectively. Positive Canadian employment data and hawkish remarks from Bank of Canada Governor Tiff Mackem have a negative impact on the USDCAD exchange rate. However, despite hawkish remarks from James Bullard, president of the St. Louis Federal Reserve, a lower revision to the US Nonfarm Payrolls overshadows the positive headline figures and weakens the US Dollar.

Crude Oil Analysis

Crude Oil price is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Amid a weaker US Dollar and cautious optimism in the market, WTI crude oil prints a three-day uptrend as it continues a corrective comeback from the lowest levels since December 2021 to $71.70 heading into Monday’s European session. However, anticipation for US President Joe Biden’s meeting with Republican House Speaker Kevin McCarthy, Republican Senate Minority Leader Mitch McConnell, and top congressional Democrats to discuss the debt ceiling issue on Tuesday at the White House also affects the price of USDCAD. It’s important to note that according to Reuters, US Treasury Secretary Janet Yellen on Sunday issued a stern warning that failure by Congress to act on the debt ceiling may result in a “constitutional crisis” that also calls into question the creditworthiness of the federal government. In this environment, the US 10-year Treasury note yields declined 1.5 basis points to 3.43%, under pressure for the third consecutive week, while the S&P 500 Futures print slight losses near 4,147 following a great run-up on Friday. A wildfire disaster in Alberta, the main oil-producing province of Canada, presents a challenge for USD/CAD bears before the important US Consumer Price Index for April.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has reached the higher high area of the channel.

The US NFP report last Friday had a negative impact on the GBPUSD, which increased in advance of the Bank of England’s anticipated 25bps rate hike this week. 10.1% in March, a four-decade high for the UK, is lower than the previous record of 11.1% in October 2022. The Bank of England must raise interest rates continuously this year to offset rising consumer spending and bring inflation down to more manageable levels.

In advance of Thursday’s Bank of England interest rate announcement, GBPUSD reached a one-year high. The downward adjustments to the March jobs figures overshadowed the better-than-anticipated US April jobs statistics, maintaining market expectations for 75 basis points of Fed rate cuts by year’s end. Since headline inflation increased more quickly than anticipated in March to 10.1% on-year, not far from the four-decade peak of 11.1% reached in October, the BOE is largely expected to increase interest rates by 25 bps to 4.5% as UK pricing pressures continue stubbornly high. The terminal rate is valued by the market closer to 5%, and it is anticipating confirmation of this. A hawkish increase might push the GBP higher.

The UK Economic Surprise Index is at a 2-year high compared to its US counterpart, which has been falling since the end of March. Additionally, UK macro indicators have recently outperformed expectations. In this sense, the US CPI data due on Wednesday will be key after the US Federal Reserve raised interest rates last week and signalled it may stall there (core CPI forecast to drop to 5.5% on-year in April from 5.6% in March).Market expectations for no BOE rate reduction this year indicate that the GBP is now supported by the outlook for relative monetary policy.

GBPNZD Analysis

GBPNZD is moving in an Ascending channel and the market has reached the higher low area of the channel.

To increase demand, New Zealand migration may reach 100,000, which raises wage pressures and drives up inflation as more people spend their money on goods and services. If the RBNZ tightens monetary policy settings, migration will be reduced and the cost of living in New Zealand would increase too much.

In February, gastroenterologist Wesley Kasen travelled from Colorado to Hawke’s Bay in New Zealand with his wife Marnie, two children, and dog. They filled a gap at the neighbourhood hospital. The Kasens are a part of a migrant boom that is easing the severe labour shortages in the nation. This is good news for businesses struggling to fill positions and control costs, but analysts warn that it also runs the risk of fueling inflation and keeping interest rates higher for longer. The government is encouraging the influx of migrants attracted to the nation’s unspoiled, picturesque nature, relative safety, and liberal politics in an effort to address the labour shortages and gain ground in the global talent war. Marnie stated, “I am simply continually in awe of how welcoming the people are everywhere we go, and how simple things are. The Reserve Bank of New Zealand, who stated that rising long-term net migration might improve activity and inflation, may not find it to be so simple, as this week’s strong labour market statistics revealed soaring migration inflows. There is a risk that we don’t get the recession and that we keep sort of plodding in a lot stronger environment, which would frustrate the outlook for inflation, would frustrate the central bank, and keep interest rates higher for longer,” said Jarrod Kerr, chief economist at Kiwibank.

In fact, New Zealand’s migrant population is growing far more quickly than anticipated and is on track to set a record this year, which could keep demand high and, more concerningly, re-ignite the housing market, a recurring obstacle for the RBNZ in its fight against inflation. According to Statistics New Zealand, a net 51,955 immigrants relocated to New Zealand in the year that ended in February. If current trends continue, according to economists at ANZ and Westpac, total net arrivals might reach a record 100,000 this year.Despite the country’s most aggressive policy tightening cycle in a quarter century, New Zealand’s inflation is still at historically high levels and well beyond the top end of the central bank’s 1%-3% target, running at an annual rate of 6.7%, down from a three-decade 7.3% peak hit in the second quarter of last year. After a series of increases that started in October 2021, the benchmark cash rate is currently at more than a 14-year high of 5.25%. However, there is a possibility that the RBNZ may still have work to do, possibly even pushing the peak beyond the current prediction of 5.50%. Stephen Toplis, head of research at the Bank of New Zealand, wrote to clients that if the demand impulse (from migration) prevails over the supply effects, it would take inflation longer to reach the RBNZ’s objective and would possibly require more tightening than has been anticipated. According to Kerr of Kiwibank, there are already indications that the economy is weakening, which should continue to bring down inflation. In the fourth quarter, economic growth decreased by 0.6%.

New Zealand is in critical need of immigrants to fill occupations ranging from bus driving to computer game programming, but just like Australia and Singapore, who are also attempting to draw in new immigrants, the nation is experiencing a severe housing shortage. Prior to reaching their peak in 2021, house prices, a major contributor to inflation, increased quickly for a decade. Since then, increased loan rates and a construction boom have caused prices to drop by 16%, although they are now beginning to stabilise in part because of migrant-driven demand for housing. The news is mostly positive for the government, which has implemented new regulations to close employment shortages that companies claim were impeding growth, but any big increase in housing costs will be unpopular with voters. A good example is NZBus, one of the largest public bus companies in the nation. It is presently training 72 bus drivers from Fiji and the Philippines. By resisting pressure to raise compensation, this aids in containing wage inflation, but it also maintains persistently high consumer prices. Although it presents a serious problem, increased migration, according to Infometrics lead economist Brad Olsen, is excellent news for businesses struggling to find personnel. “Given that inflationary pressures are still high, adding any more demand to the economy at the time does seem to be a struggle for New Zealand.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/