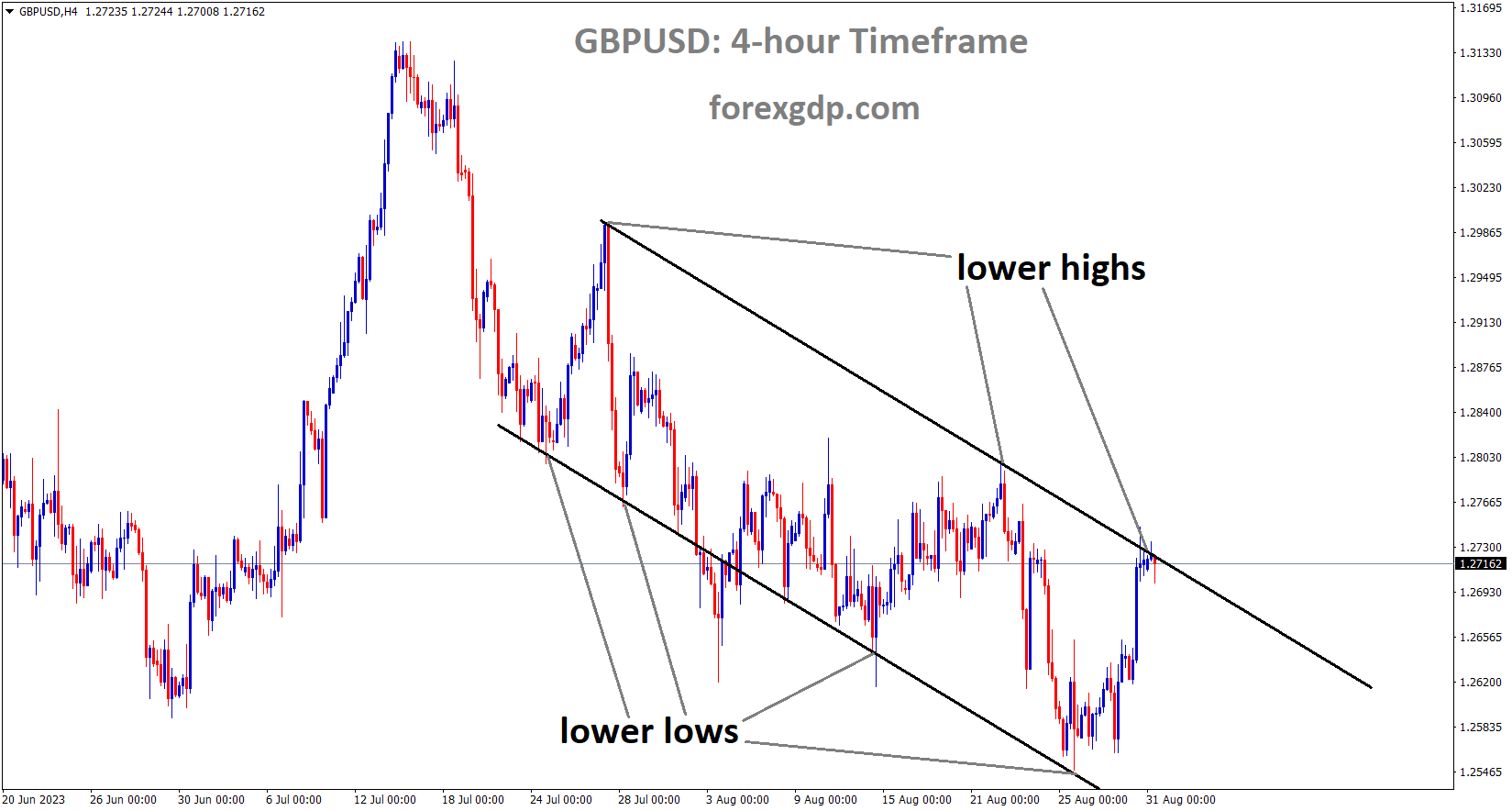

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel

The Bank of England is expected to hike interest rates next month; today’s speech is scheduled to be delivered by BoE Chief Economist Huw Pill. Despite the declining rate of inflation, the GBP is trending stronger than its counterparts.

