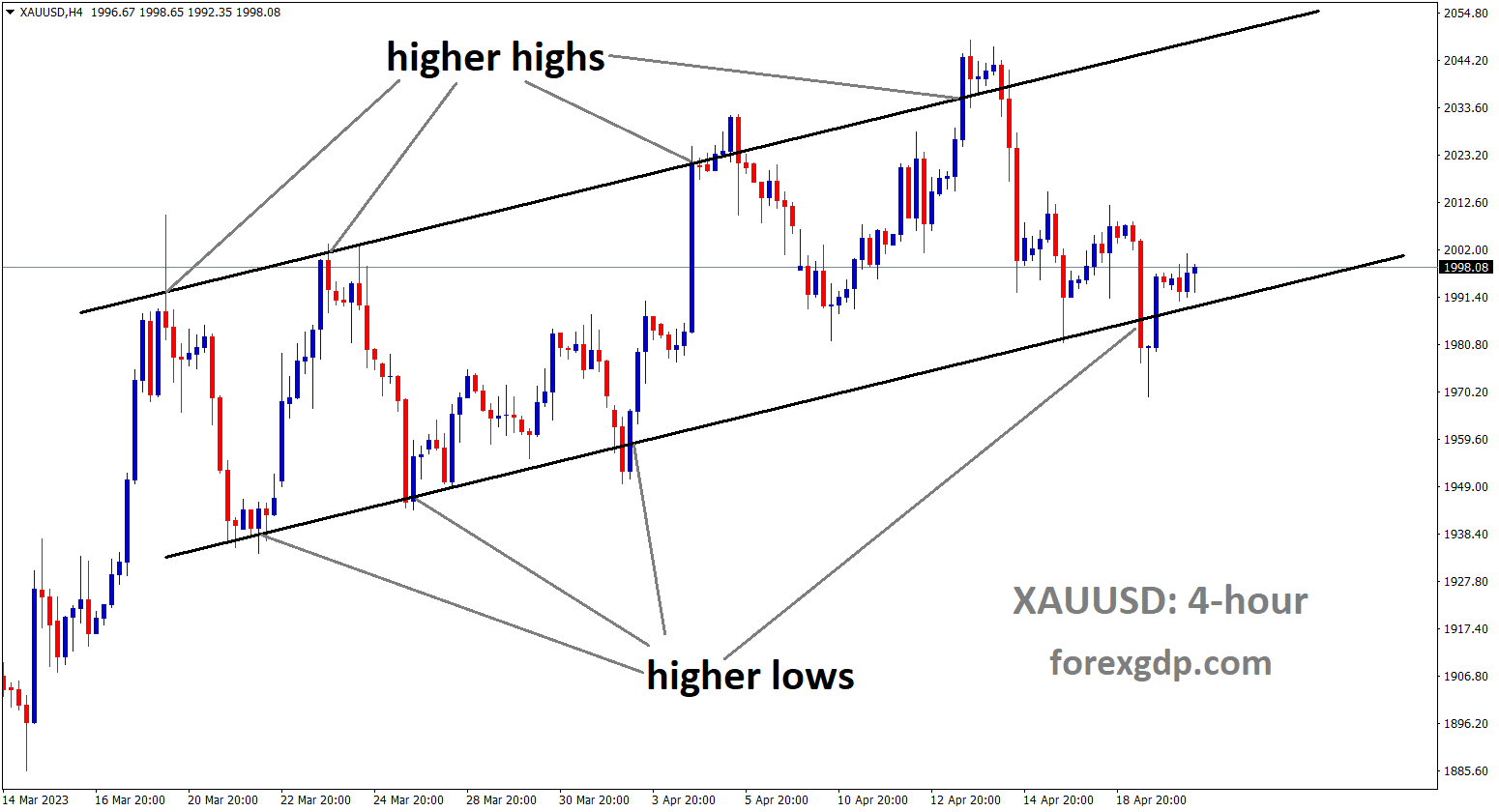

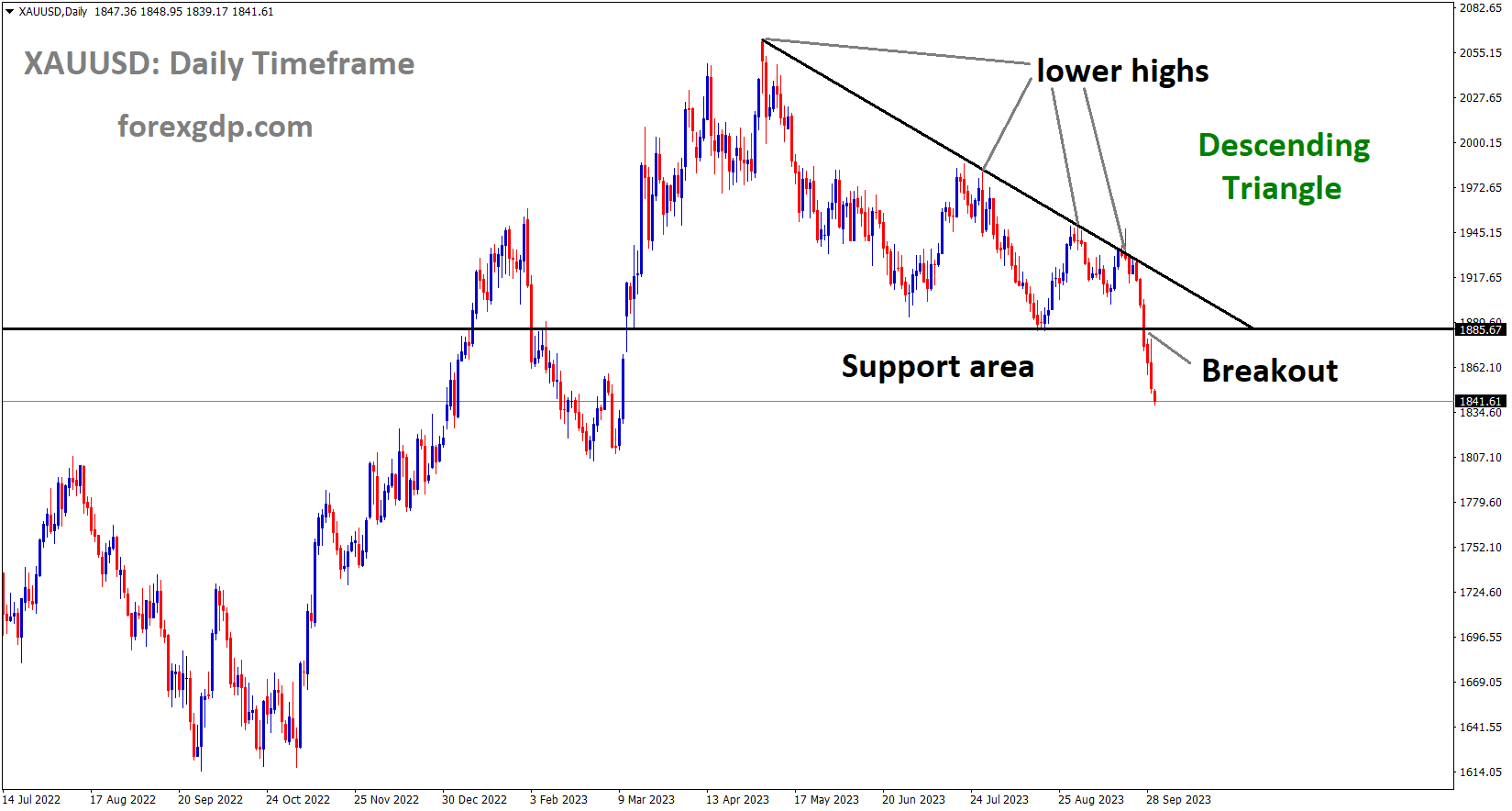

Gold Analysis

XAUUSD Gold price has broken the Descending triangle pattern in downside

Without a doubt, US tightening measures have caused a decline in gold prices. Increasing interest rates and rising US Treasury yields are concerning gold buyers.

The price of gold finished September down more than 4.5% and lower for the second consecutive quarter on Friday, with significant losses. Additionally, the yellow metal saw its largest weekly loss in over two years and is still being weighed down by the growing consensus that the Federal Reserve (Fed) will maintain higher interest rates for an extended period of time. The possibility of one more rate hike by year’s end was hinted at by the US central bank, and this is thought to be a major factor driving flows out of the non-yielding commodity. Following the release of the US Personal Consumption Expenditures (PCE) Price Index on Friday, the price of gold did experience some respite, but the increase was short-lived. The information does not significantly alter the expectation that the Fed will continue to tighten monetary policy. Meanwhile, the outlook pushes US Treasury bond yields higher on Monday, dragging the non-yielding yellow metal down to its lowest level since March 10 ahead of the early European session. This is the sixth straight day of such a move.

