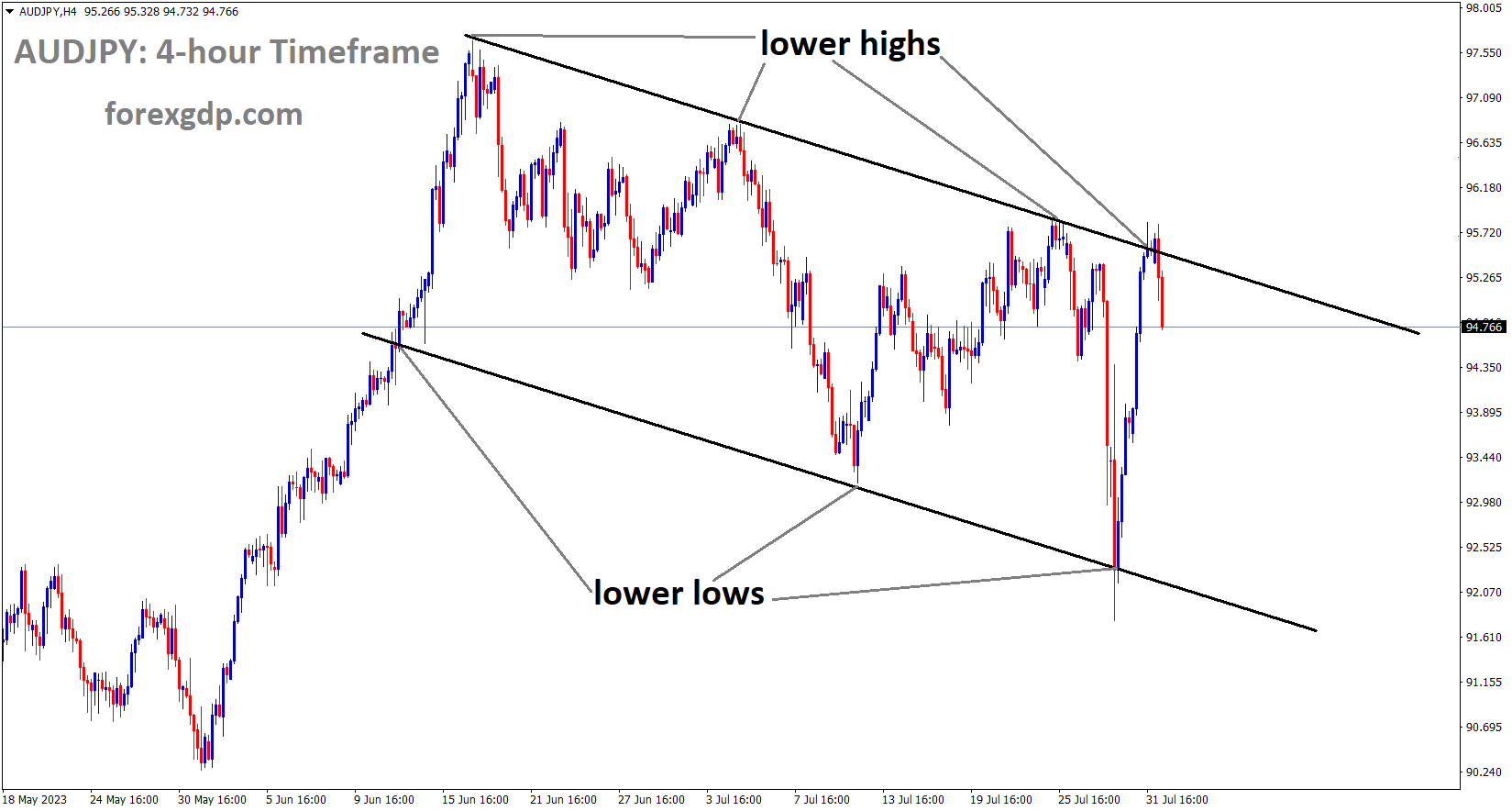

AUDJPY Analysis

AUDJPY is moving in the Descending channel and the market has fallen from the lower high area of the pattern.

Shunichi Suzuki, the finance minister of Japan, stated on Tuesday that he would “closely monitor FX market movements, which have seen changes in the environment. FX should reflect fundamentals steadily. By making YCC flexible, the BoJ decision on Friday would make monetary easing more sustainable. The BoJ is in charge of choosing particular monetary policy instruments.

