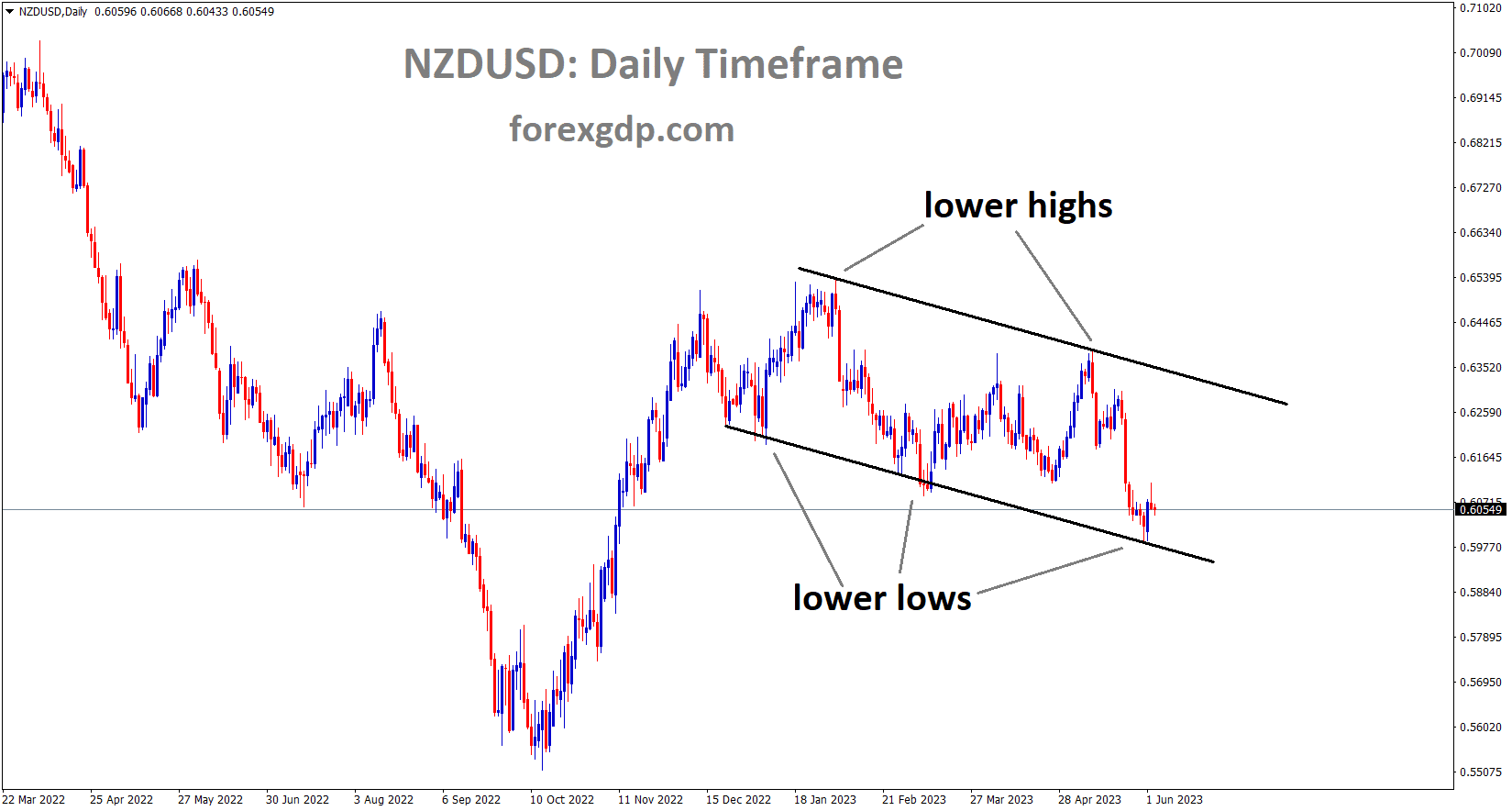

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel. According to US NFP data, labour demand is slowing down in the US, and the unemployment rate is currently at a 53-year low of 3.7%. US Bond Yields are rising as a result of the US economy’s resilience in the face of higher rate hikes.

