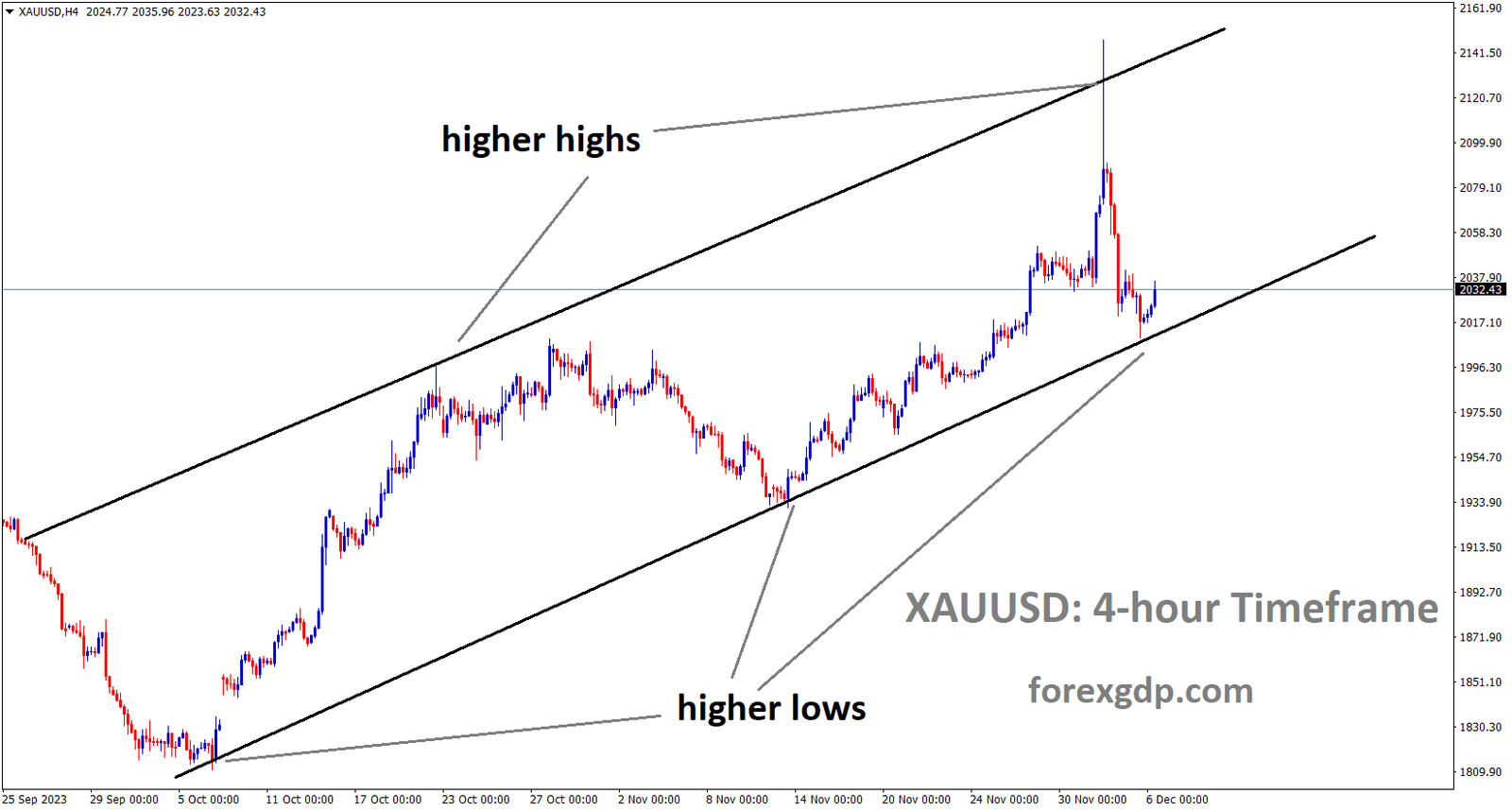

XAUUSD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher high area of the channel

US consumer confidence fell to 106.10 in August from 114.00 in July; US job openings decreased to 8.827 million from 9.165 million in July; US dollar declined against other currencies following the release of the data.