During the course of Thursday’s Asian session, the GBPUSD pair seesaws between modest gains and slight losses, consolidating its weekly gains over the previous three days. At the moment, spot prices are hovering around 1.2720, essentially unchanged on the day and only a few points below a one-week high that was touched on Wednesday. The 200-day Simple Moving Average SMA, which is technically significant, provides some support for the US dollar USD, which appears to have stopped its recent decline from its highest level since early June. This is therefore considered to be a major factor driving the GBPUSD pair lower, even though the likelihood of additional interest rate hikes by the Bank of England BoE could continue to support the British Pound and encourage traders who are bearish to exercise caution. Deputy Governor Ben Broadbent of the Bank of England stated, during his speech at the Jackson Hole Symposium on Saturday, that policy rates might need to stay in restrictive territory for a while because it is unlikely that the ripple effects of the price increase will subside quickly. Apart from this, the USD may be capped and the decline in the GBPUSD pair may be limited if it is anticipated that the Federal Reserve Fed will halt its rate-hiking cycle in September.

Due to the discouraging US macrodata released on Wednesday, investors appeared to be more certain that the US central bank would moderate its hawkish stance. According to the ADP report, US private sector employers created 177K new jobs in August, a significantly lower number than the downwardly revised 324K reading from the previous month. In addition, the 2.4% initial estimate of the US Q2 GDP growth rate was revised down to a 2.1% annualised pace. The fundamental background mentioned above indicates that the GBPUSD pair is likely headed towards an upside move, but traders are hesitant and are focusing on a speech that BoE Chief Economist Huw Pill is scheduled to give. The Fed’s preferred inflation indicator, the US Core PCE Price Index, will be released later in the early North American session, which will impact the USD price dynamics and present traders with short-term trading opportunities around the pair.

