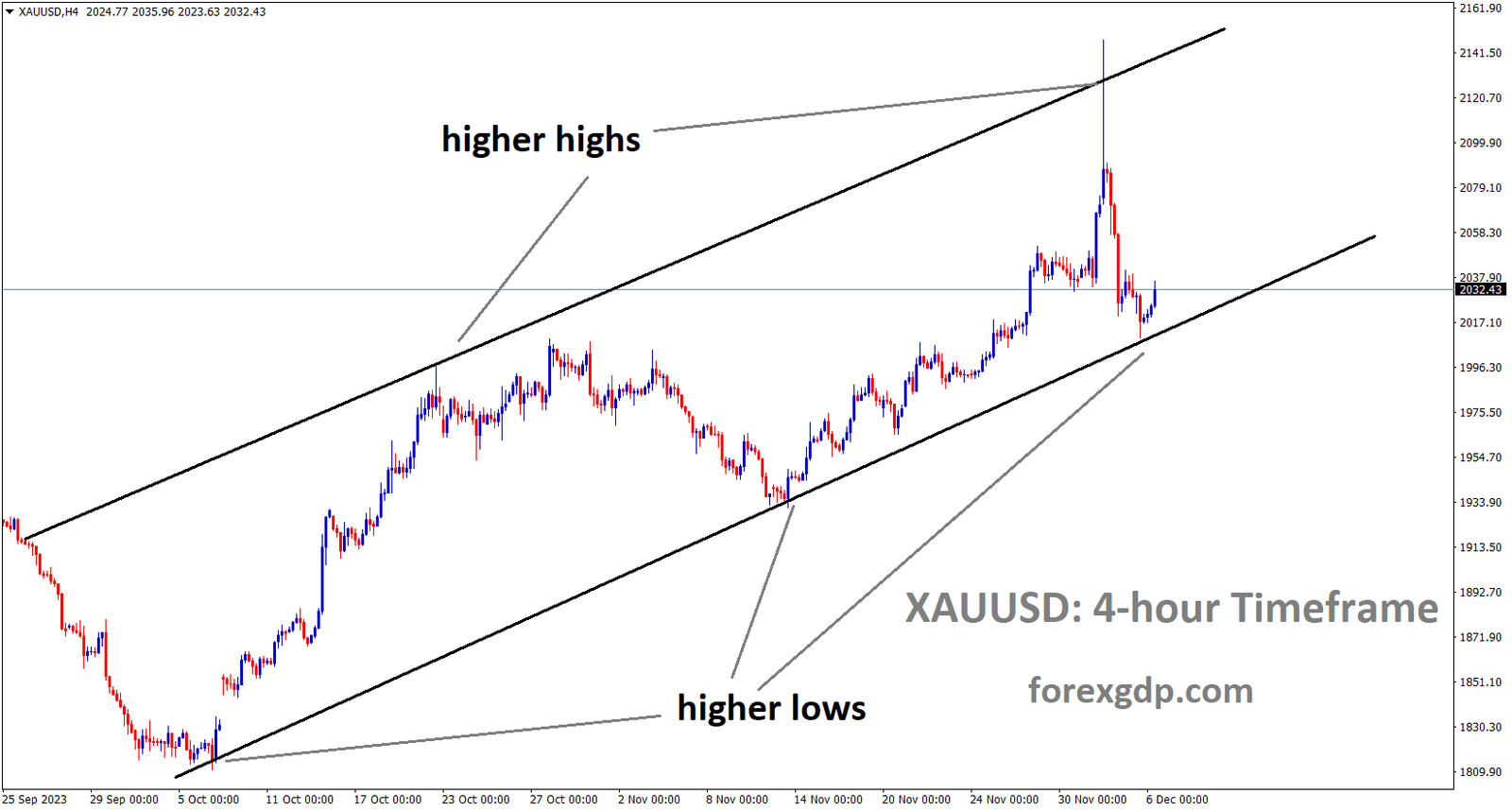

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Gold prices are undergoing further corrections against the USD in the market, with the Israel conflict experiencing a slight reduction in tension, which is contributing to corrections in commodity prices.

The attempt by GOLD to recover from the $2,020 level has been limited, with its rise halting at $2,040. This halt is attributed to the US Dollar’s resurgence, which is benefiting from a cautious market sentiment. Investors are exercising caution as they await the release of crucial US macroeconomic data scheduled for this week, with a particular focus on Friday’s Nonfarm Payrolls report. These figures are of great interest as they could confirm the conclusion of the Federal Reserve’s tightening cycle and raise expectations of rate cuts in the first quarter of 2024.