Bears on the US Dollar Index DXY take a break at the weekly low, rounding to 103.50 by press time as investors wait for additional evidence to support the recent dovish bias regarding the Federal Reserve Fed as a result of the poor US data. Nevertheless, the measure of the US dollar against the six major currencies fell the most in six weeks the day before, and it stabilised during Wednesday’s Asian session. In contrast to market expectations of 116.0, the US Conference Board’s CB Consumer Confidence Index for August fell to 106.10 on Tuesday from a downwardly revised 114.00 prior from 117.0. Nevertheless, the US JOLTS Job Openings fell to 8.827 million for July, the lowest since March 2021, compared to 9.465 million foreseen and 9.165 million fore revised from 9.582. Furthermore, the S&P/Case-Shiller Home Price Indices improved to -1.2% YoY from -1.7% previous readings and -1.3% market forecasts, while the US Housing Price Index eased to 0.3% MoM for June from 0.7% prior and 0.2%. Recall that Fed Chair Jerome Powell challenged the hawks following the dismal US statistics by emphasising in his speech the need for data to inform future decisions.

XAGUSD Analysis

XAGUSD Silver price is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern

The CME’s FedWatch Tool indicated a 16% probability of a rate hike after the data, down from a 20% prior. The US Dollar and US Treasury bond yields were also affected by the same factors that drove Wall Street benchmarks. Nevertheless, by the end of Tuesday’s North American trading session, the US 10-year Treasury bond yields had fallen to their lowest point in 13 days, while the Wall Street benchmarks increased for the third straight day. The US Dollar Index was negatively impacted not only by the depressing US statistics but also by optimistic stock market results and expectations of further stimulus from China DXY. The People’s Bank of China PBoC early rate cuts and the Dragon Nation’s reduction in mortgage rates contributed to the traders’ optimism.

On the other hand, the DXY bears are irritated by US Commerce Secretary Gina Raimondo’s complaints regarding the difficulties faced by US companies in China. In the same vein, given the current climate of rising interest rates and inflation, the International Monetary Fund IMF may be willing to exercise greater caution when allocating Special Drawing Rights SDRs in the future. Further hints that the Fed may change course in 2023 will be closely watched and could have an impact on the US Dollar Index. Nevertheless, the important things to keep an eye on today are the US ADP Employment Change, the final GDP and PCE readings for the US second quarter Q2.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

In July, Japan’s unemployment rate increased to 2.7% from the projected 2.5%. The Bank of Japan stated that it will take almost 25 years for Japan to overcome its deflation rate. Monetary policy will begin to tighten as soon as inflation stabilises in a sustainable manner, according to BoJ Governor Ueda.

The Yen pair rationalises Japan’s inflation conditions as well as the recent shift in sentiment towards the Bank of Japan (BoJ. Yen pair sellers are, nevertheless, prodded by pessimistic worries about Japan’s employment conditions and the cautious atmosphere preceding the important data and events. Nevertheless, the Jobs Applicants Ratio decreased to 1.29 for the aforementioned month compared to 1.30 predicted and previous readings, and Japan’s Unemployment Rate offered a surprise increase to 2.7% for July versus 2.5% expected and prior. More significantly, after 25 years of attempts to combat deflation, the Japanese government recently published its annual report, which indicates the turning point for the country’s inflation conditions. The hawkish bias regarding the BoJ thus intensifies.

The contradictory information released on Monday regarding Japan’s June Coincident Index and June Leading Economic Index also prompted traders of the USDJPY pair. Recall that at the Jackson Hole Symposium, Bank of Japan Governor Kazuo Ueda used Japan’s slightly below-target inflation to support the current ultra-easy monetary policy, which in turn riles pair sellers. Ahead of today’s US CB Consumer Confidence for August report, negative yields and the overall decline in the US dollar will also affect the USDJPY exchange rate. Around 4.19% pressure is still applied to US 10-year Treasury bond yields, and as of press time, the US Dollar Index (DXY had fallen to 103.85. It is noteworthy that the US two-year bond coupons fell from their highest point since 2007 the day before and were still below 5.00% at the time of publication.