In addition to hawkish Fed projections, the risk-on tendency is thought to be another element weakening the price of safe-haven gold. Investors’ appetite for riskier assets is increased by slightly better-than-expected official Chinese PMIs and the passing of a temporary US government funding bill over the weekend. Nevertheless, the oversold Relative Strength Index (RSI) on the daily chart and a slight decline in the US Dollar prevent bearish traders from making new bets around the XAUUSD and lessen the bearish pressure. Still, for the ninth day out of the last ten, the price of gold is down. Furthermore, the underlying context implies that the precious metal’s least resistance is to the downside. Because of this, any significant rebound attempt may still be viewed as a selling opportunity and be limited ahead of significant US macro data that is scheduled for the start of a new month. Monday’s release of the US ISM Manufacturing PMI promises to be a busy week, but the US NFP report on Friday will still be the main attraction.

Investors appear to be certain that the Fed will maintain its aggressive stance and raise interest rates for an extended period of time. In keeping with expectations, the US PCE Price Index increased by 3.5% during the course of the previous 12 months through August. The Fed’s preferred inflation indicator, the annual Core PCE Price Index, decreased from 4.3% in July to 3.9%. In the meantime, rising consumer spending and skyrocketing petrol prices indicate future price increases. A hawkish outlook from the Fed undermines the metal and keeps the yield on the US 10-year Treasury at a 16-year high. The manufacturing sector experienced growth in business activity for the first time in six months, according to the official Chinese PMIs. To prevent a 45-day government shutdown, the US Congress approved a stopgap funding bill on Sunday. Now, traders are waiting for a new boost from the US ISM Manufacturing PMI, which is predicted to register at 47.9 in September. It is possible that investors will not be making any new directional bets before Friday’s highly anticipated US NFP report.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher high area of the channel

In an effort to lower JGB yields, the Bank of Japan declared that it would buy JGBs. Every basis point has been added to the 10-year JGB rate since September of last year.

Governor of the Bank of Japan, Ueda, stated that rate hikes will take time to materialise and that inflation will fall to the target of 2.0%. The market became more vulnerable to JPY weakness as the Bank of Japan stopped taking action.

The Bank of Japan declared that it would be buying Japanese government bonds on an ad hoc basis in an attempt to moderate the continuous yield surge. Following a 1 basis point increase in early Asia, the benchmark 10-year JGB yield hit 0.775%, its highest level since September of last year.

The USDJPY pair is trading around 149.70, having fallen from 11-month highs of 149.82 in the early European trading session on Monday. The resurrected US Dollar USD boosts the major pair ahead of the US ISM PMI, which is due later on Monday. However, traders may become cautious in the face of potential FX intervention by Japanese authorities. The stronger demand for longer narratives in the United States boosts the Greenback broadly. Meanwhile, the US Dollar Index DXY, which measures the value of the US dollar relative to a basket of foreign currencies, resumes its upward trend, climbing to 106.28, its highest level since November of last year. The Federal Reserve Fed Bank of New York President John Williams stated on Friday that the central bank is at or nearing the peak for the federal funds rate and that the Fed will need a restrictive policy stance for some time to achieve its goals, while the Fed Bank of Richmond President Thomas Barkin stated that the central bank’s holding steady at the September FOMC meeting was appropriate and that the Fed has time to see data before deciding what is next for rates. The Personal Consumption Expenditures PCE Price Index increased 3.5% year on year in August, up from 3.4% in July, according to data released on Friday. Meanwhile, the annual Core PCE Price Index, the Fed’s preferred inflation indicator, rose 3.9% from 4.3% in July, as expected.

The PCE Price Index and the Core PCE Price Index increased 0.4% and 0.1% month on month, respectively. Both of these figures fell short of the expectations of experts. Furthermore, Personal Income and Personal Spending both increased by 0.4% on a monthly basis, as expected. Market participants will be looking for cues from Fed Chair Jerome Powell’s speech later in the American session on Monday. Officials’ hawkish comments may boost the US Dollar USD and act as a tailwind for the USDJPY pair. However, the possibility of Japanese FX intervention may warn traders away from bullish bets as the pair trades near the 150.00 level, a psychological round mark and the zone where the BoJ intervened in the market last year. Japanese Finance Minister Shunichi Suzuki continued his verbal intervention early Monday. Suzuki stated that he was cautiously watching currency movements. On Saturday, Bank of Japan Governor Kazuo Ueda stated that the country still has a long way to go before exiting its ultra-easy monetary policy. According to the BoJ Summary of Opinions at the Monetary Policy Meeting on September 21 and 22, the BOJ stated that they do not need to make additional changes to YCC because long-term rates are moving fairly steadily and that the end of negative rates must be linked to the achievement of the 2% inflation target. Market participants will be watching the US ISM Manufacturing PMI for September, which is due on Monday, as well as Fed Chair Powell’s speech. On Wednesday, the US ADP Employment Change and ISM Services PMI for September will be released. On Friday, the focus will shift to the US Nonfarm Payrolls. These events could give the USDJPY pair a clear direction.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Retail trade turnover fell by 0.20% year on year in August, following a 0.40% increase the previous month. The Swiss franc fell slightly after the news release.

