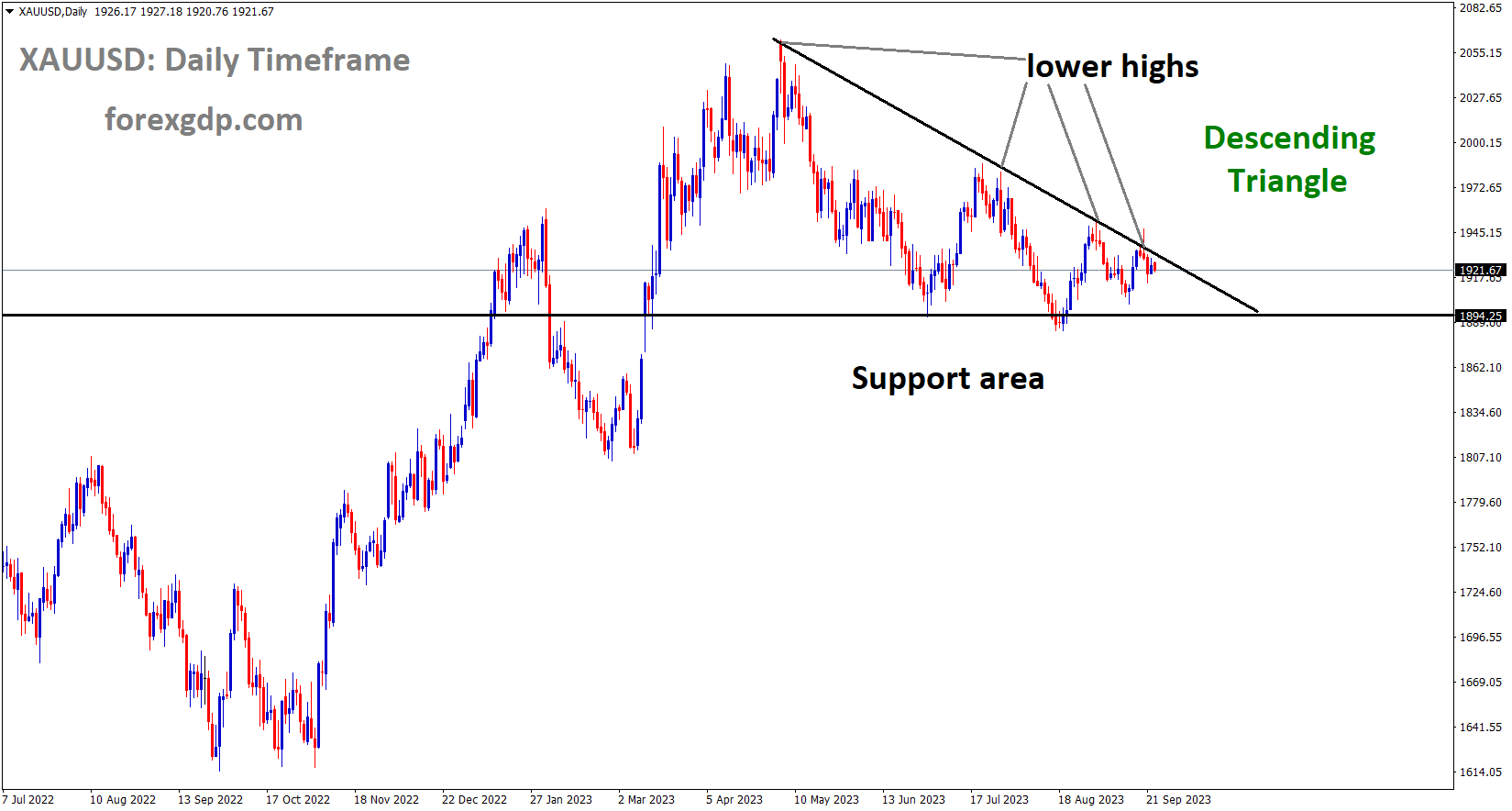

Gold Analysis

XAUUSD Gold price is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern.

Recent drops in gold prices are attributed to the FED’s belief that the US’s longer-term higher interest rates will be maintained. US Q2 GDP and the Core PCE index are scheduled for this week.