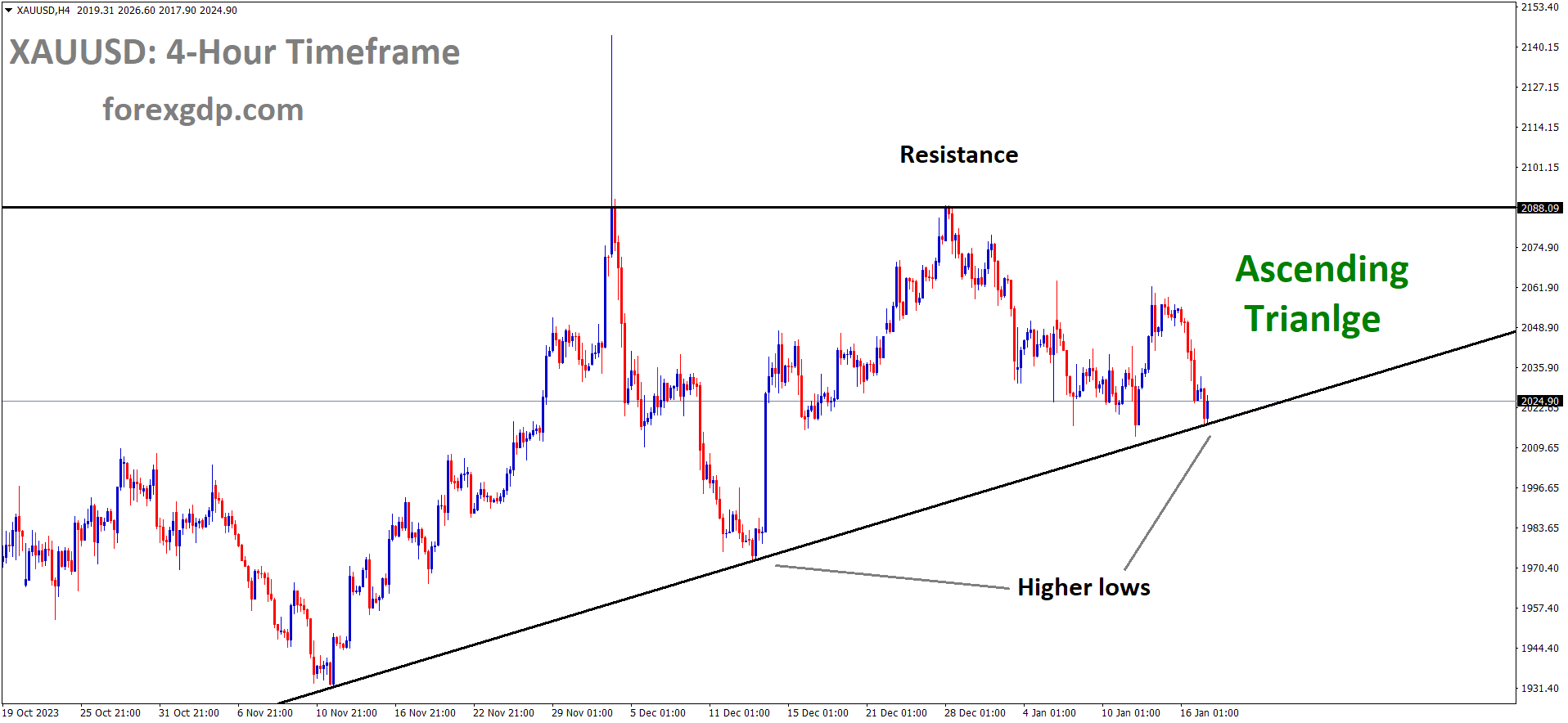

XAUUSD Analysis

XAUUSD Gold Price is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern

Over the past two days, weaker US domestic data has caused gold to soar against the USD. The September meeting’s rate hike is less likely, which makes the USD less strong relative to gold.

For the third day in a row, the XAUUSD pair gained momentum on Wednesday, closing the day in the $1,940 range and displaying gains of almost 1.50% in the bullish trend. Due to the US labour market’s negative data, the US dollar was weak against most of its competitors on Wednesday. This allowed the yellow metal to find demand as US Treasury bond yields decreased. The US reported weaker labour market data on Wednesday as ADP Employment Change increased by 177,000 employed people in the US, lower than the expected 195,000 and the previous 371,000. This came as market participants continued to digest soft July JOLTS Job Openings from Tuesday. It is important to note that Jerome Powell stressed at the Jackson Hole Symposium last week that the tight monetary policy will remain in place until data indicates a cooling trend and the US economy releases weak data that allows Treasury yields to move lower, which hurts the value of the US dollar. Nevertheless, with roughly 0.40% of a daily loss, the US bond yields for 2, 5, and 10-year maturities dropped to 4.88%, 4.26%, and 4.11%, respectively. The drop in Treasury bond yields, which are frequently viewed as the opportunity cost of owning gold, accounts for the XAUUSD advance.

XAGUSD Analysis

XAGUSD Silver Price is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern

According to the CME FedWatch Tool, investors are currently placing bets on increased odds that the Federal Reserve (Fed) will not raise rates at its meeting on 20 September. In contrast, the odds of a hike in November have marginally dropped to 40%. In addition, the US bond yields are under pressure to decline as swaps markets are currently discounting earlier rate cuts in June 2024. These wagers might, however, alter following the release of the August Nonfarm Payrolls on Friday.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Swiss retail sales for the month of July (YoY) increased 1.8% from the previous reading, but ended up -2.2%. After the release, the value of the Swiss franc fell compared to the US dollar.

The USDCHF pair strengthens on Thursday morning during the early European session, trading around 0.8795. After Swiss Real Retail Sales are released, the Swiss Franc loses value in relation to the US Dollar (USD). The weekly Jobless Claims report, which is due later in the North American session, and the US Core Personal Consumption Expenditure Price Index (PCE) will draw the attention of market players. According to the most recent data released on Thursday by the Swiss Federal Statistical Office, the country’s Real Retail Sales YoY for July increased by 1.8% over the previous reading, but ended up at -2.2%.

EURCHF Analysis

EURCHF has broken the Descending channel in upside

With the Euro CPI coming in at 5.1% YoY compared to 5.3% previously, the Euro is losing ground to counter pairs. At the symposium meeting last week, ECB President Christine Lagarde stated that rate hikes will continue until the rate of inflation declines.

President of the European Central Bank (ECB) Christine Lagarde voiced her concerns about inflation at the recent Jackson Hole economic symposium, but she was less directive about the rate path. However, she made it apparent that rates will remain high in order to contain inflation for as long as it takes.

The market will receive the most recent Euro-wide CPI data later today. According to a Bloomberg survey of economists, the headline figure is expected to be 5.1% year over year compared to 5.3% previously. The forecast for the core CPI is 5.3%, down from the previous 5.5%. The German and Spanish CPI figures from yesterday were slightly higher than expected, and this significant miss on forecasts could cause volatility in the Euro.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

In contrast to expectations of 0.20% and a previous reading of 3.4%, NZD building permits came in at -5.2% MoM, which forced the RBNZ to hold interest rates until their next meeting.

