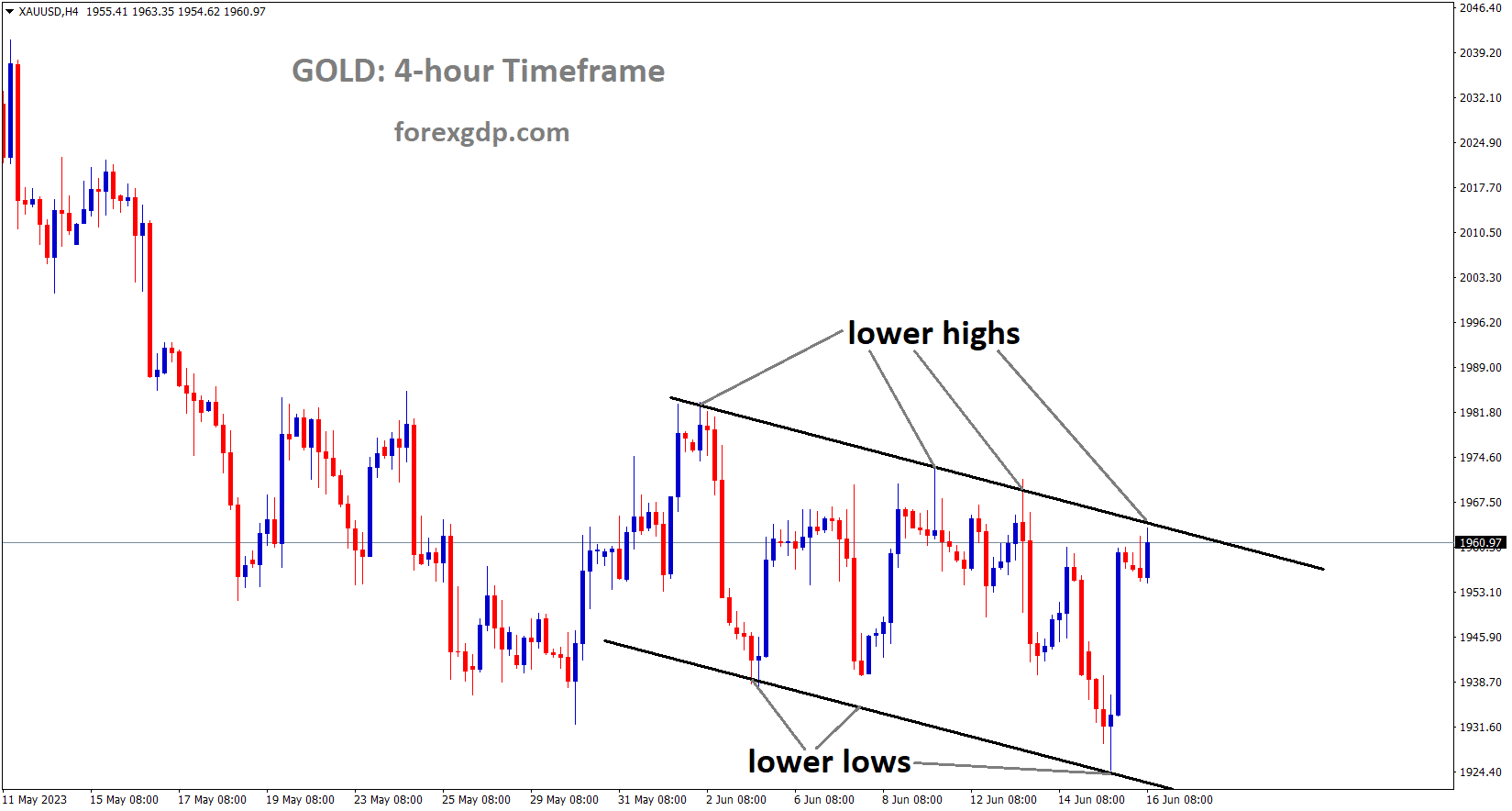

GOLD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel.

After all central banks raised interest rates to curb inflation, gold prices began to fall. For non-yielding assets like gold, rising yields are difficult.The Chinese economy was more negatively impacted by COVID-19 in the manufacturing and industrial employment sectors. As a result of China’s economic worries, gold demand is slowing down.