XAUUSD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel.

Due to the resumption of the US-Sino trade war and China’s restrictions on drone exports to the US, gold markets are rising. Due to concerns over public safety, the US imports 50.0% of all Chinese drones.

As market participants wait for the United States manufacturing activity data for July on early Tuesday in Asia, the gold price XAUUSD pauses its two-day recovery from the key moving average confluence. In spite of this, the most recent Federal Reserve Fed Bank Loan Survey revealed gloomy results and combined with news from China to keep the US Dollar firmer, which in turn propelled the Gold Price run-up below the crucial $1,985 hurdle, close to $1,965 by the time of press. It is important to note that the risk-on attitude allowed XAUUSD to continue firming up for the past two days. In the wake of recent negative headlines from China and a dismal Federal Reserve Fed Bank Loan Survey, the price of gold has lost some of its two-day recovery gains. But late on Monday, according to Reuters, China’s Commerce Ministry rekindled concerns about a Sino-US trade war by announcing measures to restrict exports of some drones and equipment associated with them beginning on September 1. The ministry cited “national security and interests” as its justification. It is important to note that China is a significant exporter of drones to other top-tier economies, including the US. According to earlier statements made by US policymakers, more than 50% of the drones sold in the US, most of which are used for public safety, were manufactured in China by DJI.

On the other hand, US banks reported tighter credit standards and weaker loan demand during the second quarter Q2 2023, according to the Fed’s quarterly Senior Loan Officer Opinion Survey SLOOS. The market’s cautious attitude before the US ISM Manufacturing PMI and the final readings of the S&P Global PMIs for July also puts a strain on the previously stronger risk appetite and the upward movement of the gold price. S&P500 Futures, which had a positive start to the week, are still on the sidelines, while interest rates on US Treasury bonds are rising after falling for the last two days in a row. Reducing concerns about major central banks raising interest rates, combined with positive results from US mega-corporations during the most recent earnings season, helped to boost sentiment and keep the gold price firmer. However, it is important to note that the stronger US Dollar Index encourages XAUUSD buyers. The China State Council unveiled a slew of stimulus measures designed to reduce waste and increase consumption, which in turn fueled the risk-on sentiment in the market on Monday morning. The improvement in China’s official PMI was an additional factor. Despite this, China’s official NBS Manufacturing PMI rises to 49.3 from 49.0 in the previous reading and 49.2 expectations, while the Non-Manufacturing PMI declines to 51.5 from 53.2 in the previous reading.

Conversely, the Chicago PMI increased to 42.8 from 41.5 prior to 43.0 market forecasts, while the Dallas Fed Manufacturing Business Index improved to -20.0 for July from -23.2 prior versus -26.3 expected. It should be noted that even though the US Dollar Index managed to stay firmer on the day, Friday’s weaker prints of US inflation clues and the weekend remarks from Minneapolis Fed President Neel Kashkari criticising higher interest rates also put downward pressure on the dollar against the Australian dollar. In spite of this, the US Dollar Index DXY managed to hold its ground on Monday, advancing steadily towards 102.00 by the time of publication. Now that the hawkish bias towards the US Federal Reserve Fed has recently mellowed, the US Manufacturing Purchasing Managers Indexes PMI from the ISM and S&P Global for July will be crucial to determining intraday moves of the Gold Price. It should be noted that since it is US Nonfarm Payrolls NFP week, the employment portion of the scheduled PMIs will be closely monitored.

USDCAD Analysis

USDCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Due to China’s anticipated decrease in energy consumption and the strengthening of the US dollar, oil prices have slightly declined from their recent highs. This week’s Canadian S&P Global Manufacturing PMI is planned, and CAD will move in the direction of the news being reported.

Bulls on the USDCAD pair maintain control at around 1.3230 as they push the intraday high ahead of Tuesday’s European session despite a stronger US Dollar and a decline in WTI crude oil, Canada’s main export. In doing so, the Loonie pair consolidates its largest daily loss in two weeks prior to the release of the US and Canadian July activity data. However, the Dollar Index DXY maintains modest gains at a three-week high of roughly 102.00 set earlier in the day as positive Fed talks join firmer US data and unfavourable China statistics. On Monday, Austan Goolsbee, the president of the Chicago Fed, defended the hawkish actions taken by the US central bank, and the Dallas Fed Manufacturing Business Index improved to -20.0 for July from -23.2 previously versus -26.3 anticipated. Additionally, Chicago’s PMI increased from 41.5 to 42.8 versus 43.0 market expectations. In doing so, the DXY disregards Friday’s softer US inflation clues prints as well as Neel Kashkari’s weekend comments criticising higher interest rates. The Caixin Manufacturing PMI for China for July fell to 49.2 from 50.5 the month before, below the market consensus of 50.3, and reached its lowest level since January. It does not match its upbeat NBS counterpart.

