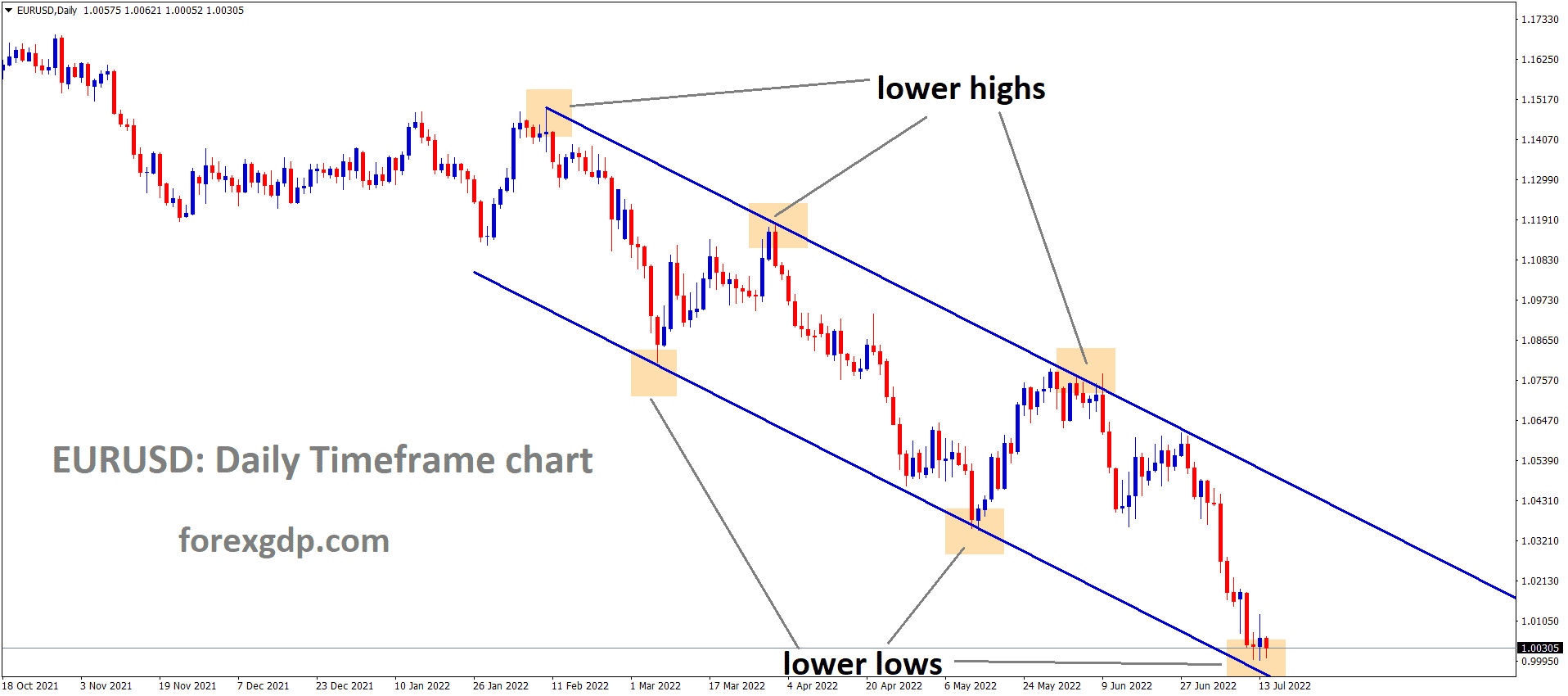

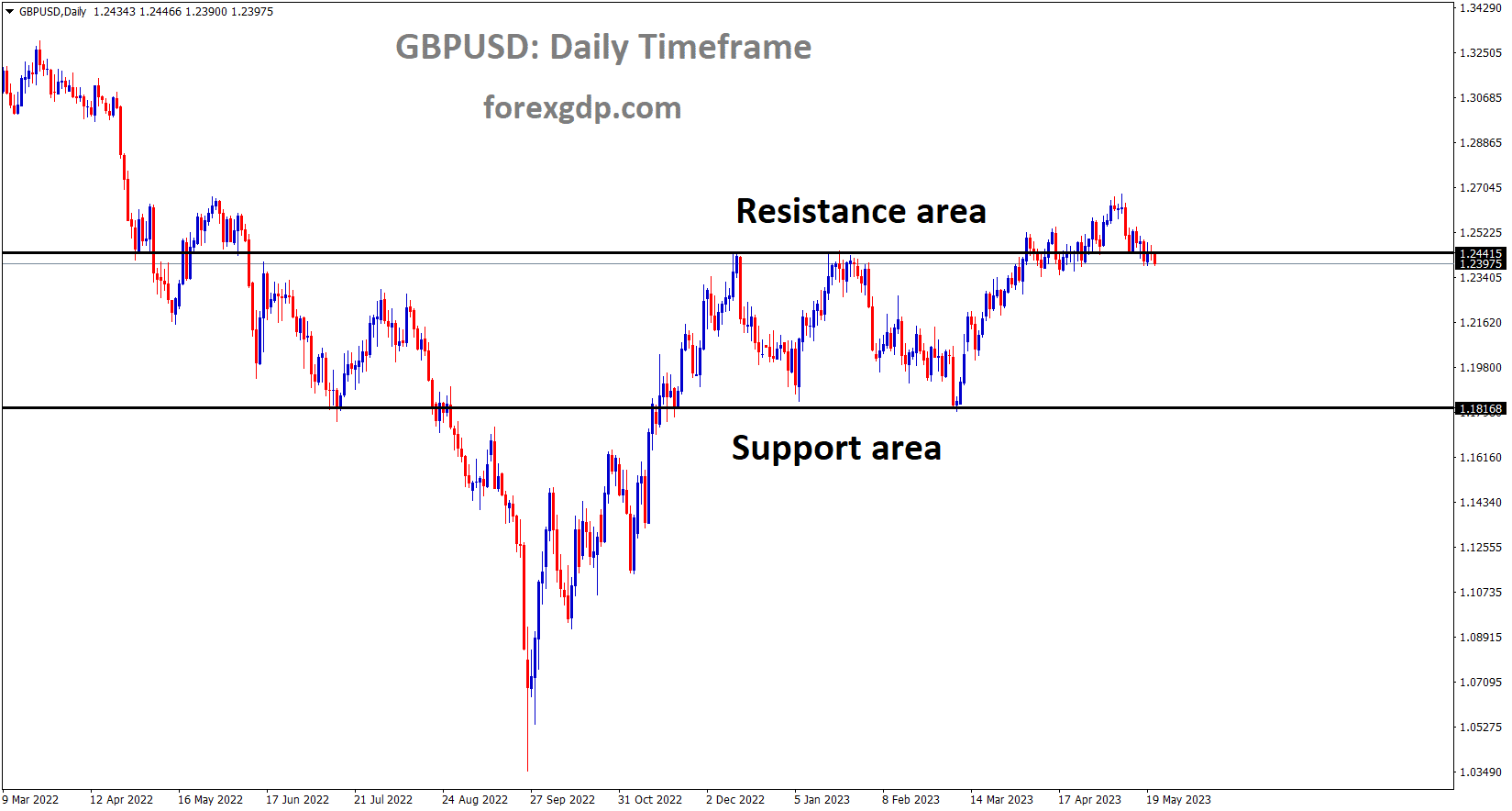

GBPUSD Analysis

GBPUSD is moving in the Box pattern and the market has fallen from the resistance area of the pattern.

The most anticipated outcome of Bank of England Governor Bailey’s speech this week is a rate increase. This week’s UK inflation report, which is expected to come in at 8.3% from 10.1%, is scheduled. If the data are as expected, the BoE will hold off on raising interest rates in June.

In the early European session, the GBPUSD pair appears vulnerable above the immediate support of 1.2420. Investors are anticipating Bank of England (BoE) Governor Andrew Bailey’s speech as The Cable struggles to hold onto the closest cushion.Half of the gains made in Asia are being held by S&P500 futures, which indicates a modestly upbeat market climate. The US Dollar Index is facing barriers above 103.30, with the downside being supported by hawkish remarks from Federal Reserve policymakers and the upside being constrained by further delays in US debt-ceiling issues. The preliminary S&P PMI figures are expected to keep the US Dollar Index on edge. Manufacturing PMI has dipped from its previous reading of 50.2 to 50.0. whereas the Services PMI is predicted to stay constant at 53.6. The manufacturing sector is emerging from the contraction phase if the Manufacturing PMI is released twice in a row at or above 50.0.

Investors are anticipating the publication of the UK’s Consumer Price Index data as it relates to the Pound Sterling. The headline UK Consumer Price Index is currently estimated to be 8.3%, a significant decrease from the previous release of 10.1% annually. The headline CPI has been increasing steadily each month by 0.8%. It is anticipated that the 6.2% level of core CPI, which excludes the effects of food and oil costs, will not change. The BoE Andrew Bailey’s speech will continue to be in effect going forward. The BoE’s Bailey’s speech is anticipated to offer guidance on interest rates for the monetary policy that is scheduled for June.

GOLD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has fallen from the lower high area of the channel.

With 2-year bonds rising to 4.35% on Friday and 3.66% traded earlier this month, US Treasury yields increased on Monday.

A few weeks ago, when the 10-year note was trading above 3.3%, real yields drove up the US dollar while non-yielding assets like gold fell. The US parties are making good progress in their negotiations over the debt ceiling, and the decision to delay the US default until after June 1 was warmly welcomed.

