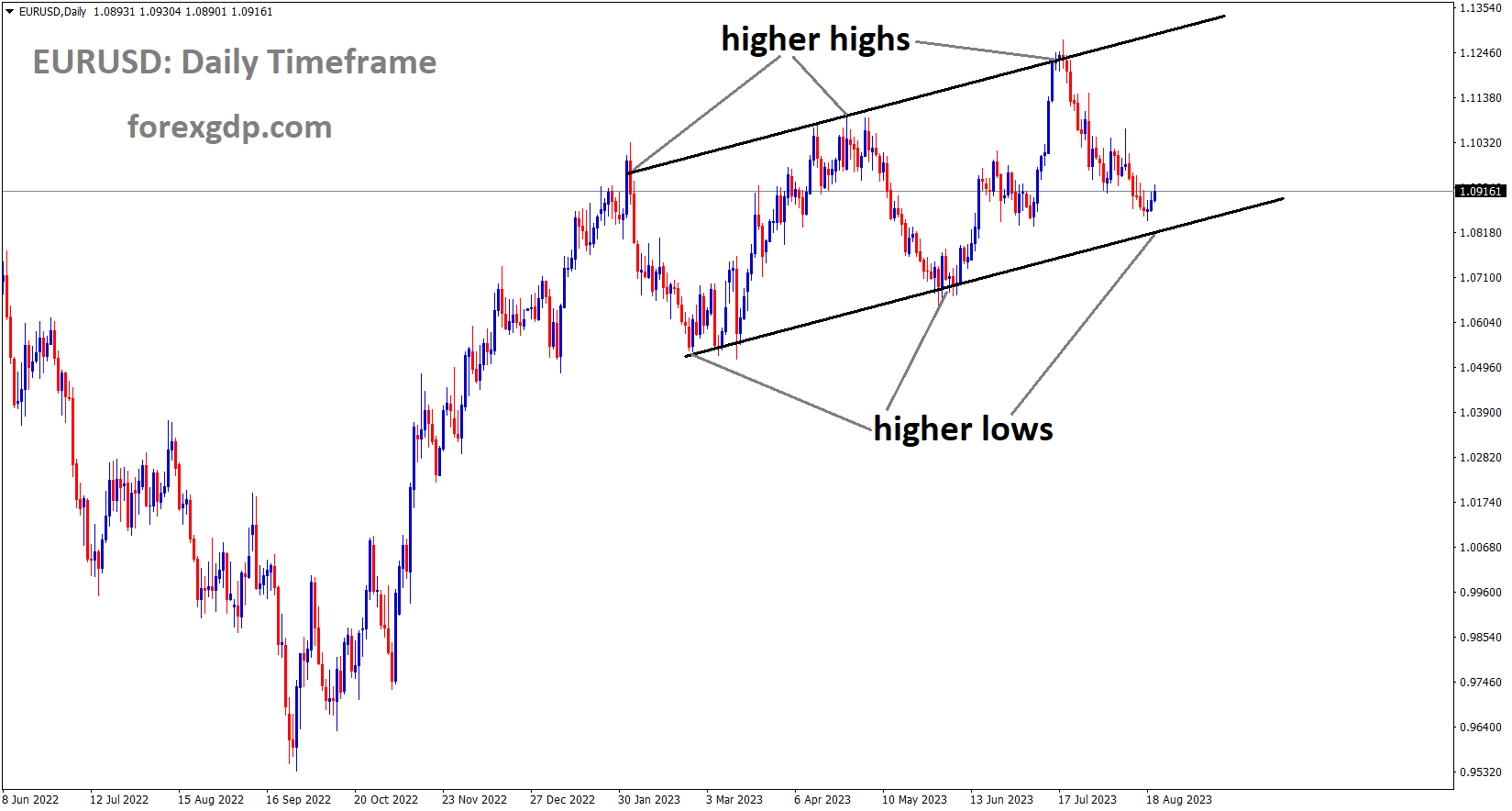

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

This week’s Jackson Hole Symposium is quickly approaching, and FED Powell likes to assess the hike speech using the data-dependent method. In the US, industrial production, retail sales, and building permits have all increased recently.

