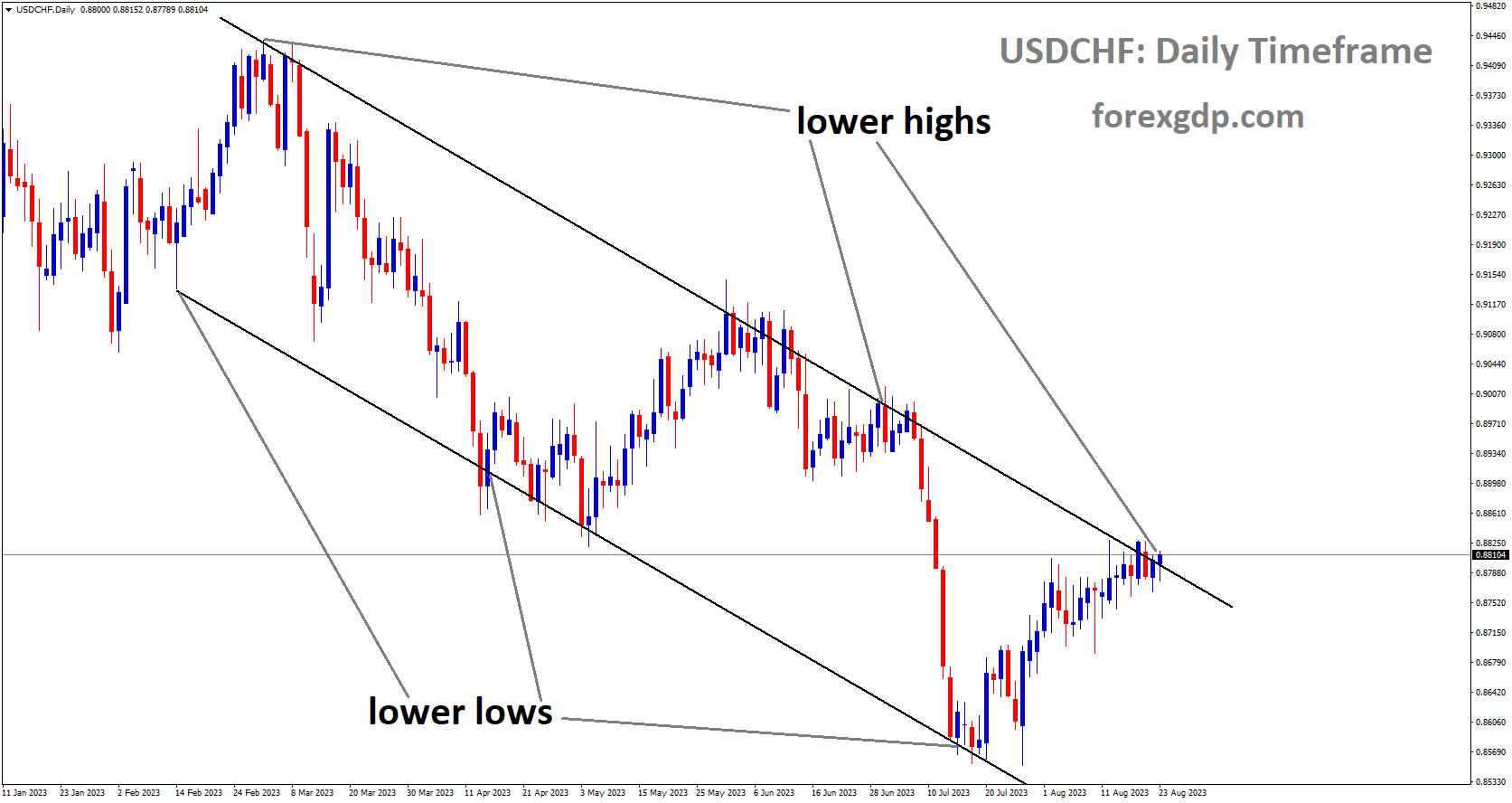

USDCHF Analysis

USDCHF is moving in Descending channel and market has reached lower high area of the channel