On Thursday, gold prices continued to decline in Asia and Europe as these markets, like all others, processed the US Federal Reserve’s widely anticipated decision to halt its protracted cycle of interest-rate hikes in the previous session. The Fed’s decision might have been anticipated to support the market because rising interest rates frequently have a negative impact on non-yielding assets like gold. The US central bank appears to have decided that the pause will essentially be a hawkish pause, which is what it will undoubtedly be called. This means that even though the central bank fully anticipates raising the Federal funds rate once more, if not more than once, it still plans to wait and assess the results of its previous round of increases. Given this, it is easier to understand why the gold market should have declined. Perhaps the biggest reason for optimism among investors in the safest haven is the possibility that the US is close to ending its cycle of monetary tightening. Given the persistence of inflation across the globe, the majority of other central banks are probably still in the thick of things.

SILVER Analysis

XAGUSD Silver Price is moving in the Descending channel and the market has reached the lower high area of the channel.

Although there is much economic disagreement regarding the metal’s true usefulness as a hedge against rising prices, many investors insist that it is. Nonetheless, rampant inflation will likely keep a floor under the gold market. It is noteworthy that despite significantly higher interest rates almost universally, prices are still relatively close to historic high levels. Perceived “haven assets” are also unquestionably supported by the backdrop of the Ukrainian conflict, the South China Sea tensions, and the resilience of the post-covid recovery. With US retail sales and sentiment data likely to have an impact on interest rate expectations and, ultimately, on gold, the week still carries some event risk for this market.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher high area of the channel.

Interest rates at the Bank of Japan remain unchanged at -0.10%, as does the YCC. Inflation will reach the 2% target in this fiscal year, and as BoJ Governor Ueda noted, there is uncertainty in the Japanese economy. Prices in the corporate sector will rise, which will cause inflation to soar in the coming months. It is noted that core inflation in April was 3.4%. Due to Japan’s lax policy versus the tight policy of global central banks, the Japanese Yen declines against counter pair currencies.

In an effort to support the emerging economic recovery and sustainably meet its inflation target, the Bank of Japan (BOJ) maintained ultra-loose policy settings, particularly the closely watched yield curve control policy, which caused the Japanese yen to weaken slightly against the US dollar. After BOJ Governor Kazuo Ueda stated last month that the central bank would ‘patiently’ maintain the current policy because there is still some way to achieve its 2% inflation target stably and sustainably, the BOJ was widely expected to maintain its ultra-easy monetary policy at its meeting on Friday. The central bank stated that the level of uncertainty surrounding the Japanese economy is very high on Friday.

Ueda also stated that the central bank anticipates inflation to decline to below 2% by the midpoint of the current fiscal year and then rise. Ueda added last week that the nation’s corporate price-setting behaviour was displaying changes that could cause inflation to rise faster than anticipated. Core inflation in Japan reached 3.4% in April, well above the BOJ’s 2% target, and an adjustment to the YCC policy is only a matter of time. At its April meeting, the BOJ did away with its long-standing forward guidance while swiftly reacting to changes in economic activity and price levels. As a result, the meeting on July 28 will be live.

USDCAD Analysis

USDCAD is moving in the Box pattern and the market has reached the horizontal support area of the pattern.

Compared to the -0.10% predicted, US retail sales growth for the month of May increased by 0.30%. US industrial production for the month of May came in at -0.20% instead of the predicted 0.10%. In contrast to expectations of 249K, initial jobless claims for the week totaled 262K. Following yesterday’s publication of negative data, the US Dollar fell, which benefited the Canadian Dollar.