It is important to note that worries about the US-China trade war, which are stoked by Beijing’s restrictions on drone exports in retaliation for US tech and trade war tactics by citing “national security” measures, encourage pessimists and allow the US Dollar to hold its value due to its appeal. In other news, WTI crude oil records its first daily loss in four days while falling from its highest level since April 17, down 0.30% intraday to $81.30 by press time, on concerns about a slowing in China’s energy demand as well as the stronger US Dollar. Looking ahead, the USDCAD pair’s intraday movements will be influenced by the Canada S&P Global Manufacturing PMI for July, the US ISM Manufacturing PMI for the same month, as well as the US JOLTS Job Openings for June. The American Petroleum Institute’s API weekly crude oil inventory data will also be crucial.

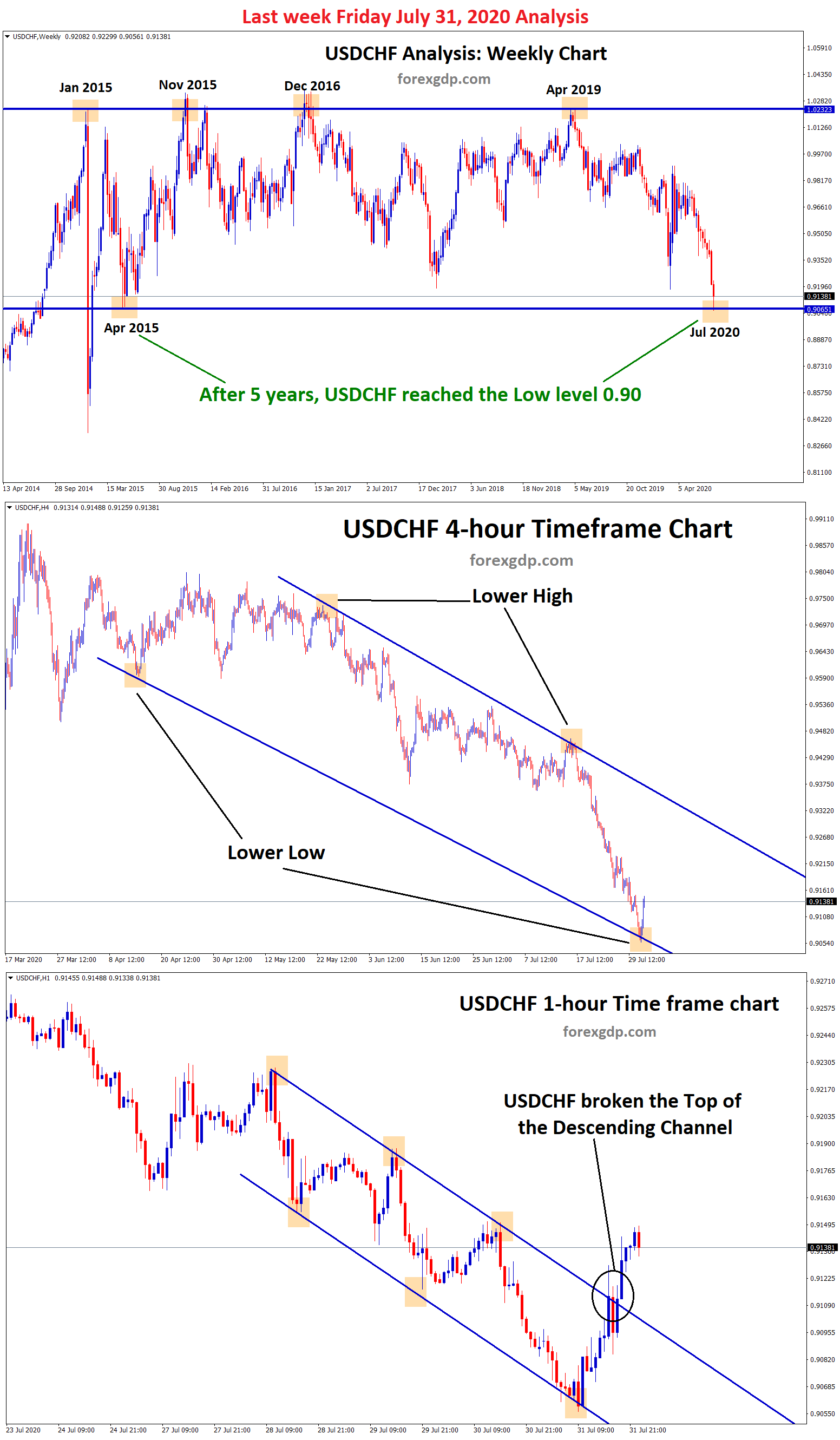

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Following last week’s 25 bps increase in the FED’s policy rate, the USDCHF pair gains strength against the CHF. Since 1980, this rate increase is the largest. The FED makes this decision in the meeting due to Q2 GDP resilience and declining inflation.

Following an intraday dip to levels below 0.8700 during the Asian session, the USDCHF pair draws some buying and moves back towards a two-week high reached last Friday. Spot prices are currently trading in the 0.8725 area and appear ready to build on last week’s decent recovery from the mid-0.8500s, which is a new low since January 2015. The safe-haven Swiss Franc CHF is thought to be weakening due to an overall upbeat tone in the equity markets, which is also helping the USDCHF pair. The most recent optimism regarding additional stimulus measures from China is still welcomed by investors. The risk-on environment is still supported by this as well as expectations that the Federal Reserve Fed will soften its stance amid signs of easing inflationary pressures. In fact, the markets now appear to be convinced that the US central bank’s fastest cycle of interest rate increases since the 1980s is about to come to an end.