In contrast, Goldman Sachs predicts that the USDJPY pair will reach a 30-year high of roughly 155.00, up from the previous prediction of 135.00, citing the US growth outlook and the BoJ’s defence of the easy-money policy. In the near future, worries regarding the Federal Reserve’s (Fed and Bank of Japan’s (BoJ monetary policies will be added to the risk catalysts that will pique the interest of USDJPY traders ahead of the US Conference Board’s (CB August Consumer Confidence Index, which is anticipated to be 116.2 instead of the previous 117.00.

According to Naoki Tamura, a board member of the Bank of Japan, the early termination of the loose monetary policy is not feasible. The negative rate will end first, once the 2% inflation target is reached sustainably.

The Bank of Japan (BoJ) board member Naoki Tamura stated on Wednesday that the end of the easy policy should not come too soon or too late. Whether to reduce the easy policy early in the following year will depend on a number of factors at the moment. If the BoJ were to break its easy policy, the options would be to end the negative rate and YCC. Monetary tightening or rate hikes would not occur even if the BoJ abandoned the negative rate because loose monetary conditions would still exist. Assessing whether Japan has achieved the BoJ’s price target in a sustainable way will require some additional time. Depending on the state of the economy at the time, the BoJ will exit its easy policy in what order and at what speed. If the goal of 2% inflation is achieved in a sustainable and stable manner, then ending the negative rate becomes an option.

Will not remark on FX movements or levels. Discuss whether the 2% inflation target can be sustained before January or March of the following year, or whether the BoJ’s July decision was not specifically directed at FX. It is crucial that FX movements take financial and economic fundamentals into account. BoJ will monitor the effects of FX movements on Japan’s economy while implementing monetary policy.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

After China’s economic slowdown and the challenging trade relationship between the US and China, the Swiss franc is stronger than the US dollar. The Swiss franc strengthened against the US dollar on the back of lower US consumer confidence data the previous day.

In the early hours of Wednesday’s European session, USDCHF holds onto slight gains around 0.8790 as it consolidates the largest daily loss since late July, marked the previous day. Notably, the Swiss Franc (CHF) pair printed its first daily gains in three days thanks to the US Dollar’s positioning for superior data and the market’s reevaluation of the prior dovish bias regarding the Federal Reserve (Fed). However, the US consumer confidence, employment, and housing data from the previous day raised concerns about the Fed’s policy change. This was especially true after Fed Chair Jerome Powell emphasised the data-dependency for future actions to support the hawkish bias. As a result, the US Dollar Index (DXY) is holding onto modest gains. The US Treasury bond yields and the Greenback were submerged by the same.

In other news, the USDCHF rally is also fueled by conflicting worries about US-China relations and uncertainty over the softer landing. China recently expressed disapproval of US Commerce Secretary Gina Raimondo’s grievances regarding the difficulties faced by US companies operating in China. The market was previously more optimistic due to rumours of early rate cuts from the People’s Bank of China (PBoC), a decrease in mortgage rates, and a probable improvement in US-China relations. It should be mentioned that the current environment of higher interest rates and inflation, along with the International Monetary Fund’s (IMF) willingness to exercise greater caution when allocating Special Drawing Rights (SDRs) in the future, appears to be revitalising demand for the US dollar.

The riskier assets are encouraged by the US S&P 500 Futures, which prints modest gains during these plays, driving up the USDCHF prices. That being said, after hitting a new weekly low the day before, the yield on US 10-year Treasury bonds fluctuated around 4.15%. In order to validate the Fed’s concerns about the policy pivot, the US ADP Employment Change, the final GDP and PCE data readings for the US second quarter (Q2), and the US GDP data will all be closely watched. The USDCHF could see more declines if the planned data supports the need to end the tight monetary policies.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Euro is rising versus the USD ahead of German inflation data. The US’s Last Day Domestic data is more favourable to the euro.

Recent data releases appear to have somewhat dented the Federal Reserve’s (Fed) tighter-for-longer stance, and they also cast doubt on expectations of a 25 basis point rate hike at the meeting on November 1. On the other hand, there is no information available about the European Central Bank’s (ECB) prospective rate decision after the summer break.