After the NFP data came in at positive numbers, the New Zealand dollar slightly declines.

In response to strong labour market data from the US, the NZDUSD pair lost gains that had the Kiwi soaring to the 0.6111 area at the end of the week and falling towards the 0.6065 area. The information pointed to a potential reevaluation of additional rate increases by the Federal Reserve, favouring the US Dollar in the face of rising US bond yields. Employment in the United States increased by 339k in May, more than double the consensus forecast of 190k, according to the US Bureau of Labour Statistics. The Unemployment Rate, however, increased slightly and ended up at 3.7% as opposed to the anticipated 3.5%. Average Hourly Earnings, a measure of wage inflation, were 4.3% YoY, just under the anticipated 4.4%.Although the overall labour market outlook indicates that labour demand is slowing, the Fed may want to rethink a 25 basis point (bps) hike at its upcoming June meeting given the strong employment growth and rising inflationary pressures. As a result, there is an upward trend in US bond yields. The yield on a 10-year bond has risen to 3.68%, representing a gain of 2.70% for the day. Similar to this, the 2-year yield has increased by 3.64% to stand at 4.51%, and the 5-year yield has increased by 3.81% to stand at 3.84%.

The May Consumer Price Index, which will be released next week, will be crucial in influencing the expectations and considerations of the Federal Open Market Committee regarding the next interest rate decision because, as stated by Fed officials, their ultimate goal is to ensure full employment and price stability. As of right now, according to the CME FedWatch tool, markets continue to discount a greater likelihood of a rate cut for the upcoming meeting on June 13-14, but the case for a 25 bps hike has gained some significance.