However, the positive US GDP report released last week showed that the economy is remarkably resilient and left the door open for one more 25 bps rate hike in September or November. In addition, Fed Chair Jerome Powell had stated that for inflation to credibly return to the 2% target, the economy still needs to slow down and the labour market to deteriorate. The US Dollar USD is helped by the hawkish outlook to maintain stability near a three-week high, which is seen as another factor supporting the USDCHF pair and supporting the bullish bias. The aforementioned fundamental background suggests that the upward path for spot prices is the one that presents the least amount of resistance. Any intraday decline may therefore now be viewed as a buying opportunity. Despite this, it will still be wise to hold off on declaring that the USDCHF pair has formed a short-term bottom until there is substantial follow-through buying. Investors are now focusing on the US economic calendar, which will include the publication of the ISM Manufacturing PMI JOLTS Job Openings data. This should give the major some significant impetus, along with the general risk sentiment.

China’s Commerce Ministry declared that starting on September 1 they will restrict some drone exports to the US. This is China’s response to the US announcing restrictions on Chip exports to China. After the arrival of well-received domestic numbers and fears related to global news, the US dollar performed resolutely against counter pairs.

The US Dollar Index DXY is still in the lead despite recent inaction near 101.90. As a result, the gauge of the US dollar against six important currencies gains from the US ISM Manufacturing PMI’s haven appeal. Amid a slow Tuesday morning in Asia, news from China and the US Federal Reserve Fed as well as pre-data anxiety drive the DXY. But late on Monday, according to Reuters, China’s Commerce Ministry rekindled concerns about a Sino-US trade war by announcing measures to restrict exports of some drones and equipment associated with them beginning on September 1. The ministry cited “national security and interests” as its justification. The US banks reported tighter credit standards and weaker loan demand during the second quarter Q2 2023, according to the Fed’s quarterly Senior Loan Officer Opinion Survey SLOOS.