Early on Friday, amid sluggish markets, USDCAD posts marginal gains at its lowest level since September 2022, as of the previous day. After falling the most in two weeks the day before, the Loonie pair now licks its wounds near 1.3225. In addition to the shaky markets, the recent inaction of the quote may also be related to conflicting worries about the Bank of Canada (BoC) and the US Federal Reserve. The Canadian job numbers disappointed the policy hawks after the BoC shocked the markets by raising rates last week. On the other hand, the Fed’s hawkish pause could not win any more plaudits given that the most recent US data show a mixed picture. In spite of this, US retail sales growth increased by 0.3% in May, beating expectations of -0.1% and 0.4%, while the core readings, or mean retail sales excluding autos, were in line with market expectations of 0.1%, down from 0.4% in April. While the Philadelphia Fed Manufacturing Index declines to -13.7 for the aforementioned month from -10.4 prior and compared to -14 market forecasts, the NY Fed Empire State Manufacturing Index increases to 6.6 in June from -15.1 expected and -31.8 prior. In the same vein, initial jobless claims for the week ending June 9 were revised upward to 262K from 249K, while US industrial production for May fell to -0.2% from 0.1% expected and 0.5% from the prior month.

After seeing the Bank of Japan decision, other factors such as a light calendar and conflicting concerns about China spur the recovery of the WTI crude oil price. In contrast, the WTI crude oil grinds near a one-week high, mildly offered near $70.70 by press time, while the US Dollar Index grinds near 102.20-30 while trying to reverse the largest daily loss in three months. Looking ahead, it will be crucial to keep an eye on the Canadian Wholesale Sales for April, the US Michigan Consumer Sentiment Index (CSI) preliminary readings, and the five-year inflation expectations for June for clear indications. However, after his most recent failure to persuade hawks, major attention will be focused on Fed Chair Jerome Powell’s testimony the following week.

USD Index Analysis

USD index has broken the Descending triangle pattern in downside.

According to the September dot plot, a further rate increase of 50 basis points to 5.1% to 5.6% in 2023 is anticipated. The US economy is dealing with low unemployment and lower inflation than at its peak. According to economists, the FED may raise rates in July with a higher probability.

The Federal Reserve may increase interest rates by another half-point, bringing them to 550–575. The most recent SEP dot plot indicates that chair Powell is still struggling with high and persistent price pressures. When compared to the previous SEP, projections for this year’s PCE inflation were also increased. The midpoint of the target range was raised from 5.1% to 5.6% for 2023. The market is indicating that the US central bank will only raise rates by 25 basis points this year before starting a rate-cutting cycle in 2024, despite the Fed’s indications that it is willing to raise rates by 50 basis points, data dependent.

AUDUSD Analysis

AUDUSD is moving in an Ascending channel and the market has reached the higher high area of the channel.

Retail sales, weekly jobless claims, and other US macroeconomic data were mixed, making them favourable for the Australian dollar and unfavourable for the US dollar. This week’s strong employment data and low unemployment rate helped the AUD gain ground against the USD.

The AUDUSD pair experiences some selling pressure during Friday’s Asian session and loses some of the gains made the day before, which helped it reach its highest level since February 22 in the 0.6900 neighbourhood. The pair is currently trading in the 0.6870 area, down more than 0.20% for the day, and appears to have ended a run of six straight winning days. The US Dollar makes a modest recovery from a five-week low after suffering significant losses over the previous three days. Due to the recent massive rally of over 500 pips since the start of the current week, traders are then prompted to reduce their bullish bets around the AUDUSD pair. The Federal Reserve is believed to be approaching the peak of its policy tightening cycle, which limits the upside potential for the USD and calls for caution before positioning for any significant corrective slide for the major.

Recall that the US central bank made the decision to maintain interest rates at the conclusion of a two-day policy meeting earlier this week, but also cautioned that by the end of the year, borrowing costs may still need to increase by as much as 50 basis points. That said, the prospects for further rate hikes by the Fed to combat persistently high inflation were cast into doubt by Thursday’s rather unimpressive US macro data, specifically Industrial Production, Weekly Jobless Claims, and Retail Sales. In actuality, the US CPI is still above the Fed’s 2% target, at 4.0% in May. The overnight decline in US Treasury bond yields was caused by uncertainty regarding the Fed’s rate-hike trajectory, which could discourage USD bulls from making risky bets. In addition, the Reserve Bank of Australia’s (RBA) unexpected 25 bps lift-off last week and hawkish policy statement may continue to support the Australian dollar. In the absence of any pertinent macroeconomic data from the US, this may further help to limit the downside for the AUDUSD pair. Spot prices, however, are still expected to post significant gains for a third straight week.

NZDUSD Analysis

NZDUSD is moving in an Ascending channel and the market has reached the higher high area of the channel.

