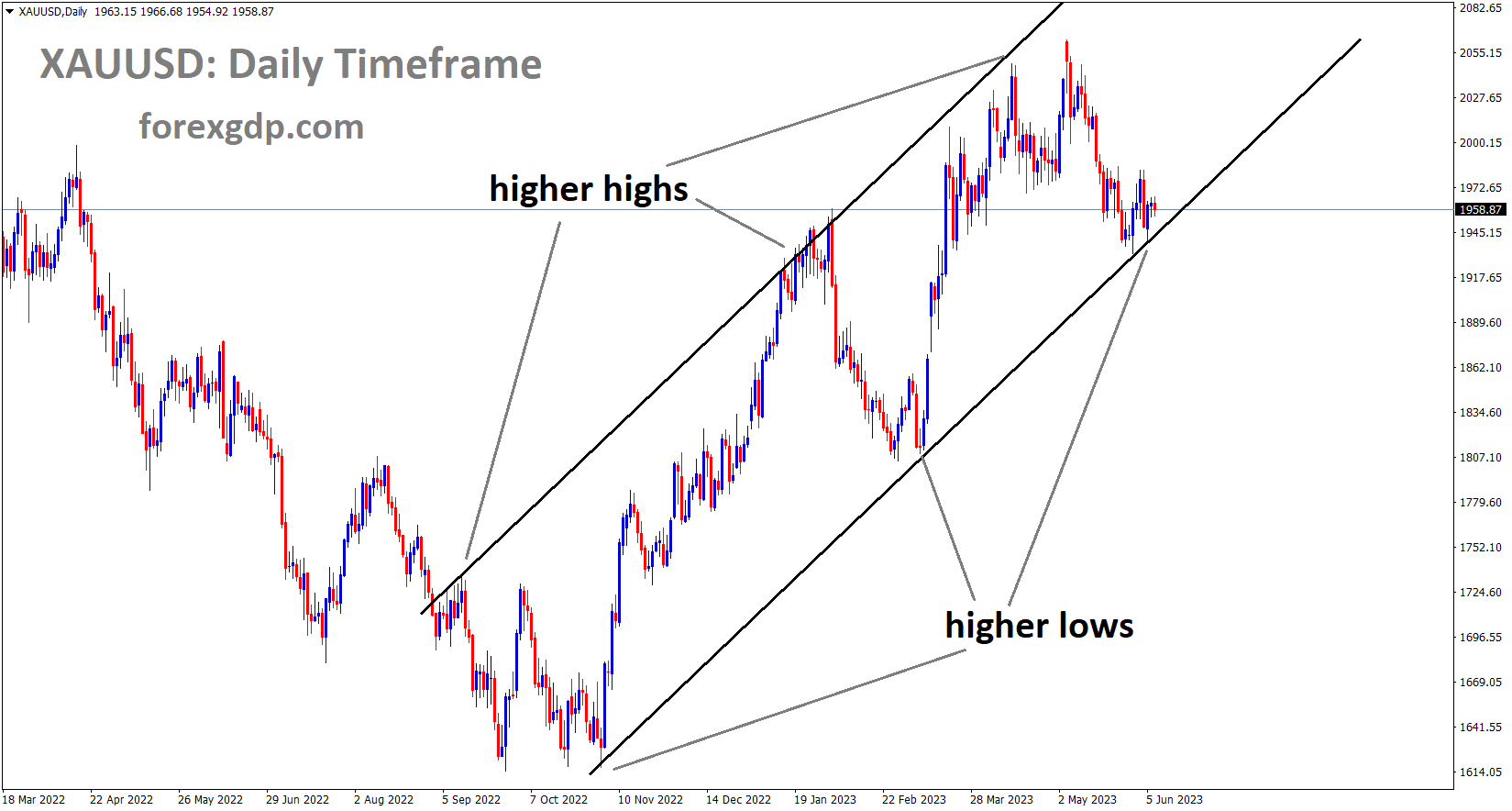

GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel.

Due to lower domestic data showing that the US and China are consuming more gold as a result of increasing economic stimulus, gold is trading higher against the USD. The FED is anticipated to hold rates steady in June and raise them by 25 basis points in July. These hopes raise the value of gold relative to the dollar.