The price of gold XAUUSD falls during Monday’s early European session, centred around $1,920. In the meantime, buyers are drawn to the US Dollar Index DXY, which is currently trading close to 105.60, the highest level since March 2023. Nevertheless, the US Dollar’s rise is primarily caused by stories about higher interest rates for longer periods of time, which pulls down the price of gold. Recall that investing in non-yielding assets has a higher opportunity cost when interest rates rise, which suggests a poor outlook for XAUUSD.

Silver Analysis

XAGUSD Silver price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Looking ahead, traders will be closely observing the release of the Core Personal Consumption Expenditure PCE Price Index, the Fed’s preferred measure of consumer inflation, on Friday and the US Gross Domestic Product GDP Annualised for the second quarter on Thursday. The yearly percentage is anticipated to decrease from 4.2% to 3.9%. Market participants will identify a clear direction for XAUUSD by taking cues from these numbers.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has reached the higher high area of the channel

Because of the lower-than-expected inflation, the Swiss Franc saw weakness against its counterparts following the SNB’s decision to cut interest rates last week. Following five increases in a row, the Swiss Franc’s vulnerability against counter pairs is revealed by its first pause.

The additional policy tightening by the Federal Reserve Fed helps the US Dollar USD maintain its strength close to a six-month high, which is viewed as a major driver supporting the USDCHF pair. Actually, last week the US central bank cautioned that at least one more interest rate hike by the end of this year was likely due to persistently sticky inflation, reinforcing the longer-for-higher narrative. Furthermore, the ‘dot-lot’ predicted only two rate cuts in 2024 as opposed to the four previously predicted. As a result, the US fixed-income market saw a prolonged selloff, which caused the yield on the rate-sensitive two-year government bond to rise to its highest point since 2007. The dollar and USDCHF pair are supported by the benchmark 10-year US Treasury yield, which is standing tall close to a 16-year peak.

However, the fact that the Swiss National Bank SNB ended its run of five straight increases last week continues to be a burden on the Swiss Franc CHF. At the conclusion of the quarterly monetary policy meeting, the SNB decided to hold onto its benchmark interest rate, defying expectations that it would hike by 25 basis points in response to sub-2% inflation readings and the recent weak economic data. This, along with acceptance above the crucial 200-day SMA, raises the possibility that the USDCHF pair’s well-established uptrend, which has been in place for the last two months or so, will continue. The US bond yields will be crucial in determining the dynamics of the USD price and giving the USDCHF pair some momentum on Monday if there are no significant market-moving economic releases from the US.