In defiance of the prevailing trend, which is supporting the US Dollar’s weakness, NZDUSD extended its day-long reversal from a three-week high to 0.5950 on Thursday morning during the early Asian session. By doing this, the Kiwi pair rationalises negative domestic data and mixed worries about a significant client, China, in the context of a cautious outlook preceding the Fed’s favoured inflation gauge. It is important to note that sellers of the Antipodeans benefitted from the early-week rebound’s inability to surpass May’s low. The Reserve Bank of New Zealand’s RBNZ status quo was supported by a sharp decline in building permits in New Zealand NZ, which had an impact on the NZDUSD pair the day before. Nevertheless, the July NZ Building Permits showed a noteworthy decline of 5.2% MoM compared to 0.2% predicted and 3.4% previous revised from 3.5%. However, China’s response to the US accusations, stating that it is being risky for businesses, dashed earlier expectations of a smooth Sino-American meeting in Beijing. But a number of Chinese banks lowered mortgage rates and supported the expectation of further stimulus from the Asian major, which helped to mend the rift in sentiment outside of New Zealand.

In other news, weaker US data prints supported the Federal Reserve’s Fed call for a policy change and hurt the US currency and Treasury bond yields. Nevertheless, the GDP Price Index also decreased to 2.0% from the first readings of 2.2%, and the US GDP Second Quarter Q2 Annualised fell to 2.1% from the initial projections of 2.4%. Additionally, the Personal Consumption Expenditures PCE Prices preliminary readings decreased marginally from 2.6% to 2.5% in previous estimates for the same period. More significantly, the ADP Employment Change decreased to 177K from 371K prior readings revised from 324K and 195K market estimates. The US Dollar Index DXY fell during these plays for three days in a row, reaching its lowest point in two weeks and recently rounding to 103.15-10. Nevertheless, the benchmark US 10-year Treasury bond yields, which were at 4.11% at the time of writing, are still under pressure and are at their lowest points in three weeks. Next, to keep the NZDUSD traders entertained, the details of China’s official NBS Manufacturing PMI and Non-Manufacturing PMI for August will be combined with New Zealand’s ANZ Activity Outlook and Business Confidence survey for the same month. In spite of the dovish statements regarding the US central bank, the US Core PCE Price Index for August—the Fed’s preferred inflation indicator—will receive significant attention in order to provide clear guidance.

AUDUSD Analysis

AUDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The PMI for China’s NBA Manufacturing is 49.7, up from 49.3 in July. The Non-Manufacturing PMI drops from 51.5 in July to 51.0 in August. Following the mixed data, the Australian dollar is slightly higher.

A brief increase in the value of the Australian dollar relative to the US dollar was accompanied by hints that China’s manufacturing sector might be rebounding. Compared to expectations of 49.4 and 49.3, the China NBS manufacturing PMI increased marginally to 49.7 in August. The non-manufacturing PMI for NBS decreased to 51.0 from 51.1 in July and 51.1 as predicted. Even though the manufacturing sector is still in contraction, the improvement gives hope that the economy is benefiting from the recent stimulus measures. The data released on Thursday is consistent with the less-than-expected macro data from China recently, which have generally been disappointing, as the Economic Surprise Index demonstrates. Although the China Economic Surprise Index has somewhat recovered recently, analysts have downgraded growth estimates for the current year because it is still relatively close to the mid-2020 lows (Covid levels). Australia’s top export market is China, and shifts in the second-biggest economy in the world typically affect the Australian economy.

AUDCHF Analysis

AUDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

In response, Chinese authorities have launched a flurry of focused stimulus programmes in recent weeks, hoping to prop up the flagging post-Covid recovery and a beleaguered real estate industry. But since a significant stimulus programme appears to be off the table due to the potential for causing economic imbalances, general risk sentiment is probably going to drive AUD in the interim.Since recent soft data does not point to a revival in US economic growth, risk appetite has been restrained for the time being, which has capped US yields and put pressure on the US dollar internationally. The moderation of Australian inflation has been overshadowed by the stabilisation of risk sentiment, reducing the need for additional rate hikes by the Reserve Bank of Australia.

CADCHF Analysis

CADCHF is moving in the Box pattern and the market has rebounded from the Support area of the pattern

After US GDP data came in lower than anticipated, oil prices increased and the Canadian dollar strengthened versus the US dollar.