It is also important to note that despite mixed US data on Monday, the US Dollar Index DXY managed to hold firmer, advancing towards 102.00 by press time. On the other hand, the Chicago PMI increased to 42.8 from 41.5 prior to 43.0 market forecasts, while the Dallas Fed Manufacturing Business Index improved to -20.0 for July from -23.2 prior versus -26.3 expected. In doing so, the DXY disregards Friday’s softer US inflation clues prints as well as Neel Kashkari’s weekend comments criticising higher interest rates. The S&P500 Futures, which had a positive start to the week, are still inactive, while interest rates on US Treasury bonds are rising after falling for the last two days in a row. Before the final readings of the US S&P Global Manufacturing and Non-Manufacturing PMI for July, DXY traders should keep an eye on the risk catalyst and China Caixin Manufacturing PMI for July for immediate direction. The US ISM Manufacturing PMI for that month will be another important indicator to keep an eye on. It is important to pay close attention to the employment and inflation hints from the scheduled data for clear guidance.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

According to ECB President Lagarde, annualised GDP increased to 0.60% from 0.40% and the April-June month quarter GDP increased by 0.30% from a contraction of 0.10%. As a result of lower inflation and higher GDP in the Eurozone, public purchasing power is higher than anticipated, and the ECB raises interest rates at its next meeting.

Economic data for the Eurozone indicate that the European Central Bank (ECB) is unable to stop the current tightening cycle. While announcing the interest rate policy on July 27, ECB President Christine Lagarde said that any future policy decisions would depend on the availability of data. The Gross Domestic Product (GDP) and inflation data for the eurozone, which were released on Monday, showed that the ECB cannot, at least temporarily, change its stance to neutral. The April–June quarter of the Eurozone’s economy saw positive growth of 0.3% against a contraction of 0.1%, exceeding investors’ expectations of a 0.2% expansion. Instead of growing at the expected 0.4% annualised rate, the GDP increased at a 0.6% rate.

The resilience of the Eurozone economy is demonstrated by the way it managed to escape contraction and outperform forecasts despite higher interest rates. In addition, annual headline inflation came in at 5.3%, beating expectations of 5.2% but still coming in below June’s reading of 5.5%. The core rate of inflation, which excludes volatile prices for food and oil, remained constant at 5.5%, exceeding the forecast of 5.5%. Positive GDP growth and persistent inflationary pressures suggest that consumer spending is stable and has the potential to raise inflation.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Instead of the anticipated 50bps increase, the Bank of England is anticipated to raise interest rates by 25 basis points this week. The UK’s CPI makes it cool for the BoE to raise rates gradually rather than dramatically. More As a result of tightening, the UK housing market will collapse and loans will have higher interest rates to repay.

The likelihood that the Bank of England (BOE) will raise interest rates by a smaller amount at its meeting on Thursday is increasing as it appears that UK price pressures have finally abated from their high levels. Even with the negative surprise in UK June CPI, it will likely be premature to declare victory given that inflation is still significantly above BOE’s comfort level. High inflation and strong wage growth in May indicate that the move will be 25 basis points rather than 50 basis points.

GBPCHF Analysis

GBPCHF is moving in an Ascending channel and the market has reached the higher high area of the channel.

The main focus will be on the BOE’s forward guidance, which contrasts a reiteration of further tightening given persistently sticky inflation with a data-dependent approach. GBP could decline in the first scenario, while GBP could struggle to maintain gains in the second, as forward-looking price and activity indicators point to a downward trend in underlying price pressures. Speculative long GBP positioning is still at its highest level since 2014. However, given the GBP’s continued wide interest rate differentials from some of its peers, the downside is supported.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has reached the lower low area of the channel.

RBA maintains the interest rate at 4.10%, the same as the previous reading. The CPI target set by the RBA is 6.0%, but the most recent data, from the Q2 report, showed that the economy is in sync with the tightening cycle at 5.9%. According to the RBA statement, a pause this month is appropriate for the economy because further tightening will increase the likelihood that the economy will experience a recession.

The RBA again decided against tightening monetary policy, leaving the cash rate at 4.10%, causing an initial spike in the Australian Dollar before it began to decline. The news caused the S&P/ASX 200 to increase. Traders and commentators were divided on the likely outcome going into today’s decision. A Bloomberg survey of economists found that 18 were in favour of a rise and 12 were looking for no change, while the futures interest rate market had priced in a less than 20% probability of a 25 basis point increase. For the remainder of this tightening cycle, the market has now assigned a probability of about 50% that a 25 basis point increase will occur. Governor Lowe stated in the statement that was published with the report that “some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will depend on the data and the evolving assessment of risks. They also mentioned that while Australian inflation is declining, it is still too high at 6%. The headline CPI for the three months ending in June was 0.8%, which was less than the 1.0% forecast and 1.4% prior. To the end of June, the trimmed-mean CPI, the RBA’s preferred measure, had decreased to 5.9% from the previous month’s 6.6% and the estimated 6.0%.The trimmed mean quarter-to-quarter CPI reading of 1.0% fell short of the forecasted 1.1% and Q1 reading of 1.2%.