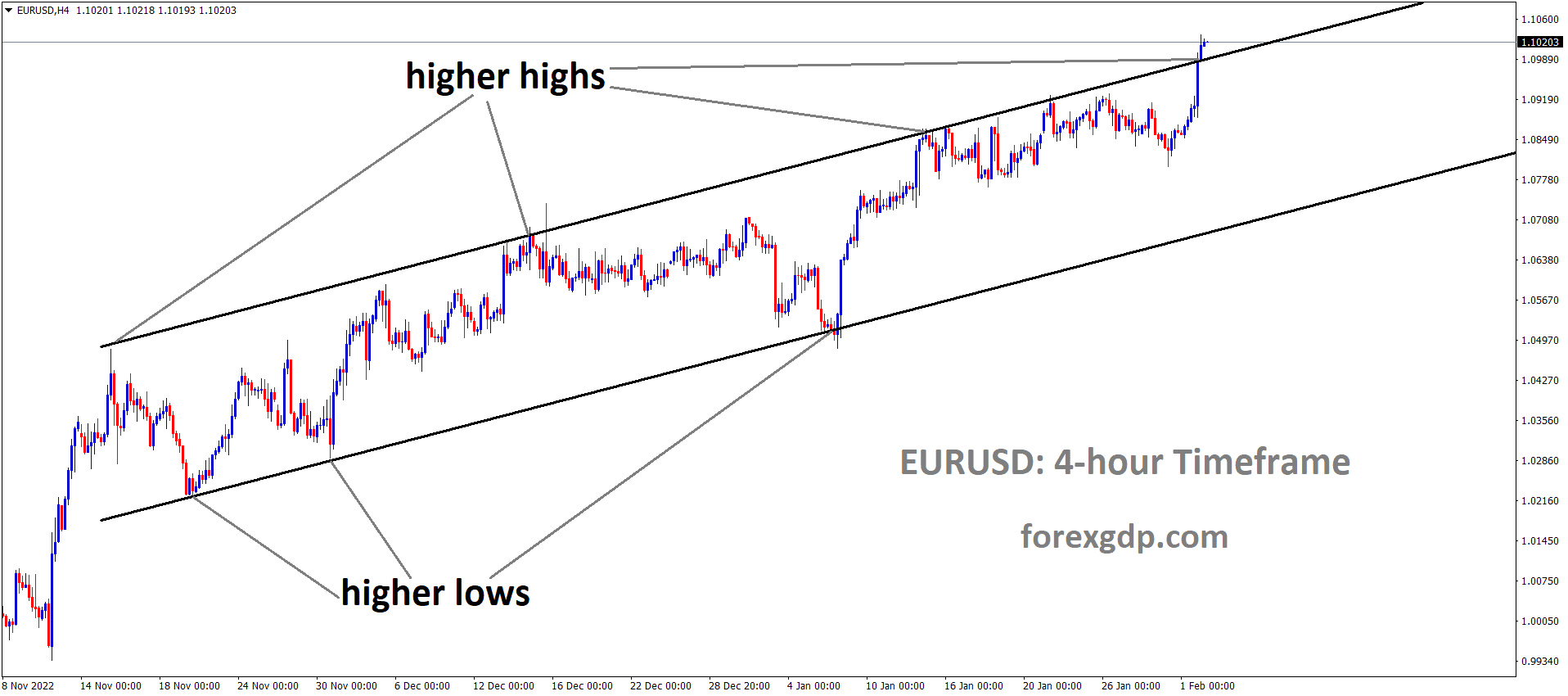

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has reached the lower low area of the channel

Rate increases are being done gradually, according to ECB Governing Council member Villeroy, with the current rate hike at 4.00% marking the peak rate. Inflation is expected to decline to 2% by 2025.

President of the Minneapolis Federal Reserve Neel Kashkari stated that US consumer spending is rising and the country’s economy is expanding quickly. Although we raised rates by 5.00 to 5.25%, there was little effect on consumer spending.

Francois Villeroy de Galhau, the president of the Bank of France and a member of the European Central Bank’s (ECB) Governing Council, stated in a weekend interview that he is not in a rush to raise rates further after doing so to 4.00% last week, according to Bloomberg. Patience is more important than further rate increases in today’s world. Very attentive to oil but it does not put into doubt the underlying disinflation, Our goal and plan is to raise inflation to about 2% by 2025.

Despite steep interest rate increases from the US central bank, consumer spending in the US has continued to outpace expectations that it would contract. President of the Minneapolis Federal Reserve Neel Kashkari stated on Friday, according to Reuters. I would have assumed that we would have put a stop to consumer spending with 500 basis points or 525 basis points of interest rate increases, but instead, spending has continued to rise and surpass expectations.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lower low area of the channel

The Bank of England held rates at 5.25% last week, which is the same level as it has been since November 2021. Retail sales decreased last month, and the CPI was lowered for the third straight month. More people in the UK are worried about the recession as a result of the ongoing rate hikes.

The British Pound’s already finite appeal is rapidly running out, and its lengthy decline appears likely to continue into a new trading week. What is most concerning is that Sterling no longer has as much dependable interest-rate support. On September 21, the Bank of England decided to maintain the base rate at 5.25%, which was the first meeting of the Monetary Policy Committee without an increase in borrowing costs since November 2021.

This choice was made in the wake of August’s news that consumer price inflation had slowed for a third straight month, defying predictions that it would rise once more. In light of the most recent economic data, which it will have access to before the markets, the Bank of England’s call appeared to be entirely warranted. The official figures for retail sales last month indicate a decline. On the year when the markets had anticipated a comparable increase, they dropped 1.4%. The more optimistic Purchasing Managers Index series for this month revealed that every sector of the economy was firmly in contractionary territory, which is at least as concerning.