As the US dollar remains weak in the early hours of Wednesday, the gold price records a three-day winning streak near $1,965. In doing so, the precious metal also boosts expectations for more stimulus from China and market caution amid a lack of speeches from Federal Reserve (Fed) policymakers as a result of the pre-FOMC blackout and a light calendar. However, the US Dollar Index reverses the corrective bounce from the previous day while accepting bids near 104.00, down 0.10% on the day as of the time of publication. In doing so, pessimistic market wagers on the Fed’s next move hurt the greenback’s gauge against six important currencies. According to the CME Group’s FedWatch Tool, traders of Fed funds futures believe the Fed will then start raising rates again, with a 65% chance of at least a 25 basis-point increase in July. It is important to note that the probability of a rate hike in June is almost 15% according to interest rate futures. The reason may be related to the pessimistic U.S. economic data released on Monday and the previously dovish remarks made by Federal Reserve Officials in the run-up to the pre-Fed blackout.

SILVER Analysis

XAGUSD Silver Price is moving in an Ascending channel and the market has reached the higher low area of the channel.

Beijing is one of the world’s largest consumers of gold, so recent firmer China PMIs and domestic policies to loosen credit restrictions allow the Gold Price to rise elsewhere. However, it should be noted that the Gold Price’s movements are constrained by a light calendar and a lack of significant market commotion. The 10-year coupons continue to be sluggish at around 3.69%, reflecting the mood, whereas their two-year counterparts increased slightly to 4.50%. In a similar vein, while manufacturing stocks weighed on sentiment and reduced Wall Street’s gains, technology stocks remained firmer. The S&P500 Futures also post modest gains by press time, supporting the XAU/USD’s continued strength. Looking ahead, the direction of the gold price will be determined by China’s monthly trade figures along with risk catalysts and bond market momentum.

USD Index Analysis

US Dollar index is moving in an Ascending channel and the market has reached the resistance area of the minor Box pattern of the channel..

US stocks are declining in anticipation of the FED’s anticipated rate hike in June. However, according to economists, 75% of the FED will most likely press the pause button at the June meeting and the play button at the July meeting. Strong labour markets, a low unemployment rate, and next week’s CPI data will indicate whether or not the FED will raise interest rates at its meeting next week.

As investors continued to assess the likelihood of another Federal Reserve interest rate increase, U.S. stocks were falling. The S&P 500, NASDAQ Composite, and Dow Jones Industrial Average were all down 0.1%, 33 points or 0.1%, respectively. The Fed will meet the following week to discuss the next course of action as economic data indicate that while the economy is cooling, the labour market is still tight. Futures traders predict that the Fed will hold off on another hike next week, with a probability of 75%. Slightly more than half of traders anticipate another hike of one-quarter point in July. On Tuesday, as the Fed’s two-day meeting gets underway, the latest reading of the consumer price index—this time for May—is scheduled to be released. Prior to the meeting, Fed policymakers are currently taking a break, but last week, several of them spoke publicly to argue for a pause.

The Nasdaq has increased recently as a result of stocks, particularly tech stocks, rising on the prospect of a halt to interest rate increases. After the Securities and Exchange Commission filed a lawsuit against the cryptocurrency exchange for running an unregistered broker and exchange, shares of Coinbase Global, Inc. (NASDAQ:COIN) dropped 15.8%. The SEC only recently filed a lawsuit against Binance and its founder for securities violations. Following the unveiling of its first significant new product in a decade, a $3,499 mixed reality headset, Apple Inc.’s (NASDAQ:AAPL) shares fell 0.9%. Shares of Thor Industries, Inc. (NYSE:THO), a manufacturer of recreational vehicles, increased 13% after the company reported stronger-than-anticipated earnings and revenue and increased its full-year guidance. Oil was dropping. Brent Oil Futures crude is down 1.4% to $75.64 per barrel while Crude Oil WTI Futures is down 1.5% to $71.08 per barrel. To $1,973, gold futures saw a 0.06% decline.

USDJPY Analysis

USDJPY has broken the Descending channel and the market has retest and rebound from the support area of the minor Descending triangle pattern.

If our goals are met in a forecasted manner, Bank of Japan Governor Ueda said there is time to discuss ending the easy monetary policy. A simple policy’s removal from the economy will have an impact on finances and consumer spending. Additionally, they must consider how best to liquidate BoJ’s ETF holdings in preparation for an economic soft landing.