Retail trade turnover in Switzerland fell 0.2% year on year in nominal terms in August, while seasonally adjusted nominal turnover increased 0.4% compared to the previous month, according to a preliminary report released on Monday by the country’s Federal Statistical Office. Real retail trade turnover was down 1.8% in August compared to the same month a year ago, while seasonally adjusted real retail sales increased by 0.4%.

In nominal terms, turnover in the Swiss retail sector excluding service stations increased 0.4% year on year and 0.3% month on month. Nominal turnover in retail sales of food, beverages, and tobacco increased by 2.1% year on year and by 0.9% month on month. The nominal turnover of the non-food sector fell 1.0% from August 2022 to July 2023, but increased 0.1% from July 2023 to August 2023.

EURUSD Analysis

EURUSD is moving in the Box pattern and the market has rebounded from the support area of the pattern

Congress passed legislation to fund US government spending until November 17. This information contributed to the avoidance of a government shutdown in the United States. The main issue is that Ukraine’s support and border tightening measures are preventing the Senate from passing spending bills.

Congress passed legislation funding the US federal government until November 17. According to Commerzbank economists, a government shutdown could still occur after November 17. The feared October 1 government shutdown is off the table for the time being, thanks to last-minute interim funding passed by Congress. This, however, will only last until November 17. Congress must pass either regular budget legislation or another stopgap funding measure by mid-November. However, congressional positions on the level of government spending, as well as issues such as Ukraine aid and border security, remain diametrically opposed. As a result, the 22nd government shutdown since 1976 looms.

EURCHF Analysis

EURCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel

Rate cuts, according to ECB Vice President Luis De Guindos, will not reduce inflation. In my opinion, lowering inflation is more difficult than usual.

In a Financial Times interview on Monday, European Central Bank (ECB) Vice President Luis de Guindos dismissed rate cuts and said that getting back to the 2% target of inflation will not be easy. He went on to say that the last mile of disinflation is the hardest.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The Bank of England will raise or lower interest rates at its next meeting based on inflation readings. Interest rate freezes cause GBP weakness against counter pairs.

During the early European session on Monday, the GBPUSD pair remains on the defensive below the 1.2200 barrier and trades in negative territory for the fifth consecutive week. The major pair is trading near 1.2180, down 0.16% on the day. On Friday, the US Bureau of Economic Analysis reported that the Personal Consumption Expenditures (PCE) Price Index increased 3.5% year on year in August, up from 3.4% in July, meeting market expectations. Meanwhile, the annual Core PCE Price Index, the Fed’s preferred inflation indicator, rose 3.9% from 4.3% in July, as expected. The PCE Price Index and the Core PCE Price Index increased 0.4% and 0.1% month on month, respectively. Both of these figures fell short of the expectations of experts. Furthermore, Personal Income and Personal Spending both increased by 0.4% on a monthly basis, as expected. On Friday, Federal Reserve (Fed) Bank of New York President John Williams stated that the central bank is at or nearing the peak for the federal funds rate, while also stating that the Fed will need to maintain a restrictive policy stance for some time to achieve its goals. Fed Bank of Richmond President Thomas Barkin stated that the central bank’s decision to hold rates steady at the September FOMC meeting was appropriate, and that the Fed has time to review data before deciding what to do with rates.

Market participants will, however, take cues from Fed Chair Jerome Powell’s speech later in the American session on Monday. Officials’ hawkish comments could boost the US Dollar (USD) and act as a headwind for the GBPUSD pair. On the GBP front, after the BoE decided to halt its rate-hiking cycle earlier this month, policymakers stated that the central bank could raise or halt interest rates if necessary. However, the market expects the Bank of England (BoE) to maintain its monetary policy at the next meeting, putting pressure on the British Pound (GBP). In the absence of UK economic data this week, the GBPUSD pair remains at the mercy of USD price dynamics. On Monday, the US ISM Manufacturing PMI for September will be released, followed by a speech by Fed Chair Powell. On Wednesday, the US ADP Employment Change and ISM Services PMI for September will be released. On Friday, the focus will shift to the US Nonfarm Payrolls.