GBPCHF Analysis

GBPCHF is moving in the Box pattern and the market has rebounded from the support area of the pattern

The United Kingdom faces the ominous threat of recession, which seemed far away earlier in the year when the nation unexpectedly outperformed some of its European counterparts. The MPC has appropriately revised down its own economic projection, estimating that the third quarter of 2023 will see a 0.1% increase in GDP. That represents a decrease from the already weak August forecast of 0.4%. It will be fortunate to receive even that on the current show. There will not be much first-tier data available in the upcoming week, so sterling will likely be left to stew in its own bad juice. September 29 is the date of the final official examination of the second-quarter GDP data, but it is probably going to turn out to be far too historic at this point to have much of an impact on the market. In any event, the market is only anticipating a slight 0.2% quarterly increase.

Bulls in the pound will hold onto the hope that markets undervalue the possibility that local interest rates may still need to rise in order to control inflation; after all, UK consumer price increases continue to be the highest of all the major developed economies at 6.7%. However, that thesis will take time to develop, if it does so at all, so this week’s call for the Pound has got to be bearish. The currency’s evolving base case is that rates will probably stay where they are for a while but probably will not rise further. Although the governor’s casting vote was needed to break a 4/4 deadlock between holding and raising rates, the BoE’s rate setters remained sharply divided.

GBPJPY Analysis

GBPJPY has broken the Descending triangle pattern in downside

The Bank of Japan maintained its rate of 0%, which contributed to the JPY Yen’s continued weakness against counter pairs. Japan differs from other central banks in that it does not adopt a hawkish stance. Analysts predict that Bank of Japan lifting will become feasible when other banks’ lifting slows.

Monetary easing will continue until a 2% inflation rate is reached, according to Shinichi Uchida, deputy governor of the Bank of Japan, providing stable and sustainable wage growth.

Deputy Governor Shinichi Uchida of the Bank of Japan BoJ stated on Monday that the institution needs to patiently continue monetary easing. Must monitor changes in the currency market closely. The goal of the July yield target decision was to respond to upside and downside risks in a flexible manner. 2% inflation target to be met in a stable and sustainable manner while maintaining wage growth. There is no indication that the 2% inflation target will be met in the near future.

The Bank of Japan BOJ maintained the status quo at its meeting last week, reinforcing the Japanese yen’s current weakness. Following the Bank of Japan’s BOJ expected decision to maintain its ultra-loose policy settings at its meeting on Friday, JPY gave up some of its gains. Compare this to its peers, where central banks maintain a hawkish monetary policy, and BOJ’s ongoing ultra-easy monetary policy. Furthermore, there is no longer a significant relative growth advantage that could cause the JPY to materially appreciate because the outlook for growth has converged. This means that the yen’s path of least resistance will continue to be sideways to downward unless the global central bank eases up on its hawkishness or the BOJ increases its hawkishness.

CADCHF Analysis

CADCHF is moving in the Descending channel and the market has reached the lower high area of the pattern

The Canadian dollar gained strength against counter pairs last Friday when retail sales data was released from Canada. The reading increased by 0.30% from the previous reading of 0.10%. The upward trend in the Canadian dollar is supported by oil prices.

Friday, Statistics Canada reported that July’s Canadian Retail Sales increased by 0.3% over the previous reading of 0.1%, which was less than the 0.4% market expectation. In contrast, Core Retail Sales increased 1.0% from a 0.7% decline in the prior reading, exceeding the 0.5% market estimate. Furthermore, since Canada is the top oil exporter to the US, a surge in oil prices supports the commodity-linked Loonie.

AUDUSD Analysis

AUDUSD is moving in the Box pattern and the market has fallen from the resistance area of the pattern

Australian manufacturing PMI data was 48.2 from 49.6 in the previous reading, and services PMI data was 50.5 from 47.8 in August. The previous reading of 48.0 was replaced by 50.2 for the composite index. Australia’s currency is consolidating as a result of the approaching pause in the RBA rate hike.