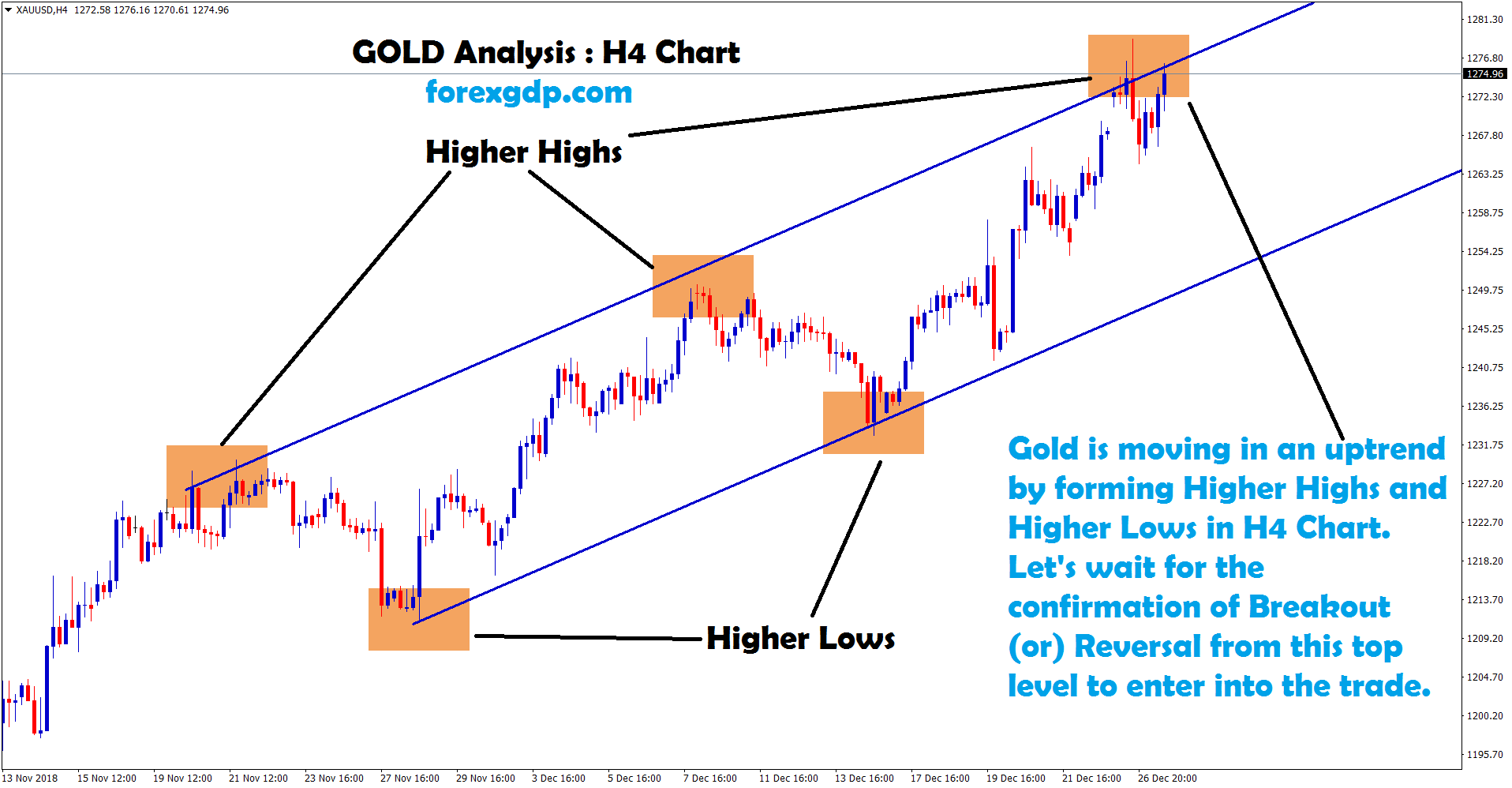

GOLD Analysis

XAUUSD Gold Price is moving in an Ascending channel and the market has reached the higher low area of the channel.

Gold fell against the US Dollar last week as a result of US NFP data that came in higher than anticipated. Due to the US economy’s resilience, the FED was able to raise interest rates by 25 basis points in June.

Inflation in the US has increased slightly but remains above the target range of 2-3% due to rising consumer spending and wage growth.

From its peak levels around $2,070 in May, gold prices have experienced a significant decline, falling by nearly 6% in a short period of time. Bullion made an attempt to recover this past week, briefly reaching $1,983, but quickly changed direction and pulled back as the weekend approached, settling just below the $1,950 mark. The dynamics of U.S. interest rates, particularly their recent upswing, can be blamed for the metal’s inability to sustain bullish momentum. Yields increased sharply on Friday in response to remarkably positive U.S. jobs data, continuing their broader rebound that started around the second week of April, despite modest declines earlier in the week. The most recent payrolls report, which focuses on the macroeconomic front, revealed that U.S. employers added 339,000 workers in May, significantly more than the projection of 190,000. Strong hiring indicates that, despite the Fed’s fast-and-furious tightening campaign that started in 2022, the economy is doing well and is still far from entering a recession.

SILVERAnalysis

XAGUSD Silver Price is moving in an Ascending channel and the market has reached the higher low area of the channel.

The economy’s and the labour market’s resilience could delay inflation’s return to the target rate of 2.0%. In light of this, policymakers may decide to keep raising borrowing costs in the second half of the year, even if they temporarily paused at their meeting in June to consider the lag time effects of cumulative tightening. The possibility that the FOMC will need to raise its terminal rate and maintain it there for an extended period of time in order to restore price stability ought to keep bond yields high, at least theoretically, strengthening the dollar in the process. Precious metals and other non-yielding assets will likely be considered in this scenario. Due to the aforementioned factors, gold’s fundamental outlook is beginning to turn more bearish, which means that before stabilising later in 2023, additional losses may be on the horizon. This also suggests that new record highs will have to wait and might not be within bullion’s current grasp.

US Dollar INDEX Analysis

US Dollar index is moving in an Ascending channel and the market has rebounded from the support area of the minor box pattern of the channel.

The US Dollar rose against other currency pairs last week Friday NFP data came in at higher than anticipated numbers printed at 339K Jobs in May month. The unemployment rate was recorded at 3.7%, which is a slight increase from the earlier reading of 3.4%.