Tuesday’s report from the Swiss Federal Customs Administration showed that the nation’s trade balance fell to 3,129 million, compared to the market’s estimated 4,300 million. In July, however, exports decreased by 16.7%. Over that same time frame, imports decreased by 12.5%. The poorer data caused the Swiss franc to lose value relative to its competitors. Additionally, according to a statement released by the US Commerce Department late on Tuesday, US Commerce Secretary Gina Raimondo met with Chinese ambassador Xie Feng and had a fruitful conversation before leaving for China, as reported by Reuters. Market players will monitor the potential for cooperation between the two nations. The USD/CHF pair is hampered by the renewed tension between the US and China, but it may be advantageous to the traditional safe-haven nation of Switzerland.

When Switzerland releases no economic data that could move the market, the USD/CHF pair is left to the whims of USD price dynamics. It is later in the day that market participants await the US S&P Global PMI data. The annual Jackson Hole symposium on Thursday and Fed Chair Powell’s speech on Friday are sure to be the highlights of the week. The happenings might provide cues for additional monetary policy. Investors now anticipate that the Fed will hike interest rates by 25 basis points (bps) in November and pause rates in September.

XAUUSD Analysis

XAUUSD is moving in Ascending channel and market has reached higher high area of the channel

Despite lacking upside momentum ahead of the elite statistics, the gold price XAUUSD maintains its lead for the fourth day in a row. Nevertheless, the recent surge in the XAUUSD exchange rate may be connected to the US Dollar’s decline in the face of lower Treasury bond yields and somewhat upbeat market sentiment. Additionally, the gold buyers benefit from expectations of better US-China relations as well as conflicting worries about the dedollarization of the BRICS Summit, which is being held in South Africa to promote diplomatic dialogue between Brazil, Russia, India, China, and South Africa. The market’s heavy bets, as indicated by interest rate futures, that the Fed will not raise rates in September and that Fed Chair Jerome Powell’s speech at Friday’s Jackson Hole Symposium will not be overly hawkish could be on the same line. However, it is important to note that the Federal Reserve policymakers’ reluctance to embrace the rate-cut bias and the recently stronger US data appear to be protecting the XAUUSD rebound while markets await the preliminary readings of the August month Purchasing Managers Indexes PMIs for major economies.

USDCAD Analysis

USDCAD has broken Descending channel in upside

A slow weekly move is being shown by USDCAD as it remains lower near 1.3540 ahead of Wednesday’s European session. The Loonie pair is holding onto slight losses as markets wait for superior data from the US and Canada. This is despite a weaker US dollar and recent improvements in WTI crude oil, Canada’s main export. That being said, the WTI crude oil breaks a two-day losing streak by rising 0.20% intraday to $79.75 by press time, while the US Dollar Index (DXY) retreats from the 10-week high marked the previous day to at most 103.50. It is important to note that the cautious optimism in the market works in tandem with a decline in the yield on US Treasury bonds to encourage buyers of greenbacks and support the recovery in oil prices. The headlines indicating a possible improvement in US-China ties because of US Commerce Secretary Gina Raimondo’s visit to Beijing next week are among the main factors contributing to the somewhat upbeat mood. In a similar vein, early-week reports indicate that the US plans to remove 27 Chinese entities from its Unverified List, thereby lifting sanctions against those entities and raising the prospect of improved diplomatic relations.

Moreover, the DXY bulls are also encouraged by mixed US data and Fed discussions, as market players do not anticipate Fed Chair Jerome Powell’s hawkish presence at this week’s annual Jackson Hole event. Nevertheless, the US showed a tiny improvement in the Richmond Fed Manufacturing Index for August and the US Existing Home Sales for July, which should pique the interest of USDCAD sellers. Thomas Barkin, the president of the Federal Reserve Bank of Richmond, made some hawkish remarks, though, which put a floor under the two. In light of this, the yield on US 10-year Treasury bonds maintains its decline from the peak reached in late 2007 to 4.31% from the previous day, while S&P 500 Futures gain 0.25% intraday to reclaim the 4,410 level following a one-week high the day before. Ahead of the preliminary readings of the August month Purchasing Managers Indexes (PMIs) and Existing Home Sales for the US, traders of the USDCAD pair may be directed by the Canadian Retail Sales for June, which are predicted to ease on a month-over-month basis but are likely flashing improving the positive Core details.