The US dollar’s recent surge appears stale in comparison to some of its competitors ahead of this Thursday’s Jackson Hole Economic Symposium. It is scheduled for Friday for US Federal Reserve Chair Jerome Powell to address the three-day gathering of central bankers. He might offer a revised economic analysis. Solid housing starts, above-expected retail sales, and industrial production increase the likelihood that inflation increased slightly in July, indicating the need for further tightening. Powell might, however, restate a data-dependent strategy rather than making a firm commitment. Given that speculative USD positioning is currently slightly long due to recent shorts, a fair analysis might offer a justification for unwinding some of those longs.

XAUUSD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel

Because the US has solid job fundamentals and a low inflation tone, the gold markets are sluggish. This week is the FED’s Jackson Hole Symposium meeting; more rate hikes are anticipated.

The price of gold holds steady at about the lowest point in the last five months, with bids recently rising to about $1,895 in the early hours of Tuesday’s Asian session. The US Dollar’s decline, the news out of China, and the market’s positioning ahead of this week’s speeches by leading central bankers at the Jackson Hole Symposium all help the XAU/USD pair. However, the recent bearish consolidation in the metal ignores the market’s mixed sentiment and the multi-year high US Treasury bond yields, casting doubt on the recovery of the gold price. It should be mentioned that the most recent confirmation of a falling wedge also benefits bullion buyers who purchase intraday. After restraining to retest the five-month low reached last week, the price of gold is now rising. The US Dollar’s weak performance in front of this week’s preliminary readings of the August month PMIs and July durable goods orders, as well as the central bankers’ speeches at the annual Jackson Hole Symposium event on August 24 and 26, may be the cause.

Furthermore, the Federal Reserve (Fed) is showing signs of weakness despite the majority of positive US data from the previous week, though some of the country’s best banks seem unable to support Fed Chair Jerome Powell’s hawkish move at Jackson Hole. Nevertheless, Goldman Sachs anticipates that Fed Chair Powell will sound defensive at the annual gathering of central bankers, while the Bank of America (BofA) anticipates that Powell will resist calls for a rate cut. The US Dollar Index (DXY) printed a fifth weekly run-up last week thanks to hawkish Fed Minutes combined with positive activity and wage growth data. In addition, it raised doubts about the prior policy pivot and increased market trepidation prior to this week’s speeches by central bankers at the Kansas Fed’s annual gathering. Firmer prints of US Treasury bond yields, in addition to the US dollar, support the hawkish stance regarding the Fed and pose a challenge to gold buyers. Nevertheless, the yield on US 10-year Treasury bonds increased to its highest point since 2007—roughly 4.354%—before closing Monday’s trading session close to 4.34%. Many of China’s attempts to regain the trust of gold buyers proved unpopular, which presented difficulties for the gold buyers themselves.

XAGUSD Analysis

XAGUSD Silver price is moving in the Ascending channel and the market has reached the higher high area of the channel

The one-year Loan Prime Rate (LPR) was cut by the People’s Bank of China (PBOC) on Monday from 3.55% to 3.45%, which was below expectations at 3.40%. Nonetheless, the five-year LPRs were maintained at 4.20% by the Chinese central bank. In a similar vein, Reuters was informed by Chinese state media Xinhua that the government intended to subsidise pesticides and fertilisers in the country’s north. Moreover, the weekend news from China indicates that the country’s policymakers intend to boost the amount of liquidity in the second-biggest economy in the world. China’s real GDP growth estimate for 2023 was lowered by UBS late on Monday from 5.2% to 4.8%, which forced the Dragon Nation to take further action to protect the economy and stabilise the gold price. It is important to remember that the news of the country’s leading real estate firm and a shadow trust bank having trouble meeting their bond obligations initially caused the XAU/USD to plunge due to worries about the Chinese debt markets. On the other hand, China is pushing for competition with the Group of Seven (G7) countries, according to a Financial Times (FT) story published over the weekend. China was present at the BRICS meeting, which featured speeches from representatives of Brazil, Russia, India, China, and South Africa. Furthermore, the recent strain between China and Taiwan exacerbates geopolitical concerns, but it does not garner much notice due to the cautious attitude preceding this week’s important data and events. Although the geopolitical unrest surrounding China puts buyers of gold to the test, the metal’s historical status as a safe haven may allow the XAU/USD to heal from its losses. The Gold Price is able to show a bearish consolidation overall due to the mixed markets prior to this week’s important data and events. But the main focus will be on Fed Chair Jerome Powell’s speech at the Jackson Hole Symposium on Friday. If Powell is able to support the hawks, there could be more decline in the XAU/USD.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