SILVER Analysis

XAGUSD Silver price is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

Last week, the price of gold fell to a 2-month low, but it has since stabilised as the US dollar has stopped rising as recently as it had. With the benchmark 2-year bond clipping 4.35% on Friday and again this week after trading at 3.66% earlier this month, Treasury yields have been favourable for the “big dollar.” Similar to how the 10-year note was trading a few weeks ago, it is now trading above 3.7%. The increase in US real yields, however, may be the focus for gold traders. The market-priced inflation rate derived from Treasury inflation-protected securities for the same tenor less the nominal yield results in the real yield.

The current target for the US 10-year real yield is a rise above 1.50%. Gold was below US$ 1,850 when it was at this level before Silicon Valley Bank Financial et al. collapsed, which is concerning for gold bulls. The US debt ceiling debate seems to be finally moving in the right direction going into Tuesday’s session. President Joe Biden and House Speaker Kevin McCarthy both stated that a default is not anticipated following talks on Monday. Although the news is generally welcomed, markets seem to be waiting for more clarity because there has not been much of a price reaction so far. The US Dollar has recently been strengthening, and the direction of the DXY Index may indicate where the precious metal will move next.

USDCHF Analysis

USDCHF is moving in the Box pattern and the market has reached the resistance area of the pattern.

Employees of Credit Suisse sued the FINMA regulator after they lost $400 million in bonuses that were partially based on the bank’s AT1 bonds. Credit Suisse also requested that FINMA treat CCAs differently from AT1s, but employee awards were also cancelled with the AT1s.

After losing $400 million in bonuses partially linked to the bank’s AT1 bonds, Credit Suisse Group AG employees are reportedly preparing to sue Swiss regulator FINMA. The Swiss regulator mandated that CHF16 billion of the lender’s AT1 debt be written down to zero as part of the takeover in March, with some compensation being given to shareholders. Senior managers at Credit Suisse have requested multiple times that Quinn Emanuel and Pallas, law firms that are already suing Swiss regulator Finma on behalf of investors who owned Additional Tier-1 bonds, represent them in court, according to a Financial Times report.

USD Index Analysis

USD index is moving in an Ascending channel and the market has reached the higher low area of the channel.

White House negotiators and US House Speaker Kevin McCarthy had productive discussions on the debt limit on Monday, and McCarthy expressed optimism that a deal would be reached. McCarthy later that day met with President Joe Biden. McCarthy stressed the urgency of making decisions as the June X deadline drew near, but added that an agreement might be reached as soon as the following meeting or even today.

GBPJPY Analysis

GBPJPY is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

Because of the Bank of Japan’s continued adoption of an ultra-easy monetary policy, JPY is weak on all markets. The Japanese economy is more divergent when the inflation rate is higher and the interest rate is lower.

Following this week’s increase in US Treasury yields, USDJPY increased.

After this week’s opening trading day, the Japanese Yen declined against its major rivals. It fell at the same time that Treasury yields increased. The 10-year rate recently enjoyed its longest winning streak since April 2022, rising for the seventh straight day. The Japanese Yen will continue to be sensitive to changes in the international economy and financial markets, as was mentioned in this week’s outlook. Because of the Bank of Japan’s continued ultra-loose monetary policy, the future of the JPY will largely depend on yields in other countries. In this instance, the US economy’s ongoing optimism over the coming 24 hours supported bond yields. Financial markets appear to be still optimistic that US politicians can agree on a debt ceiling agreement before a possible default.

The US Core PCE Deflator print on Friday will probably represent a significant risk for the Japanese Yen this week. The Federal Reserve uses this as its preferred inflation indicator. The central bank’s communicated pause from the most recent policy meeting would be undermined by additional indications that price pressures in the largest economy in the world remain sticky. This could raise Treasury yields and have an impact on bond rates around the world. Looking ahead 24 hours, there are no significant economic event risks for Tuesday’s Asia-Pacific trading session. Several US PMI data will be released later today. If the preliminary May data is positive, that could increase bond yields even more, which would hurt the Japanese Yen. The current state of the financial markets could keep JPY on edge in the interim.

GBPCAD Analysis

GBPCAD is moving in an Ascending channel and the market has reached the higher low area of the channel.

Following the optimistic talks outcome of yesterday’s US Debt ceiling talks, oil prices increased. Oil demand is relieved by China’s stable situation, and China will increase oil imports in the coming days. The Canadian Dollar is still consolidating as it awaits this week’s decision on the US Debt Ceiling.

The Loonie pair’s failure to account for the recently higher prices of WTI crude oil, Canada’s main export. If we look for a cause for the duo’s lacklustre performance on Monday, we might find it in the Canadian Bank Holiday. Nevertheless, the US Dollar appears to have recently been supported by expectations of a hawkish Federal Reserve and hopes that the United States will not default. Due to the geopolitical tension involving the US, Russia, and China, the oil price, however, seems to support China’s willingness for increased investment and a potential supply shortage. US President Joe Biden recently stated that he thought the debt ceiling negotiations would advance, and House Speaker Kevin McCarthy stated, “We both believe we need to change the trajectory.