The NZD Business PMI for June came in at 48.9, below both the 50.2 expectation and the previous reading of 49.1. This is the third month in a row that New Zealand’s business confidence data have decreased. NZD remains stronger this week against USD despite this.

In the early hours of Friday’s Asian session, the NZDUSD accepts bids to retest its intraday low near 0.6230. In doing so, the Kiwi pair reverses course from the highest levels seen since May 24 and breaks a three-day uptrend amid unfavourable New Zealand data. NZ Business PMI for June was 48.9 as opposed to the 50.2 expectations and 49.1 recorded in May. The Pacific country’s activity gauge registered this as the third consecutive month of declining business performance. In addition to the unfavourable NZ data, the NZDUSD bulls were able to pause at the multi-day high thanks to the RSI 14 line’s above 50.0 levels. For intraday traders, the NZD/USD price is restrained by the 100-DMA support near 0.6220 and the bullish MACD signals; however, a break of either of these supports can quickly push the quote to the 38.2% Fibonacci retracement of the October 2022 to February 2023 upside, which is close to 0.6150.

The resistance-turned-support line that has been in place since early May, at the latest around 0.6120, will then take centre stage. It is possible that the NZD/USD will fall below the 0.6120 support level and continue to fall, possibly reaching the previous monthly low of 0.5985. On passing the most recent peak of 0.6250, the NZDUSD buyers can aim for the 23.6% Fibonacci retracement level of around 0.6300. However, a horizontal area with multiple levels marked since early February and a 4.5-month-old resistance line near 0.6330 and 0.6385-90, respectively, seem like tough nut to crack for the Kiwi pair buyers to overcome afterward.

EURGBP Analysis

EURGBP is moving in the Descending triangle pattern and the market has reached the horizontal support area of the pattern.

Joachim Nagel, the head of the Bundes Bank and an ECB policymaker, claimed that Germany’s GDP decreased to 0.30 percent in 2023 before increasing to 1.2% in 2024 and 1.3% in 2025. It is anticipated that German inflation will be 6.0% in 2023, 3.1% in 2024, and 2.7% in 2025. This year, inflation is the main theme and it is worse. Inflation in Germany will be reduced gradually.

Joachim Nagel, the head of the Bundesbank and a policymaker at the European Central Bank (ECB), will participate in a panel discussion titled “The Macroeconomic Outlook: Growth, Inflation and Risks” at a gathering sponsored by the Group of Thirty in Amsterdam. German economic growth is projected to be 0.3% in 2023, 1.2% in 2024, and 1.3% in 2025. At 6.0% in 2023, 3.1% in 2024, and 2.7% in 2025, inflation in Germany is projected. To reduce the likelihood of inflation becoming more persistent, decisive monetary policy action is essential. Although the economy is expected to only recover slowly, inflation is at last decreasing. The risk of inflation is elevated.

GBPCAD Analysis

GBPCAD has broken the Descending channel in upside.

Due to the FED pausing its rate hike this week, the UK pound increases. The Bank of England’s ongoing cycle of rate increases strengthens the pound against the dollar. GBP GDP increased by 0.20% in April compared to the previous reading of -0.30%, strengthening GBP against the USD.

GBPUSD holds steady at 1.2780–70 during the early hours of Friday morning in London as traders on the Cable pair look for additional cues to support the previous day’s strong rally. This is the currency pair’s highest level in 14 months. Nevertheless, amid widespread US Dollar weakness and hawkish concerns about the Bank of England, the Pound Sterling rose the most in a week while rising for a third straight day to re-establish the multi-month high. The GBPUSD bulls were unable to be subdued earlier in the week despite a mixed batch of UK data and hawkish BoE worries, largely because of the previously encouraging inflation data. The Gross Domestic Product (GDP) of the UK increased by 0.2% in April compared to the previous month’s -0.3% decline, but Industrial Production declined in the same period. Nevertheless, the Manufacturing Production and the Services Index for the three months ending in April both fall short of expectations. To counteract the largest daily loss in three months, the US Dollar Index (DXY) picks up bids around 102.30, which in turn encourages buyers of Pound Sterling. Even though the policymakers did say the same thing on Wednesday, the quote fell sharply the day before due to conflicting US data and the market’s lack of confidence in the Fed’s rate hike in July.