China supports the Swiss Franc against its rivals because it lacks a stimulus plan for the country’s economic recovery. This week’s Swiss Trade data determined the next course of action.

The USDCHF pair weakens and stays below the 0.8800 level during Tuesday’s early Asian trading session. The US Dollar Index DXY, which compares the value of the US dollar to six other major currencies, is struggling to rise and is currently trading at 103.32. The increase in US Treasury bond yields, which indicates that market participants believe the Federal Reserve Fed will extend the tightening cycle, supports the current cautious outlook. The yield on US 10-year Treasury bonds rises to 4.342%, nearly to its peak in 2007. Investors increase their bets on the Federal Reserve Fed raising rates further in spite of the strong labour and weaker inflation data. The remarks made by Federal Reserve Fed Chairman Jerome Powell on Friday will serve as a roadmap for investors and may shed light on the state of the economy. A more aggressive stance could strengthen the US dollar USD and support the USDCHF exchange rate.

Conversely, the Swiss franc gains from risk aversion in the face of concerns about a worsening real estate market, slowing consumer spending, and declining credit expansion in China. The People’s Bank of China PBoC cut its one-year Loan Prime Rate LPR on Monday, although the drop was not as drastic as expected. The Chinese central bank made the decision to keep the five-year Loan Prime Rate LPR at 4.2% while reducing the one-year LPR by 10 basis points bps to 3.45% from 3.55%. China’s economic recovery has stalled, placing pressure on policymakers to unveil additional plans for fiscal stimulus. The absence of stimulus plans may strengthen the CHF relative to its competitors. Traders are anticipating the Swiss Trade data, which is expected later on Tuesday. Later this week, the S&P Global PMIs, Initial Jobless Claims, US Existing Home Sales, and Durable Good Orders will all be released. The Fed Chair Jerome Powell’s speech on Friday is going to be the main event.

USDCAD Analysis

USDCAD is moving in the Box pattern and the market has fallen from the resistance area of the pattern

The Canadian dollar continues to weaken in the market as the country’s inflation data for this month was less than expected. This month’s meeting is anticipated to see another 25 basis point rate hike from the Bank of Canada, which occurred in July.

The USDCAD pair stabilises at 1.3530, maintaining its upward trajectory for a fifth week running. Rising US Treasury yields and positive US economic data provide support for the US dollar USD. Before putting new bets on the USDCAD pair, market participants may become cautious and look for additional information about the direction of the potential US Federal Reserve’s Fed monetary policy. The Bank of Canada BoC raised interest rates by 25 basis points bps to 5% in July as a result of strong labour market conditions and strong consumer spending. In order to address the ongoing inflationary pressures, this action was taken. Additionally, the central bank updated its forecasts, estimating that it will take longer than anticipated for inflation to return to target levels. Investors are bracing themselves for the possibility of an additional 25 basis point hike in interest rates at the September policy meeting. However, the Canadian dollar CAD continued to decline last week despite Canada’s lower-than-expected inflation figures.

Around 103.30, the US Dollar Index DXY, which measures the strength of the USD relative to a basket of six important currencies, is trading marginally lower. Investors may become more cautious and seek to learn more from Fed Chair Jerome Powell’s upcoming speech at the Jackson Hole Symposium regarding the state of the economy and inflation outlook. Regarding economic data, market players will be keeping a close eye on Canada’s retail sales, the preliminary S&P Global PMI surveys for August, and data on home sales. These datasets might provide a clearer picture of the circumstances, assisting investors in determining how both economies might respond.