On Monday, as markets processed the OPEC+ production cut agenda that was announced over the weekend, the US dollar added modest gains to Friday’s rally. A mixed jobs report on Friday that was generally viewed as more positive than negative had helped USD. The week has gotten off to a slow start on the currency markets. The non-farm payrolls data show that 339k jobs were created in May. This was higher than the 195k forecast, and the April figure was increased from 253k to 295k. However, the unemployment rate increased slightly from 3.4% to 3.7%, which is higher than the projected 3.5%. After Wall Street recorded respectable gains in their cash session to end last week after the resolution of the debt ceiling deal lifted the mood, APAC equity indices have generally had a good day. Futures indicate that Monday will begin quietly. China’s Caixin services PMI May reading of 57.1 instead of the 55.2 anticipated and 56.4 prior lifted the mood.

Saudi Arabia absorbed the majority of the reductions in oil production following the announcement by OPEC+. They will contribute a million fewer barrels per day to the world supply. While Russia’s production goal remained the same, the UAE’s increased. Although prices are still higher than where they closed the Friday session, crude prices spiked higher at the opening of today’s trading session but have since given up some of the gains. While Brent is just under US$ 77 bbl, the WTI futures contract is close to US$ 72.50 bbl. You can see current prices here. The 1-year bond is still close to the 23-year high above 5.30%, and Treasury yields are still high to start the week. The Federal Open Market Committee will meet again on June 14; the blackout period started over the weekend. This means that until after the meeting, committee members will not publicly discuss policy. Future factory and durable goods orders data for the US will come after the Swiss CPI and Eurozone PPI. The RBA will make its decision on monetary policy tomorrow, and the Bank of Canada will implement it on Wednesday.