EURCHF Analysis

EURCHF is moving in the Descending channel and the market has reached the lower high area of the channel

According to data, consumer confidence in Italy slightly decreased to 106.5 for the current month, while flash inflation figures in Spain show that the CPI increased 2.6% in the year ending in August. The final Eurozone Consumer Confidence report and Germany’s advanced inflation statistics are due later in the session. Investor focus in the US will be on the release of the ADP report, which will be followed by flash figures for the goods trade balance, pending home sales, and another estimate of the Q2 GDP growth rate.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel

People suffered more from higher interest rates when purchasing homes with larger monthly payments, and the Bank of England is more likely to raise rates in the upcoming month. Inflation is declining, factory output prices have dropped, and housing prices have eased.

With the expectation that the Bank of England BoE will neutralise the Federal Reserve-BoE divergence by raising interest rates by 25 basis points bps at its September monetary policy meeting, the pound sterling GBP saw a strong recovery on Tuesday. Since the BoE’s additional policy tightening will deteriorate the outlook for the economy, the recovery move in the GBP/USD pair faded. The effects of the UK central bank’s tight monetary policy have expanded to include the housing and manufacturing sectors. As a result of growing prices, businesses are not using all of their production capacity because forward demand appears to be weak. While nuclear families have put off buying a house in order to avoid having to make larger monthly payments. The United Kingdom is still experiencing inflationary pressures in spite of low fuel and energy prices. The pound sterling recovers in spite of the growing effects of high inflationary pressures. Despite expectations that this month’s Fed-BoE policy divergence will neutralise, the value of the UK currency falls quickly. While the BoE is anticipated to hike interest rates for the fifteenth consecutive time, investors are hoping that the Fed will maintain its current range of 5.25 to 5.50%. A 25 basis point bps increase in interest rates is anticipated by investors, bringing rates to 5.50%.

Power in the Measure Because of the anticipation of a neutralised Fed-BoE policy divergence, sterling is worthless. Bulls in sterling may lose traction if the negative effects of a tight monetary policy begin to compound. Ben Broadbent, deputy governor of the Bank of England, stated that interest rates will stay higher for a longer time. In spite of low energy prices, he continued, inflation will not abate as quickly as it did initially. The historically aggressive rate-tightening cycle by the Bank of England is causing a significant slowdown in the UK’s housing sector, factory activities, and hiring momentum. As buyers delayed their plans for residential investments in order to avoid larger installment obligations, home sellers lowered their prices. In the meantime, UK businesses are still running at reduced capacity because of the poor demand forecast. A declining ability to service debt is a factor contributing to the increased risk of corporate default. Additionally, because rising interest rates have put economic prospects in jeopardy, businesses have slowed down their hiring procedures. Nonetheless, the rate of pay growth is very robust, suggesting that companies are prioritising talent retention over new hires.

To strengthen diplomatic ties with China, UK PM Rishi Sunak meets face-to-face with Chinese President XI Jinping at the G20 summit. XI Jinping hasn’t, however, officially announced his arrival. The US Dollar Index makes an effort to rebound but is still limited while investors wait for the ADP Employment Change data. It is scheduled to be released on Wednesday at 12:15 GMT. According to projections, the US labour market will add 195K new jobs in August, up from the previous 324K additions. Since Fed Chair Jerome Powell stated in his remarks at the Jackson Hole Symposium that the central bank will continue to rely on data before taking further policy action, the labour market data from August will have a greater impact. Significantly fewer new job openings were reported in July by the US Bureau of Labour Statistics. Investors anticipated 9.465 million openings, but US companies only accepted new applications for 8.827 million positions, down from June’s reading of 9.165 million. This suggests that there has been a slowdown in the hiring process. The official labour market data and the August ISM Manufacturing PMI, which will serve as the foundation for September’s monetary policy, will be the main topics of discussion later this week.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

New Zealand building permit data was 5.2%, up from the previous reading of 3.4% and the expected 0.20%. NZD Dollar declined versus counter pairs following the publication of the data.