On Wednesday, Bank of Japan Governor Kazuo Ueda stated that when price target achievement is anticipated, we will discuss the specifics of an exit strategy and disclose information as necessary. BoJ’s financial situation will be impacted by current economic, price, and financial developments. BoJ must make sure that its finances are in good shape to prevent unintended market attention from influencing monetary policy decisions. It is too soon to discuss a specific plan for how the BoJ might sell ETFs in the future. Shunichi Suzuki, the finance minister for Japan, stated that as part of efforts to secure a source of income, “the government must investigate whether govt can buy BoJ’s ETF holdings at book value.

USDCHF Analysis

USDCHF is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern.

It is more likely, according to researchers and a Major Banks survey, that the Bank of Canada will postpone raising interest rates today. Strong GDP, inflation, and retail sales data will drive any interest rate increases the Bank of Canada makes at its upcoming meeting or by the end of 2023.

The Swiss bank stated in a regulatory filing on Tuesday that UBS anticipates concluding its agreement with the Swiss government to cover up to 9 billion Swiss francs in losses from its emergency takeover of Credit Suisse by June 7. UBS agreed to pay the first 5 billion francs of any potential losses under the terms of the takeover arranged by Swiss authorities in March, and the government agreed to pay the remaining up to 9 billion francs. According to documents filed with the U.S. Securities and Exchange Commission, UBS Group AG anticipates that the Loss Protection Agreement will be completed by June 7, 2023. According to the SEC filing, any additional loss guarantee that is greater than CHF 14 billion and was not included in the Special Ordinance requires a separate legal foundation in the form of parliamentary approval through the regular legislative process in addition to the commitment credit. One of the last obstacles that UBS must overcome before it can formally close the acquisition of its smaller rival is the government agreement.

The UBS anticipated closing the deal in the second quarter of 2023, as stated in the SEC document, which was dated June 5. The bank stated on Monday that it anticipated concluding the acquisition as early as June 12. The filing also revealed that UBS and Switzerland’s financial watchdog, FINMA, were in talks about the capital and liquidity specifications for the combined bank. In an email response to a Reuters inquiry, FINMA stated: “We can confirm that the higher “too big to fail” capital requirements due to the progressive component will fully apply to UBS after an appropriate transitional period. It stated that higher capital requirements would be implemented gradually beginning at the end of 2025 and finished at the latest by the beginning of 2030.

EURUSD Analysis

EURUSD has broken the Descending channel and the market has retest the broken area of the channel.

German industrial production came in at 0.30% MoM, down from the previous reading of 2.1% and the market expectation of 0.60%. Already, as a result of ECB rate increases, German factory orders and Euro retail sales are slowing down.

In the early hours of Wednesday’s London open, EURGBP is still under pressure around the intraday low near 0.8600. In doing so, the cross-currency pair ignores pessimism in the UK and hawkish remarks from ECB officials in favour of taking cues from the depressing German data. The Industrial Production figures for Germany increased to 0.3% MoM from -2.1% prior and 0.6% market forecasts, while the annual growth rates decreased to 1.6% from 2.3% previous readouts and 1.2% anticipated. In contrast, Isabelle Schnabel, a member of the ECB Governing Council, dismisses the recent dovish worries by claiming that the impact of our tighter monetary policy on inflation is anticipated to peak in 2024. Before, the Euro’s value was hampered by the Eurozone’s easing inflation expectations as well as the Eurozone’s and Germany’s disappointing factory orders and retail sales reports. The UK Prime Minister Rishi Sunak’s impending visit to the US and concerns that the British economy will be forced to deal with too much inflation and a lack of productivity growth weigh on the EURGBP exchange rates as well.

Looking ahead, a light calendar will advise EURGBP traders to focus on local politics and UK PM Sunak’s visit to the US for guidance. According to a British Government press release, British Prime Minister Rishi Sunak will promote a strengthening of economic ties between the United Kingdom and the United States when he addresses the nation’s lawmakers and business representatives during his trip to Washington, D.C., this week, Reuters reports. In conclusion, EURGBP bears are likely to maintain control as recent Eurozone statistics irritate ECB doves and higher British inflation keeps pointing to future rate hikes by the BoE.

The impact of our tighter monetary policy on inflation is anticipated to reach its peak in 2024, according to European Central Bank (ECB) Governing Council member Isabelle Schnabel in an interview with De Tijd on Wednesday. She was quick to add that there is a lot of uncertainty regarding the strength and speed of this process. Inflation at the base level is still high. There is still more to cover. How much further the ECB will raise rates depends on the data. A peak in underlying inflation is insufficient to guarantee success.