EURJPY Analysis

EURJPY is moving in the Box pattern and the market has fallen from the resistance area of the pattern

Rate hike conflicts are evident among ECB members, and the ECB’s future meetings are less likely to see tightening measures. The July PPI data for Germany fell to 1.1%, which is bad news for the euro.

The European Central Bank (ECB) and its Council members’ differences over whether to keep up the tightening process after the summer break have contributed to the Euro’s recent deterioration.

The finance minister of Japan, Shunichi Suzuki, calmed FX intervention from the BoJ by stating that the FX markets are moving in an undesirable way. Therefore, based on JP Morgan’s analysis, 150 is the expected range for Spark FX Intervention.

Condemning China’s recent “dangerous and aggressive behaviour,” US President Joe Biden welcomed leaders from South Korea and Japan to Camp David. Taiwan has reported that 71 Chinese planes have crossed the Taiwan Straight median line during China’s current military drills around the island nation, coinciding with the meeting. Between the two sides, the line acts as an unofficial barrier. As for other developments, since Japanese Finance Minister Shunichi Suzuki declared that unfavourable FX volatility is more important than currency level, the discourse surrounding Japanese intervention has subsided.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel

The Bank of England anticipated raising interest rates at its September meeting in response to a slowdown in job growth and slower wage growth. Lowered petrol prices in the UK contributed to a decrease in inflation.

Even though Bank of England (BoE) policymakers are anticipated to raise interest rates even further at their September monetary policy meeting, the Pound Sterling (GBP) is unable to sustain its recovery. The labour market’s hiring slowdown was countered by robust wage growth in July, while the price front saw a persistently high core inflation rate offset a softer headline Consumer Price Index (CPI) due to lower petrol prices. Retail sales in the UK fell sharply as the wet weather decimated store sales. Nonetheless, demand at online retailers surged with the help of promotions, indicating that retail demand is largely steady. In order to get more information about September’s monetary policy meeting, investors will be concentrating on the preliminary PMI data for August this week. The pound sterling is trading sluggishly at 1.2750 while investors are waiting for new economic data to provide more direction. Because of the inconsistent readings from July’s economic indicators, Bank of England policymakers appear perplexed about September’s monetary policy. In July, the pace of hiring slowed but wage growth remained robust. Lower petrol prices caused the headline CPI to decline, but core inflation remained high.

The rainy weather in July caused households to stay indoors and place orders for necessities from online retailers, which resulted in a sharp decline in UK retail sales. According to data from the British Office for National Statistics (ONS), bad weather and more sales encouraged people to shop online, which increased the percentage of online retail sales to 27.4% in July from 26% in June. Because of inflationary pressures, the gap between the volume and value of retail sales remained large. The UK’s July monthly retail sales fell 1.2%, missing already bleak projections of a 0.5% contraction. Retail sales increased by 0.6% in June. Retail sales decreased 3.2% annually, which was greater than the 2.1% decrease that was anticipated and the 1.6% annual decline that was recorded in June. The real estate industry in the United Kingdom is still suffering from rising interest rates. As rising borrowing costs make it harder for buyers to invest in a home, sellers of real estate saw a sharp decline in prices demanded. According to a Reuters poll, the BoE will continue its tightening cycle by raising interest rates to 5.75%. There are still three monetary policy meetings this year, and the BoE has already raised interest rates to 5.25%. Investor attention will be focused this week on the preliminary August S&P Global/CIPS Manufacturing and Services PMI data.