The decline in WTI crude oil, Canada’s principal export, provides support for prices following a three-day losing run. With slight losses at $81.30, WTI crude oil reverses from a two-week high and ends a two-day winning streak. In the midst of conflicting China PMI data and stimulus updates, the black gold thus fails to lift the price-positive weekly inventory from the US and the weaker US Dollar. Earlier in the day, the Non-Manufacturing PMI for China came in at 51.0 compared to 51.5 prior and market forecasts of 51.1, while the country’s official NBS Manufacturing PMI for August increased to 49.7 from 49.4 expected and 49.3 previous readings. The People’s Bank of China PBOC then declared on Thursday that, in an additional attempt to strengthen the private sector economy, it will continue to step up loans to private companies. And It will also be crucial to keep an eye out for any clear signals regarding employment and manufacturing activity in the US and Canada, as well as Canada’s current account balance.

CHFJPY Analysis

CHFJPY is moving in the Box pattern and the market has fallen from the resistance area of the pattern

Member of the Bank of Japan Board Nakamura stated that until demand-driven inflation is achieved, the Bank of Japan will not alter its policy. Wage increases will offset import price increases, ending the deflationary mindset and eliminating the need for negative interest rates.

In a return appearance on the wire on Thursday, Bank of Japan (BoJ) Board member Toyoaki Nakamura stated that the July policy decision “was not part of any exit from ultra-loose policy.” It was timing, not the YCC, that was my objection to its flexibility. The policy change in July is not likely to cause any market turbulence. Because Japan’s inflation is not yet driven by demand, the output gap is still negative. Because of Japan’s economic recovery, the BoJ had to think about removing its negative rate policy. When deciding when to end the negative rate policy, economic developments will probably be closely considered. We will not require YCC if Japan’s economy experiences a long-term recovery, but regrettably, the country’s deflationary mentality has not been completely eradicated. We can get rid of YCC when we feel that Japan’s deflationary mindset has been dispelled, but that time is not yet here. The focus of monetary policy is not on FX. FX changes have a significant effect on prices.

Price and economic effects of Yen movements will be closely monitored by BoJ.Differences in interest rates are not the only factor driving FX. A weaker yen is good for exports and foreign travel, but bad for households and businesses that rely on domestic demand. In my opinion, there is no need to wait until January through March to determine whether Japan’s economy is prepared for a change in BoJ policy. The most crucial thing to watch is whether growth expectations among Japanese firms are rising. Determining whether the circumstances are favourable for the BoJ to normalise monetary policy will probably take some time. Demand-driven inflation is what can be called if unit labour costs increase more and take the place of gains in import prices as the main cause of inflation. This type of inflation is probably sustainable. In order to ascertain whether businesses have been successful in developing a business model that permits consistent wage growth, it is desired to examine a variety of data, such as the government’s quarterly business survey and monthly wage survey. Additionally, Prime Minister (PM) Fumio Kishida of Japan is thought to be considering raising the national minimum wage standard to 1,500 yen per hour by the mid-2030s, according to a report by Japan’s NHK broadcaster.

Japan’s industrial output was 2.0%, lower than the previous reading of 2.4% and the expected 1.4%. Due to China’s economic issues, Japan’s chip exports to the country are declining. Retail sales in China printed at 6.8%, higher than the 5.4% predicted and 5.6% reading from the previous report.

According to Reuters, which was published early on Thursday, Japan’s latest government estimates of industrial production for July indicate that the country is seesawing and expect a fall in activity. In contrast to market expectations of 1.4% and 2.4% in the previous readings, manufacturers surveyed by the Ministry of Economy, Trade, and Industry revealed a 2.0% MoM decline in industrial production for July. It is important to note that the government report also predicts that seasonally adjusted output will rise 2.6% MoM in August (compared to the previous forecast of 1.1%), and 2.4% in September.

Furthermore, July Retail Trade in Japan increased to 6.8% YoY compared to 5.4% predicted and 5.6% prior (revised). An official from the Japanese government stated that the global economic downturn has caused an undershoot risk in factory output for August, based on data and forecasts. The ambassador also mentioned the need for close observation, pointing to a decline in demand in July both domestically and internationally. A government official from Japan also notes the dire prognosis for the equipment used in the production of chips because of the weak demand abroad. The Tokyo-based diplomat continues, Japanese output would be weak unless the Chinese economy recovered.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/