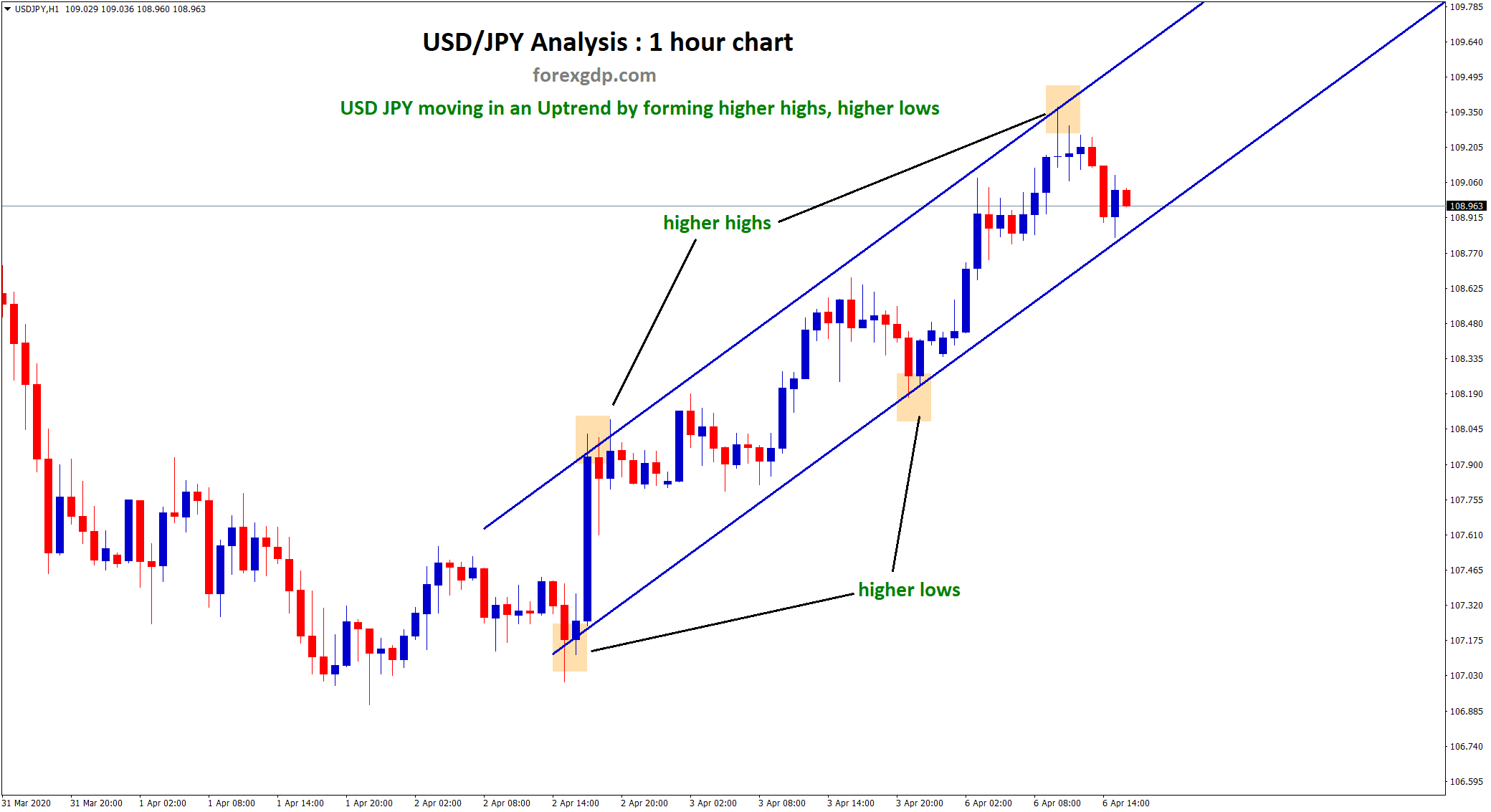

USDJPY Analysis

USDJPY has broken the Descending channel in upside.

The Bank of Japan may alter its yield curve control policy at its next meeting, in the opinion of SocGen economists, after which the USDJPY will once more drop to 130. If the Bank of Japan sells foreign assets, net inflows to Japan will strengthen the yen and weaken the dollar.

EURUSD Analysis

EURUSD has broken the Descending channel in upside and the market has retesting the broken area of the channel.

After ECB policymakers hinted at one or two 25 bps rate increases this year to combat Eurozone inflation, the euro fell. The ECB will decide whether to raise rates more or less in June based on the eurozone GDP data scheduled for this week.

From the perspective of the European Central Bank, not much has changed, with ECB policymakers largely betting on one or two additional 25bps hikes. This is in spite of a decline in inflation in the Euro Area this week, which is supported by comments made by ECB policymakers after the inflation release. The data are not expected to convince the Central Bank to delay raising interest rates in June. Following the inflation print, the Euro made significant gains thanks to the US debt ceiling agreement, which caused the US Dollar to weaken. Though the rate hike expectations for the Fed’s June meeting rose after the release of the NFP report and the US jobs data on Friday, the US dollar only experienced a brief period of weakness. As we start a new week, there are not many risk events or economic data releases that are relevant to the Euro Area. However, the US ISM services PMI data and the June 8 deadline for the third estimates of Euro Area GDP growth pose the greatest risk to the EURUSD. Given that the US economy is predominately service-based and ongoing concerns about services inflation, the Fed may closely monitor the release. A strong reading might cause the Fed to hawkishly reprize its rate hike expectations, which would increase the downside risk for the EURUSD.

EURCHF Analysis

EURCHF is moving in the Descending channel and the market has reached the lower high area of the channel.

By June 12 of this month, UBS will fully complete the acquisition of Credit Suisse Bank. This month, the Swiss Government is making the necessary preparations for the merger of UBS and Credit Suisse Bank. Investors’ confidence in the Swiss Government and Banks will increase after the merger is complete.

Following a government-backed rescue earlier this year, UBS anticipates completing its acquisition of Credit Suisse as early as June 12. This will result in the creation of a massive Swiss bank with a balance sheet of $1.6 trillion. The registration statement, which covers the shares to be delivered, must be approved by the U.S. Securities and Exchange Commission in order for the transaction to close, according to a statement released by UBS on Monday. As soon as June 12, 2023, UBS anticipates completing the acquisition of Credit Suisse. At that time, it said, Credit Suisse Group AG and UBS Group AG would merge. In Swiss premarket trading, UBS shares were up 1.1%, while Credit Suisse shares were up 0.7%. According to Michael Klien, an analyst at Zuercher Kantonalbank, “we view the completion of the takeover as an important step in launching what we perceive to be a protracted integration process and getting things done.” Even though UBS’s risk profile has significantly changed, there are still excellent investment opportunities, he continued. Following a collapse in customer confidence that brought its smaller Swiss rival to the verge of failure, Switzerland’s top bank agreed on March 19 to pay 3 billion Swiss francs ($3.37 billion) and assume up to 5 billion francs in losses for its smaller Swiss rival. This agreement came after the Swiss authorities took action to prevent a wider banking crisis. By late May or early June, the bank had hoped to complete the largest bank transaction since the global financial crisis. However, it stated last month that it was still in discussions with Swiss authorities regarding loss protections and capital requirements, indicating that these issues needed more time to be resolved.