USD Index Analysis

USD Index is moving in Ascending channel and market has reached higher high area of the channel

Tracked by the USD Index (DXY), the greenback continues its march north, hitting new two-month highs around 103.70. The index builds on its recovery from Tuesday and continues its six-week winning run, albeit with some slowdown in US yields across the curve this time. Ahead of the important Jackson Hole Symposium and Chairman Powell’s speech, which are both slated for later this week, the bid bias seems to be unaffected in the interim. Weekly MBA-measured mortgage applications, advanced Manufacturing and Services PMIs, and new home sales are all due later in the NA session in the US data space. The dollar seems to be seeing strong buying interest, which pushes the index to break through the 103.80 zone for the first time since early June.

Meanwhile, the US economy’s strength continues to support the dollar, which appears to have rekindled the Federal Reserve’s tighter-for-longer policy narrative. Moreover, the notion that the dollar might encounter challenges due to the Fed’s data-dependent approach, given the ongoing persistent deflation and cooling of the labour market, seems to be waning.

EURUSD Analysis

EURUSD is moving in Ascending channel and market has reached higher low area of the channel

Even though the euro attempted to move higher at the start of the week in an attempt to maintain the 1.09 level, The catalyst for yesterday’s increase in the US currency was once again the ongoing turbulence in global stock markets and the high prices of US government debt securities. The overall state of the market shows little change from the days prior, as the overall situation appears to be burdening the Euro, limiting its capacity to respond and make meaningful corrections.

There are a lot of significant announcements from fundamental economic news on the agenda today, including indicators of how the manufacturing and services sectors are doing in Europe and the US. These announcements carry significant weight and could cause significant market volatility. Remember that the presidents of the two major central banks will make significant remarks towards the end of the week, and after a few days off, they might reshuffle the deck. Regarding ideas for the future regarding the key interest rate level

EURJPY Analysis

EURJPY is moving in Ascending channel and market has reached higher low area of the channel

The EURJPY cross is still under strong selling pressure for the second straight day on Wednesday, continuing its overnight retracement slide from the mid-159.00s, or its highest level since September 2008. The downward trend accelerates in the early European session, pushing spot prices to a two-week low in the final hour, centred around 157.25. After a preliminary report revealed that German business activity shrank in August at its fastest rate in over three years, the common currency began to decline overall. As a matter of fact, the recession fears were stoked when the HCOB Flash German Composite PMI missed forecasts and dropped to 44.7, the lowest level since May 2020. In addition, the manufacturing PMI stayed well below contraction territory and the services sector’s business activity shrank for the first time in eight months.

The most populous economy in the Euro Zone is showing signs of deteriorating economic conditions, which feeds rumours that the European Central Bank (ECB) will end its nine-year run of rate hikes in September. In fact, compared to about a 60% chance priced in ahead of the data, money market futures now price just a 40% chance of a 25 bps lift-off from the ECB in September. Consequently, the Euro is perceived to be under pressure, leading to a decline in the EURJPY cross. In contrast, there are some haven flows drawn to the Japanese Yen (JPY) as concerns about a deeper global economic downturn grow. Aside from this, the JPY is supported by fears of intervention, which also add to the negative sentiment surrounding the EURJPY cross. However, the Bank of Japan’s (BoJ) dovish stance may limit any significant gains for the JPY, so it is advisable to exercise caution before concluding that the cross has topped out in the near future.