GBPJPY Analysis

GBPJPY is moving in an Ascending channel and the market has rebounded from the support area of the minor Box pattern.

Since the year 2023 began, GBP has performed well against counter pairs. In comparison to the prior year, domestic data performed well as well. In May, inflation decreased slightly from the previous month’s double-digit growth. In 2023, the Bank of England plans to raise rates four times, from the current 4.50% to 5.41%. GDP, employment, and manufacturing data for the UK will determine the direction of interest rates at the Bank of England meeting on June 22.

The British pound might be at the mercy of some of its peers in a week with few UK macroeconomic data points. The UK macro data have generally underperformed since mid-May, according to the Economic Surprise Index, following a spectacular run of outperformance since February. However, the stronger-than-anticipated data since the beginning of the year has led to upgrades in the year’s economic outlook. While this is happening, the probability of a Bank of England rate hike this month has increased due to the slower-than-expected moderation of UK inflation in April.

Following a pause in April, the BOE increased its benchmark rate by 25 basis points in May. The market is pricing in nearly four rate increases by year’s end, raising the terminal rate from 4.50% to 5.41%. Before the BOE meeting on June 22, data on the UK’s manufacturing output, GDP, and jobs will be released. This data could cause some volatility for the pound. The pound may need a rest until then after a stellar run against some of its competitors.

CADCHF Analysis

CADCHF is moving in an Ascending channel and the market has reached the resistance area of the minor consolidation pattern.

Researchers and a Major Banks survey indicate that it is more likely that Bank of Canada will delay raising interest rates today. Any time the Bank of Canada raises interest rates at its next meeting or by the end of 2023, it will do so because of strong GDP, inflation, and retail sales data.

Here are the predictions made by the economists and researchers of six major banks regarding the upcoming announcement from the Bank of Canada, which is scheduled to make its interest rate decision on Wednesday, June 7 at 14:00 GMT. BoC is anticipated to maintain interest rates at 4.5%, but may indicate that it is prepared to increase them further if necessary. Macroeconomic forecasts will not be updated until the meeting in July. TDS We anticipate that the BoC will exit the doldrums in June with another 25 bps increase to 4.75%. Without clear indications of a significant slowdown in the first half of 2023, the Bank’s conditional pause is becoming less tenable as economic data has remained resilient. We anticipate a somewhat pessimistic statement from the Bank, one that leaves the door open for additional tightening in the upcoming months. ING- However, given the stronger-than-anticipated GDP and consumer price inflation as well as the continued strength of the labour market data, we cannot completely rule out a surprise interest rate increase by the BoC. The Canadian Dollar should be supported by a hawkish hold.

RBC Economics: The Bank of Canada is likely actively considering raising interest rates as a result of the economy’s strong start to 2023. But ultimately, we believe it will continue the hiatus in hikes that started in January, keeping the overnight rate constant at 4.5% for the time being. NBF – We anticipate that the BoC will keep its overnight target at 4.5%. Although the most recent headline data has not exactly been encouraging, we still think that some patience is required or warranted in order to better understand whether the apparent recovery in inflation, housing, and GDP will be sustained. It is also important to note that the decision will not be announced along with a new MPR. Even though a rate increase is not ruled out, there will not be a Macklem-Rogers press conference or new economic or inflation forecasts to back it up. The day after the decision, the BoC will hold a speech and press conference, but the speaker will be Deputy Governor Paul Beaudry. Once more, it stands to reason that the top official(s) of the BoC should deliver the news, preventing any potential interpretational problems. Even so, the Bank has not shied away from uncertainty in the past year, and even though we lean in the direction of no change, this forecast does not have a high degree of confidence. Investors beware—this meeting is very much live.

Citi – Given that both activity and inflation have been steadily stronger than anticipated, the 4.50% level of policy rates is unlikely to be sufficiently restrictive to slow down activity and lower inflation to 2%. The BoC is therefore anticipated to increase rates once more by 25 bps. Despite the fact that we do not foresee many changes in this area, the policy statement’s guidance will be crucial. The Governing Council should still be instructed to “remain prepared to raise the policy rate further if necessary to return inflation to the 2% target.” Maintaining the current guidance could be seen as somewhat hawkish. Wells Fargo – For the third consecutive meeting, the BoC will decide to keep interest rates at 4.50%. There is still a chance that the BoC will increase its policy rate above 4.50% if inflation trends remain strong and economic activity is resilient. The more pertinent discussion, in our opinion, is how quickly the BoC implements monetary easing in the upcoming quarters. We now anticipate the BoC to delay rate cuts until the first quarter of 2019, as opposed to our previous prediction that rate cuts would start in Q4-2023. This is because we now anticipate the Fed to start monetary easing in 2024 and because Canadian inflation is slowing down steadily but gradually.