The Australian dollar fell against the US dollar on Monday during the Asian session, retracing the gains from the previous session. Nonetheless, the soft US Dollar USD and the release of Australian PMI data on Friday provided upward support for the pair. On Friday, Australia’s PMI data showed a slight improvement. September’s preliminary S&P Global Services PMI was 50.5, up from August’s 47.8. The Manufacturing PMI, however, fell from 49.6 to 48.2 in the preceding reading. The Composite Index improved as well, going from 48.0 to 50.2 previously. The case for maintaining the current policy was stronger, according to the Reserve Bank of Australia’s RBA minutes from the September monetary policy meeting, even though further tightening might be necessary if inflation persists. Moreover, the overall economic outlook has not changed significantly in response to recent economic data. It is possible that the RBA’s dovish attitude is hurting the Australian pair. Also, later this week, traders will be watching Australia’s Retail Sales data and Monthly Consumer Price Index CPI. As of this writing, the US Dollar Index DXY, which compares the value of the US dollar to six major currencies, is trading at about 105.60. The index is having difficulty gaining momentum, which may be related to market caution prior to the release of US economic data.

The US economic calendar, which includes important data releases like Consumer Confidence, Durable Goods Orders, Initial Jobless Claims, and the Core PCE, the Fed’s preferred inflation indicator, will be closely watched by investors. It is anticipated that Core PCE will drop from 4.2% to 3.9% annually. These datasets will offer perceptions into the inflationary pressure and US economic conditions, which will impact the AUDUSD pair’s trading choices. But as of the time of publication, the yield on the US Treasury note maturing in 10 years had increased to 4.46%, a 0.63% increase. It is possible that the rising yields are helping the US dollar. Additionally, remarks made by US Federal Reserve Fed Governor Michelle W. Bowman and Boston Fed President Susan Collins emphasise the need for patience and more rate hikes to control inflation, suggesting that further interest rate tightening may be necessary. Pressure on the AUDUSD pair could come from rising interest rates. There will likely be at least one more rate hike of 25 basis points by the end of the year due to the Federal Reserve’s commitment to keeping interest rates higher for an extended period of time in order to bring inflation back to its target of 2%.

NZDUSD Analysis

NZDUSD is moving in the Box pattern and the market has fallen from the resistance area of the pattern

New Zealand data for the month of September is unexpectedly positive; the trade balance for the month of August increased to $15.54 billion from the previous reading of $15.88 billion. The NZD Dollar is consolidating versus counter pairs, and by the end of 2023, the RBNZ is anticipated to hike interest rates once more.

The yield on a US 10-year bond, however, reversed the recent declines and was now 4.45%, up 0.32% as of the time of publication. It seems that the New Zealand economy is more resilient than first thought, and the September domestic data underscores the need for additional tightening of monetary policy. Therefore, it appears that the markets have factored in the Reserve Bank of New Zealand’s RBNZ increase in the Official Cash Rate OCR through the end of 2023. According to the economic data released on Friday, the annual trade deficit decreased from $1588 billion to $15.54 billion in August thanks to the Trade Balance NZD. However, the Westpac Consumer Survey Q3 report revealed a downturn in the outlook for the economy, with the index dropping from 83.1 to 80.2. However, statistics from S&P Global show that in September, business activity in the US remained essentially unchanged. The S&P Global Manufacturing PMI increased from 47.9 to 48.9 in the previous month, above the predicted 48.0 readings.

In the meantime, the Services PMI fell from 50.5 in July to 50.2, below the predicted growth rate of 50.6. Although it was less than August’s 50.2 level, the Composite reading, which offers a broad picture of business activity, was in line with estimates at 50.1. The US Dollar Index DXY, which compares the value of the US dollar to other major world currencies, has difficulty gaining traction. At the time of writing, the spot price is better than roughly 105.50. Furthermore, Boston Fed President Susan Collins acknowledged the need for patience while acknowledging that additional tightening is a possibility. More rate hikes are required to control inflation, according to Michelle W. Bowman, the governor who sits on the board of the Federal Reserve. In order to return inflation to its target of 2%, the Federal Reserve Fed has underlined the significance of keeping interest rates higher for a prolonged amount of time. Because of this position, the market is now more likely to see at least one more rate increase of 25 basis points before the year is out.

Furthermore, the Fed’s dot plot now shows only two rate hikes in 2024, as opposed to the previous estimate of four. The US economic calendar for the coming week will feature important data releases like the Core PCE, the Fed’s preferred inflation indicator, Initial Jobless Claims, Durable Goods Orders, and Consumer Confidence. Data on business and consumer confidence will be included in the Kiwi docket’s economic indicators. Market players will be keeping a close eye on these announcements in order to gain insight into the state of the economies in both nations.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/