Credit Suisse shares and American Depositary Shares will be taken off the SIX Swiss Exchange and the New York Stock Exchange once the process is complete, according to UBS. Credit Suisse shares would be delisted at the earliest on June 13, according to a separate statement from SIX. Shareholders of Credit Suisse will receive one UBS share for every 22.48 shares they currently own under the terms of the all-share acquisition. The transaction will establish a group in charge of $5 trillion worth of assets, giving UBS an instant competitive advantage in markets where it would normally take years to expand its size and reach. The megabank will have 120,000 employees worldwide, but it has already stated that job cuts will be made in order to capitalise on synergies and cut costs. In an effort to give Credit Suisse clients and employees more assurance and prevent departures, UBS had been rushing to close the transaction in record time. The agreement was supported by 200 billion francs in liquidity support from the Swiss central bank and the government’s promise to absorb additional losses up to 9 billion francs. UBS CEO Sergio Ermotti said at a financial conference on Friday that it is important to understand that this is an acquisition rather than a merger and that difficult choices lie ahead.

The Financial Times reported on Sunday that the largest lender in Switzerland is thinking about delaying the release of its quarterly results until the end of August as it works through the complications brought on by the acquisition. The bank chose not to comment on the possible holdup. What UBS will do with Credit Suisse’s Swiss retail bank, long regarded as the group’s crown jewel, is still an open question. Although integrating it into UBS could result in significant cost savings, concerns have been raised about the combined organization’s size and potential job losses. Ermotti stated on Friday that the bank was still analysing the situation, but that the “base scenario” remained a full integration with UBS and that he would not be influenced by “nostalgia” in making his decision. Ermotti, who was brought back to UBS to oversee the acquisition, was upbeat about the difficulties ahead and dismissed suggestions that the new bank would be too large for Switzerland. I am confident that this will be a great story for our shareholders, employees, clients, and the Swiss financial services sector as a whole, he said on Friday.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

UK Inflation is decreasing in comparison to target levels, but there is still a long way to go before it reaches the Bank of England’s target level of 2-3%. The manufacturing PMI data improved last week; inflation dropped from double digits to single digits, which cooled the pound against the US dollar and the euro.

The British pound has had a strong week, rising against a number of other currencies over multiple weeks. The British pound has gained more than two big figures this week versus the US dollar, more than one big figure versus the Euro, and roughly one and a half big figures versus the Japanese yen. Expectations that the Bank of England will need to keep raising interest rates in the near future to help bring inflation back to target have increased in response to the recent UK inflation report, which showed that price pressures are easing but slowly. In opposition to this, market analysts currently believe that the Federal Reserve will probably pause its recent rate hike programme this month and that the ECB may scale back its programme after recent Euro Area data showed inflation easing at a faster pace than anticipated. The new BoJ governor in Japan recently stated that until inflation reaches the central bank’s target on a sustainable basis, monetary policy conditions will remain lax.

GBPCAD Analysis

GBPCAD is moving in an Ascending channel and the market has reached the higher low area of the channel.

To keep oil prices at their current levels, OPEC+ countries decided to cut 1 million barrels per day. Saudi Arabia said the agreement can go into effect on July 1st, 2023. Following the news, oil prices rose. Russia’s output is unchanged at the standard level.