Neel Kashkari, President of the Minneapolis Federal Reserve, on the other hand, supported the rate hike trajectory while citing concerns over a potential US default and banking crisis, which helped to keep the US Dollar firmer overall. In a similar vein, St. Louis Federal Reserve President James Bullard dismissed recession worries on Monday while predicting that there will be two more rate increases before the base rate is reached. Additionally, recent calls for higher rates have received support from San Francisco President Mary C Daly, Richmond Fed President Thomas Barkin, and Atlanta Fed President Raphael Bostic. A US official recently stated that they are directly collaborating with China on the Micron issue. Beijing outlawed chips made by the US company Micron after deeming them a security threat, which led to an argument between Washington and Beijing. The People’s Bank of China defends its status quo, which in turn benefits commodity prices, including WTI, because China dominates as the largest industrial player in the world, according to the China Securities Journal .

With this, the US Dollar Index resumed its upward trend on Monday following a depressing close on Friday that ended a two-week winning streak. As a result, the gauge of the value of the dollar against the six most important currencies ended the day around 103.23, and it had reached that level by the time of publication. Notably, WTI Crude Oil started the week poorly before rebounding off $70.65 to end the day favourably at around $72.15. Wall Street ended the day with a mixed performance amid these manoeuvres, but US Treasury bond yields continued to rise. Despite this, the US 10-year and 2-year Treasury bond yields have risen for the past seven days straight, reaching the highest levels in 10 weeks, respectively, of 3.72% and 4.32%. As the full markets return, the US S&P Global PMIs for May and the Canadian Industrial Production for April might amuse.

EURNZD Analysis

EURNZD is moving in the Descending channel and the market has reached the lower high area of the channel.

We will raise rates until the 1-2 year range, ECB Policy Maker Francois Villeroy De Galhau stated at the Bank of France meeting. We will soon reach the terminal rate, which will cause a rate increase of 50 to 25 basis points in upcoming meetings. controlling inflation As a result, we observe data one by one before lifting rates.

Francois Villeroy de Galhau, a policymaker at the European Central Bank, stated, according to Reuters, “I expect today that we will be at the terminal rate not later than by summer.” Today, the key question is not how much more to raise interest rates, but rather how much of what is already in the pipeline will be passed through. The transmission of policies may lag in the upper end of the 1-2 year range during the current tightening cycle. It was prudent and wise to reduce rate increases from 50 bp to 25 bp. We need to keep an eye on how quickly and in how much depth our previous hikes have progressed. The duration of high rates is now more significant than the exact terminal level. We will continue to be data-driven, assessing the strength of monetary policy transmission and the outlook for inflation at each meeting.

In tomorrow’s RBNZ meeting, a higher OCR is anticipated, according to ANZ economists’ bank report. Increased fiscal and migratory activity enables lower inflation expectations to be expected at higher rates. Trade and fiscal deficits continue to cast a gloomy shadow over the economy.

The main concern, according to ANZ Bank economists, is the outlook for carry. Now that some short-end rates are around 6%, which is world-beating, Kiwi seems to be mostly about carry. With migration and fiscal factors driving the majority of calls for higher OCR, higher rates should be beneficial to the New Zealand dollar, but twin deficits cast an ominous shadow in the background.

AUDNZD Analysis

AUDNZD is moving in an Ascending channel and the market has reached the higher low area of the channel.

The Australian retail sales data that is due on Friday is predicted to decline from 0.40% to 0.10% month-over-month. Positive retail sales figures on Friday may prompt the RBA to increase rates by another 25 basis points in June. The unemployment rate increased, and if printed higher, the easing job market could cool down the results of the retail sales data.

The RBA has set an inflation target of 2% to 3% for 2025.

AUDCAD Analysis

AUDCAD has broken the Descending channel in upside.

The Australian dollar has fluctuated against its counterparts as expectations for a rate hike in Australia have decreased as a result of an unexpected drop in employment in April. The primary focus is currently on the April retail sales data, which is due on Friday and is anticipated to have slowed from 0.4% to 0.1% on-month. Since early April, most Australian macroeconomic data have exceeded expectations, according to the Economic Surprise Index. Therefore, encouraging retail sales data may help counteract some of the recent easing of rate hike expectations, supporting the Australian dollar. At its meeting earlier this month, the Reserve Bank of Australia unexpectedly increased the benchmark rate by 25 basis points and left the door open for further tightening given that inflation, which is currently running at 7%, is only anticipated to return to the top of the central bank’s 2%-3% target by mid-2025.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/