GBPCAD Analysis

GBPCAD has broken the Descending channel in upside

The Canadian Dollar is falling as a result of the disappointing GDP reading of 0.0% in July, compared to the 0.10% expected. This is slightly higher than the 0.20% contraction in June.

The Canadian dollar was under pressure due to disappointing July GDP data, which came in flat at 0.0% versus market expectations of 0.1% growth.

In June, the GDP contracted by 0.2%. Crude oil prices fell from one-year highs in the previous week’s last two trading sessions, owing to market uncertainty about the Fed’s interest rate policy.

Crude Oil Analysis

Crude Oil price is moving in an Ascending channel and the market has reached the higher low area of the channel

Because Canada is the largest oil exporter to the United States, this development weakened the Canadian Dollar against the Greenback. However, the US crude oil benchmark, Western Texas Intermediate, is attempting to end its losing streak on Monday, trading around $90.10 per barrel.

AUDUSD Analysis

AUDUSD is moving in the Box pattern and the market has fallen from the resistance area of the pattern

The Australian dollar is falling ahead of the RBA’s interest rate decision tomorrow. Many economists believe the RBA will make an interest rate decision tomorrow; CPI is expected to fall in September compared to August.

On Monday, the Australian Dollar AUD ends its three-day winning streak. The AUD/USD pair gained ground, aided primarily by positive Chinese PMI data released over the weekend. However, the US Dollar USD has remained resilient in the aftermath of Friday’s moderate economic data. According to Australia’s TD Securities Inflation YoY data, inflation expectations in September were lower than in August. In its upcoming policy meeting on Tuesday, the Reserve Bank of Australia RBA is expected to keep interest rates unchanged. However, the Consumer Price Index CPI in Australia improved in August compared to July, which could be attributed to rising energy prices. Inflationary pressures may influence the RBA’s policy decision. The US Dollar Index DXY maintains its gains in the second trading session following moderate data from the United States US. Core Personal Consumption Expenditures PCE – Price Index YoY increased in August, as expected, but at a lower rate than in July.

In comparison to the market consensus, US Core PCE MoM showed a soft reading. While the Michigan Consumer Sentiment Index Sep rose from previous levels. Furthermore, the USD’s strength is attributed to the performance of US Treasury yields. The 10-year US Treasury note yield is hovering near record lows. The Australian Dollar may face additional challenges as market participants become more concerned about the US Federal Reserve’s Fed interest rate trajectory. The AUDUSD falls as the RBA is expected to maintain current interest rates at 4.1% at its policy meeting on Tuesday. In September, Australia’s TD Securities Inflation YoY rose 5.7%, down from 6.1% in August. Australia’s Monthly Consumer Price Index CPI rose 5.2% year on year in August, as expected, up from 4.9% previously. The Manufacturing PMI in China has risen into positive territory. China’s NBS Manufacturing PMI increased to 50.2 in August, up from 49.7 in July, exceeding the 50.0 forecast.

Furthermore, the Non-Manufacturing PMI increased to 51.7 from 51.0 in the previous reading, exceeding the market consensus of 51.5. Positive US Treasury Yields are supporting the USD’s strength. The US Core PCE – Price Index YoY rose 3.9% in August, as expected, easing from the previous reading of 4.3%. Core PCE MoM showed a soft reading of 0.1% versus the market consensus of 0.2%. The US Michigan Consumer Sentiment Index Sep increased to 68.1 from 67.7, which was expected to remain unchanged. Following the Friday session, bills to avert a government shutdown were successfully passed in the United States, securing funding until November 17. The US Dollar Index USD has resumed its upward trend as a result of this development. Traders are anticipating the September US ISM Manufacturing PMI ahead of Fed Chair Jerome Powell’s speech on Monday. The RBA’s interest rate decision is scheduled for Tuesday.

NZDUSD Analysis

NZDUSD is moving in the Box pattern and the market has reached the resistance area of the pattern

In comparison to counter pairs, the Kiwi pair tends to be weaker ahead of this week’s RBNZ interest rate decision. As anticipated by most analysts, the rate hold causes Kiwi tone losses versus counter pairs.

Although the quarter-end rebalancing may have increased volatility, recent moves have been largely centred around the USD, and it is unlikely that this will change much as we approach year-end and this week’s batch of important US data.

However, the RBNZ will also be discussed this week. If we see a more hawkish tone, we believe the Kiwi will benefit more, but that might only help it maintain parity with the USD rather than overcome its strength.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/