Monday’s data revealed that US Factory Orders contracted more than anticipated in October, adding to the evidence that US economic growth is slowing down in the final quarter of the year. On Tuesday, investors will closely monitor the US ISM Services PMI and the JOLTS Job Openings data. Wednesday’s ADP Employment Change and Friday’s Nonfarm Payrolls will be the highlights of the week, providing insights into the labor market’s strength and influencing the Fed’s near-term direction.

The current market sentiment is risk-averse, supporting the US Dollar and putting pressure on precious metals. Investors are reluctant to take on risky positions as they await the release of US employment data. Gold, however, remains steady above the psychological $2,000 mark, supported by soft US macroeconomic data, which fuels expectations that the Fed may initiate rate cuts in early 2024. Eurozone and UK services PMI data have indicated an increase in sector activity, alleviating concerns about a sharp economic slowdown in the coming months. The CME Group FedWatch tool suggests a 54% probability that the US central bank will reduce its benchmark rate by 25 basis points in March.

In October, US Factory Orders recorded a larger-than-expected decline of 3.6%, following a 2.3% increase in September, compared to the anticipated 2.6% drop. In China, the Caixin Services PMI accelerated to 51.5 in November from 50.4 in October, surpassing market expectations but remaining below pre-pandemic levels. The Israel-Gaza conflict and concerns about a new epidemic in China are tempering the optimism generated by the positive Caixin Services PMI data, which indicates an acceleration in business activity in November. The upcoming release of the US ISM Services PMI is anticipated to show a slight uptick to 52 in November from the previous month’s 51.8. Any deviation from this expectation could offer short-term trading opportunities. US JOLTS Job Openings are projected to have declined to 9.3 million in October from 9.55 million in the prior month, setting the stage for Wednesday’s ADP report and the highly significant NFP report scheduled for Friday.

SILVER Analysis:

XAGUSD Silver price has broken the Descending channel in upside

The US ISM Services PMI data showed a reading of 52.7, surpassing the previous reading of 51.8 and slightly exceeding the expected value of 52.0. Following the release of this data yesterday, the USD experienced a modest increase in value compared to other currencies.

In November 2023, the US ISM services PMI remained robust, surpassing expectations by registering a reading of 52.7, up from 51.8 in October. This marked the 11th consecutive month of expansion in the services sector. The growth in November was modestly driven by increased business activity and slight employment growth. Additionally, new orders remained strong, and inventories rebounded 55.4 vs. 49.5, while price pressures eased slightly 58.3 vs. 58.6. Furthermore, the backlog of orders reversed its trend 49.1 vs. 50.9, and the Supplier Deliveries Index indicated improved supplier delivery performance 49.6 vs. 47.5.

Respondents’ comments varied by company and industry, with ongoing concerns about inflation, interest rates, and geopolitical events. Rising labor costs and labor constraints continue to pose challenges for employment.

In October, the number of job openings in the United States decreased to 8.7 million. The U.S. Bureau of Labor Statistics reported that over the month, the number of hires and total separations remained relatively stable at 5.9 million and 5.6 million, respectively. This decrease in job openings was largely attributed to declines in health care and social assistance -236,000, finance and insurance -168,000, and real estate and rental and leasing, with the only increase coming from the information sector.

With another round of key data released ahead of the FOMC Meeting and the NFP report still pending for Friday, the U.S. Dollar has continued its upward trajectory due to renewed safe haven demand and reduced expectations of rate cuts. The ongoing adjustment of Fed rate cut expectations for 2024 persists, with the minor adjustment this week not being driven by any specific data releases. This aligns with the mixed comments from Fed policymakers, many of whom acknowledge progress but believe that market participants may be getting ahead of themselves regarding rate cut expectations.

While the ISM Services data may not align perfectly with the Fed’s goals, it remains a factor to consider in relation to inflation. However, any further decrease in the JOLTS job openings number may overshadow the ISM data, especially with the NFP report looming on Friday. This week’s employment data may continue to create uncertainty in expectations until Fed Chair Powell addresses the situation at the FOMC meeting.

USDCHF Analysis:

USDCHF is moving in the Descending channel and the market has rebounded from the lower low area of the channel

The Swiss CPI data came in below expectations, raising hopes that the Swiss National Bank might consider another rate hike in their upcoming meeting. Meanwhile, in November, US factory orders fell short of expectations, leading to a decline in the USD against the CHF.

The impact of the disappointing Swiss CPI reading observed on Monday continues to influence the market sentiment. This downturn is benefiting the safe-haven Swiss Franc while also acting as a restraint on the strength of the US Dollar. In the United States, the Factory Orders data released on Monday further confirmed that economic growth is decelerating in the fourth quarter of the year. Coupled with the subdued inflation figures, this is fostering expectations that the Federal Reserve has completed its rate hikes, which is exerting downward pressure on the USD. Today, the release of the US ISM Services PMI and the JOLTS job openings will provide additional insights into the US economic outlook. However, the highlight of the week remains Friday’s Nonfarm Payrolls report.