After OPEC+ announced over the weekend that the output target would be reduced starting on July 1st, crude oil opened at a 5-week high on Monday. Following a similar move in April that caused black gold to soar to its highest level in six months, the Organisation of Petroleum Exporting Countries made its decision at its meeting in Vienna. After that surge, it dropped to an 18-month low at the beginning of last month before the conclave last weekend. Similar price movement has been seen so far today, with a rally of over 4% from Friday’s close followed by a loss of the majority of those gains. You can see the most recent prices right here. Saudi Arabia will carry out the majority of the heavy lifting within OPEC+, reducing their production by one million barrels per day. The largest oil exporting country now exports about 9 million barrels per day, down from about 10.5 million before the April production cuts. The United Arab Emirates was given permission to slightly increase production while the Russian production targets were left unaltered. Some African countries experienced slight production declines, and their output will be watched.

Abdulaziz bin Salman, the Saudi Arabian minister of energy, had partially hinted at the move. Speculators are here to stay in any market, he claimed two weeks prior. They will be ouching, I keep saying. In April, they produced ouch. Since I do not play poker, I do not have to reveal my hand, but I would merely warn them to be cautious. After mixed jobs data on Friday, which showed 339k jobs were added in May according to the non-farm payrolls data, the US dollar is also stronger to start the week. This was higher than the 195k forecast, and the April figure was increased from 253k to 295k. However, the unemployment rate increased slightly from 3.4% to 3.7%, exceeding the forecast of 3.5%. Several Fed speakers had hinted in their remarks from the previous week that the bank might’skip’ a hike at the Federal Open Market Committee meeting on June 14. As of right now, committee members are not allowed to publicly discuss policy until after the meeting. Without more information on the Fed’s thinking, markets could become more volatile, which would affect oil prices.

AUDUSD Analysis

AUDUSD has broken the Descending channel in upside.

In his most recent speech to the Senate Economic Legislation Committee, RBA Governor Philip Lowe predicted that rates would remain unchanged at tomorrow’s meeting. The cost of living is rising, and it is hard to stop inflation.

After hitting a six-month low in the middle of the week, the Australian Dollar put together an outstanding rally heading into the weekend. Once again, US Dollar manoeuvres dominated the proceedings, but Tuesday’s RBA meeting may bring some volatility due to domestic factors. Following the Friday resolution of the US debt ceiling controversy, markets as a whole exhaled a sigh of relief. All types of risk assets rose, and the growth-linked Australian dollar joined the celebration. Although Tuesday’s building approvals were weak, falling 8.1% instead of rising by the expected 2% and 1.0%, there are growing concerns about inflationary pressures in the financial system. An estimate of the monthly CPI that represents 62–73% of the weighted quarterly basket is released by the Australian Bureau of Statistics. The quarterly number is related to the RBA’s mandated target range of 2 to 3% over the cycle. Although the monthly CPI measure’s validity has been called into question ever since it was introduced last year, the RBA cited it as justification for pausing the cycle of rate increases earlier this year. When they get together again to decide on rates on Tuesday, they might acknowledge it.

According to the monthly gauge, year-on-year CPI reaccelerated to 6.8% to the end of April, far exceeding the prior estimates of 6.4% and 6.3%. The annual wage review decision made by the Fair Work Commission on Friday only makes the RBA’s predicament worse. It resulted in a 5.75% increase in the minimum wage across all modern awards. This exceeded the typical expectation of a 5% increase. It will go into effect on July 1st, 2023. While there is a feeling of fairness in the outcome, it actually increases consumers’ purchasing power, feeding the price-wage spiral even more. The Australian private sector credit for April showed growth of 0.6% month-over-month as opposed to the 0.3% anticipated, strengthening the case for a hawkish RBA decision. Last week, RBA Governor Philip Lowe testified before the Senate Economics Legislation Committee. He discussed the challenges of bringing the CPI down while wages are increasing at the current rate. The probability of a rate increase on Tuesday is low according to the interest rate market. There appears to be a compelling argument for tightening things up even more. In other rate news, the benchmark 2-year bond spread increased to 105 basis points in favour of the ‘big dollar’ at the beginning of last week, but it has since decreased to about 70 bp at the same time that the AUDUSD appreciated. The difference in interest rates may continue to dominate the AUDUSD exchange rate, and a surprise monetary policy stance by the RBA could spur movement in the currency.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/