GBPCHF Analysis

GBPCHF is moving in the box pattern and the market has reached the resistance area of the pattern

The Manufacturing PMI is predicted to decline from 45.3 in July to 45.0 in August. A reading of less than 50.0 is thought to indicate a decline in manufacturing activity. Compared to the previous release of 51.5, the Services PMI is likewise seen to be lower, at 50.8. After five weeks of gains, the US Dollar Index (DXY) stayed sideways on Monday, hovering around 103.50. A strong move in the US dollar is probably in store ahead of the Jackson Hole Economic Symposium. At the Jackson Hole meeting on Friday, Federal Reserve (Fed) Chair Jerome Powell will provide the economic outlook and the interest rate guidance. The “last mile” of inflation will be difficult for Fed policymakers to crack due to tight labour market conditions and robust consumer spending. Less than anticipated unemployment claims were reported by the US Department of Labour. The number of people applying for unemployment benefits for the first time fell to 239K from the previous release of 250K for the week ending August 11 and the anticipated 240K. The minutes of the Federal Open Market Committee (FOMC), which were made public last week, made it very evident that the inflationary environment is still unstable and that any future policy decisions will depend on the data that is received. Awaiting August economic data, investors will be watching for September’s monetary policy guidance.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

China recently raised the lending rate for a year by 10 basis points, which helped the Australian dollar rise from its lows. Australian PMI data is eagerly awaited this week for additional movement ahead of the S&P Global PMI.

For a second day in a row, the AUDUSD pair is rising. During Tuesday’s Asian session, the pair moves up to the 0.6420 mark. Following a similar move by Moody’s, S&P Global downgraded and revised its outlook for multiple US banks on Monday, which may result in some follow-through selling of the Greenback. AUDUSD has increased as a result of the US dollar’s decline. S&P Global downgraded several US banks on Monday, a sign that the financing and liquidity of numerous US institutions are being strained by the quick rise in interest rates. Market players, however, are stepping up their wagers on more rate hikes by the Federal Reserve Fed, pushing the yield on US 10-year Treasury bonds to 4.366%, the highest level since 2007.

Conversely, the Loan Prime Rate LPR cut by the People’s Bank of China PBoC for a year was less drastic than expected. The Chinese central bank made the decision to keep the five-year Loan Prime Rate LPR at 4.2% while reducing the one-year LPR by 10 basis points bps to 3.45% from 3.55%. Investors will be watching the news about China’s economic problems because it could have an effect on the Australian dollar, which is a good indicator of China’s economic future. Ahead of them, investors are awaiting the S&P Global PMI, which is expected on Wednesday from both the US and Australia. The United States Existing Home Sales, Initial Jobless Claims, and Durable Good Orders are scheduled to be released later this week. This week, attention will be focused on Fed Chair Jerome Powell’s speech at the Jackson Hole Symposium on Friday. Using the data as a guide, traders will look for opportunities near the AUDUSD pair.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

In 2024, there is a 40% chance that the RBNZ will hike rates again before keeping them at 5.50%. In the coming months, mortgage rates, household spending, and lending will all be impacted.

NZDUSD holds steady at 0.5930 in the early hours of Tuesday’s Asian trading session, maintaining the gains from the previous trading day. Because of the yields on US government bonds, there may be downward pressure on the pair. The yield on the 10-year Treasury note is at its highest level since 2007, which might help the US dollar gain ground. In a note, Kiwibank’s analysts expressed that the Official Cash Rate OCR track was more aggressive than anticipated. In the coming months, the RBNZ hopes to make sure that the recent tightening measures have a big effect on households. The deliberate suppression of any thoughts about lowering interest rates was done so as to preserve high wholesale rates and high mortgage and other lending rates.

The Reserve Bank of New Zealand RBNZ also maintained its projection for the official cash rate OCR to remain at 5.5%, according to the monetary policy review MPR. Additionally, the MPR showed a 40% chance of a further 25 basis point bps increase in 2024. This possible development might have an impact on the NZDUSD exchange rate. The US Dollar Index DXY, which compares the value of the US dollar to a basket of other currencies, is trading at 103.30. Expectations that the Federal Reserve Fed will maintain its hawkish stance in light of positive US macroeconomic data may provide support for the US Dollar USD. The US Existing Home Sales Change MoM, which is scheduled for later in the North American session, will be closely monitored by market participants. The focus will also be on Fed Chair Jerome Powell’s speech at the Jackson Hole later this week in order to gain new perspectives on the state of inflation and the US economy as a whole.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/