EURUSD Analysis:

EURUSD is moving in the Descending channel and the market has reached the lower low area of the channel

Isabel Schnabel, a member of the ECB Governing Council, noted that inflation in November registered at 2.4%, a cooling trend that exceeded expectations. Nevertheless, further sustainable cooling of inflation is anticipated. It is believed that the rate hikes implemented will be sufficient to bring inflation under control in the Eurozone.

ANZ Bank analysts anticipate a downward adjustment in the Dot plot program by the Fed in 2024. This projection is influenced by the easing inflationary pressures in the US and the improving labor market conditions. While a rate hike is not completely dismissed for 2024, there is a growing expectation that a rate cut may become more likely in the latter part of the year, as supported by the data.

In a recent Reuters interview, Isabel Schnabel, a member of the ECB’s executive board, expressed confidence in the central bank’s monetary policy, affirming their commitment to achieving the target inflation rate of 2%. Notably, prior to this interview, Ms. Schnabel was known for her hawkish stance, particularly during the ECB’s interest rate hikes.

The interview began with a significant statement when Ms. Schnabel was asked about her reaction to the recent mild inflation data. In response, she quoted Keynes, saying, ‘When the facts change, I change my mind, what do you do sir?’ Throughout the interview, Ms. Schnabel further elaborated that the ‘inflation developments have been positive,’ and the recent inflation figures have made the prospect of ‘further rate increases rather unlikely.’ She also noted that underlying inflation is now ‘decreasing at a faster pace than initially anticipated.’

Euro Zone’s annual inflation for November dropped to 2.4%, which was below market expectations and a notable decline from October’s 2.9%. Ms. Schnabel’s comments didn’t go unnoticed in the financial markets, as they led to adjustments in forecasts, with expectations of deeper rate cuts in 2024. The latest market projection anticipates more than 140 basis points of rate reductions in the coming year, with the first 25 basis point cut anticipated at the March ECB meeting.

The upcoming US Federal Reserve monetary policy decision scheduled for next week, analysts from the Australia and New Zealand banking group have observed that there may be a potential reduction of 50 basis points or more in the dot plot. They expect that Chair Powell will have to maintain a hawkish stance during this shift towards lower economic growth and inflation, emphasizing the need for patience. Furthermore, they suggest that the long-run estimate for fed funds could see an increase.

GBPUSD Analysis:

GBPUSD is moving in the Box pattern and the market has reached the support area of the Box pattern

The GBP experienced a decline against the USD, and there is a possibility that the Bank of England might consider a rate cut in the first half of 2024, especially if inflation shows more significant signs of cooling. Today, the Bank of England is set to unveil its Financial Stability Report, while the Construction PMI data for November is also scheduled for release.

by the Job Openings and Labor Turnover Survey, declining by 617,000 to 8.733 million in October. This marked the lowest level recorded since March 2021. The focus now shifts to Wednesday’s release of the November ADP job report, which is expected to show an increase of 130,000. Furthermore, the US ISM Services PMI for November exhibited growth, rising to 52.7 from the previous reading of 51.8, surpassing market expectations. This week’s US employment data, including the ADP Employment Change and Nonfarm Payrolls (NFP), will be closely watched as they could provide insights into the potential future interest rate trajectory. However, the prevailing market consensus suggests that the Federal Reserve is likely to maintain its current interest rates during its December meeting next week.

GBPCHF Analysis:

GBPCHF is moving in the Box pattern and the market has rebounded from the support area of the pattern

Turning to the British Pound, market sentiment is leaning toward the possibility of earlier interest rate cuts by the Bank of England. Financial markets have nearly fully priced in the likelihood of the BoE implementing its first rate cut by June 2024.

On Wednesday, the BoE will release its monthly Financial Stability Report, which will offer investors valuable insights into the central bank’s inclination towards a hawkish or dovish stance. Traders will also keep a close eye on the UK S&P Global/CIPS Construction PMI for November, alongside the monthly Financial Stability Report. Additionally, the US ADP private employment and Unit Labor Cost data may provide clear directional cues for the GBPUSD pair.

GBPJPY Analysis:

GBPJPY is moving in the Box pattern and the market has reached the support area of the Box pattern

Ryozo Himino, Deputy Governor of the Bank of Japan, emphasized the need for inflation and wages to rise simultaneously, acknowledging that achieving a sustainable inflation target in Japan would require time. He expressed the view that there is currently no immediate need for changes in the monetary policy settings at the Bank of Japan.