EURCHF Analysis

EURCHF is moving in Descending channel and market has reached lower low area of the channel

The latest data from HCOB’s latest purchasing managers index survey showed on Wednesday that while the contraction of the manufacturing sector in the Eurozone slowed down, there was a downturn in the services sector in August.In August, the Eurozone Manufacturing Purchasing Managers Index (PMI) increased to 43.7 from 42.7 in July, above the 42.7 predicted by the market. The index peaked after three months.

The Services PMI for the bloc fell to 48.3 in August from 50.9 in July, a 30-month low, and significantly below the 50.5 forecast. In August, the HCOB Eurozone PMI Composite fell to 47.0 from 48.5 in July’s booked reading and 48.5 expected. It was the lowest point the index had been in 33 months.

GBPUSD Analysis

GBPUSD has broken Ascending channel in downside

On Wednesday, the pound sterling GBP is unable to find direction while investors wait for the preliminary August S&P Global PMI data. The GBP/USD pair is trading in a dull manner, but after the release of the PMI data—which will show how the Bank of England’s BoE higher interest rates are affecting British economic activity—volatile action is anticipated. BoE policymakers issued a warning regarding growing risks of corporate default brought on by a low debt-service coverage ratio. Small and mid-sized businesses in the UK are finding it difficult to pay their interest due to growing borrowing costs and a bleak economic outlook. In the meantime, BoE policymakers find some solace in the fact that pay hikes decreased in the July quarter following six straight strong quarters. The pound sterling makes a slow upward move after finding support close to 1.2720 in front of the preliminary August S&P Global PMI data. Estimates indicate that the Manufacturing PMI will decrease from July’s reading of 45.3 to 45.0. A value of less than 50.0 indicates a downturn in the economy. Additionally, compared to the previous reading of 51.3, the Services PMI is predicted to remain lower at 50.8.

The vicious cycle of rate tightening by the Bank of England has been wreaking havoc on UK economic activity. According to a report by the British Confederation of British Industry CBI, the net balance of output decreased to -19 from +3 in July for the three months ending in August. Since September 2020, this reading has been the lowest. The disparity between the factories projecting a decline and the parts reporting increasing output is shown by the net balance. Amidst rising interest rates, the BoE issued a warning about substantial upside risks to corporate defaults. According to a BoE survey, the percentage of non-financial UK companies with a poor debt-service coverage ratio will increase from 45% at the end of the previous year to 50% by the end of the current year. Growing corporate default risks will push up delinquency costs for commercial banks in the UK, lowering the quality of their assets. The British Chambers of Commerce stated that increased borrowing costs are placing a great deal of pressure on many smaller businesses, who are unable to absorb the increases following three years of economic shocks, regarding rising risks of corporate defaults. The likelihood of a recession in the UK economy will increase if more businesses face increasing stress related to servicing their corporate debt. Pay awards given by employers in the United Kingdom decreased for the first time in the previous seven quarters. According to XpertHR, the median basic pay for the three months ending in July decreased from a record 6% to 5.7%.

Reductions in pay awards will relieve some of the pressure from policymakers at the Bank of England, who maintain that inflation has been sustained by robust wage growth. This weekend, there was still a lot of discussion regarding the UK’s cabinet reshuffle. According to Reuters, Prime Minister Sunak is now thinking about concentrating on replacing ministers, like former Defence Secretary Ben Wallace, who have already declared their desire to resign. As investors wait for more action from the Jackson Hole Symposium, the market is in an incredibly quiet state. The US Dollar Index DXY gains momentum to move past the 103.70 immediate resistance level. Resilient consumer spending and a tight labour market may make the residual excess inflation very hard to overcome. Thomas Barkin, the president of the Richmond Federal Reserve Fed Bank, stated on Tuesday that inflation is likely to decline if it stays high and there is no indication from demand. A more stringent monetary policy would be necessary in that setting. Fed- Barkin anticipates that things will be less severe in terms of the recession. Fed Chair Jerome Powell is anticipated to make a hawkish speech at Jackson Hole. Longer-term increases in interest rates are anticipated from the Fed. The likelihood of an interest rate increase will depend more on data.