The NZDUSD pair accepts offers to move up towards the intraday low of 0.5945 early on Wednesday morning in Europe. By doing this, the Kiwi pair illustrates the market’s cautious attitude ahead of the premium US data and provides justification for the negative New Zealand NZ housing data. July’s New Zealand Building Permits showed a noteworthy decline of 5.2% MoM against 0.2% predicted and 3.4% previous revised from 3.5%.

It is important to keep in mind that the US ADP Employment Change, the final GDP and PCE readings for the US second quarter Q2, and the NZDUSD exchange rate are scheduled to release and may influence sentiment. In light of this, the US Dollar Index DXY, which had dropped to its lowest level in six weeks the day before, is also licking its wounds at 103.60.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

Australian CPI for July was 4.9% as opposed to 5.4% in June, which was predicted to be 5.2%. Because of the end of inflation, the RBA is more likely to keep rates unchanged at its September meeting.

Following a more than anticipated slowdown in consumer price inflation last month, the Australian dollar declined, supporting the expectation that the Reserve Bank of Australia RBA will maintain interest rate stability for the foreseeable future. Australia’s CPI decreased significantly from 5.4% in June to 4.9% on-year in July, compared to an expected 5.2%. The RBA believes that the worst of inflation is likely behind us, so the easing of price pressures is encouraging. That being said, the monthly CPI data is frequently erratic and not always a reliable indicator of the quarterly CPI, which is more significant in the eyes of the Reserve Bank of Australia.

However, the RBA will probably find solace in the disinflation trend as it works to create a soft landing. Markets are pricing in a high likelihood that the Australian central bank will hold rates steady at 4.1% during its meeting next week, given the deteriorating growth outlook in China, early indications of the labour market cooling, and worsening growth prospects. Australian retail sales increased last month, indicating a slowdown in consumer demand, but the annual rate fell even more. Despite the disappointing US activity data from last week, overall the US economy looks to be beating some of its competitors, particularly China and Europe. The US dollar has increased due to the US economy’s resilience. Powell gave some additional support to the greenback last week with his mostly cautious but slightly hawkish remarks at Jackson Hole. Further depressing the AUD has been the belief that rate hikes by the RBA are finished. However, given the recent support actions taken by Chinese policymakers, the decline in US yields, and the stretched bearish sentiment, risk appetite seems to have stabilised for the time being.

AUDCAD Analysis

AUDCAD is moving in the Symmetrical triangle pattern and the market has reached the bottom area of the pattern

According to China’s embassy in the US, China is open for business with all nations and treats domestic and foreign companies equally. They are assisting US chip maker Micron with their cyber security review. US Commerce Secretary Gina Raimondo expressed support for the US companies experiencing difficulties in China.

China’s embassy in the US defended its cybersecurity review of US chipmaker Micron early on Wednesday in Asia, citing national security concerns. This was particularly true after US Commerce Secretary Gina Raimondo voiced concerns about the difficulties faced by US companies doing business in China. However, the China Embassy also dismissed rumours that it was aiming to attack specific nations or areas, as well as rumours that Beijing was pulling certain goods or technologies out of any given nation. China will only open its doors even wider to the outside world, the Chinese embassy in Washington stated, adding that China is working to further ease market access and treat foreign companies in the same manner as domestic firms.

The slowdown in China’s economy has caused the Canadian dollar to weaken in the market. The IMF has advised being more cautious in the economy and issuing special drawing rights to address the country’s inflation and interest rate problems. The USD is benefited by this action.

Despite positive prices for Canada’s primary export, WTI crude oil, which renews its weekly high around $81.40 due to expectations of further stimulus from China and increased demand as a result of unfavourable weather in the West, the Loonie pair records its first daily run-up to date. The rise in black gold is also supported by a significant draw from US inventories, according to weekly Crude Oil Stocks Change data from the American Petroleum Institute (API). The market’s optimism was supported by rumours of the People’s Bank of China (PBoC) cutting rates early, a decrease in mortgage rates, and a probable improvement in US-China relations. It is noteworthy that the International Monetary Fund (IMF) has expressed its willingness to exercise greater caution in the future when assigning Special Drawing Rights (SDRs).

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/