On Wednesday, Bank of Japan Deputy Governor Ryozo Himino emphasized that he does not have a predetermined timetable for exiting the accommodative monetary policy. He expressed the view that it would be inappropriate to establish a predefined sequence for ending various forms of monetary easing. Himino stated that, apart from considering wage and price movements, it is essential to assess factors such as consumption, capital expenditure (capex), and global developments when determining the timing of policy normalization.

He acknowledged that decisions regarding the exit from the easy policy would ultimately be made by evaluating a mixed set of signals emerging from the economy. Himino also mentioned that he is not in a position to provide an exact estimation of how close they are to achieving their price target in a sustainable manner.

Himino acknowledged the possibility that the adverse effects of the easy monetary policy might diminish upon its eventual exit. He pointed to Tokyo’s Consumer Price Index (CPI) data, which indicated a diminishing impact of import price increases.

He further noted that it typically takes more than a year for the effects of monetary policy to fully manifest in the economy. This, in turn, explains the central bank’s patient approach in maintaining its accommodative policy stance. As of now, he does not have a specific prediction regarding when the Bank of Japan can confidently determine the sustained and stable attainment of its price target.

GBPCAD Analysis:

GBPCAD is moving in an Ascending channel and the market has reached the higher low area of the channel

The Bank of Canada is expected to keep its interest rate steady at 5.00% today, primarily due to concerns about the cooling labor market and inflation readings in Canada, which are falling more than anticipated.

The Bank of Canada (BoC) is scheduled to announce its interest rate decision on Wednesday. BoC Governor Tiff Macklem has stated that higher interest rates have cooled down the overheated economy and subdued inflation pressures. While Macklem believes that the central bank may have taken sufficient measures to control inflation, he also indicated that the BoC would consider raising rates again if inflation persists. Market expectations are leaning towards the BoC maintaining the interest rate steady at 5.0% during its December meeting. And Additionally, a rebound in oil prices could provide support to the Canadian Dollar.

AUDCAD Analysis:

AUDCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Australian Q3 GDP data showed a growth rate of 0.20%, which is lower than the 0.40% growth recorded in Q2. However, on an annual basis, there was a 2.1% increase, the same as in Q2, and this exceeded the estimated expansion of 1.80%.

Australia’s economy unexpectedly decelerated in the third quarter, influenced by higher interest rates affecting consumer spending and a shift to negative trade dynamics. The Australian Bureau of Statistics revealed on Wednesday that Australia’s Gross Domestic Product (GDP) grew by a mere 0.2% in the third quarter of 2023, a noticeable drop from the 0.4% growth seen in the second quarter. This figure fell short of the anticipated 0.4% expansion. On an annual basis, the growth rate increased by 2.1%, compared to the 2.1% growth recorded in Q2, surpassing the market’s consensus of a 1.8% expansion.

However, the prevailing risk-averse sentiment and concerns about China’s economic prospects could limit the strength of the Australian Dollar, often viewed as a proxy for China’s economic performance. Moody’s, a credit rating agency, recently downgraded its outlook on China’s sovereign credit rating to negative, citing growing growth-related risks and a crisis in the country’s property sector. Investors will closely monitor key indicators such as the US ADP private employment data and Unit Labor Costs on Wednesday. Additionally, the release of Australia’s Trade Balance on Thursday will be of significant interest to market participants.

NZDUSD Analysis:

NZDUSD is moving in the Box pattern and the market has rebounded from the support area of the Box pattern

The US JOLTS job opening data reported 8.73 million job openings, with a decrease of 617,000 job openings in the month of November. This decline in job openings is seen as a positive development in line with the Federal Reserve’s inflation target. The New Zealand Dollar has been performing strongly against the USD since last week, following China’s stimulus measures aimed at the real estate sector.

The New Zealand Dollar is experiencing a resurgence, thanks to a broad-based retreat of the US Dollar. This recovery is occurring despite sluggish Asian stocks and renewed buying interest in US Treasury bond yields. It follows the recent rebound of the US Dollar, driven by traders adjusting their positions ahead of the forthcoming US ADP Employment Change data, scheduled for release later in the American trading session on Wednesday.

The momentum of the US Dollar’s recovery has temporarily stalled, as financial markets reevaluate their expectations for potential interest rate cuts by the US Federal Reserve. This reassessment comes in the wake of a mixed bag of US economic data released on Tuesday. The Institute for Supply Management reported on Tuesday that its Services PMI bounced back from a five-month low of 51.8 to 52.7 in November. However, the Labor Department’s data revealed that JOLTS Job Openings for the month totaled 8.73 million, marking a decline of 617,000.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/