AUDUSD Analysis

AUDUSD is moving in Descending channel and market has reached lowr high area of the channel

Despite recent struggles, AUDUSD remains strong for the fourth straight day as market participants applaud the weak US Dollar in the early hours of Wednesday morning in Europe. In light of this, the Australian dollar pair gains 0.30% during the day to reach the 0.6450 mark at press time. The market’s cautious optimism and a decline in the yield on US Treasury bonds are two of the main catalysts. It is noteworthy, nevertheless, that the AUDUSD pair’s initial upward movement is limited by the negative prints of Australia’s preliminary S&P Global PMIs for August. Notwithstanding, the headlines point to a probable strengthening of US-China relations as a result of US Commerce Secretary Gina Raimondo’s upcoming visit to Beijing. In a similar vein, early-week reports indicate that the US plans to remove 27 Chinese entities from its Unverified List, thereby lifting sanctions against those entities and raising the prospect of improved diplomatic relations.

On the other hand, as market players do not anticipate Fed Chair Jerome Powell’s hawkish appearance at this week’s annual Jackson Hole event, mixed US data and Fed talks also encourage the DXY bulls. However, the US showed a tiny improvement in the Richmond Fed Manufacturing Index for August and the US Existing Home Sales for July, which should entice those selling AUDUSD. Thomas Barkin, the president of the Federal Reserve Bank of Richmond, made some hawkish remarks, though, which put a floor under the two. The US 10-year Treasury bond yields, which reflect the mood, continue to decline from their peak since late 2007 to 4.31%, while S&P 500 Futures gain 0.25% intraday to reclaim the 4,410 level after reversing from a one-week high the day before. Additionally, the US Dollar Index (DXY) drops to at most 103.50 from the 10-week high reached the day before. Looking ahead, traders of the AUDUSD pair will be interested in the preliminary readings of the US Existing Home Sales data for July and the August month Purchasing Managers Indexes (PMIs). The annual Jackson Hole Symposium, which takes place on August 24–26, will feature speeches by prominent central bankers, and those speeches will be essential for providing direction.

NZDUSD Analysis

NZDUSD is moving in Descending channel and market has reached lower high area of the channel

The modest decline in the US dollar (USD) that followed a somewhat softer tone surrounding the yields on US Treasury bonds and against the backdrop of the recent rise to a more than two-month peak is what is driving the intraday uptick. This decline is primarily due to profit-taking. Aside from this, the New Zealand Dollar (NZD) and other antipodean currencies benefit further from expectations for further stimulus from China and indications of a deeasing of US-China trade tensions. It is important to remember that the Bureau of Industry and Security (BIS) of the US Commerce Department declared on Monday that it would be removing 27 Chinese companies from its Unverified List. China praised the action and stated that it would facilitate regular trade between the two countries. This is in advance of US Secretary of Commerce Gina Raimondo’s August 27–30 visit to China, during which she will meet with top Chinese officials and influential US businesspeople. Nevertheless, growing worries about China’s deteriorating economic situation should temper market optimism and the risk-averse Kiwi, who showed little reaction to rather weak domestic data. To be exact, the second quarter (Q2) of 2023 saw a 1% decline in retail sales, which was better than the 1.6% decline in the previous quarter and better than the 2.6% contraction predicted by Statistics New Zealand.

Moreover, the Reserve Bank of New Zealand (RBNZ) had previously signalled that rate increases were finished. Because of this and growing confidence that the Federal Reserve (Fed) will maintain higher interest rates for an extended period of time, it is wise to exercise caution before making large, aggressive bets on the NZD/USD pair. For a significant boost, market players are now anticipating the release of the US flash PMI prints. But all eyes will be fixed on the pivotal Jackson Hole Symposium, where remarks made by Fed Chair Jerome Powell will be carefully examined for hints regarding the direction of future rate hikes. This will therefore have a significant impact on the short-term USD price dynamics and aid in identifying the next leg of the NZD/USD pair’s directional move.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/