The choice was made today after Michelle Bullock’s appointment as the new RBA Governor was made public just over two weeks ago. Mid-September will see her start in her new position. Since April 2022, Ms Bullock has served as the bank’s deputy governor. She has worked for it since 1985. She is known for being a prominent economist in her own right. The majority of people see the appointment as a smooth leadership transition occurring at a crucial time for RBA monetary policy. Australian building approvals data for June decreased by -7.7% month-over-month earlier today, which was less disastrous than the -8.0% expected and -8.1% prior. 3.5% is close to multi-generational lows for the unemployment rate right now. The accompanying statement made mention of the tight labour market, and according to the bank, for the CPI to once again fall below 3%, the unemployment rate must increase to around 4.5%. The bank has stated that they will be able to assess the effects of the 400 basis point increase in borrowing costs since May of last year based on the incoming data. The volatility surrounding economic data could be higher than it has been recently for Australian financial markets.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

In June, New Zealand’s building permits increased 3.5% month over month, compared to a decline of 2.23% in May. The ANZ Activity Outlook shows a 0.80% increase over the predicted 0.90% decline. From -18 in June, ANZ business confidence dropped to -13.1 in July. NZD Dollar declines after positive data readings.

In the early Asian session, the NZDUSD pair trades favourably and extends its gain above the 0.6200 level. The pair is currently up 0.02% on the day as it trades near 0.6210. Market participants are waiting for fresh momentum from the New Zealand employment data on Wednesday. Following last week’s gains against significant rivals, the US Dollar Index DXY, a gauge of the value of the US dollar against a basket of six major currencies, consolidates near 101.85. On Monday, the US released unimpressive economic data. The Dallas Manufacturing Index edged up to -20 in July from -23.2 in June, while the US Chicago Purchasing Managers Index PMI came in at 42.8 from 41.5 in June, versus 43 expected. Additionally, last week’s annual US inflation data revealed that the rate of growth was the slowest in more than two years. The Personal Consumption Expenditures PCE Price Index decreased from 3.8% in May to 3% in June, according to the US Bureau of Economic Analysis, falling short of the market expectation of 3.1%. The Core PCE Price Index, the Federal Reserve’s preferred inflation indicator, came in at 4.1% annually, below market expectations of 4.2% and down from 4.6% in May. The Federal Reserve Fed may be getting closer to the end of its cycle of rate hikes as a result of the softer data, which shows that pricing pressures are easing. This could then limit the US Dollar’s upside potential and support the NZDUSD currency pair.

On the other hand, Building Permits increased 3.5% MoM in June after declining 2.23% in May, according to data released on Tuesday by Statistics New Zealand. This week’s earlier data from the National Bank of New Zealand revealed that the 0.8% increase in the July New Zealand ANZ Activity Outlook was higher than the 0.9% decline that was predicted. ANZ Business Confidence, meanwhile, declined from -18 in June to -13.1 in July. On Wednesday, New Zealand will publish data on employment. JOLTS Job Openings data will be released by the US Bureau of Labour Statistics on Tuesday, followed by ADP private sector employment data on Wednesday, and Nonfarm Payrolls data on Friday. It is anticipated that the economy has generated 180,000 new jobs. These occurrences may have a significant effect on the US Dollar’s dynamics and provide the NZDUSD pair with a clear trend.

Crude Oil Analysis

Crude Oil price is moving in the Box pattern and the market has reached the resistance area of the pattern.

Saudi Arabia cuts its daily oil production by 840000 barrels. According to a Reuters survey, OPEC+ output decreased from June to July by 840000 barrels per day, or 27.34 million bpd. However, the output from Iraq and Angola makes up for this decline.

According to a Reuters survey, OPEC’s (Organisation of the Petroleum Exporting Countries) crude oil output decreased by 840,000 barrels per day (bpd) from June to July to 27.34 million bpd. According to reports, Angola and Nigeria failed to meet the agreed-upon oil output goals during that time, and Saudi Arabia cut its production by 860,000 as part of a voluntary output reduction. However, the decline in the organization’s overall output was constrained by increases in Angola and Iraq’s output.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/