AUDCAD Analysis

AUDCAD is moving in an Ascending channel and the market has reached the higher high area of the channel.

Australia’s first-quarter GDP in 2023 was 2.3% as opposed to the 2.4% anticipated and 2.7% recorded in 2022. The economy is slowing down from its peak, the RBA has already made 400 basis points, and the RBA anticipated a soft landing for GDP in the market.

After the Australian economy expanded less quickly than anticipated in the first quarter of the year, In the January-March quarter, the economy expanded 2.3% on-year, slower than the 2.7% seen in the final quarter of 2022 but still higher than the 2.4% expected. The growth represents the sixth consecutive increase, but it has undoubtedly slowed in recent quarters as the economy adjusts to the enormous 400 basis point increase in interest rates. At a conference in Sydney on Wednesday, Reserve Bank of Australia Governor Philip Lowe acknowledged the possibility of a more pronounced slowdown in the economy, saying the road to a soft landing was narrow and “significant risks” threatened the outcome. Despite a slight decline from a peak of 7.9%, headline inflation increased by 6.8% in April and 7.0% in the first quarter of 2018. The market was expecting the benchmark rate to reach 4.18% by September before Tuesday’s meeting, but now there is a strong likelihood that the RBA will raise rates another 25 basis points, bringing the terminal rate to 4.32% by the end of the third quarter.

The main focus right now is on the China trade data that is due later in the day on Wednesday. In the second-largest economy in the world, imports are anticipated to have decreased 8% year over year in May after falling 7.9% in April. Factory activity decreased in May faster than anticipated due to weaker demand, casting doubt on the outlook for the economy Australia’s top export market. However, news that China is developing fresh policies to help the real estate market has revived hopes for focused stimulus to help the economy.

NZDUSD Analysis

NZDUSD is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern.

With an export decline of 7.5%, China’s trade surplus shrank to its lowest level in 13 months in May. The global central banks are raising interest rates more than ever as a result of weaker demand for materials imported from China. For the New Zealand economy to export goods to China more quickly, China’s economic growth is more crucial.

The NZDUSD pair faces selling pressure on Wednesday as it struggles to build on its modest gains from the previous two days. Through the early European session, the pair holds its offered tone and is currently trading close to the day’s low, around the 0.6060 area, down about 0.20%. Worries about a global economic slowdown are increased by weaker-than-expected Chinese macroeconomic data released earlier on Wednesday, which dampens investor confidence. The US Dollar, a safe-haven currency, receives some support from a generally weaker tone in the equity markets, which puts some downward pressure on the NZDUSD pair. In fact, a surprise 7.5% decline in exports in May caused China’s trade surplus to reach a 13-month low. The data indicates that, in the wake of deteriorating economic conditions worldwide, overseas demand for Chinese goods remained weak. The second-largest economy in the world is subsequently faced with new challenges, and demand for antipodean currencies, such as the Kiwi, is reduced.

The Reserve Bank of New Zealand’s explicit signal that it was finished with its most aggressive hiking cycle since 1999 further devalues the New Zealand Dollar. However, the ambiguity surrounding the Federal Reserve’s upcoming policy decision may discourage USD bulls from making risky bets and assist in containing losses for the NZDUSD pair. In fact, expectations for a 25 bps lift-off at the June FOMC meeting were maintained by the most recent data on inflation and the labour market. However, dovish comments made by a number of Fed officials last week increased market expectations of a soon-to-come pause in the cycle of policy tightening by the US central bank. The probability that the Fed will maintain current interest rates next week is higher according to market pricing at the moment. The expectations cause US Treasury bond yields to continue to decline, which should continue to weigh on the US dollar and provide some support for the NZD/USD pair. The recent recurrent failures near the round-figure 0.6100 support bearish traders. However, given the aforementioned fundamental backdrop, it is prudent to hold off on positioning for any additional intraday depreciating move in the absence of pertinent market-moving economic releases from the US until there is strong follow-through selling.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/