On Thursday, the US Retail Sales growth rate was 0.3% for May, up from the 0.4% previous readings and the -0.1% expected, while the Core readings, or mean Retail Sales ex-Autos, were in line with 0.1% market forecasts for the same month. Additionally, the June NY Fed Empire State Manufacturing Index increased to 6.6 from -15.1 expected and -31.8 prior, while the June Philadelphia Fed Manufacturing Index decreased to -13.7 from -10.4 prior and -14 market expectations. Additionally, US industrial production for May decreased to -0.2% from 0.1% expected and 0.5% from the previous month, while initial jobless claims for the week ending June 9 were revised upward to 262K from 249K. In light of this, market participants seem to be less bearish on the Fed and more hawkish on the BoE, keeping the Cable on the bull’s radar despite the most recent price decline. In order to predict future readings of the Michigan Consumer Sentiment Index and five-year inflation expectations for the same month, the UK’s Consumer Inflation Expectations for June will be used to guide intraday GBPUSD movements.

CADCHF Analysis

CADCHF is moving in an Ascending channel and the market has reached the higher low area of the channel.

Due to lower interest rates, Poland’s top court backed consumers getting mortgages in foreign currencies like Swiss Francs. Now that Swiss Bank is raising rates and the Swiss franc has strengthened against the Polish zloty, consumer repayments will require larger monthly payments.

The same problem with foreign mortgages that Hungary had a year ago is now present in Poland, Croatia, and Romania.

In a protracted case that the Polish regulator has warned could cost the nation’s banks 100 billion zlotys ($24 billion), the top court of the European Union on Thursday sided with Polish borrowers with mortgages denominated in Swiss francs. Due to lower interest rates, hundreds of thousands of Poles obtained mortgages in foreign currencies, primarily Swiss francs. But now that the Swiss franc has appreciated against the Polish zloty and as a result of Swiss interest rate increases, they are paying them back in much larger amounts than they had anticipated. Analysts had anticipated the court’s decision, which prohibits banks from charging for the cost of capital on foreign currency loans that were deemed invalid because they contained unfair terms. In the event that a mortgage loan agreement is void due to unfair terms, EU law does not prevent consumers from suing the bank for damages beyond a refund of the monthly payments made, the court said in a statement. It prevents the bank, however, from making comparable claims against customers. The decision was in accordance with a February opinion provided by a court adviser.

Although there will be a significant cost to the Polish banking industry, analysts believe it will be able to withstand the blow. According to the court’s ruling, the argument regarding the stability of the financial markets is irrelevant to how the directive should be interpreted in order to protect consumers. At 1046 GMT, the WIG Banks index for Poland was down 1.1%. Hungary forced its banks to convert their Swiss franc mortgages into forints years ago as they became more expensive, and similar issues with foreign currency mortgages have also affected Poland, Croatia, and Romania.

The ruling was unfavourable for the banking industry and the overall economy, according to the Polish financial regulator KNF, but lenders in the nation were secure.The ruling would make banks less willing to lend, according to Tadeusz Bialek, president of the Polish Bank Association, which would hurt the economy. Banks have been offering out-of-court settlements to clients, but many would rather go to trial, especially given that, according to Votum Robin Lawyers, judges have ruled in favour of plaintiffs in 97% of cases in the first quarter.

A partner at the law firm Pilawska Zorski, Andrzej Zorski, predicted that the decision would encourage more mortgage holders to sue banks. After today’s ruling, borrowers who had been scared to sue the bank for reimbursement for the use of capital should no longer be so concerned, he wrote in an email. Kamil Chwiedosik, the organization’s founder who assists mortgage holders in legal disputes with banks, declared himself “ecstatic,” while 40-year-old Zofia Karaszewska, who holds a Swiss franc mortgage, said she had decided to sue the bank that had provided her with the loan. I felt like I got so much support here, both as a customer and as a victim, that I should get this money instead of the bank, she said over the phone to Reuters. It was described by Bialek as a “cheap and quick way of amicably resolving cases” and that banks had already reached 60,000 settlement agreements with customers.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/